LOW - Hillman Solutions: Navigating A Tough Housing Market

Summary

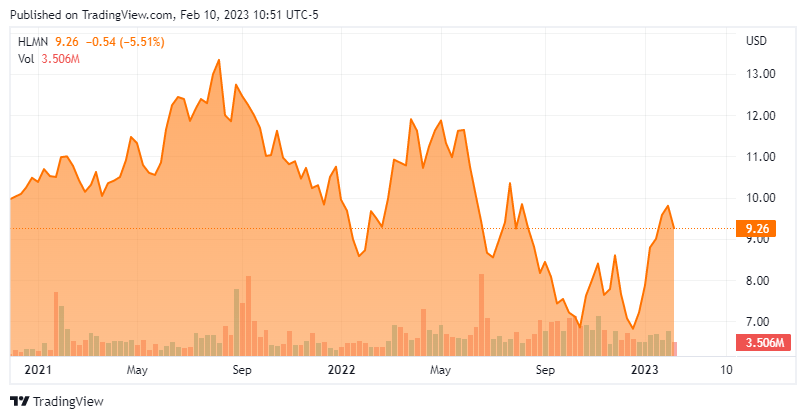

- Shares of home improvement store supplier Hillman Solutions Corp. are down 30% from their June 2022 high, but have been rallying recently.

- The company enjoys the number one market position in fasteners, keys, and protective gear, yet has managed to grow revenue in 56 of 57 years through outstanding customer service.

- The recent c-suite insider buying merited further investigation.

- A full investment analysis follows in the paragraphs below.

Do not let us mistake necessary evils for good. ” ? C.S. Lewis.

Today, we look at a company that has been a ridiculously consistent performer for over a half century even as the firm just came public in late 2020. Fears of recession have knocked its stock down substantially in recent quarters, which has brought in some recent insider buying. An analysis follows below.

{kind=link}

Company Overview:

Hillman Solutions Corp. ( HLMN ) is a Cincinnati, Ohio-based provider of hardware-related and home improvement products, protective gear, and key duplication services to ~42,000 hardware stores, home centers, and other retailers in North America. It manages ~112,000 SKUs – mostly for repair, remodeling, and maintenance projects – out of 22 distribution centers, with ~90% of its revenue derived from company-owned brands. Hillman was founded in 1964 and went public in July 2021 when it reverse-merged into special purpose acquisition company Landcadia Holdings III with its first trade conducted at $11.99 per share. Its stock currently trades just above nine bucks a share, translating to a market cap of $1.8 billion.

November Company Presentation

The company operates on a 52-53 week fiscal year ((FY)) ending the last Saturday in December.

Concentration

Hillman Solutions Corp.'s biggest accounts are Home Depot ( HD ) , Lowe’s ( LOW ) , Ace Hardware, and Walmart ( WMT ) , which contributed 27%, 21%, 11%, and 7% of FY21 sales, respectively.

Approach

With a huge SKU count that provides a ubiquitous presence throughout its accounts, Hillman defends its turf with an ~1,100 person-field sales and service team that provides in-store set-up and stocking services at its customer locations, allowing their clients to focus their resources elsewhere. This embedded arrangement allows Hillman to ship ~80% of its SKUs directly to the store, bypassing its accounts’ distribution centers; thus increasing product-to-shelf speed while reducing retailer shipping and handling costs. Another byproduct of this approach are very high fulfillment rates (96% in YTD22) on customer shelves. As such, it has received numerous vendor of the year awards from its largest accounts and has grown its top line 56 out of its 57 years in business (2009), building a competitive moat along the way.

Although it can be argued that fasteners are commoditized products, big home improvement retailers like Home Depot (HD) are not going to throw Hillman out on price if it means their own employees will have to keep the fastener shelves stocked and orderly. Despite its established position, Hillman Solutions management believes it can grow EBITDA at a 15% clip (10% organically) and revenue at 10% (6% organically) over the long term.

Segments

The company views its operations through three segments: Hardware and Protective Solutions [HPS]; Robotics and Digital Solutions [RDS]; and Canada.

HPS consist primarily of fasteners, anchors, specialty fasteners, and personal protective equipment including gloves and eye-wear. It is the number one supplier of both hardware solutions and protective solutions in North America. The segment accounted for Adj. EBITDA of $80.6 million on revenue of $818.1 million (72% of total) for the first 39 weeks of FY22 ending September 24th (YTD22) versus Adj. EBITDA of $95.8 million on revenue of $775.5 million in YTD21.

RDS is comprised of key copying, pet tags, automobile fob and RFID fob duplication, as well as knife sharpening and locksmith services. The key copying and pet tags (as well as name engraving) are provided via self-service kiosks, with all services supported by a team of sales and service professionals. Unsurprisingly, Hillman is the number one North American provider in this segment as well. RDS was responsible for YTD22 Adj. EBITDA of $63.7 million on revenue of $192.2 million (17% of total) versus YTD21 Adj. EBITDA of $64.6 million on revenue of $189.7 million.

