HITI - High Tide: Insiders Are Buying And So Am I

2023-11-29 07:02:30 ET

Summary

- High Tide Inc. has an extremely competitive business model and a low cost of expansion.

- The cannabis industry is facing catalysts from both rescheduling and the passage of some form of the SAFE Banking Act.

- High Tide has reached positive cash flow a quarter earlier than management previously projected.

- Multiple valuation methods indicate the company is significantly undervalued.

- I consider HITI a Strong Buy.

Thesis

With rescheduling on the way , and momentum growing for the passage of some form of SAFE banking , the cannabis industry is eagerly awaiting its next rally inducing catalyst. For the U.S. sector, this will mean improvements to their margins and returns. For the Canadian sector, they will finally be allowed to expand out of their overly competitive market.

High Tide Inc. (HITI) is my highest conviction investment because of their extremely competitive business model and low cost of expansion. I believe they will be able to capture significant market share in any ecosystem they are allowed to enter. Two important events have occurred since my last article on High Tide . They achieved positive cash flow a quarter earlier than expected, and a cluster of insider buying was announced on November 22nd . After looking over their present financials and valuation, I currently rate High Tide as a Strong Buy.

Company Overview

High Tide is a discount cannabis retailer headquartered in Calgary, Canada. They have 158 stores in Canada and exposure to markets in Europe, The United States, and internationally. They have vertically integrated the production and distribution of cannabis accessories. They also own three of the top five highest traffic cannabis E-commerce platforms. Also, they operate a data analytics service platform, and are continuing to roll out their automated kiosks which operate under the name Fastendr.

High Tide's CEO-founder Harkirat "Raj" Grover started with a single store and two employees in 2009. He has built this empire up to 158 stores generating a quarterly revenue over $94M USD. By refusing to grow cannabis and instead vertically integrating the production of accessories, this company is in a unique situation where their business model has them selling cannabis as a loss leader. When consumers enter their stores for the ultra-cheap cannabis, they are also offered higher margin accessories. Not only does this give them an unparalleled ability to capture market share, they also place a downward pressure on the retail price of cannabis.

As most of their competition has been forced to divest away from growing cannabis in order to survive, they currently have more cannabis-based revenue than any other company in Canada. Their founder-CEO has repeatedly made clear their intentions to expand into both Germany and the United States as soon as the laws allow.

Born In A Gladiatorial Deathmatch

I began researching the cannabis industry in early 2021 when the entire industry rallied into valuations that left logic behind. I knew most of the industry was extremely unprofitable, so I chose to wait for it to cool off before I began buying. While I waited, I was given ample opportunities to examine the various business models the companies were developing.

Both the Canadian and the U.S. sectors were suffering, but for very different reasons. The players in the United States were all being crushed by the oppressive 280e tax obligation . Also, the highly competitive environment up in Canada lead to overproduction and a price war was forcing most of the sector to operate with negative gross margins. After watching both sectors for a few months, it became clear to me that the companies up in Canada were under far more stress than those in the United States. I have been studying Applied Game Theory for many years now, so I knew that Canada's more competitive environment was going to take many victims . I also knew that the survivors would only be able to avoid bankruptcy by becoming extremely efficient.

I shifted more of my attention to Canada's more competitive market because the companies there had been placed on what Sun Tsu refers to as Death Ground. They were forced to adapt or die. Most of the larger players abandoned their original strategies. Canopy Growth Corporation (CGC) divested away all of its Canadian retail locations, SNDL Inc. (SNDL) bought a chain of liquor stores, Tilray (TLRY) moved a significant portion of their production capacity to fruits and vegetables, and High Tide switched to a discount model .

That last choice caught my attention in a very big way. With all of the largest players in the Canadian sector already suffering from overproduction and negative gross margins, a relatively unknown retailer decided it was a good idea to alter its business model into one which places additional downward pressure on the price of cannabis. I decided this company was worth a deeper dive, and was not disappointed.

When they made the switch, they controlled roughly 3.6% of the Canadian market. Since then, their discount model has captured market share at a rate slightly under 1% per quarter. Excluding Quebec, they currently control approximately 9.5% of the market.

Cannabis consumers are highly price sensitive, so they are willing to drive right past non-discount stores to reach better deals. During a period where everyone else was struggling to find a viable business model, High Tide was opening new stores while capturing market share. This increased the stress the rest of the industry was already under. The situation became dire enough that High Tide's primary competitor, Fire & Flower, was knocked out of the game and found itself filing for bankruptcy this last summer. Meanwhile, in a show of extreme confidence , multiple insiders bought shares of HITI both last March , and again just last week .

Long-Term Trends

The global smoking accessory market is projected to experience a CAGR of 6.5% through 2030. CBD is projected to have a CAGR of 31.5% until 2031. The Canadian cannabis industry has an expected CAGR of 13.26% until 2027. The United States cannabis industry has a projected CAGR of 14.2% until 2030. Germany's cannabis market is projected to have a CAGR of 14.01% through 2027.

Guidance

During their Q1 2023 earnings call , they announced the goal of becoming cash flow positive by the end of the year. Their most recent earnings call revealed that they met this goal a full quarter ahead of schedule.

Guidance 1 (Q3 2023 Earnings Call Transcript)

{kind=link}

The company has already been collecting metadata on the macro-purchasing habits of their consumers and selling it to their competition. This most recent quarter they also announced they were offering Cabanalytics Consumer Insights, which is the same data repackaged into a more consumer friendly format for consumption by the general public.

Guidance 2 (Q3 2023 Earnings Call Transcript)

{kind=link}

I had to go to their Q3 2023 Financial Results report on their website to find the up to date numbers for Cabanalytics revenue. The rollout of CCI helped them generate even more revenue from the same metadata. Cabanalytics revenue rose from $5.5M CAD to $6.5M CAD and now represents 5.22% of total revenue. The collecting of this data grants management an information edge over their opponents. Any of their competitors who desire to remove this information advantage can choose to pay High Tide for access to the data, replacing it with a financial edge.

Additionally, the company continues to improve its operational efficiency. This is the third quarter in a row they have managed to decrease the cost of salaries and wages when compared to total revenue. This expense now represents only 11.1% of total revenue. They attribute this to the continued rollout of Fastendr.

Salaries, and Cabanalytics Q3 2023 Financial Results (Hightide.com)

{kind=link}

Earlier this year they shifted gears away from prioritizing relentless growth and toward achieving positive cash flow. They intend on maintaining positive cash flow while shifting back into growth mode.

They also set a goal of reaching $500M CAD annual revenue. Their quarterly revenue has reached $124.4M CAD; so as long as the current trends are maintained, they have effectively already achieved this. They met this goal one quarter ahead of schedule.

Guidance 4 (Q3 2023 Earnings Call Transcript)

{kind=link}

High Tide grew their discount membership program (Cabana Club) to over 1.1M members. Their Costco ( COST ) style ELITE membership program has grown by another 5,300 members and is now up to over 18,800 members. Both of these programs build lasting brand loyalty and represent a significant competitive moat.

Guidance 5 (Q3 2023 Earnings Call Transcript)

{kind=link}

As a testament to just how excessively competitive their discount business model is, same store sales are up by 114% over the last seven quarters. This growth continues to improve gross margins, which are now up to 28%.

Guidance 6 (Q3 2023 Earnings Call Transcripts)

{kind=link}

As competitors continue to fail around them, they are regularly presented with attractive buying opportunities.

