RDFN - Housing Market 2023: How To Navigate Between Industry Optimism And Macro-Economic Headwinds

Summary

- Despite recessionary market conditions, earnings reports from the industry are full of optimism.

- Stocks priced in recession at last year's lows and are now discounting a lot of today's optimism as shown in reports from Lennar, KB Home, LGI Homes, and Redfin.

- The recent breakout in the iShares U.S. Home Construction ETF further underlines the current optimism and supports the seasonal trade in home builders.

- Looking past today's headwinds, slowing household growth will likely be the next big challenge for home builders and transactional players.

“We have been wrong so far. We thought it’s going to get better and it’s gotten worse.”

LGI Homes – Q3 2022 Earnings Conference Call , November 1, 2022

The above words from LGI Homes ( LGIH ) during its last earnings conference call serve well as an important footnote to commentary on today’s housing market. The current conditions are unfamiliar relative to recent history. That unfamiliarity can either bolster confidence in the temporary nature of today’s challenges or it can breed concerns that the end must be nowhere in sight. In the middle, are the participants looking to the Spring selling season to provide guidance. A realtor in Missoula, Montana recently told Marketplace that “many people are waiting to see what happens with the spring market before pulling the trigger on buying or selling a property.” In that same broadcast, a realtor in Lake Tahoe, California explained why prices remain near all-time highs, “We have a lot of sellers in our market that are sitting on piles of equity … and they’re not motivated to sell.” In other words, broad and bold predictions do not fit the moment. Instead, this is a time for modest observations, flexibility, and responsiveness. That approach guides my outlook on the housing market as I navigate between the notable optimism of industry participants and the increasing macro-economic pressures.

Rebounding Builder Sentiment

An on-going housing recession has given market participants time to normalize deteriorating economic and business conditions for housing. On the other hand, the persistent strength in the labor market and on-going supply tightness in many markets help sustain residual optimism among publicly traded builders. That lingering optimism finally translated into January’s small rebound in builder sentiment off the 2020 pandemic low , the first monthly uptick in sentiment in 13 months. In December , the National Association of Home Builders (NAHB) interpreted the slowing pace of decline in sentiment as an indicator of an imminent bottom in builder sentiment. For January, the NAHB optimistically looked ahead:

“It is possible that the low point for builder sentiment in this cycle was registered in December, even as many builders continue to use a variety of incentives, including price reductions, to bolster sales. The rise in builder sentiment also means that cycle lows for permits and starts are likely near, and a rebound for home building could be underway later in 2023.”

If true, then the lows for home builder stocks last year likely priced in the base case of a housing market recession. The market could even muddle through a recession in the broader economy assuming economic weakness pressures mortgage rates lower as the Federal Reserve rolls back some of its rate hikes. Some demand pent-up since last summer could step back into the market on lower rates.

A prelude to the possibilities appeared after the 30-year mortgage peaked in November. New single-family home sales jumped sharply back to the summer highs. Mortgage applications have experienced several week-over-week gains since then. The Mortgage Bankers Association (MBA) even reported a seasonally adjusted surge in mortgage applications in its latest weekly report . The 34% week-over-week gain pales in comparison to the 35% year-over-year decline, but this change in momentum is a classic dynamic of a bottoming process.

The 2023 Playbook

Home builders learned valuable lessons coming from the bust in the Great Financial Crisis ((GFC)). Over time these lessons have helped bolster optimism for meeting market challenges. Those lessons served them well during major demographic shifts and increasing supply scarcity going into the pandemic and especially in the over-stimulated early pandemic days. Public home builders are generally financially strong and nimble. Profits from the Fed-induced housing mania are today’s cash cushion on the balance sheet. Home builders followed similar playbooks over this time period. Now, they share a playbook that accommodates the rapid reversal in the Fed’s accommodative policies.

- Increase sales and marketing even at the cost of higher SG&A.

- Adjust base sales prices, increase incentives, and provide mortgage rate buydowns to maintain or regain sales momentum – intensity dialed on a per community basis.

