CA - Hidden Assets And Improved Cash Flow Make Rogers Communications A Buy

2023-10-11 05:09:26 ET

Summary

- Rogers Communications is an underappreciated stock due to a lack of interest in yield-paying assets, family boardroom drama, and an uncertain outlook after a big acquisition.

- The company's recent acquisition of Shaw Communications has expanded its wireline footprint and increased its subscriber base, which should translate into much higher earnings.

- Rogers' ownership stake in various sports teams are hidden assets that provide additional value to investors.

Rogers Communications ( RCI.B:CA )( RCI ) is an underappreciated stock due to a lack of interest in yield-paying assets, family boardroom drama, and an uncertain outlook after a big acquisition. But once these storm clouds clear, there's nice upside potential.

(All figures are in CAD unless indicated otherwise)

Introduction

Rogers Communications is Canada's third-largest telecommunications company by market cap, only surpassed by rivals BCE and TELUS . The company's operations include wireless phone service, wireline cable, internet, and home phone service, and a media division that owns some of Canada's top television channels, as well as ownership stakes in various sports teams.

Starting with the wireless business, Rogers has long been a leader in Canadian wireless service . It boasts more than 11M customers and generated $9.2B in revenue in 2022. Rogers is the 100% owner of its wireless network, while rivals BCE and TELUS share certain parts of their networks .

Rogers' wireline business has traditionally been focused in Eastern Canada, specifically Ontario, where it has fought BCE for market share. The company recently acquired Shaw Communications, which expanded its wireline footprint into Western Canada, notably in higher-growth provinces like B.C. and Alberta. Now that the acquisition has closed, Rogers' wireline service territory covers approximately 9.8M homes with more than 4M subscribers.

Finally, the company is also the owner of various media assets, including television channels, radio stations, and sports franchises. Assets in television include Citytv, OMNI Television, FX, and Sportsnet. It also owns 55 radio stations , spread among major markets across the country. Included in these radio assets are some of Canada's top podcasts.

The more interesting part of the media business is Rogers' ownership stake in various sports teams. Rogers and BCE each own a 37.5% stake in Maple Leaf Sports and Entertainment (Larry Tanenbaum owns the other 25%), which owns the NHL's Toronto Maple Leafs, the NBA's Toronto Raptors, Toronto FC of the MLS, as well as the CFL's Toronto Argos and various real estate holdings. Rogers is also the sole owner of the Toronto Blue Jays, as well as the team's home stadium, the Rogers Centre.

Despite an enviable position in a cozy telecom oligarchy -- the top three players in Canada own approximately 80% of the market -- Rogers shares haven't performed very well. The stock has underperformed its rivals over the last decade, with both TELUS and BCE raising dividends on at least an annual basis since 2013. Rogers, on the other hand, has only given investors marginal dividend increases, increasing the payout only two times since 2013.

Ultimately, dividend increases come from earnings, and Rogers has disappointed there too. Normalized earnings increased from $2.78 per share in 2013 to just $3.22 per share in 2022, a growth rate of under 2% per year.

Rogers has also made headlines for many of the wrong reasons. In 2021 the company was caught in the middle of Rogers family drama , with members of the family feuding over then-CEO Joe Natale. The company's Chairman, Edward Rogers, wanted Natale fired. Various members of his family wanted the CEO to stay. Eventually, the feud ended up with the board split, with both sides vowing to fight it out in court. The case was eventually settled and Edward was reinstated as Chairman.

Natale, who was eventually fired, has just sued the company for wrongful dismissal, despite walking away with more than $14M in severance .

In short, it's been a mess, and investors have punished Rogers' shares for the drama.

Shares have also been hit lately as fears of higher interest rates engulfed the market. Telecoms are known for issuing a great deal of debt to fund their seemingly never-ending capex expenses, and Rogers took on approximately $20B of debt when it acquired Shaw, a deal that closed in the early part of 2023. If rates stay higher, the company's interest expense will undoubtedly increase.

Put it all together and there are seemingly few investors bullish on Rogers, with most preferring rivals BCE or TELUS as potential investments. With all the attention on the company's rivals, Rogers is poised to outperform as it integrates the Shaw acquisition, investors embrace a more bullish stand on the industry, and as investors value the company's media assets more accurately.

Let's take a closer look at each part of the Rogers bull case, starting with the general issues surrounding Canadian telecom.

The Canadian telecom market

As mentioned, Canada's domestic telecom market has long been a cozy oligarchy with the top three players enjoying a dominant market share.