Guidance 7 (Q3 2023 Earnings Call Transcript)

{kind=link}

As soon as the United States changes its laws, High Tide plans to execute a rapid expansion into the U.S. market through M&A activity. This will shortcut their way through the fact that many of the states require permits to open new stores. Although this would represent a significant dilution event, the company has a history of being extremely selective when choosing which stores to acquire and has already proven they can efficiently translate dilution into revenue growth.

Guidance 8 (Q3 2023 Earnings Call Transcript)

{kind=link}

Quarterly Financials

I should note that this is a Canadian company which reports in Canadian dollars and the values I use here in the financials section are all in USD.

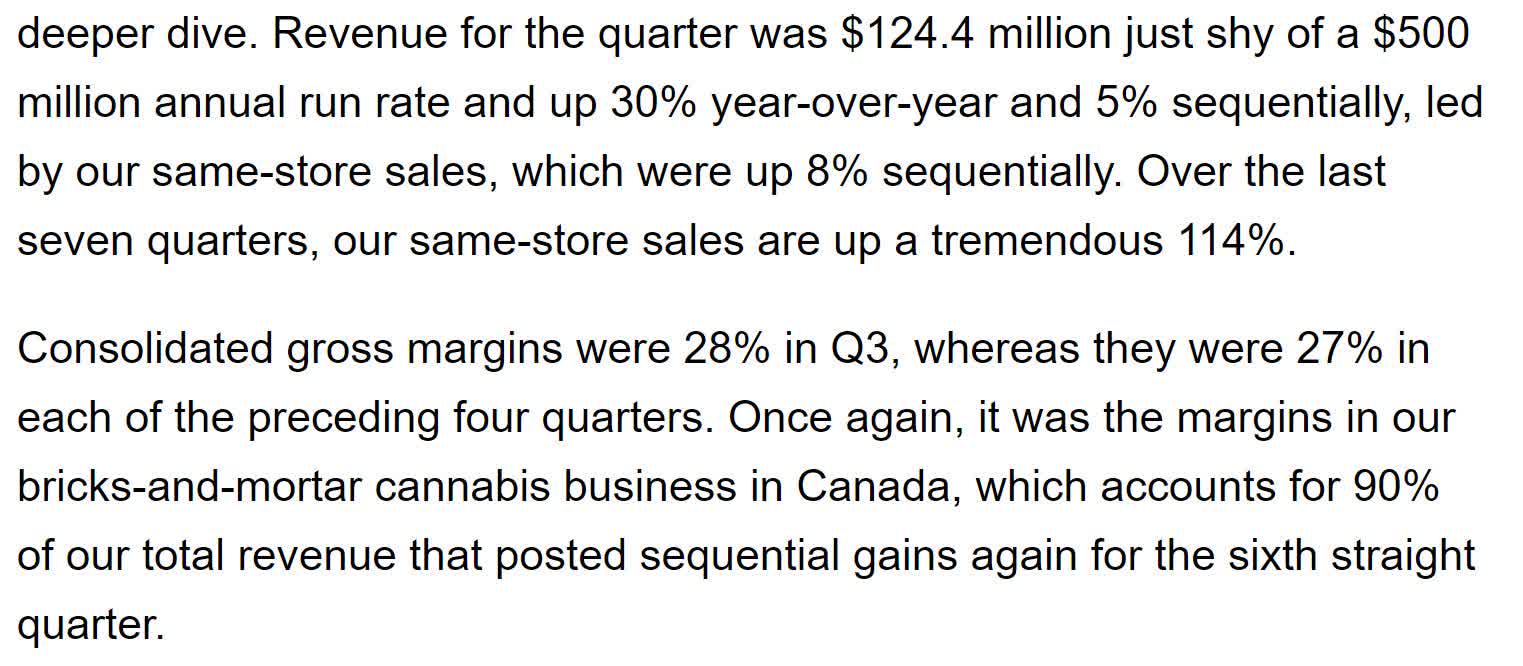

Their quarterly revenue chart is clearly showing their impressive growth, emphasizing how wildly popular their discount model is among consumers. Eight quarters ago High Tide had a quarterly revenue of $38.5M. Four quarters ago that had grown to $74.5M. By this most recent quarter that had further increased to $94.3M. This represents a total two-year rise of 144.94% at an average quarterly rate of 18.12%.

HITI Quarterly Revenue (By Author)

{kind=link}

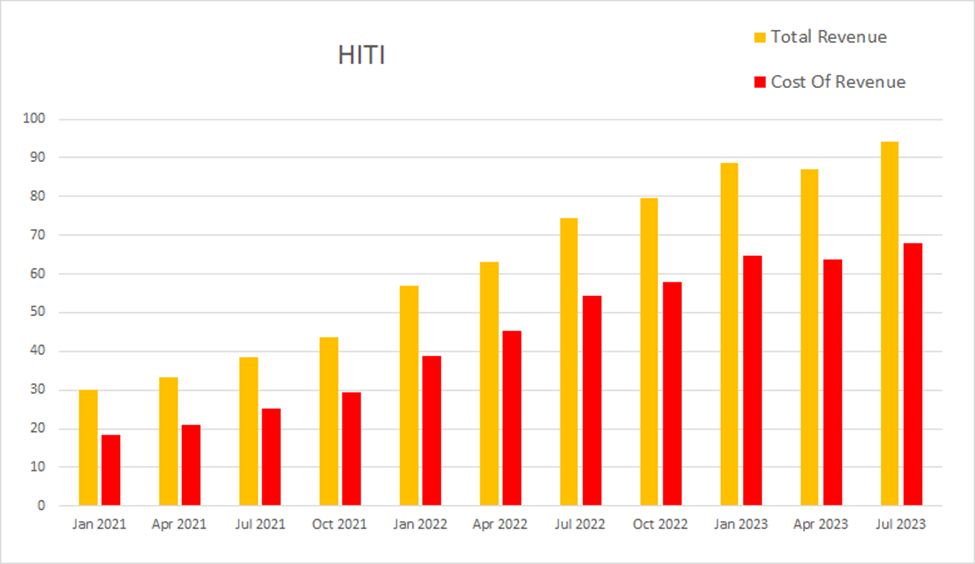

When they implemented their discount model in late 2021, it caused a gross margin contraction. Gross margins reached a low of 26.98% in Q3 of 2022, but have been improving since then. As of this most recent quarter, gross margins were 27.78%, EBITDA margins were 4.24%, operating margins were 0.53%, and net margins were at -2.86%.

HITI Quarterly Margins (By Author)

{kind=link}

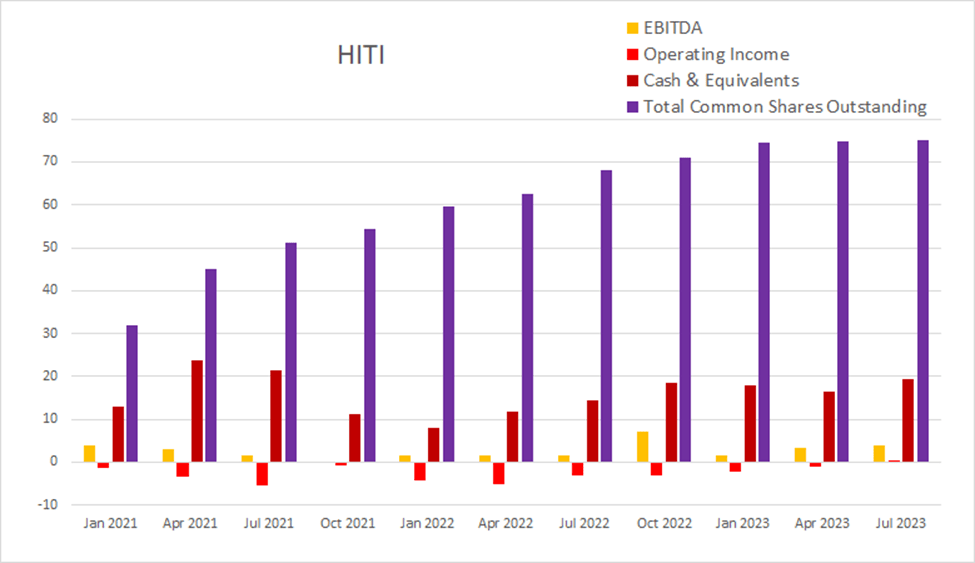

As they spent 2023 emphasizing the improvement of their financial metrics instead of growth through M&A activity, the pace of their dilution has been lower over this last year. The sum of their last eight quarters of dilution comes to 39.63%; over the last four quarters this has dropped to 10.00%. Considering they have grown revenue by 144.94% over the last eight quarters and 26.58% over the last four, this dilution has been accretive.