The Canadian geography provided YTD22 Adj. EBITDA of $21.0 million on revenue of $125.3 million versus Adj. EBITDA of $8.4 million on revenue of $116.2 million in YTD21.

As for consolidated Hillman, it earned $0.38 a share (non-GAAP) and Adj. EBITDA of $165.3 million on revenue of $1.14 billion in YTD22 against $0.49 a share (non-GAAP) and Adj. EBITDA of $168.8 million on revenue of $1.08 billion in YTD21. This performance is a function of price increases lagging its cost inflation.

Share Price Performance

The question surrounding Hillman is its ability to grow, given its number one positions in most of its product lines and its already pervasive footprint inside most of its customers’ stores. As it adds to its remarkable record of consistent growth, it becomes increasingly more difficult to outpace the economy or its already established customers. It requires more new customer wins and additional shelf space through the design or acquisition of adjacent SKUs.

With a significant amount of its products for resale manufactured in China and Taiwan, Hillman has endured supply chain bottlenecks, raw material inflation, and higher freight costs, which have impacted financial performance. However, it has pushed through four price increases in the past 18 months enabling it to offset ~$225 million of cost increases since the onset of FY21. The company also had the foresight to raise its inventory levels during FY21, from $391.7 million at the onset to $533.5 million at the close, which it has maintained ever since, allowing it to raise order fulfillment rates from 90% in FY21 to 96% in YTD22 and seize additional market share.

However, with the Fed raising rates and perceptions of softening demand, shares of HLMN are down nearly 30% since early June 2022, when they got a bump on the announcement that the company was being added to the Russel 3000. That said, the selloff has been very orderly, with no one-day 10%+ downdrafts during the retreat. In other words, shares of HLMN have been victimized by a down tape and multiple compression that have impacted most stocks with perceived exposure to a 2023 recession. They have shown some legs during the first six weeks of 2023, however.

3QFY22 Results & Outlook

Signs of that softening demand were brought to light on its Q3 FY22 earnings report of November 3, 2022, when the company posted 3QFY22 earnings of $0.14 a share (non-GAAP) and Adj. EBITDA of $59.0 million on net sales of $378.5 million versus $0.13 a share (non-GAAP) and Adj. EBITDA of $56.5 million on net sales of $364.5 million in 3QFY21, representing improvements of 8%,4%, and 4%, respectively. The bottom line beat Street consensus by $0.04 (as it did in the prior quarter) while the top line was $8.8 million shy of expectations. Compared to pre-pandemic levels (3QFY19), Adj. EBITDA improved 16% while net sales increased 19%.

November Company Presentation

That said, Hillman achieved these results because higher pricing slightly outpaced softer demand. As such, it was unable to meaningfully lower its inventory – down ~$40 million sequentially but essentially flat versus YEFY21 – compelling management to lower its FY22 cash flow forecast from $125 million to $80 million, its Adj. EBITDA estimate from $217 million to $209 million, and its top-line outlook from $1.55 billion to $1.48 billion, all based on range midpoints.

November Company Presentation

Balance Sheet & Analyst Commentary:

On September 24, 2022, Hillman Solutions Corp. held cash and equivalents of $29.2 million and debt of $951.3 million (weighted average interest rate of 4.6%) for net leverage of 4.5. The company does not pay a dividend nor repurchase shares. Management is currently focused on lowering its leverage and inventory levels as the supply chain normalizes.

November Company Presentation

Street analysts are unanimously impressed with Hillman’s consistent performance despite the miserable macro backdrop, bestowing the HLMN stock with four buy and five outperform ratings, although their median price target has fallen from $15 to $10.75 to reflect expectations of a recession in 2023. Also, on average, they are skeptical on its growth prospects for FY23, expecting the company to earn $0.37 a share (non-GAAP) versus $0.44 in FY22 with revenue flat at $1.48 billion.

Although Hillman’s stock didn’t react severely to its 3QFY22 financial report, the c-suite used the end of November as a buying opportunity with the CEO, CFO, and CTO collectively purchasing 207,000 shares between $7.50 and $7.75 per share. That said, Hillman Solutions Corp. stock did drift below $7 post-purchase.

Verdict:

The overlooked aspects of Hillman Solutions Corp.’s business model are that its products are both consumable and geared toward the repair, remodel, and DIY market. This positioning should allow it to weather a recession better than those providers comparatively more exposed to housing starts in a higher interest rate environment. That said, if Street analysts are correct on their FY23 forecast, its stock is not cheap, trading at north of 20 times next year’s earnings and at an EV/TTM Adj. EBITDA of over 13.

Hillman Solutions Corp. is a very good company with solid management, and it should see a margin tailwind from falling commodity and freight prices in FY23. However, its growth prospects are somewhat tempered over the next year, and given that there is no high-growth scenario for this steady company exiting any recession, Hillman Solutions Corp. stock has more (or similar) downside risk than (as) upside potential. As such, we will take a pass.

Love without sacrifice is like theft ”? Nassim Nicholas Taleb.

For further details see:

Hillman Solutions: Navigating A Tough Housing Market