CA - HIVE's Resilience Shines Through Challenging Crypto Landscape

2023-04-17 18:48:39 ET

Summary

- HIVE's mining operations are diversified in Canada, Iceland, and Sweden, taking advantage of attractive power costs and renewable energy sources.

- The average cost of production per Bitcoin for HIVE was $13,599 for the quarter ending December 31, 2022, representing a 37% increase from the previous quarter.

- Despite the recent rebound in crypto, HIVE's stock performance has lagged behind Bitcoin tokens, suggesting that investors may find more value in the token or other mining companies.

It has been a turbulent year for Bitcoin ( BTC-USD ) mining companies like HIVE Blockchain ( HIVE ). HIVE is one of the smaller miners in the industry, but notable differences made it an interesting pick going into a macroeconomic slowdown. As expected, the massive selloff in Bitcoin brought the stock down to historic lows, but with the Federal Reserve making notable progress in its fight against inflation and a possible pasta interest rate increase on the cards, the stock does not seem to be performing as well as one would like. Today, will look at HIVE Blockchain and see if the company has underlying problems or if the stock lacks publicity.

Miners Getting Hammered

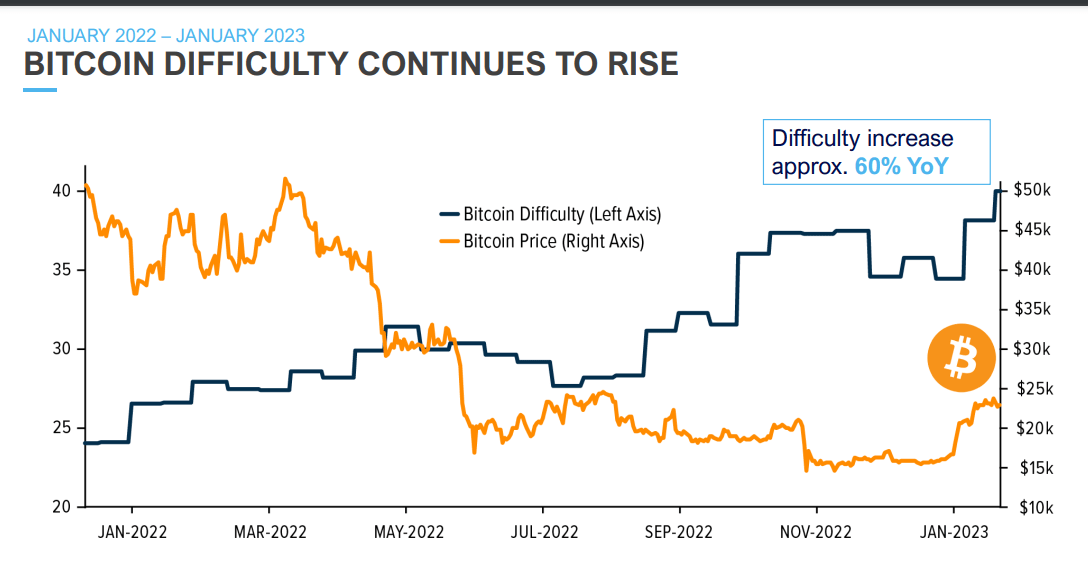

One of the age-old debates with Bitcoin mining company investments has been whether it is better to buy the token or the mining company's stock. There are essential dynamics to remember when making this deliberation. Investors often point to the fact that the Bitcoin supply is being diluted daily, which is true. But as most investors know, Bitcoin's difficulty rates increase as more tokens are mined.

{kind=link}

On the other hand, mining companies tend to rely on financing and secondary offerings to fund operations as they wait for advantageous prices to sell their tokens. As you can see below, HIVE has been no exception to this rule. It is important to note that this is understandable. If one is expecting outsized returns for Bitcoin, then it makes sense for the company to offer shares in the short term to preserve its treasury and reap future rewards.

While HIVE has been selling Bitcoin to help fund operations, it also benefits from building out its comprehensive mining fleet in low-cost regions. As a result, production figures have improved significantly over time, and the company can now sell tokens while maintaining a good treasury. Below, we can see the production figures from November through January.

