CA - High-Yield High-Growth SWANs On Sale: Brookfield Renewable And Brookfield Infrastructure

2023-10-28 08:00:00 ET

Summary

- Rising interest rates have created opportunities in the high yield and dividend growth sectors.

- Brookfield Renewable Partners and Brookfield Infrastructure Partners are undervalued and offer strong growth potential.

- We address why their stock prices have plummeted so sharply in recent months and refute the most common bearish criticisms of them right now.

With the significant rise of interest rates since the beginning of 2022 - particularly with the rapid rise of long-term interest rates over the past few months - numerous golden opportunities have opened up in the high yield and dividend growth sectors. While investors may be panicking in the short term due to the steep declines in the stock prices being assigned to these businesses, their dividends remain quite safe, their balance sheets and business models remain strong, and their long-term growth profiles remain intact.

In this article, we discuss two high yield, high growth, sleep well at night investments from Brookfield ( BN , BAM ) that appear quite undervalued right now and we are buying hand-over-fist.

#1. Brookfield Renewable Partners ( BEP , BEPC )

BEP is a leading renewable power generation company with a global presence and a diverse collection of renewable energy assets, including hydro, solar, and wind resources spread over five continents. Their renewable assets are valued at a staggering $78 billion with an operational capacity of 25,900 MW, servicing around 30 markets in 20 nations.

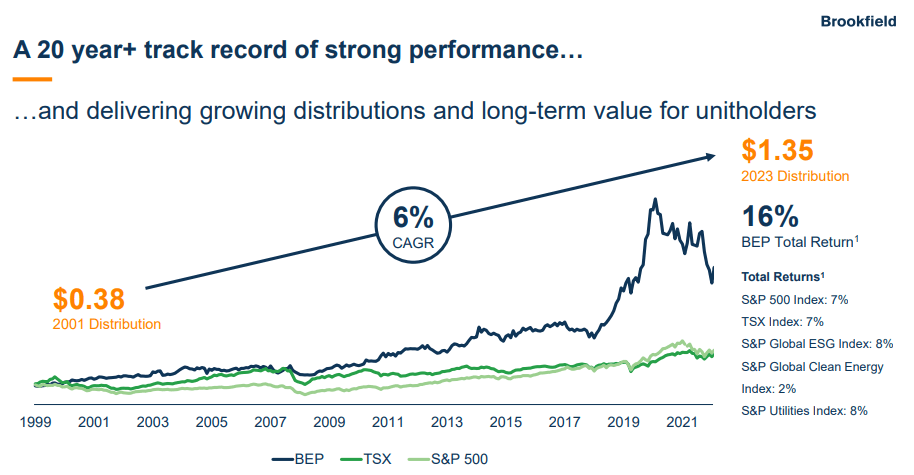

BEP's track record speaks for itself, with the company generating phenomenal long-term growth and total returns for investors:

{kind=link}

Moreover, it boasts a 9.8% adjusted funds from operations ("AFFO") per unit CAGR since 2011. With a current NTM yield of 6.3% and a promising growth forecast due to the strong expected demand for renewable power generation - 10.9% AFFO per unit CAGR and 5.6% distribution per unit CAGR through 2027 (as projected by the Wall Street analyst consensus) - BEP presents a golden opportunity for dividend growth investors.

Moreover, BEP offers investors a fairly low risk business profile, with 90% of its cash flow coming from power purchase agreements with a weighted average remaining term of 14 years left in their term and around 70% of its revenue coming from inflation-linked contracts. With a BBB+ credit rating from S&P, significant liquidity, well-laddered debt maturities, and the vast majority of its debt held at the asset level, BEP has the best balance sheet in the renewable power production sector while also offering investors a powerful combination of defensive cash flow, high yield, and high growth.

