CA - HIE: Opportunity Left In This Term Fund

2023-11-19 01:20:13 ET

Summary

- Miller/Howard High Income Equity Fund is expected to liquidate in November 2024, presenting a buying opportunity due to the potential for the fund's discount to narrow.

- The activist group Saba Capital holds a substantial stake in HIE, and that's pretty good company to be with.

- Though HIE's portfolio has a heavy weighting towards the energy sector, which can be a much more volatile area of the market.

Written by Nick Ackerman, co-produced by Stanford Chemist.

We are entering what should be the final year for the Miller/howard High Income Equity Fund ( HIE ), with an anticipated liquidation in November 2024. The fund is a closed-end fund with a term structure, and when liquidation takes place, that means the discount that the fund is trading at relative to its net asset value per share can be realized. That makes it still a buy today, but the underlying portfolio can be more volatile with a heavy weighting toward energy.

Saba Capital had been building up a large position in the fund. Since our last updat e, they sold some of their position , but it still comes to a ~12.5% stake in the fund. That's still substantial and enough of a position to hopefully make the fund do the right thing as we enter closer to the term date. Even better would be to push the management toward liquidation sooner rather than later.

On a total return basis, the fund's performance has outpaced the S&P 500 Index since our last update. However, the market was in mostly a downtrend before we saw a sharp recovery from the lows.

HIE Performance Since Prior Update (Seeking Alpha)

The Basics

- 1-Year Z-score: 1.28

- Discount: -6.49%

- Distribution Yield: 6.07%

- Expense Ratio: 1.84%

- Leverage: 0%

- Managed Assets: $200.914 million

- Structure: Term (expected November 24, 2024)

HIE is classified as a "diversified, closed-end management investment company whose primary objective is to seek a high level of current income with capital appreciation as a secondary objective."

They intend to invest "at least 80% of its total assets in dividend or distribution paying equity securities of US companies and non-US companies traded on US exchanges. The Fund will seek to invest in securities that the Investment Advisor considers to be financially strong with reliable earnings, high dividend or distribution yields, and rising dividend growth. The Fund may invest up to 25% in Master Limited Partnerships ("MLPs"), generally in the energy sector. The Fund intends to engage in an options writing strategy consisting of writing put options on securities already held in its portfolio or securities that are candidates for inclusion in its portfolio. It may also engage in covered call writing strategies, and it may buy put and call options. The Fund may write covered put and call options up to a notional amount of 20% of the Fund's total assets."

Update On Leverage

The last time we touched on the fund, they were taking down their leverage dramatically, and that was a trend that started even earlier in 2023. With the latest update, the fund has now dropped to zero leverage, and if the management does the right thing, that is exactly where it'll stay. By taking leverage down as we enter the final year, it would remove higher volatility and more uncertainty from the fund. The fund's holdings are volatile enough, with a heavy exposure to the energy sector.

Besides lower volatility for the fund in its final year, it would also take away the uncertainty of where interest rates may or may not go. With interest rate fluctuations, that has an impact on the cost of leverage since it was based on the Federal Funds Rate plus a spread. The spread depended on how much leverage was withdrawn, and the last semi-annual report put the interest rate at 5.68% as the Fed increased rates dramatically.

HIE Leverage Stats (Miller/Howard (highlights from author))

Term Structure Presents Opportunity

As we get closer to the termination date of the fund, that becomes more and more of the fund's biggest selling point. That is assuming one is comfortable with the underlying holdings in the first place, as that takes precedence over investing in any fund.

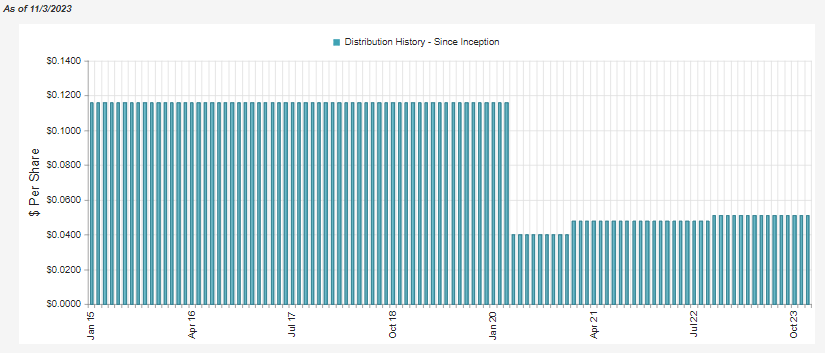

Historically, the fund had even traded at a premium pre-Covid, but after cutting its distribution, the fund was severely punished. As we get closer to the term date, the fund's discount should begin to narrow and eventually reach parity with its NAV per share. That's precisely where the opportunity comes from, as this means guaranteed alpha.

YCharts

It isn't guaranteed return but guaranteed alpha because the fund can still experience losses should its underlying holdings decline. In that case, the NAV could come to the share price rather than the share price rising to the fund's NAV. We certainly saw a big drop during Covid, and while HIE recovered most of the drop, that isn't always certain to happen. More recently, there has been pressure on equities outside of the mega-cap tech names, and that has impacted the NAV negatively for HIE in 2023.

With that being said, as we note in every update as we get closer to HIE's term date, the other risk to note is that the Board can extend the term date by a year without shareholder approval. It can also be amended to switch to a perpetual fund with shareholder approval.