- Burn down excess margins from the peak of the housing cycle to price closer to the market.

- Slow starts to align with demand.

- Shorten the time from order to delivery (reduces interest rate risk).

- Maximize cash flows by converting backlog and maintaining order flow.

- Pull back on land purchases; negotiate land prices down or else walk away even at a loss.

- Use leverage over the supply chain to drive down costs (the supply chain is less stressed with housing starts contracting).

- Provide minimal guidance for fiscal 2023 using wide ranges to reflect on-going uncertainty.

Each builder of course has some variations on these themes. Spec builders like LGI Homes are not burning down inventory and are more focused on keeping traffic flowing through the door. Other builders like D.R. Horton ( DHI ) have increased specs but still maintain a substantial backlog.

In the next three sections I reflect on builder optimism using use the recent earnings reports of three home builders: Lennar Corporation ( LEN ), LGI Homes, Inc, KB Home ( KBH ).

Lennar Corporation

During its Q4 2022 earnings conference call , Lennar looked forward into 2023 with firm optimism: “We are prepared once again to look adversity square in the eye and stick to our strategies and pull out a big win.” Accordingly, Lennar is expecting a bottom for margins in Q1 and flattish deliveries for the year (with a wide range of 60,000 to 65,000). Per the “playbook”, Lennar did not quantify any other full year guidance.

Because home builders were quick to respond to recessionary conditions, the supply crunch that defined the last cycle is likely to return at the other side of the recession. Lennar expects housing starts for “single family and multifamily dwellings nationally will be down between quarter to a third in 2023, exacerbating the national housing supply shortage.” This reason is almost sufficient to keep home builders on the investing list during whatever market sell-offs are to come. Builders are likely looking forward to an eventual return of pricing power.

Note that the large sequential jump in December that took starts back to last summer’s levels may yet betray a residual optimism misaligned to current economic conditions. For example, Lennar does not expect its own starts to plunge. Lennar’s starts in 2022 were just 1% off levels from the previous year. The company appears eager to use its starts to take market share under tight capital markets: “a very sizable portion of starts for next year are going to be under limitation.” So a surprisingly strong spring selling season could reignite starts across the industry.

Lennar’s optimism is also embedded in the expectation of a shallow housing recession: “…a fairly short duration correction without an inventory overhang to resolve.” Similarly, Lennar believes its cancellation rate has already peaked: “our cancellation rate peaked in October, declined significantly in November, and we’ve seen a continued reduction thus far in December.” Getting cancellations back under control leads to more confidence in expectations.

Using incentives and base price concessions helps secure more deliveries. Lennar acknowledged that the company is not expecting an increase in ASPs this year (if anything, I have to assume at least a small decline in ASPs). However, Lennar directly refuted a rumor that the company implemented “bulk sales at discounted rates to clear inventory.” Such a move would not make sense given the destructive impact it would have on the rest of its inventory at the related communities. KB Home discussed these dynamics at length in its earnings conference call. On the order side, Lennar will continue to press forward and thinks its digital marketing provides a key competitive advantage.

Lennar will also flex its muscles in the marketplace to maintain cash flows: “Make no mistake, Lennar led the way with reduction in margin, while maintaining volume and increasing market share as the market has corrected. We expect our trade partners to work side by side with us and follow suit… As with our trade partners, our land partners or sellers understand that we are maintaining volume and increasing market share while taking the first hit to our margin. They will need to work together and participate or we’ll need to move on… you really can’t underestimate the leverage that we get in working with our trade partners as things slow down across the board. People are looking for work.”

This relaxing of constraints in the supply chain is exactly what the Federal Reserve wants to see come from its monetary tightening. An unfortunate side effect could be the increasing dominance in the marketplace of the biggest and best capitalized players in the supply chain.

LGI Homes

LGI Homes not only intends to generate positive cash flow in 2023, but also the company plans to continue growing community count into 2024 at a healthy clip. In the Q3 earnings conference call , the company announced it would grow 2023 and 2024 community counts 20-30% each year. LGI Home will even hire more people to support this growth. Despite missing its guidance for Q4 and full-year closings , I expect the company to proceed with its growth plans. In the conference call, management declared “we think those numbers should be conservative and we are confident in that community count growth”. Q4 closings of 1,448 homes came under the extremely wide 1527 to 1927 range implied in the Q3 2022 earnings report .