Rogers acquiring Shaw has changed the landscape a bit. Shaw was primarily a wireline telecom in Western Canada, focused on home phone, internet, and cable TV service to that market. But Shaw also had a growing wireless division, Freedom Mobile.

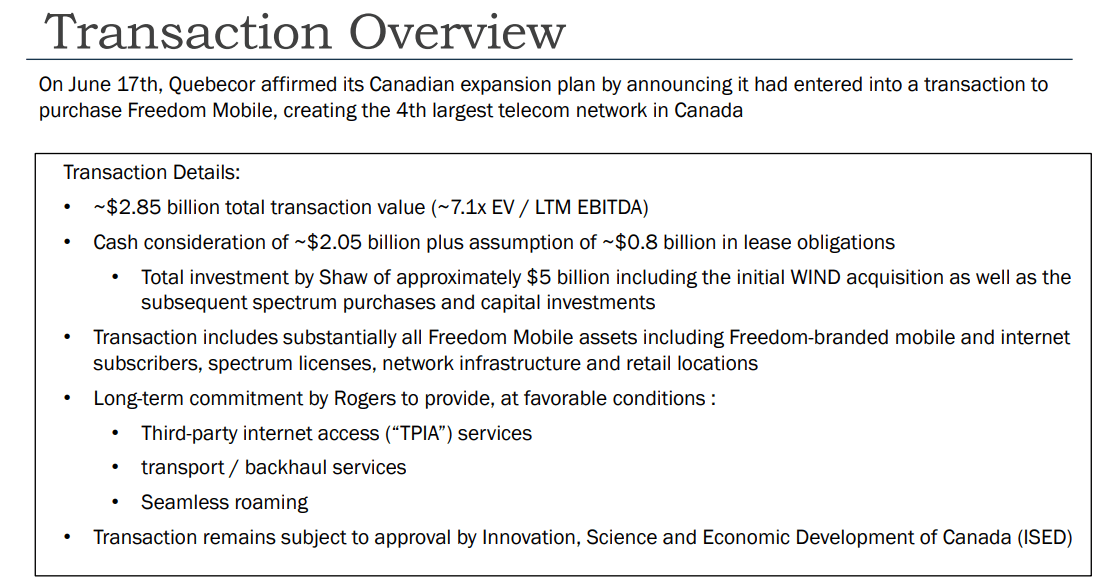

As a condition of getting the deal approved by Canada's Competition Committee, Rogers was forced to sell Shaw's wireless assets . Quebec-based Quebecor was the only logical buyer since a deal with one of the larger competitors would ultimately mean one less competitor in the market, and Ottawa wants to encourage more competition in the wireless space. Quebecor paid $2.85B for Freedom, paying just 7.1x EV/EBITDA for its latest prize.

{kind=link}

Almost immediately after the transaction closed, Quebecor announced plans to go after its three larger wireless rivals. It offered a plan for $50 per month that included national coverage across Canada, along with unlimited calls, texts, and 40GB of data usage. This immediately caused ripples throughout the telecom market, with Quebecor's larger rivals scrambling to offer similar deals.

Consumers in Canada have long complained about high rates, but average revenue per user (ARPU) has been trending lower for a few years now. ARPU peaked at nearly $74 in 2018; it fell to just over $68 in 2022. Investors are worried Quebecor's aggressive new pricing will further decrease ARPU, ultimately leading to lower profits for its more entrenched competitors.

But I'd argue things aren't quite that dire for Canada's larger telecoms, including Rogers. Rogers is free to market to all the new wireline subscribers it acquired from Shaw, offering incentives to bundle multiple services. Quebecor can only offer bundling incentives to customers in Quebec; it doesn't have wireline assets outside of the province. There's a reason why so many telecoms offer bundling -- customers generally take advantage.

The industry as a whole should also get a lift from Canada's steadily increasing population . Canada has thrown open the proverbial doors to immigrants, planning to add 465,000 new Canadians in 2023, 485,000 in 2024, and 500,000 in 2025. That's more than 1.4M new customers poised to enter the country in just a few years, which should help every wireless provider increase the top line.

Freedom also tried to undercut its competitors when it was owned by Shaw, with only mixed success. Folks didn't switch providers because changing is a pain, and because Freedom's network didn't work very well outside of major centres. The new Freedom network is much improved -- thanks partially to a roaming deal signed by Quebecor and Rogers as part of the Freedom acquisition -- but it'll take time for customers to realize that.