HITI Quarterly Share Count vs. Cash vs. Income (By Author)

{kind=link}

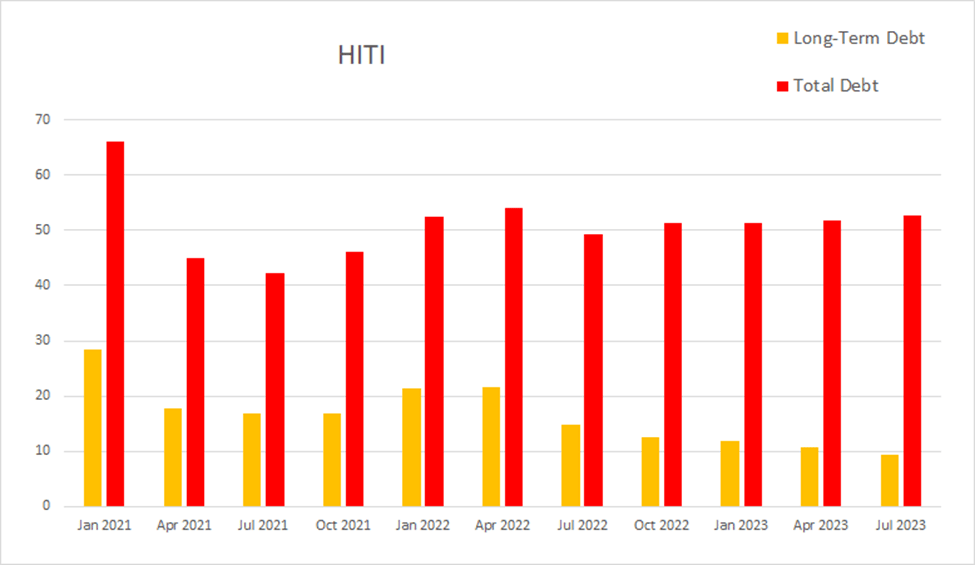

Their business model has them renting storefronts, so their total debt values include the future costs associated with their multi-year lease agreements. This most recent quarter, High Tide had -$2.5M in net interest expense, total debt was at $52.8M, and long-term debt was at $9.4M.

HITI Quarterly Debt (By Author)

{kind=link}

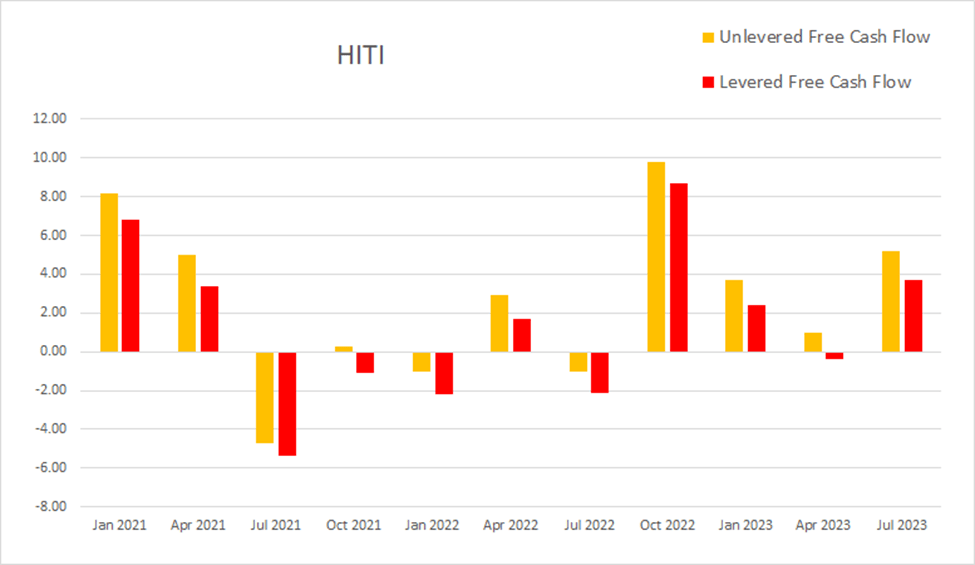

Whereas previously the company was emphasizing expansion over free cash flow, they have pledged to try to maintain positive cash flow going forward. I expect these values to continue to vary. As of this most recent earnings report, cash and equivalents were $20M, quarterly operating income was $1M, EBITDA was $4.0M, net income was -$2.7M, unlevered free cash flow was $5.2M, and levered free cash flow was $3.7M.

HITI Quarterly Cash Flow (By Author)

{kind=link}

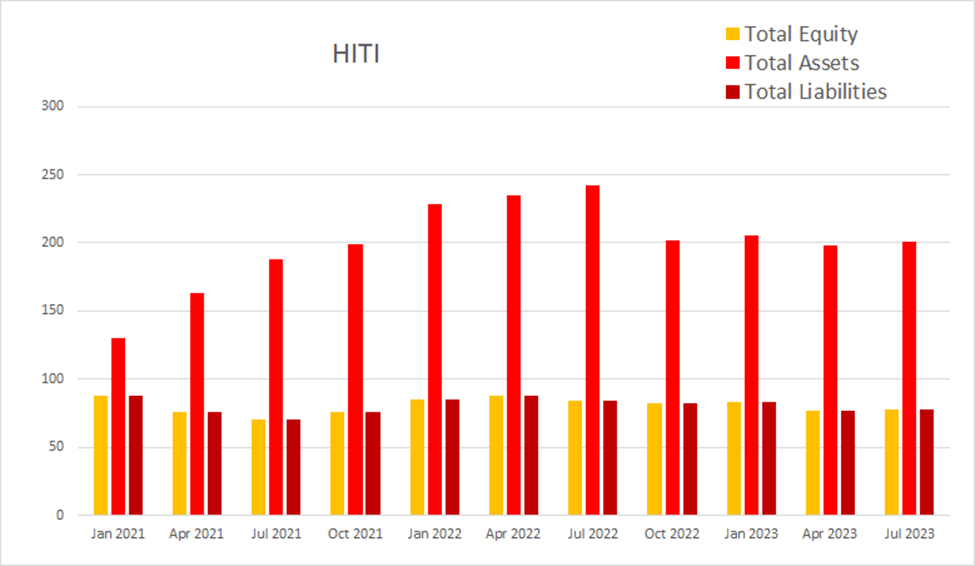

The company took a significant write down in Q4 of 2022 when they adjusted the value of their CBD assets. When inflation began forcing consumers to make tough choices about their purchasing habits, demand for CBD fell significantly. As High Tide's subsidiaries produce CBD products with some of the most positive consumer reviews in the industry, I expect that when aggregate demand for CBD returns, so will their lost revenue.