LGI Homes said its balance sheet largely reflects the investments needed for this growth. So the company in a sense needs to make the growth happen to properly leverage its assets. Like Lennar, LGI Homes is ramping up its marketing efforts to get order flow. The company reported immediate and impressive results:

“As we said on the last call, we have ramped up our marketing efforts to find qualified buyers. This continued in the third quarter and we saw positive results with over 74,000 leads, an increase of 72% over our prior quarter… Net orders were up 77.8% sequentially, illustrating our success driving more leads through increased advertising spend as well as our ability to implement the right combinations of incentives needed to qualify more customers.”

The company has also managed to drive cancellation rates significantly downward from 43.1% in Q3 2021 to 30.5% in Q2 2022 to 21.3% in Q3 2022. LGI Homes describes the current cancellation rate as its normal rate.

Per the playbook, LGI Homes will draw down on the record third quarter margins it achieved in Q3 2022, “We don’t anticipate getting to 20% or below type of gross margin. We plan on getting back to our historical range of 25% to 28%”. The process of “normalizing” margins enables the company to price with the market. Management acknowledged that competitors around them are lowering prices. Margins instead of ASPs will be a better measure of pricing power as customers are choosing smaller floor plans to achieve affordability.

Overall, the growth plans for LGI Homes demonstrate an abiding optimism even if sales will make lower margins in the near future.

KB Homes

KB Homes was the latest home builder to report earnings. The company underlined the playbook. I summarize the Q4 earnings conference call with bullet points.

- Only revenue for full-year guidance and a wide range: $5B to $6B (“supported by… backlog and growing portfolio of open selling communities”) … “A lot of the remainder of the year just depends on what the Spring selling season holds, both in terms of new sales and what it takes to close out our current backlog… we didn’t guide and just prefer to keep it that way until we see what the Spring holds for us in the market.”

- “Healthy” cash flow from a “materially lower” land spend and improved build times from a less constrained supply chain.

- Missed delivery guidance on a combination of concerning (in bold) and familiar issues: “a combination of cycle time extensions at the latter stages of construction, higher cancellations on homes that were close to or at completion and ongoing challenges with utility companies in getting communities and homes energized.” KBH even suffered cancellations from buyers who locked in mortgage rates. Still, the company reported its cancellation rate is still trending downward even with a small sequential increase in the quarter.

- Gross and net orders plunged year-over-year 47% and 80% respectively. Net orders declined 72% year-over-year in the first five weeks of the current quarter. These challenges occurred despite sacrificing margins to discount prices close to other builders. KBH’s massive backlog constrained pricing actions since the company wanted to avoid a cascade of concessions on its 7,600 home, $3.7B backlog.

- KBH plans to leverage industry-wide reduction in starts to negotiate lower supply chain costs and achieve faster cycle times. Again, this is the Fed’s rate tightening at work.

Of the three builders, the KBH story of optimism ranks at the bottom of the list since it will take another earnings cycle to prove that cancellation rates are indeed trending downward. KBH reads as most dependent on its backlog to meet full-year guidance so cancellation rates are extremely important. The builder also continues to suffer from familiar operational problems.

The Redfin Market Report

I reviewed the Q3 2022 earnings conference call for Redfin ( RDFN ) to get a non-builder perspective on the transaction market. The company included the unfortunate announcement that it laid off another 13% of its staff, bringing layoffs since April to 27% of the company. The company also officially announced the close of Redfin Now. Combined, that news aligns with the significant decline in orders that the home builders reported. Despite these challenges and predictions of on-going market softness, the company aligned with the optimism with its industry contemporaries.

