BBBY - How I Was Completely Wrong About Bed Bath & Beyond

2023-03-09 17:49:53 ET

Summary

- 2 years ago I was way too optimistic on BBBY. I reflect on the mistakes I made and the things I missed in this article.

- Currently, I would not advise trading BBBY as book value is negative, and in the event of bankruptcy, most likely all the equity will get wiped out.

- In hindsight, a higher margin of safety in the valuation would have been appropriate and very much needed.

Roughly two years ago I wrote an article about Bed Bath & Beyond ( BBBY ) being undervalued based on Fundamentals. Well since then the price dropped 95.36% and this shows that I was not only off by a bit but by a huge margin. So for now let's revisit the thesis and the underlying assumptions and see where exactly I got it wrong.

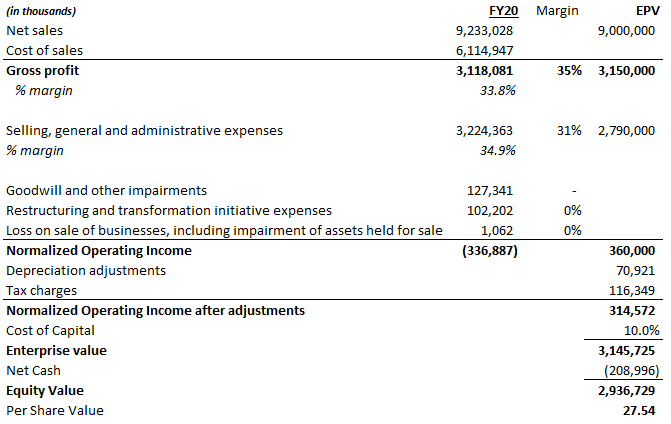

I valued BBBY based on asset value (reproduction value) and earnings power value. For the reproduction value, I tried to calculate the value, or the investment amount needed by a potential competitor to basically replace BBBY. When doing the recalculation the asset value really took a hit and went from $43.71 per share to $13.99 per share. See the table below for a short overview:

Author calculation and company filings

In the second step, I calculated the earnings power value which is where I was slightly too optimistic:

{kind=link}

I assumed sustainable net sales of $9bn for the years to come. In my defense, it was peak covid time and all sorts of factors were influencing performance but probably I was too naive and just thought the company will for sure get back on track and sales could keep up. However, this was not the case, as sales decreased to $7.8bn in FY22 and are currently at $6.2bn on an LTM basis. The Gross Profit margin is another debacle, while the company was able to hold the margin around 33% in FY22, the decrease to 26.14% LTM while the SG&A margin increased to almost 41% LTM. If calculated today I wouldn't even get to a positive normalized operating income.

However, getting assumptions wrong happens, probably the biggest mistake was the lacking margin of safety and the missing sensitivity analysis. Even at that time, a slight drop in the margin would have led to a completely different EVP, so even though I was conservative from a 2021 standpoint I probably focused too much on the asset value, and didn't consider book value at all. Moreover, I completely disregarded the debt in the sense that I did not check the debt maturity and footnotes in general.

I also checked back on the potential risks, and things not considered, section of the article and decided to review some major points:

- "The management might fail to successfully turn around the business and guide it back to profitable operating income. This would render the above analysis useless and the company at the current price would probably be overvalued." This turned out to be the most accurate thing in the article

- "I tried to be on the conservative side with my assumptions, however, the assumption might still prove to be too optimistic in which the valuation for the BBBY would be lower." I was indeed way too optimistic about the assumptions made and did not consider enough margin of safety.

- "I did not in detail assess the viability of the turnaround plan but I am bullish that it would work out and the management can make the company profitable again." How naive of me to just assume that, but I guess for a more numerical and valuation assessment it was okay at the time, but then I should've factored in this risk and required an even higher margin of safety

- "There might be other things I missed that could have a negative influence on the bull thesis." Indeed there were many other things, among them the huge debt load.

In general, it was a good learning experience and it taught me to be even more conservative and not value companies based on repurchase value but focus more on book value with a steep discount to get the appropriate margin of safety. I still managed to make a profit on the trade by averaging down and getting out on the last Cohen jump but this was all luck and had nothing to do with the analysis I did.

What now?

Currently, the company trades at $1.34, revenues are further declining, and operating loss increasing. Just considering the last 9 months they had negative cash flow from operating activities of $890m. Their Gross Profit margin decreased further to around 24.6% and their SG&A margin is at 44.6% which is the highest since 2003. The debt is still sky-high and despite best efforts, it doesn't look good for the future of BBBY. The last earnings call did not even have a Q&A session and it seems very likely they will need to restructure under Chapter 11. Of course, one could bet that they don't and maybe profit, but that's all up to the individual. For now, book value remains negative, so I think the debt will eat all the equity unless they can sell Buy Buy Baby or other assets for a good price.

Thanks for reading my reflection.

For further details see:

How I Was Completely Wrong About Bed Bath & Beyond