HITI Quarterly Total Equity (By Author)

{kind=link}

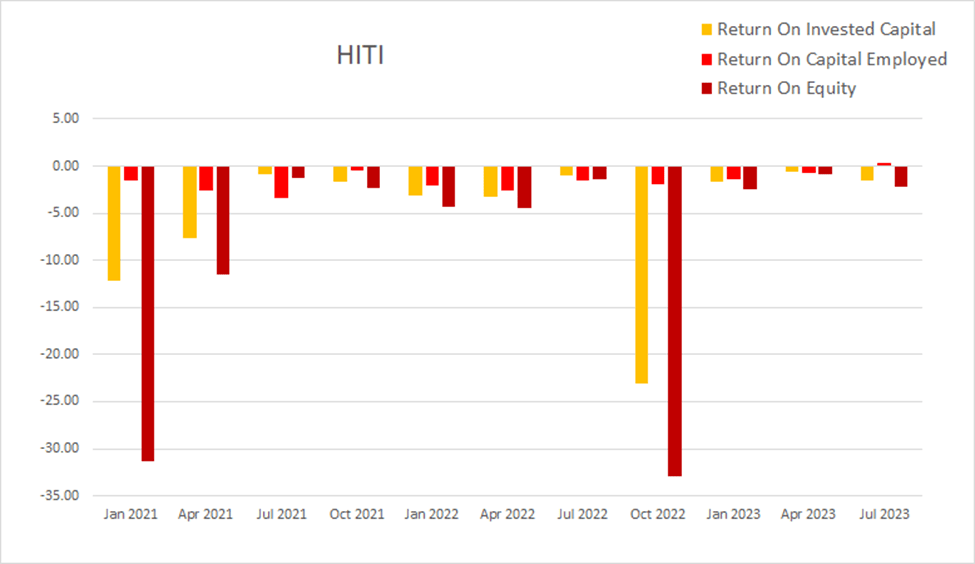

The company intends to maintain positive cash flow going forward, but they have yet to set a goal to achieve positive net income. I actually believe it is wise to avoid positive net income as this also avoids having to pay corporate income taxes. As anyone who has studied the history of Amazon ( AMZN ) will tell you, companies which maintain positive cash flow and negative net income have the potential to become true growth monsters. As of the most recent earnings report ROIC was -1.53%, ROCE was 0.32%, and ROE was -2.19%.

HITI Quarterly Returns (By Author)

{kind=link}

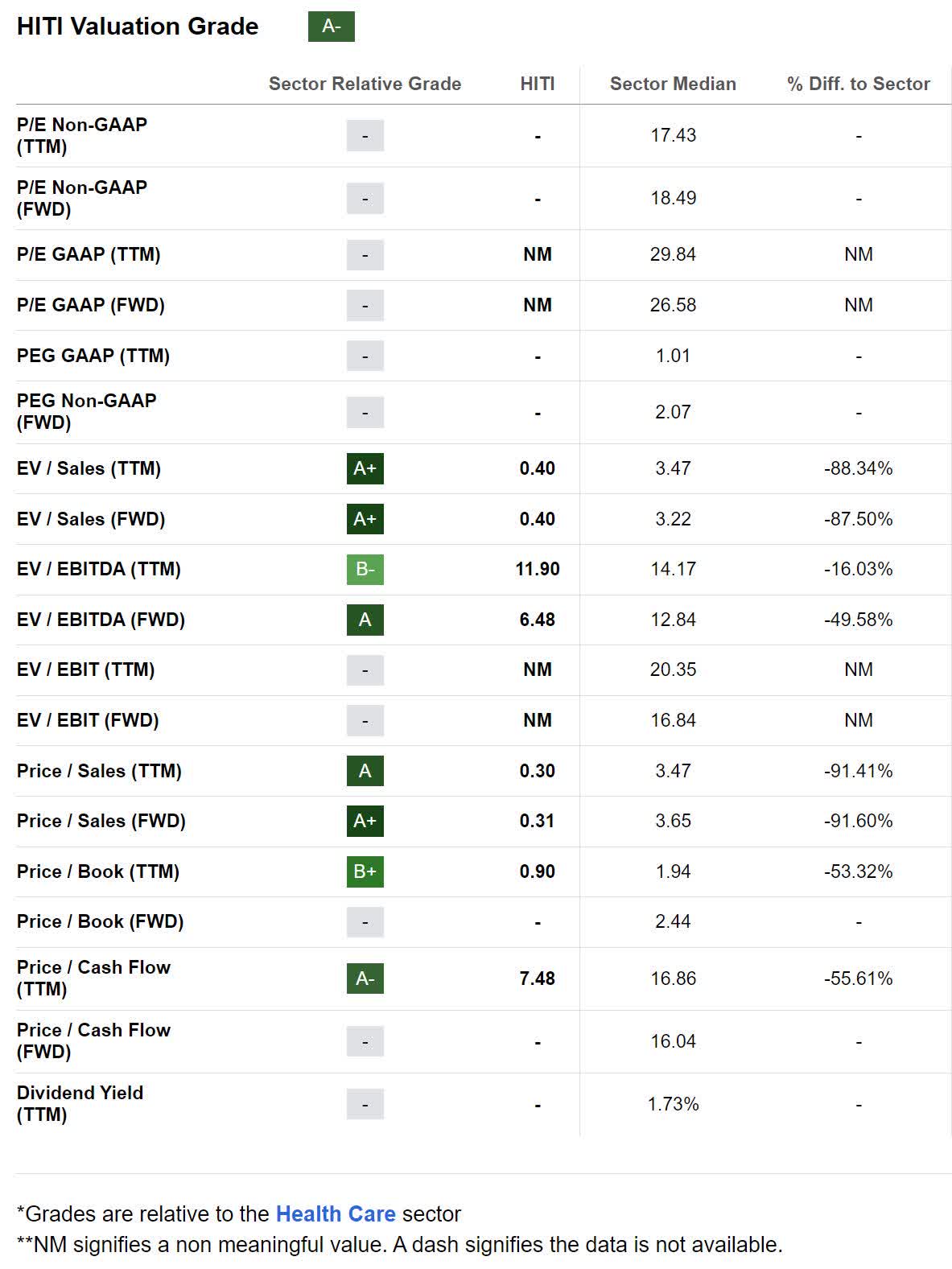

Valuation In Isolation

As of November 28th, 2023, High Tide had a market capitalization of $109.5M and had a market price of $1.42 per share. Overall, their valuation metrics are attractive, but they do not have positive net income, so I cannot use the PEGY method to produce an estimate for intrinsic value.

HITI Valuation (Seeking Alpha)

{kind=link}

However, I can use modified versions of the PEGY method to compare its present EBITDA and Cash Flow to its expected growth. These modified versions of PEGY can at least give us a rough impression on if the company is currently under or overvalued.