In short, Canada's three largest telecoms have weathered storms like this before. They're formidable competitors with strong moats, good networks, and loyal customers. An upstart competitor that has already existed for years isn't going to suddenly change that.

Earnings growth

Investors worried about Rogers losing a little bit of market share in wireless are missing an important variable in this investment thesis. The newly acquired Shaw assets are poised to significantly increase Rogers' bottom line.

The company has already started telling the market to expect significantly higher earnings. Back in March, when the Shaw deal first closed, it told investors it would generate between $16.7 and $17.3B in revenue in 2023, which would result in between $2 and $2.2B in free cash flow. It increased its free cash flow guidance in July, telling investors it would increase to between $2.2B and $2.5B in 2023.

Rogers has a current market cap of $27.5B on the Toronto Stock Exchange. If Rogers hits the midrange of its free cash flow guidance ($2.35B), then shares trade at just 11.7x forward free cash flow. That's a cheap valuation, especially when compared to its peers.

Analysts are bullish on Rogers' earnings going forward, too. According to consensus analyst estimates , earnings per share are expected to grow significantly over the next few years:

2023: $4.312024: $5.132025: $5.942026: $6.442027: $7.25

As always, we should take consensus analyst estimates with a grain of salt. But here's why this analyst thinks earnings will increase significantly.

Firstly, the assets acquired from Shaw are largely wireline assets, which don't require much in terms of capex spend. This translates into plenty of additional cash flow without the need to constantly reinvest in new technology. This makes earnings more predictable than on the wireless side of the business.

Secondly, Rogers has told investors it sees considerable synergy potential with the Shaw assets. It plans to cut $200M worth of expenses by the end of 2023, $600M by the end of 2024, and $1B by the end of 2025. As it stands today, Rogers has approximately 530M shares outstanding. $1B in synergies works out to nearly $2 per share in earnings.

Rogers also has plans to pay down the debt acquired along with Shaw. Net leverage at the close was approximately 5x EV/EBITDA. Rogers plans to dedicate a significant amount of cash flow towards paying off debt, along with selling off some non-core assets it acquired from Shaw, mainly real estate. It plans to get debt down to 3.5x EBITDA within the next three years. Decreased interest costs should also help boost the bottom line.

Rogers already trades at the relatively low valuation of 12x adjusted 2023 earnings. Even if it maintains the same multiple, shares should go higher as earnings go higher. Combine that with a higher multiple, and shares could easily be much higher 12-18 months from now.

Assuming the company earns $5.13 per share in 2024 and its multiple increases from 12x to 15x earnings, Rogers goes from a $52 stock today to a $76 stock in 2025.

Rogers' hidden assets

Finally, I want to take a closer look at two hidden assets Rogers owns, assets I believe help give investors a nice margin of safety and that make Rogers shares even cheaper than they first appear.

The first is Rogers' ownership of Cogeco (TSX: CGO:CA )(TSX: CCA:CA ) shares. In 2020, before it focused on acquiring Shaw, Rogers made an offer to acquire cable operator Cogeco. Rogers, along with Altice USA, made a bid to buy Cogeco in September 2020, with Rogers buying Cogeco's Canadian assets and Altice gobbling up Cogeco's U.S. assets. After raising its bid, the deal was ultimately rejected after Cogeco's controlling shareholder rejected the bid.

As part of this offer, Rogers accumulated a stake of 12.9% of Cogeco Inc. and 5.7% of Cogeco Communications. As of April, these two combined stakes were worth approximately $1B , although they'd be worth less today as Cogeco shares are off approximately 20% since April.

Considering the fact Cogeco shares are currently trading at a five-year low, Rogers seems likely to hold out for a higher price before considering selling. Cogeco shares are also dirt-cheap from a valuation perspective, checking in at just over 5x consensus analyst estimates for 2024's earnings .

Based on today's valuation, the Cogeco investment is worth approximately $1.50 per Rogers' share , with significant upside potential if Cogeco shares can recover.

The Cogeco stake is interesting, but the ownership stake in various sports teams is much more important. Remember, Rogers owns a 37.5% stake in MLSE, along with being the sole owner of the Toronto Blue Jays.

Sports teams are hard to value, but we can dig a little to get an approximate valuation.

The MLSE stake is relatively easy to value. Just a couple of months ago, reports came out that Larry Tanenbaum was looking to sell a 20% portion of his 25% stake in MLSE for $400M, a deal that would value the whole company at $8B. Both Rogers and Bell went as far as to officially question the deal, with the two sending a joint letter to Tanenbaum raising concerns about the sale. In other words, it sure looks like Rogers and BCE would've liked to purchase the 25% they don't already own, which supports the $8B valuation.