#2. Brookfield Infrastructure Partners ( BIP , BIPC )

BIP is structured very similarly to BEP, but is instead focused on non-renewable power infrastructure. It has substantial exposure to sectors that include midstream, utilities, transportation, and data. Its midstream business consists of pipelines, natural gas storage, and gas processing. Its utilities business includes both electrical and natural gas. Its transportation exposure includes railroads, ports, toll roads, and will soon include the world's largest shipping container company in Triton International ( TRTN ). Finally, its data business includes towers, semiconductor manufacturing plants, fiber optic cables, fiber-to-home connections, and data centers. As a result, BIP has plenty of places to harvest and allocate capital opportunistically in order to maximize shareholder value.

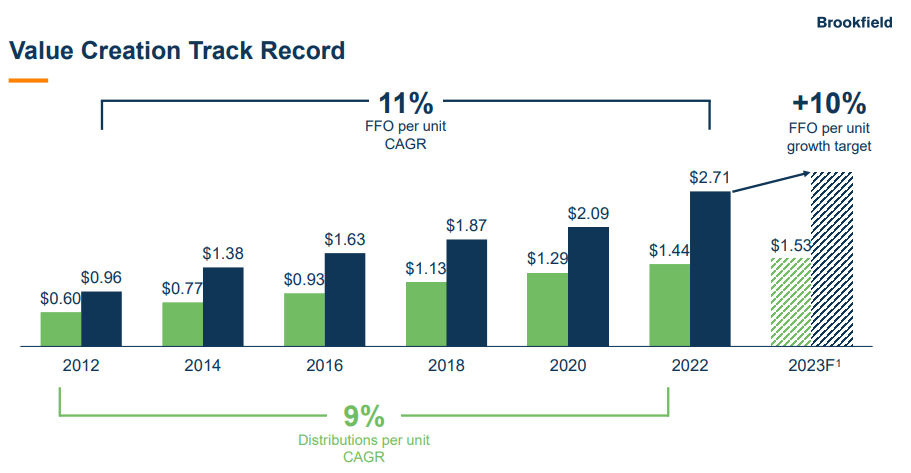

Unsurprisingly, its track record speaks for itself:

{kind=link}

Additionally, similar to BEP, BIP's business model and balance sheet are in excellent shape as evidenced by its BBB+ credit rating. 85% of its funds from operations, or FFO, is either inflation protected (10%) or indexed (75%), 90% of its FFO is either contracted or regulated with an 11-year weighted average duration remaining, and 90% of its debt is fixed rate with an average term to maturity of seven years. Additionally, like BEP, the vast majority of its debt is held at the asset level, leading to a pretty low risk financial profile for the company.

Addressing Some Concerns About BEP and BIP

While this all sounds great for BEP and BIP, why have their stock prices crashed so hard in recent months?

Two of the biggest reasons why the market has gotten so bearish on these two stocks are:

- Bear Thesis #1: They trade at a premium to peers.

It is absolutely true in that if BEP or BIP were to sell off all of their assets and businesses at similar multiples to what their publicly traded peers are trading at currently, they would undoubtedly get less back than they are currently being priced at in the market today.

However, this approach to valuation for BEP and BIP only makes sense if the highest and best way to realize the value of their assets was through a sale. In the case of BEP and BIP, this is not even close to being true (at least in the case of the vast majority of their assets). Instead, they add tremendous value to their asset base thanks to their relationship to their parent and manager (Brookfield). They get access to exclusive deal flow and asset sales as well as considerable operational expertise through their Brookfield connection. As a result, they are able to routinely buy, improve, and sell their assets and then recycle the capital into new opportunities in a manner that accelerates the wealth compounding process at a faster rate than would be the case if they were a simple buy-and-hold investor like many of the peer companies of their holdings are.

The proof of their business model and capital allocation success is clearly seen in their long-term track record of delivering market-crushing total returns and rapid and consistent distribution growth alongside paying out a hefty current yield. As a result, BIP and BEP should be valued on a discounted cash flow/yield plus growth basis, not on a sum-of-the-parts/valuation multiple analysis. When looking at BIP and BEP from both a discounted cash flow and yield plus growth valuation model, they very undervalued right now.