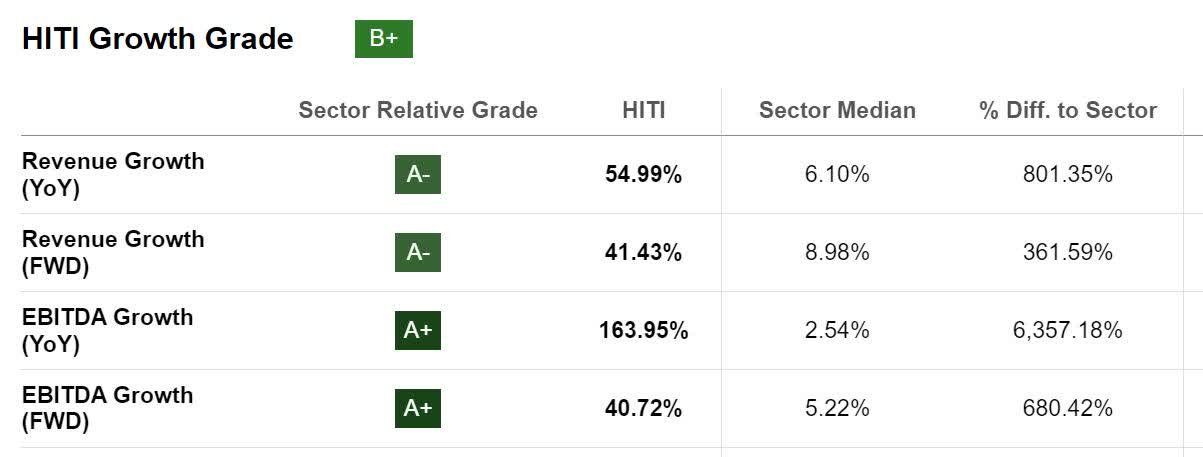

High Tide currently has a forward EV/EBITDA of 6.48x and a trailing Price/Cash Flow of 7.48x. I am unable to find a projection for their long-term growth, so I will be using their projected forward EBITDA growth instead.

Dividing their EV/EBITDA of 6.48x by their projected EBITDA growth of 40.72% produces a modified PEGY value of 0.1591x, and an inverted value of 6.2839x.

Dividing their trailing Price/Cash Flow of 7.62x by the same estimate for EBITDA growth produces a modified PEGY value of 0.1871x, and an inverted value of 5.3438x.

The (EV/EBITDA)/EBIDTA Growth method projects an intrinsic value of $8.92 per share. The (Price/Cash Flow)/EBITDA Growth method implies an intrinsic value of $7.59 per share. Both of these rough estimates indicate the company is significantly undervalued.

{kind=link}

Valuation Against Peers

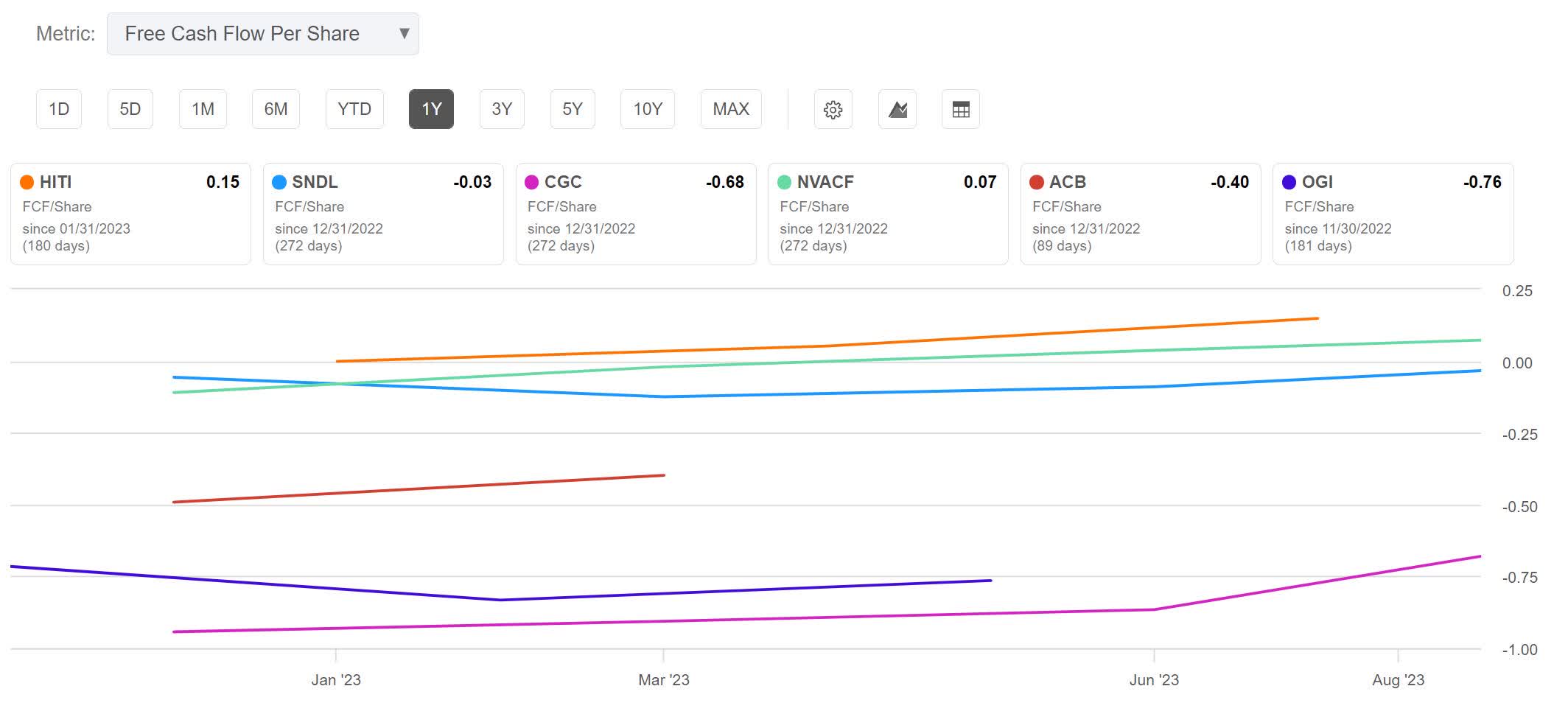

I will examine their valuation against both their Canadian peers, and their U.S. counterparts. Fire & Flower was the only other cannabis retailer of significant size in Canada, but since they fell into bankruptcy this last summer, I cannot use them for comparison. All of the rest of these companies produce cannabis while High Tide does not, so this is not a direct apples to apples comparison.

These are the highest revenue cannabis companies in Canada. With most of the Canadian Sector still not cash flow positive, I am having to limit which valuation metrics I can use. High Tide has the highest cash flow per share in its sector.

Canadian Sector - Free Cash Flow Per Share (Seeking Alpha)