At an $8B valuation, Rogers' 37.5% interest in MLSE is worth $3B, or $5.66 per share.

The value of the Blue Jays isn't as easy to acquire, but there is a reasonable valuation tool out there. Every year, Forbes estimates the value of every franchise in the four major North American sports. Although these values are hardly gospel, they give us a pretty good idea of what each team is worth.

According to Forbes, the Blue Jays are worth US$2.1B , which works out to $2.85B using today's exchange rate between the U.S. Dollar and the Canadian Dollar.

Note that several recent sales of sports teams happened at values above the Forbes values, including the Washington Commanders ( purchased for 7% higher than Forbes' value ) and the Charlotte Bobcats (with the buyers purchasing Michael Jordan's majority stake at a $3B valuation , much higher than Forbes' $1.7B valuation). This supports the Forbes valuation as being slightly conservative.

At a $2.85B valuation, Rogers' ownership of the Blue Jays is worth $5.37 per share.

Combine the two, and Rogers has $11.03 per share locked up in sports teams, meaning investors are paying approximately $41 per share for the telecom business.

Here's why I think investors aren't paying much attention to the value of these sports teams. Rogers' media division is essentially break-even from an EBITDA perspective, generating just $69M in EBITDA from $2.28B in revenue in 2022. That's a 3% EBITDA margin. The wireless and cable divisions, meanwhile, generated close to 50% EBITDA margins. Many investors don't even like Rogers' media division because it doesn't contribute to the bottom line.

Sports franchises are notorious for not generating much cash flow. Instead, cash is invested in better facilities, coaches, and analytics, anything to help give the team an edge in both attracting players and winning games. Investors in franchises put up with this in exchange for capital gains. Team values have steadily risen for years, with one study determining a basket of sports franchises rose by 16.66% per year in the ten-year period from 2013-22.

Essentially, 20% of Rogers' share value is poised to grow at double digits over time, and the market has largely ignored the assets that will be responsible for it.

Risks

There are two main risks with this thesis -- continued rising interest rates and execution risk.

Let's start with interest rates. Rogers, like many other yield plays, has seen its stock price struggle as of late as investors look at various other fixed income options. The stock pays a 3.8% yield, while the 10-year Government of Canada bond has a yield of above 4%. GICs issued by Canadian banks pay higher than 5%. This makes an investment in Rogers somewhat unattractive by comparison, which would be even worse if rates continued to march higher.

The other risk is Rogers executing after the Shaw acquisition. Much of this thesis is based on Rogers realizing synergies, paying down debt, and maximizing the cash flow from the Shaw acquisition. If Rogers fails in any of those goals and earnings growth doesn't come, shares will likely underperform.

I'll also argue that there's the risk that investors simply don't care about the sports team assets and value for each isn't crystalized until Rogers sells, a move that looks unlikely today.

This opportunity exists because Rogers already isn't getting any credit for the upcoming earnings growth. The market is taking a wait-and-see approach with shares, likely to reward Rogers when it starts hitting those earnings targets. I'd argue this means shares have a nice margin of safety today, with limited downside if the earnings growth comes in a little under expectations.

The bottom line

As I write this, Rogers shares currently trade for $52 each on the TSX, which I believe to be significantly undervalued. I estimate the true valuation based on the sum of the parts to be:

- $76 per share for the telecom assets (15x 2024's projected earnings of $5.13 per share)

- $11 per share for the sports team assets

- $1.50 per share for the Cogeco stake

- For a total value of $88.50 per share

The challenge in a sum-of-the-parts analysis is receiving the true value for each of the parts. Short of a sale of the sports franchises -- which doesn't look likely -- it's hard to envision Rogers getting full credit for the assets it owns.

Fortunately, investors don't need that for the investment to work out. Ultimately, an investment in Rogers will work out if earnings grow as much as predicted. The sports team ownership just further increases the margin of safety, that's all.

Considering the company's lack of earnings growth from 2013 to 2022, and the drama surrounding the company's Board of Directors in 2020, it's easy to see why investors are somewhat skeptical. Expectations are pretty low. If the company executes and that shifts the market's opinion, I see shares trading at close to the intrinsic value of $88.50 per share, which represents more than 70% upside potential.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Hidden Assets And Improved Cash Flow Make Rogers Communications A Buy