Here's from the prospectus :

The Fund will terminate on November 24th, 2024, absent shareholder approval to extend such term. If the Fund's Board of Trustees believes that under then current market conditions, it is in the best interest of the Fund to do so, the Fund may extend the termination date for one year, to November 24th, 2025, without a shareholder vote..."

Distribution While You Wait

The fund currently pays a 6.7% distribution rate, and based on the NAV, that works out to 5.68%. So investors can collect a monthly distribution while waiting for the liquidation to take place - an income play with a chance for capital gains upside.

{kind=link}

The fund still carries a relatively higher expense ratio, and that does cut into the net investment income for covering the distribution. That would leave the distribution needing to be covered by a large portion of capital gains.

HIE Semi-Annual Report (Miller/Howard)

One area that has been a way to generate regular capital gains even if the underlying portfolio is falling is through writing options. In their semi-annual report, they took in just over $1 million in options premiums. That helped offset the realized losses the fund took in the first half of the year to some degree.

Additionally, after cutting leverage to zero, the fund's NII should improve with its next report. They were paying 6%+ on their borrowings as rates increased, and outside of their MLP holdings, very little in their portfolio yields that much.

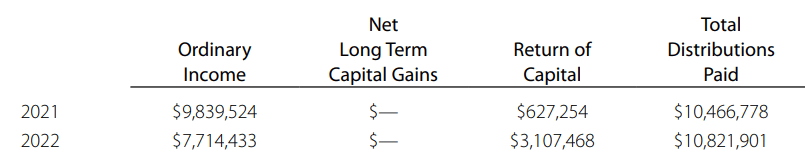

For tax purposes, with MLP exposure and capital loss carryforwards, the fund is likely to continue to distribute out return of capital on at least a portion of its distribution. Last year , for example, the fund received a total of $2.267 million in ROC distributions from the MLP holdings.

Another benefit for investors that invested post-Covid crash is that the fund is sitting on a sizeable amount of capital loss carryforwards. These carryforwards can be used to offset any potential realized gains regarding the taxable character of the fund's distribution. The fund also carries MLPs and other energy infrastructure companies that pay out return of capital distributions as well. That can result in return of capital distributions that would be non-destructive (i.e., ROC payments showing up while the NAV is still rising.)

{kind=link}

Of course, this is a benefit generally because it means they are tax-deferred until sold. With the anticipation of the liquidation date next year, that isn't the most appealing selling point of this fund for 2024. Taxes would be due assuming the fund rises above one's cost basis, which is reduced by the ROC.

HIE's Portfolio

HIE's portfolio can be difficult to keep up with since the fund's turnover rate is on the higher end. Although, it has been coming down in the last few years. In the last six months, the fund's turnover rate came to 54%, which puts it on pace to come in below 116% last fiscal year and below 155% and 277% in fiscal year 2021 and 2020, respectively.

On the other hand, what has been fairly consistent despite a complete turnover plus of the fund's value each year plus some is the fund's sector weightings. The fund has focused on energy and MLPs, and while they separate these two categories, it does mean combined, it's a significant overweight to energy-related investments at a 37.3% weight. At the end of June, the combined weights were 35.4%.

HIE Sector Allocation (Miller/Howard)

With this latest update, the fund's top holdings are all MLP or energy sector names. That might not seem too surprising given the weighting of the overall sectors in the fund, but we have seen other names make an appearance before.

HIE Top Five Holdings (Miller/Howard)

Energy Transfer ( ET ) remains HIE's largest holding as it was previously; this is then followed by Canadian Natural Resources ( CNQ ), but TC Energy ( TRP ) has slipped to the fifth largest holding after being the third. Instead, Enterprise Products Partners ( EPD ) slipped into its place, followed by MPLX ( MPLX ) coming in the fourth slot. EPD and MPLX were positions in the fund earlier in the year , but due to either market gyrations or buying from the manager have now become larger positions.

These are all names that have been seeing their distributions increase, and that, in turn, helps HIE with coverage of its distribution going forward. TRP pays in CAD, so the CAD/USD conversion is at play here.

YCharts

Conclusion

We are entering what should be the final year for HIE. The fund's track record is spotty due to heavy energy exposure. That was an area of the market that couldn't find its footing after peaking around 2015 and then bottoming out in 2020 during Covid.

Even 2023 hasn't been a year to brag about for the fund, but no place really has been when you factor out the Magnificent Seven performance. To illustrate, we can take a look at what the S&P 500 ETF ( SPY ) has done on a YTD basis relative to its equal-weighted peer represented by the Invesco S&P 500 Equal Weight ETF ( RSP ). Whether you are looking at a total return or price change-only basis, RSP has struggled. That's because SPY has moved to become increasingly overweight in the tech space.

YCharts

The RSP results are closer to what HIE is feeling this year. With the fund's termination date, that's an additional catalyst that can present some potential upside, or it can help dampen some of the decline felt if 2024 turns out to be another mediocre year. Remember, a term fund that liquidates can guarantee alpha, but it can't guarantee return - no investment can. So, there are always risks to consider; this one just happens to be even riskier due to its more volatile sector exposure. Fortunately, the fund has taken its leverage down, and that's where it should stay.

For further details see:

HIE: Opportunity Left In This Term Fund