{kind=link}

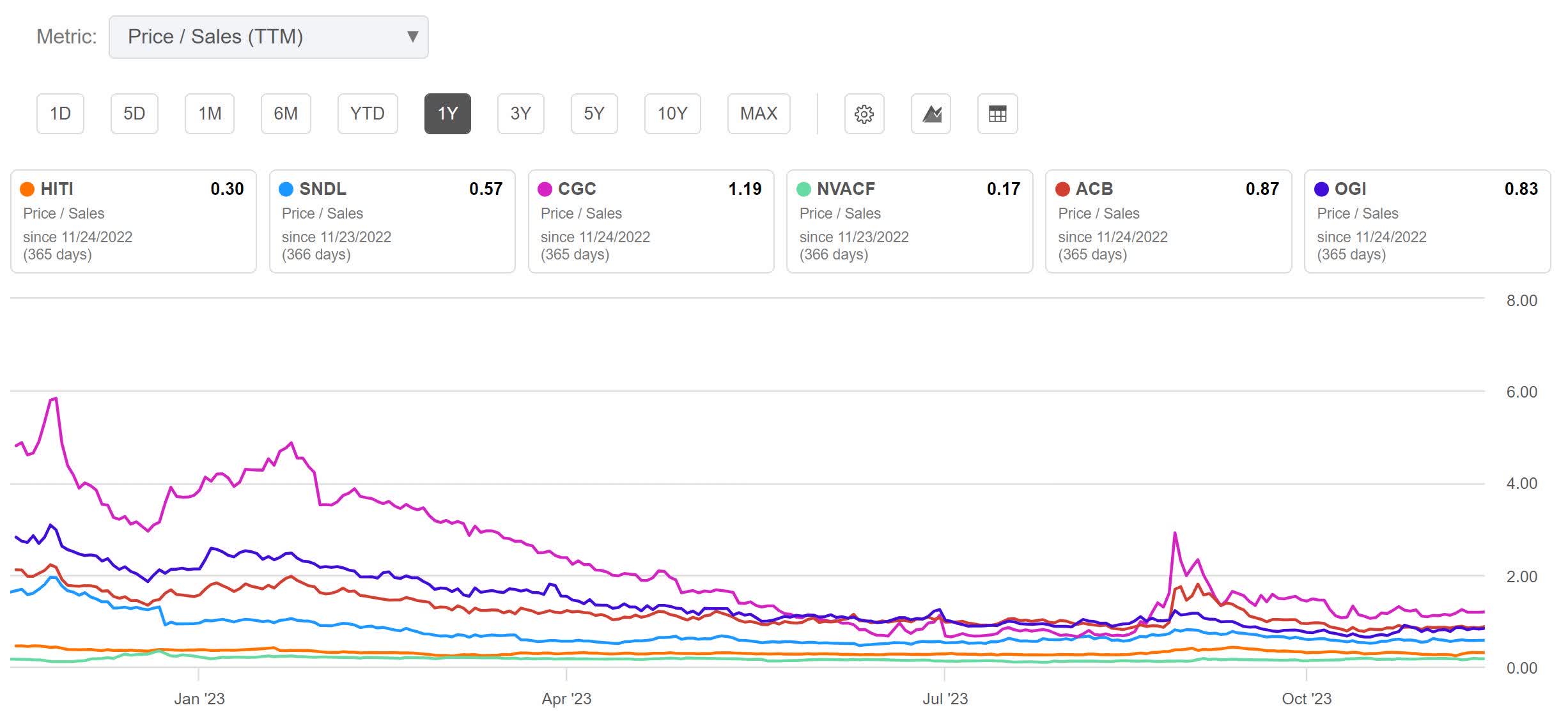

Viewing their trailing Price/Sales ratios makes clear their total revenue is undervalued when compared to most of their peers. The only company which has a lower P/S ratio is Nova Cannabis (NVACF), which is in the middle of trying to get out of the oppressive franchise agreement they signed with SNDL Inc.

Canadian Sector - Price/Sales (Seeking Alpha)

{kind=link}

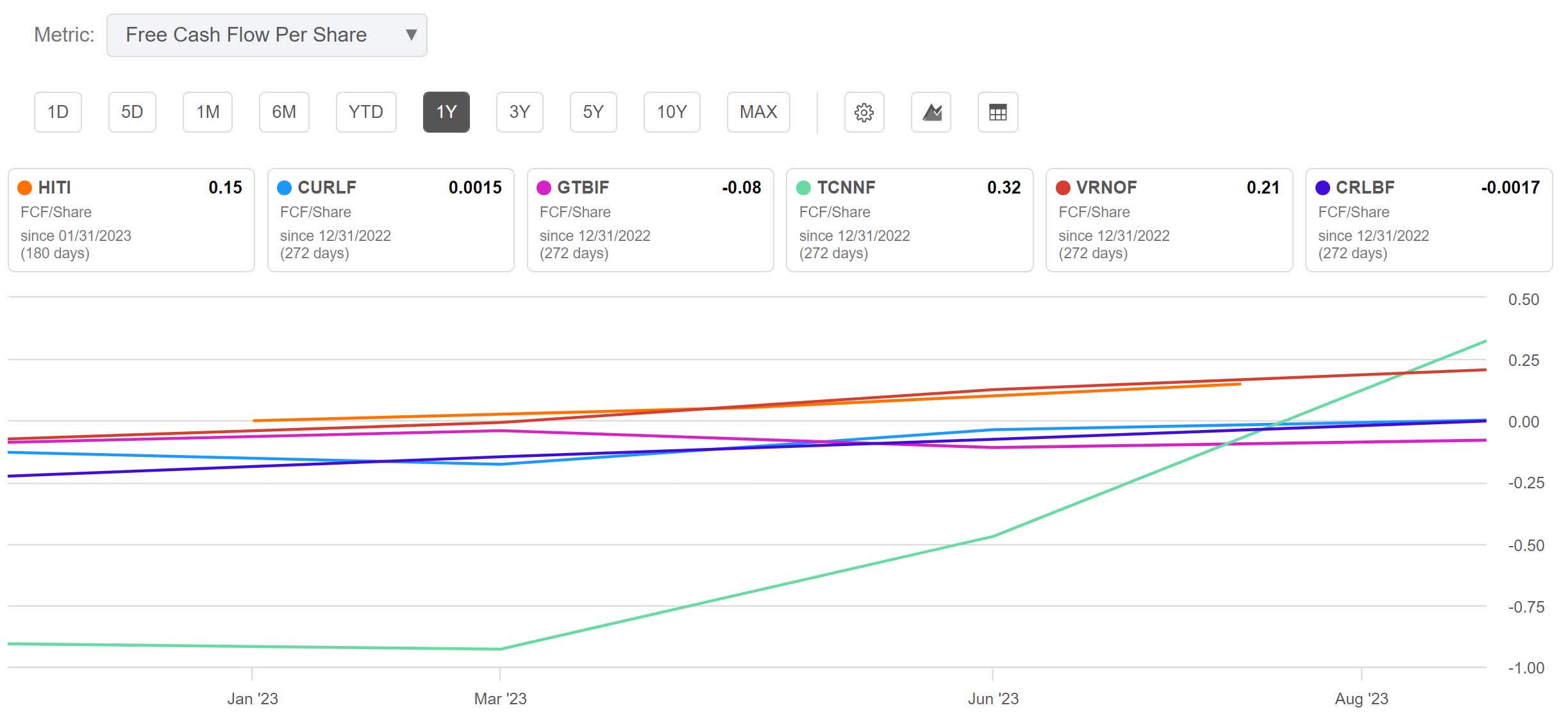

When I instead compare High Tide to the highest revenue recreational cannabis operators in the U.S. sector, they still are more profitable on a per share basis than all of them except Trulieve (TCNNF).

U.S. Sector - Free Cash Flow Per Share (Seeking Alpha)