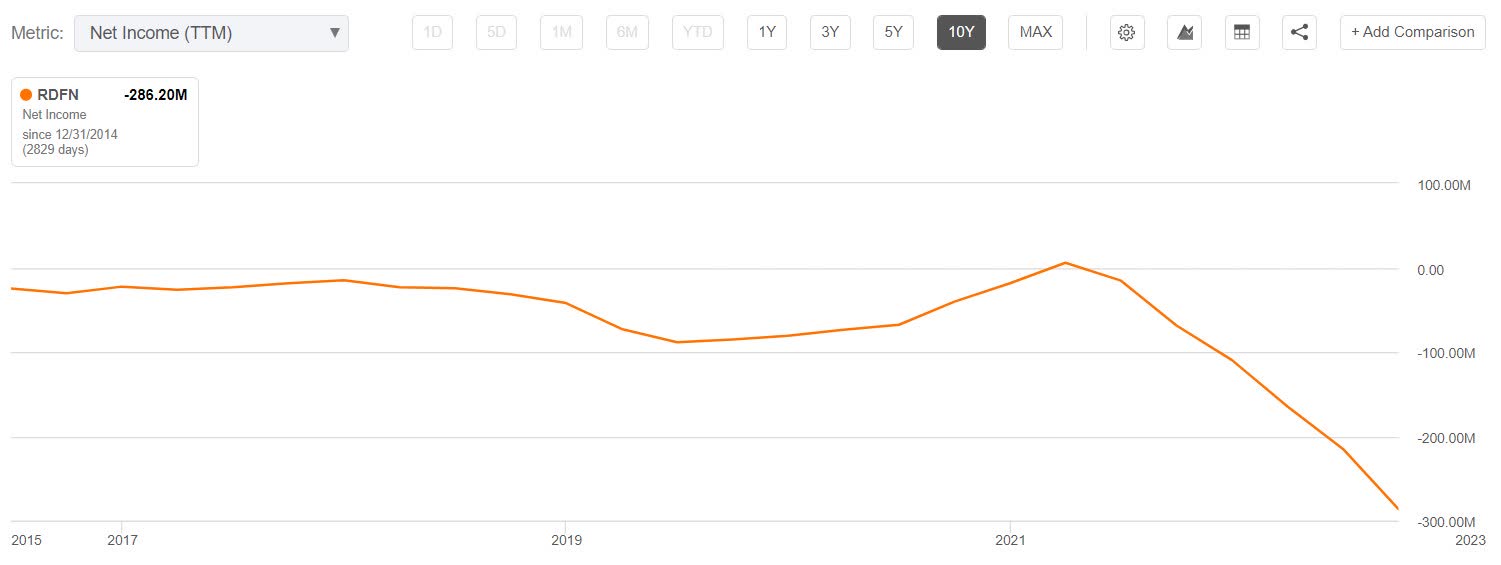

Redfin’s base case for the housing market is a slowdown that lasts through 2023. Yet the company claims it is now sized to make positive EBIDTA even if sales drop to levels last seen during the Great Financial Crisis. Redfin even expects to achieve positive net income by 2024. The chart below shows the huge stretch ahead for Redfin. Net income briefly flatlined two years ago and descended rapidly from there.

{kind=link}

Redfin has a deep hole to fill in net income. (Seeking Alpha)

New single-family home sales are still about 50% above the trough levels from the GFC. Existing home sales are on trend to drop to GFC lows because the market largely lacks motivated or interested sellers. For example, outside of “pandemic boom towns” like Boise, Idaho, Redfin expects “prices to be more stable, because homeowners have more equity today than in 2008, allowing many to set out this downturn.” This observation is consistent with the realtor commentary I quoted earlier. Redfin pointed to builders and iBuyers as the motivated sellers because of the cost of capital: “builders and iBuyers face higher holding costs and are now the ones forcing prices down in an otherwise deadlocked market.”

Affordability will continue to loom heavy over the housing market. Redfin posted some stark statistics:

“From October 2020 to October 2022, the monthly payment for an American family buying the median-priced home increased by 71%. For that same family to rent a median-priced apartment the monthly payment increased by 24%, still far faster than income growth.”