- Short Thesis #2: BIP and BEP are heavily leveraged, and their growth rate will suffer immensely from rising interest rates .

It is true that BIP and BEP have a lot of debt and that rising interest rates on the net negatively impact them. However, this headwind is vastly overstated by bears in our opinion for at least seven reasons:

- We do not think that interest rates are likely going to head much higher and the odds are that they will decline over time moving forward. Deficit government spending and a slowing economy will likely force the Federal Reserve's hand to cut interest rates sooner rather than later and inflation has largely already been tamed to a somewhat reasonable level, even if it remains slightly above the Fed's long-term target rate. With the rapid advance of AI and other technological breakthroughs, we expect strong deflationary forces to be exerting themselves on the economy over time, which will also give the Fed more flexibility to cut interest rates from current levels.

- A very high percentage of BIP's and BEP's assets are indexed to inflation. Given that high inflation is the sole justification being provided by the Fed for keeping interest rates at elevated levels, BIP's and BEP's revenue streams will also be growing at an elevated pace for as long as interest rates remain elevated, thereby helping to offset much of the headwind from rising interest rates.

- BIP and BEP have very low exposure to floating rate debt and their debt maturities are pretty well laddered. As a result, only a small percentage of their debt each year will need to be refinanced at higher interest rates, while a much larger percentage of their revenue will be contractually growing at a pace that is indexed to inflation.

- BIP's and BEP's constant portfolio churn means that they are underwriting new investments based on their current cost of capital (i.e., at higher yields), providing a margin of safety on their new investments against the elevated interest rate levels. Meanwhile, with their considerable global and business diversification, BIP and BEP are able to sell assets wherever market sentiment is favorable and recycle that capital into places where asset pricing is most opportunistic, helping to offset headwinds driven by rising interest rates and keeping their asset recycling machine going.

- The vast majority of BIP's and BEP's debt is at the asset level. As a result, if any of their assets struggle and/or fall to a value that is less than their debt on that asset, BIP and BEP can easily just hand back the keys to the lender and move on, effectively providing a put on their aggregate portfolio value in the face of potential damage caused by higher interest rates.

- BIP and BEP have a BBB+ credit rating which gives them access to debt at relatively attractive interest rates and helping to blunt some of the impact of rising interest rates. It also means that if the capital markets do go into a period of distress that causes junk bond yields to spike, BIP and BEP should be well protected from that happening to their cost of debt.

- BIP and BEP have a built-in margin of safety given their economic equivalency to BIPC and BEPC. BIPC's and BEPC's very large premiums to BIP and BEP mean that BIP and BEP can issue BIPC and BEPC shares to fund acquisitions and/or repurchase BIP and BEP units. Given that BIP and BEP can sell BIPC and BEPC at a premium price to BIP and BEP, but both are economically equivalent, it means that every time it does this it is a value-accretive event for BIP and BEP unitholders, giving us additional margin of safety and providing management with an easy vehicle for driving growth for BIP and BEP unitholders.

Investor Takeaway

BIP and BEP are facing a lot of negativity in the market today due to rising interest rates and concerns that it will grind their growth engines to a halt. However, for the reasons stated in this article, we believe that they are well-positioned to continue churning out strong growth, even if it is slightly blunted by rising interest rates. As a result, we believe that both are very attractive buys right now as investors who buy today will likely enjoy attractive income today and strong income growth and generous total returns for years to come.

Note that while BEP and BIP issue a K-1 tax form, they are structured to not generate any UBTI and therefore should be suitable for inclusion in an IRA or 401k account (note this is not tax advice; please speak with Investor Relations and/or a tax expert to confirm). Moreover, they both also have economic equivalent shares in BEPC and BIPC that issue 1099 tax forms instead of K-1s. However, these securities typically trade at a large premium to their K-1 counterparts, so keep that in mind when deciding which one to purchase.

For further details see:

High-Yield High-Growth SWANs On Sale: Brookfield Renewable And Brookfield Infrastructure