{kind=link}

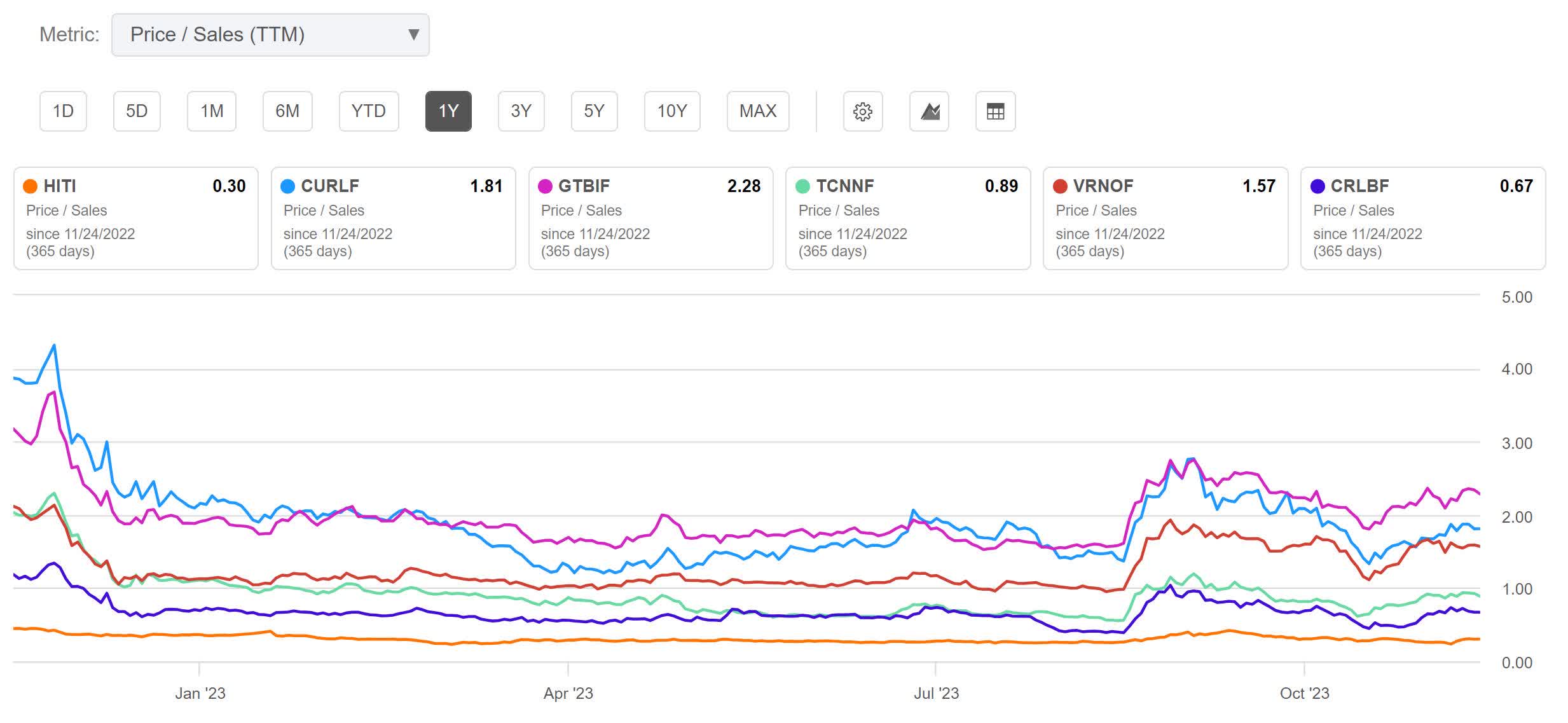

While being more profitable than most of them, High Tide has a lower trailing Price/Sales ratio than the top five recreational cannabis companies in the United States. With them currently at a 0.30x, they are less than half the price of Cresco Labs (CRLBF), which is the next cheapest one by revenue.

U.S. Sector - Price/Sales (Seeking Alpha)

{kind=link}

Valuation History

The cannabis industry experiences euphoric rallies which have a history of leaving rational valuations behind. In the time since both of the last two industry-wide rallies, the company has grown itself from a small, relatively unknown entity, to the highest revenue cannabis company in Canada. I expect it to receive far more attention during the next rally than it did during either of the previous two.

In 2019, High Tide reached a trailing P/S ratio of 7.53x. During the last industry wide rally in early 2021 they reached a trialing P/S of 2.66x. They are currently trading at a 0.30x. If the next rally carries them to their previous P/S ratios, that would translate to 2,410% gain in share price for the 2019 peak, and an 786% gain for the 2021 peak.

HITI Trailing Price/Sales History (Seeking Alpha)

{kind=link}

I get a very different result when I instead chose to view them based on a Price/Book ratio. During the 2019 rally, they peaked at a Price/Book of 4.48x. During the 2021 rally they reached a 17.09x. From today's 0.92x, if they were to reach their former values the 2019 rally would translate to a 356% gain in share price. If it were to reach their 2021 peak, it would be a 17,576% gain.

HITI Price/Book History (Seeking Alpha)

{kind=link}

Hidden Margin of Safety

As I consider myself a growth-oriented value investor, I typically avoid talking about margin of safety on any company without positive Net Income. However, because this company is running a deep discount model, and can choose how deep they push their deals, High Tide has far more control over its margins than most business models. As long as they are reasonable goals, this means they are able to more easily achieve specific financial targets. If they ever find themselves in danger of failure, they can always raise prices.

The picture below illustrates this clearly. Their discount model has them offering cannabis at prices significantly lower than the market average to Cabana Club members. Those who pay the annual fee to become Elite members pay even less. While this is only a single example, in this case Cabana Club members are presented with a 27.44% discount, while Elite members are offered a 35.8% discount. Considering their Q3 earnings report had a net margin of -2.86%, it's pretty clear that this company could be net income positive whenever it wants. Their flexibility with pricing grants investors a significant margin of safety, one which is difficult to quantify using traditional valuation methods.

Canna Cabana Price Advantage (Johnny Stonks)

Risks

Before I can cover actual risks, I need to tackle the idea that a delay in U.S. rescheduling would cause a problem for this company. High Tide has already proven its business model works in Canada's more mature market. With them still only controlling less than 10% of Canada's market, the company still has plenty of runway available there. In fact, additional delay would allow them to continue expanding their footprint and improving their financial situation before the time comes to fight another price war.

The risk of a buyout is real, but it may not necessarily be bad. High Tide has established extremely competitive moats; this only makes them more attractive for a buyer with especially deep pockets. I have a hypothesis that as soon as the laws in the United States allow for it, the tobacco industry is going to try and buy themselves a business life cycle extension by expanding into cannabis. Companies such as Philip Morris (PM) or Altria Group (MO) are trapped in a sunset industry, yet blessed with impressive cash flow. It would be wise for them to gain exposure to cannabis. While it is possible High Tide is purchased for an unfavorable price to current shareholders, management has already proven they are apt negotiators, so I believe the real risk here is what happens after the purchase. If the new owners replace the current management with people who do not understand the industry, it would be a major cause for concern.

They refuse to produce cannabis and instead use it as a loss leader; relying on the price sensitivity of consumers to drive traffic to their stores. This also means they place significant downward pressure on the price end-use consumers are accustomed to paying. This two-fold effect captures market share while enhancing the financial suffering of their competition. This produces significant competitive edge; if they were to begin producing cannabis they would lose it.

Catalysts

The company faces numerous catalysts. The most obvious one to cite is rescheduling. On October 6th, President Biden began the process by asking the DHHS and the Attorney General to review the available evidence and reassess its present schedule 1 status. By the end of this last summer , the general public was made aware that the DHHS recommended that it should become schedule 3. The industry is still waiting on the DEA to finish their assessment before the Federal Government will complete the reclassification process.

The other industry wide catalyst to cite is the passage of some form of SAFE Banking Act. This would finally allow institutional entities to invest into cannabis companies, driving valuations higher.

During both of the last two industry-wide rallies, High Tide was still a relatively unknown name. They have since achieved the top revenue slot in Canada and have established themselves as the most dominant business model. They are likely to garner significantly more attention during the next major rally.

Earlier this week it was revealed that the German government finally reached an agreement on establishing the rules for the regulation of cannabis in Germany. In preparation for this, High Tide has already formed a relationship with Berlin-based Sanity Group to assist an expansion of their retail footprint there.

