CA - How To Supercharge Your Portfolio With Apollo And Other Alt Managers

Summary

- High-growing and sizable alt management industry is not represented in the S&P 500 index today. Adding individual alt managers to diversified portfolios should benefit investors.

- APO's biggest differentiator is full ownership of Athene, a retirement specialist. Population aging represents a powerful tailwind for Athene.

- APO may be the only high-growing alt manager trading on a value basis.

- Due to its size and corporate governance, APO is eligible for inclusion in the S&P 500 index.

- High insider ownership aligns management with investors.

The alt management industry is not represented in S&P 500 today though it deserves it based on its scale and importance. Consequently, individual alt managers can be valuable additions to a stock portfolio adding diversification, growth, and often, yield.

Since a concentrated portfolio should include at least 10 stocks, a 10% allocation to alt managers appears the maximum no matter how one is optimistic about the industry. For a broadly diversified portfolio, it makes sense to commit at least 3-5% to alt managers in line with the weights of the smallest S&P 500 sectors.

Some of my readers confuse alternative asset managers with alternative investments. This is not the same! Alt managers are public stocks and represent traditional investments.

A big attraction of alternative investments is "volatility laundering" (the term coined by US investment manager Cliff Asness) achieved by limiting liquidity. Investors feel better when they do not need to watch the wild gyrations of the stock market. On the contrary, alt managers are more volatile than the market, and nobody knows it better than alt managers' management. Nonetheless, top managers are heavily invested in the stocks of their companies!

Besides smaller players, the industry consists of the Big Six represented by seven stocks: Blackstone ( BX ), Brookfield Corporation ( BN ), Brookfield Asset Management ( BAM ), Apollo Global Management ( APO ), Ares Management ( ARES ), Carlyle Group ( CG ), and KKR ( KKR ). My top choices are BAM and APO due to their structural advantages. I recently analyzed the new BAM and now it is about Apollo including fresh materials filed in conjunction with its Q4 earnings release.

This post assumes a certain familiarity with the alt-management industry. If you are a newcomer please read " How Brookfield and peers make money..." - it will help you a lot.

What is so unique about Apollo?

In the recent "Why Brookfield and peers followed Apollo into Insurance" ("previous post") I explained Apollo's business model in detail. To avoid being repetitive, I will devote only several paragraphs to the company's description and refer to the previous post when needed.

Apollo's business consists of 2 parts and the holding company (Holdco). One part is an asset-light manager ("old" Apollo not very different from BAM or BX), which reports earnings in two segments: FRE (fee-related earnings) and PII (the principal investment income). Management fee-centric FRE does not require further explanations, and PII consists of carry and the investment income from balance sheet investments excluding insurance (in normal years, carry dwarfs the investment income). FRE is much bigger, very predictable, constantly growing, and represents the lion's share of the asset manager's value.

The second part (Athene) is a retirement specialist focused on issuing fixed annuities to (future) retirees (Athene issues several kinds of annuities but derivatives, hedging, and reinsurance reduce them to simple fixed annuities). Apollo invests funds that Athene receives from retirees at higher interest rates than promised to retirees. The difference (after deducting Athene's opex) becomes spread-related earnings ("SRE"). For its services, the FRE segment charges Athene management fees and SRE is calculated AFTER deducting these fees. (As far as I know, the term "SRE" is coined by Apollo. It is similar to net interest income in banking.)

Holdco receives dividends from SRE, FRE, and PII, pays interest on the company's debt (which is rather small), incurs some operating expenses, and pays taxes (in 2022, the tax rate was about 19.6%).

This structure has existed only since Jan 1, 2022, when Apollo merged with Athene. However, Athene has been in existence since 2009 and registered a rather long track record. Based on the traditional classification, Athene belongs to the life insurance industry but does not write any insurance (top Apollo managers have jars on their desks, and whoever says "insurance" instead of "retirement services" puts $20 in them). But it is very good at generating stable spread under different macro environments, achieved by low operating expenses and superior investing by Apollo (in the previous post, I explained how Apollo invests Athene's funds).

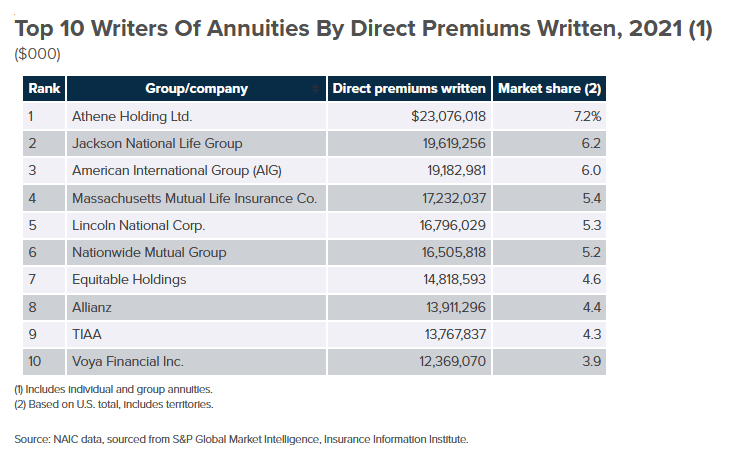

I will include two slides to illustrate Athene's performance. The first one shows Athene's place in the annuity sub-industry. Athene is not only the top company but also the youngest one on the list.