Buyers first stared down soaring prices from a mania of buying. Now they are staring down even higher total costs because of a mania in interest rates. It will take time for the market to rebalance and truly normalize across costs, income, and savings. Even assuming 2023 is a trough year, the path upward should be slow and long.

The bottom line of Redfin’s optimism came when management declared that the market and economic challenges should not generate concern about the company going out of business:

“The overriding concern our investors have is whether we can get through this downturn without running out of money. We will pay our debts come heck or high water and will keep growing. Redfin’s still regional listing search site can gain on its rivals for years to come. Our rental business can double. Our brokerages progress on close rates and loyalty sales can send our share through the roof. Our lending and title business can print money.”

Risk to the Optimism: Household Formation

A week ago the Joint Center of Housing Studies of Harvard University (JCHS) published a study titled “ The Surge in Household Growth and What It Suggests About the Future of Housing Demand .” JCHS found that “three household surveys released over the past few months by the Census Bureau all show nearly unprecedented levels of household growth from 2019 through 2021… Much of the acceleration in household growth was driven by a pickup in growth among millennials, continuing a longer-term trend that has been building since 2016.” Household growth soared from an average 1.4M to 1.5M between 2017 and 2019 to 2.0M to 2.4M between 2019 and 2021. Back in 2014, I covered the prospects for the expansion of millennial household growth as part of a bullish case for home builders. In the years going into the pandemic, home builders often referred to this expansion. However, the next juncture in this dynamic may be near.

The JCHS identified wage increases, stimulus payments, and student loan relief as primary factors fueling the acceleration of millennial household growth. Each of these factors are either gone or waning. The headship rate, the share of the population leading their own household, went from “being a headwind to household growth in 2011-2016 to a tailwind in 2016-2021 [and] led to a significant surge in household growth, equivalent to a swing of 1.2 million additional households per year.” This recovery is likely near completion. So population growth will return as a primary driver of household growth. However, JCHS reported that “in each of the years 2019 , 2020 , and 2021 , the Census Bureau reported new 100-year lows in population growth.”

Thus, home builders will need to adjust to slower growth rates in coming years. That adjustment period represents a palpable risk to today’s optimism.

Conclusion

The optimism in the industry is encouraging. Yet, the downside risks are very real and substantial. Accordingly, home builders are not likely to sustain valuation premiums for the foreseeable future.

A price/book ratio of 1.0 or lower is typically considered recessionary pricing. Lennar fell below 1.0 in June, September, and October of last year. It now sits at 1.2 and was as high as 1.8 in 2021. KB Home typically trades at a discount to the industry and saw its price/book ratio fall below 1.0 way back in March. The ratio has yet to recover and still sits at 0.8. LGI Homes typically trades at a premium to the market given its high growth rates. Its price/book ratio last touched 1.0 at the very bottom of the pandemic. Since then, LGI Homes dropped to 1.6 last June and 1.1 last October. It is back to 1.6 now and was as high as 3.8 in 2021. D.R. Horton, which kicked off the seasonal strength in home builders , currently trades at 1.7 price/book and got as low as 1.2 last year. In other words, the market priced in a housing market recession last year and has slowly started to bake in some of today’s optimism.

{kind=link}

Lennar Corporation ( LEN ) is still trading toward the bottom of a historical 1 to 2 range for its price/book valuation. (Seeking Alpha)