| Month | Bitcoin Produced | Average Bitcoin per Exahash | Income from Grid Balancing ((USD)) | Additional Information |

|---|---|---|---|---|

| Quarterly Revenue | ||||

| $14.3 million | ||||

| Gross Mining Margin | ||||

| $3.6 million | ||||

| Adjusted EBITDA | ||||

| $1.5 million | ||||

| HPC Revenue Strategy Annual Run Rate | ||||

| $1.3 million | ||||

| Bitcoin Mined in Recent Quarter | ||||

| 787 | ||||

| Bitcoin Mined in the Same Quarter Last Year | ||||

| 697 | ||||

| YoY Bitcoin Production Increase | ||||

| 13% | ||||

| Average Cost of Production per Bitcoin (excl. SG&A) | ||||

| $13,599 | ||||

| Cost of Production Increase from Last Quarter | ||||

| 37% |

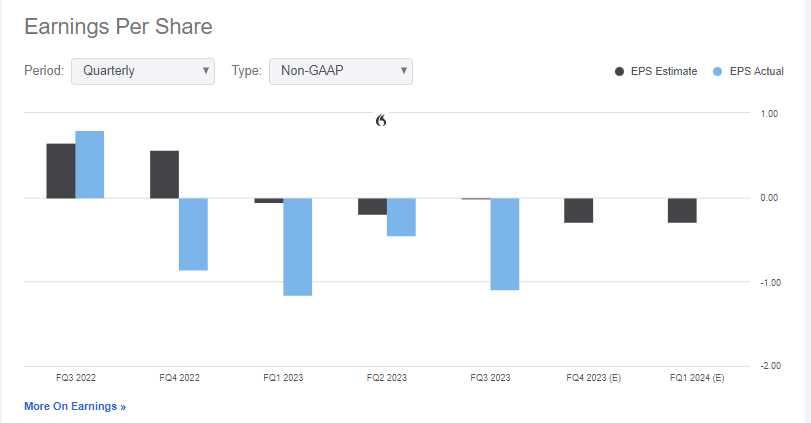

But on the other hand, we have seen some truly terrifying EPS numbers. This has been standard across the industry since impairment changes and the crypto crash.

{kind=link}

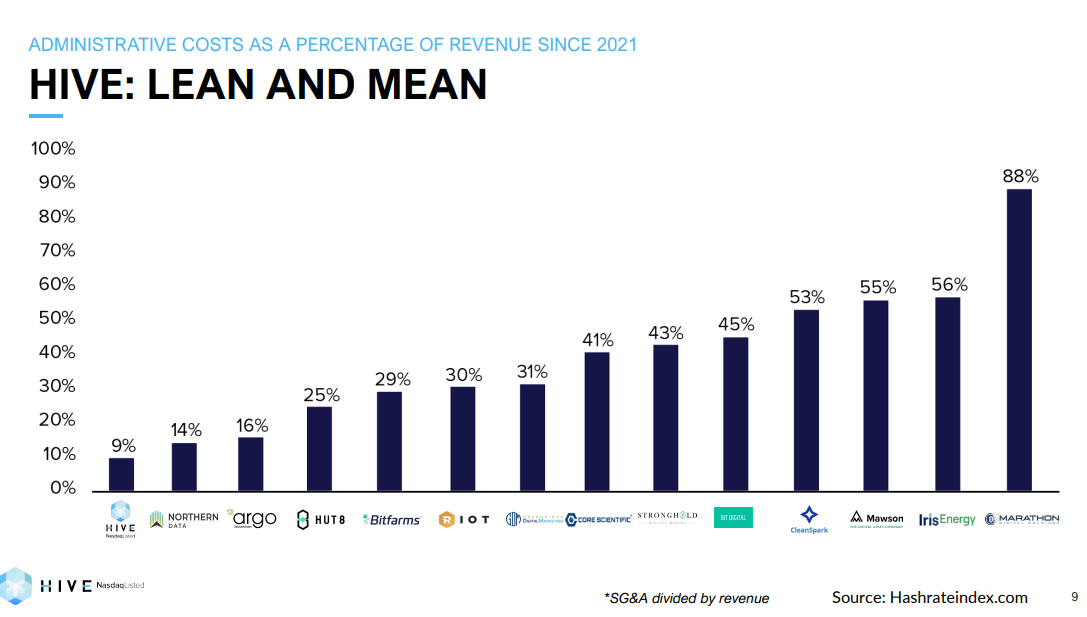

HIVE prides itself on efficient operations, and we can see that admin costs have been controlled despite notable growth for the company.