High Tide has adaptation and innovation ingrained into its DNA; they are perpetually searching for new sources of high margin revenue. In addition to constantly releasing additional white label products, they have been developing a line of digital kiosks under the name Fastendr. While they are currently using them in their storefronts to reduce labor costs, modified versions of the technology could be leased out to other retailers. Also, I speculate that the development of these digital kiosks may one day lead to the release of a line of vending machines which would be capable of checking the age of customers before a sale. In addition to cannabis, such machines could also be able to be used for alcohol or tobacco products.

In addition to their Cabana Club discount model, they are also digging a very deep moat with their Elite program. Elite customers pay an annual fee to be granted access to even deeper discounts. This model is similar to the one Costco uses. Once a consumer pays to gain access to such deep discounts, they are less likely to be interested in purchasing their cannabis and accessories anywhere else. The combined power of these two discount choices produces a recipe for building incredibly strong brand loyalty.

With most of the industry still focused on attempting to produce profits from growing the plant, they are all exposed to the risk of production while High Tide is not. During periods where the price of cannabis is high, producers can expect better margins and returns. Yet anytime the price is low, producers can expect to struggle. Also, with most commodities, selling it to end use customers allows for the opportunity of a value-added experience and is far more profitable than producing it. This is why Starbucks (SBUX) produces only a tiny amount of the coffee they sell. As the industry matures, I expect for the price of flower to continue falling. However, shifting the thinking of an entire industry takes time. Several months ago Bruce Linton, former CEO of Canopy Growth, was being interviewed by The Dales Report when he expressed to them just how powerful High Tide's business model was. Now that Bruce has had the opportunity to step outside the game and become an outside observer, he has altered his beliefs on the long-term path the industry is trending toward. "Canna Cabana and those guys, Raj gets it" - Bruce Linton Former CEO of CGC. 6/7/2023 .

While I blame most of the suffering the growers are experiencing on rampant overproduction, the additional downward pressure High Tide places on the retail price of cannabis is only making their situation worse. As time goes on, and more of their competition fails, attractive buying opportunities should continue to present themselves.

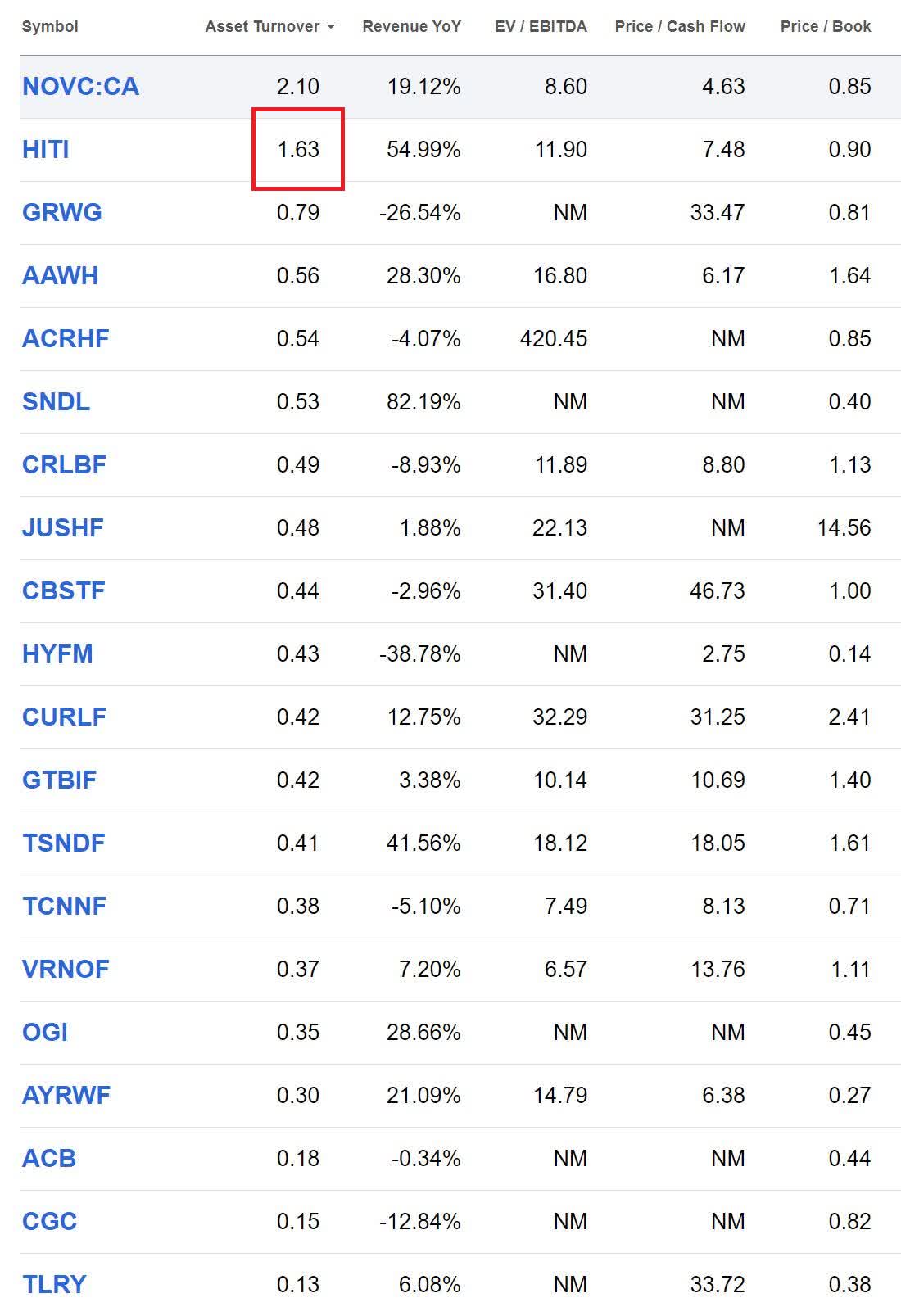

Unlike most of their competition, High Tide has an extremely low cost of expansion. Statements made by the CEO indicate their average cost of opening a new store is only about $300K CAD. They chose to vertically integrate cannabis accessories instead of the cannabis itself and already have a global supply chain in place. They merely have to secure a local source of cannabis when they enter a new market. Everyone else's business model revolves around growing cannabis, so they also have to set up growing and processing infrastructure. Producing cost of expansion estimates for every single company in the industry is beyond what I am willing to attempt. However, I can look at Asset Turnover Ratio to assess, in a very rough way, everyone's cost of expansion. I need to be clear that Asset Turnover Ratio is ttm Revenue/Assets. It is not New Market Revenue/Cost of Expansion. However, this does tell a story; it is clear that High Tide requires less capital to expand than a majority of their competition.

Cannabis Industry Asset Turnover Ratio (Seeking Alpha)

{kind=link}

Conclusions

By now, you can understand why High Tide is not just my highest conviction cannabis play, it is my single highest conviction investment. Choosing companies that are competitive is good, but I prefer to take it one step further and invest into companies which have inherently unfair business models. High Tide's discount model is wildly popular with consumers, while applying financial stress to their competitors; this is perfect.

Management has already proven they are competent and understand the needs of their customers on a higher level than their competition. When the price war broke out in Canada, it spurred adaptation and innovation. Everyone was forced to scramble to find new strategies for long-term success. This company has adapted itself into one which is capable of thriving regardless of the price of the commodity they sell. They are thirsty to expand into new markets and can do so cheaply. With them currently limited to only opening stores in Canada, and additional markets becoming available to them soon, they still have an extremely long runway.

The stock has been in an accumulation zone for the last 18 months or so, and I will continue buying until the next major rally. Because of their low cost of expansion and culture of innovation, I believe this company has the potential to become a very attractive long-term compounder.

For further details see:

High Tide: Insiders Are Buying, And So Am I