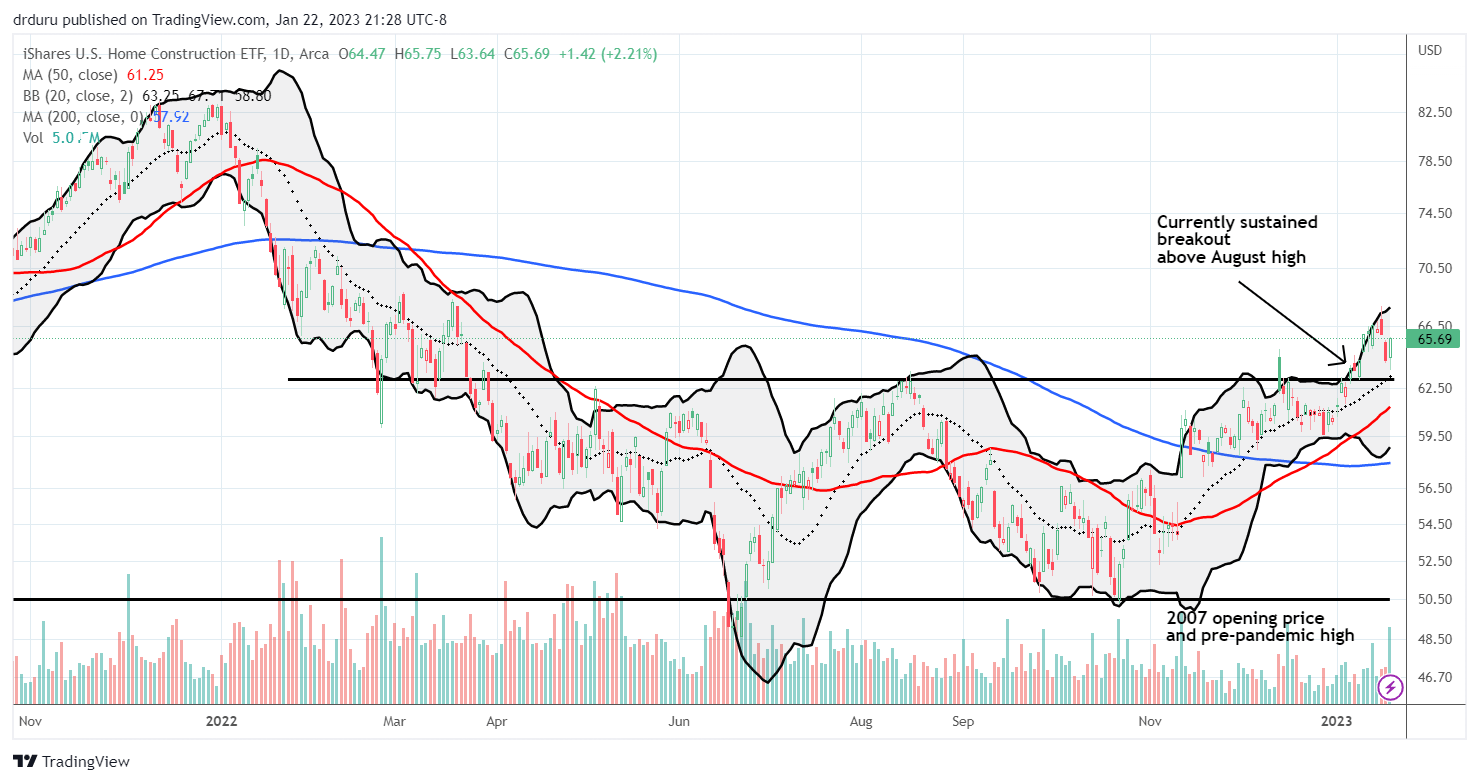

The technicals still favor home builders in general as seen in the iShares U.S. Home Construction ETF ( ITB ). ITB recently broke out to 10-month highs and is still in an uptrend as defined by both the 20-day moving average ((DMA)) and 50-DMA, the dotted and red lines below respectively. Until those uptrends break down, the seasonal trade in ITB will remain alive and well.

{kind=link}

The iShares U.S. Home Construction ETF ( ITB ) is sustaining an impressive breakout given recessionary conditions. (TradingView.com)

Assuming the seasonal trade ends somewhere around April, I think the headwinds for the housing industry will become more important and limit further gains. The unemployment rate may finally be on the move higher by then; the latest median projection from the Federal Reserve has the unemployment rate increasing to 4.6%. Even with that level expected to deliver a peak in the pain, the rise could still generate fresh concerns that slice through today’s optimism. Until then, be careful out there and keep in mind the introductory quote from LGI Homes!

For further details see:

Housing Market 2023: How To Navigate Between Industry Optimism And Macro-Economic Headwinds