{kind=link}

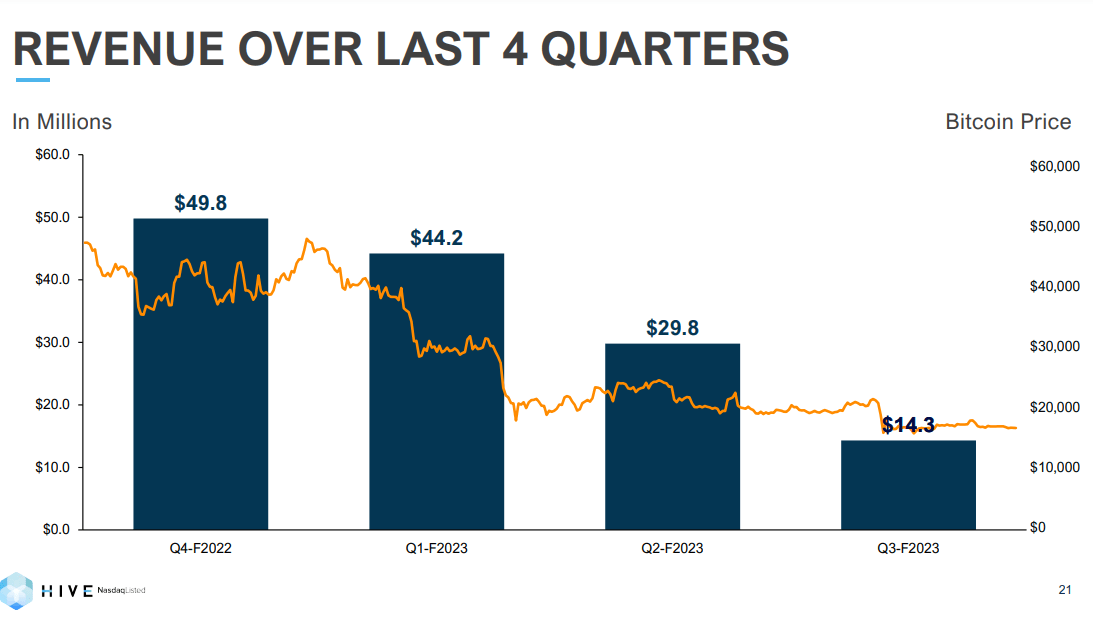

As one would expect, revenue fell significantly with Bitcoin prices, but the reverse would also be true if the company makes it to the other side of this crypto winter, which makes what the management team has been achieving even more important.

{kind=link}

Challenges in the Future

It is unlikely that the crypto market is completely out of the woods despite the strong rebound. People have been prematurely celebrating the end of inflation due to the recent achievements of the Federal Reserve, but it is likely that interest rates to remain elevated throughout the end of calendar year 2023. The Federal Reserve has made it clear that rate cuts are not in their base case for the end of the year though I suspect we may see one or two cuts due to the recent banking crisis and the general unwillingness to spark a needless recession. If inflation were to become sticky, forcing the Fed to do more damage to the economy to cool down prices, then that would be catastrophic for smaller growth stocks like HIVE.

HIVE's fleet is also geographically located in Canada, Iceland and Sweden. Many countries have been facing energy crises due to the Russia - Ukraine conflict but interestingly, Iceland and Sweden derive a significant portion of their energy supply from renewable sources, which has made them a great pick for miners. This was not by accident, the HIVE management team has been deliberate about where they deploy their miners, and investors are now seeing some benefits from this strategy.

Valuation and Forward-Looking Commentary

We can see in the charts below that the stock is trading near historic lows, but the valuation makes sense because of the widespread uncertainty in the crypto mining industry, Bitcoin prices and the macroeconomic outlook in short to medium term.

One of the major concerns gripping the industry right now is liquidity. Following the issues that have hit Core Scientific, which was among the biggest producers in the industry, there is a feeling that no Bitcoin mining company can be completely safe right now. As I mentioned earlier, HIVE is one of the more responsible names in the industry, but it is not immune to the profound impact of a prolonged depressed crypto bear market. Operating losses can pile up quickly as energy prices, the need to sell Bitcoin holdings, and a depreciating mining fleet can take a toll. The good thing is a strong upward move in Bitcoin will solve all the problems that matter if these companies can maintain a good treasury. Nevertheless, there isn't an awful lot of cash here in the event that HIVE has to weather an extremely long crypto bear market.

We can also see that the stock has not performed reasonably well despite the strong rebound in crypto. In fact, Bitcoin tokens have outperformed the stock, which is problematic when you consider the additional risks associated with the miners like dilution, regulation etc.

This is perhaps the most detrimental issue for HIVE. I like to think of Bitcoin mining companies as call options on their underlying token where theta decay is, in essence, the dilution. For this reason, I would expect negative variance when the token is going through a turbulent stint but would expect the stock to outpace the token on strong rebounds. We are not seeing this dynamic right now, which for me, suggests it is better to buy the token or another mining company.

The Takeaway

In closing, HIVE has demonstrated efficiency in its operations and strategic choices in its geographic locations, allowing it to navigate the challenges faced in the crypto-mining industry. Despite its achievements, HIVE's stock has not performed well during the strong rebound in the crypto market. This underperformance, combined with the risks associated with mining companies, such as dilution and regulation, is prohibitive right now. I respect what the management team is doing, but we aren't seeing the stock reflect that just yet. The stock likely needs a bigger move in Bitcoin to attract more attention to the space, which may not come soon. This was one of my picks for a recession, and in many ways, it still is, but for now, there a no great reasons to buy or sell if you're bullish on Bitcoin. I rate the stock a hold.

For further details see:

HIVE's Resilience Shines Through Challenging Crypto Landscape