{kind=link}

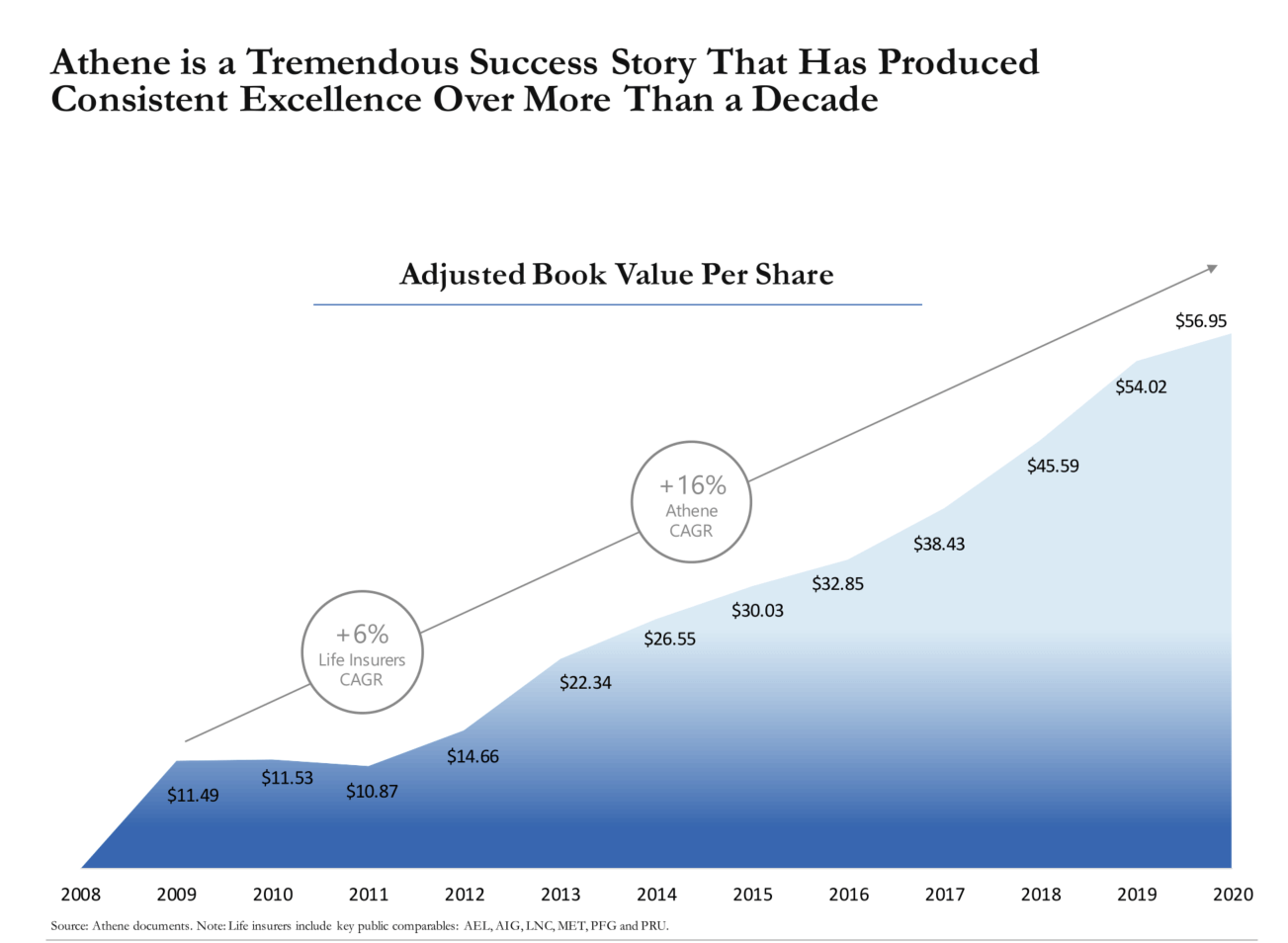

The second one shows how profitable this growth has been:

{kind=link}

This slide was related to the merger announcement in mid-2021. Since Athene had not paid dividends when it was a separate company, BVPS growth is close to its ROE which historically has been (including 2021-22 not on the slide) about 15-17%. Please remember this number - we will need it later.

The last slide also shows Athene's overperformance compared to the life insurance industry. Remarkably, it has been achieved while having lower leverage and higher excess capital than peers.

Athene is Apollo's biggest differentiator by far.

Valuing Apollo

We will value Apollo using a simplified and conservative SOTP:

- Pretax FRE and SRE are taxed at 19.6% and valued separately.

- Depending on the market environment, PII can be big or small. When markets are high, alt managers perform multiple exits from their private equity positions and generate a fat carry. When markets are low, alt managers defer exits waiting for better valuations. However, even in bad markets, PII is higher than Holdco costs and interest expenses combined. For example, in rough 2022, PII's segment generated earnings two times smaller than planned. But they were still $285M vs $122M in Holdco costs and interest expenses. For our simplified model, we will discard all three items together.

- The company's value will be the sum of the FRE and SRE segments.

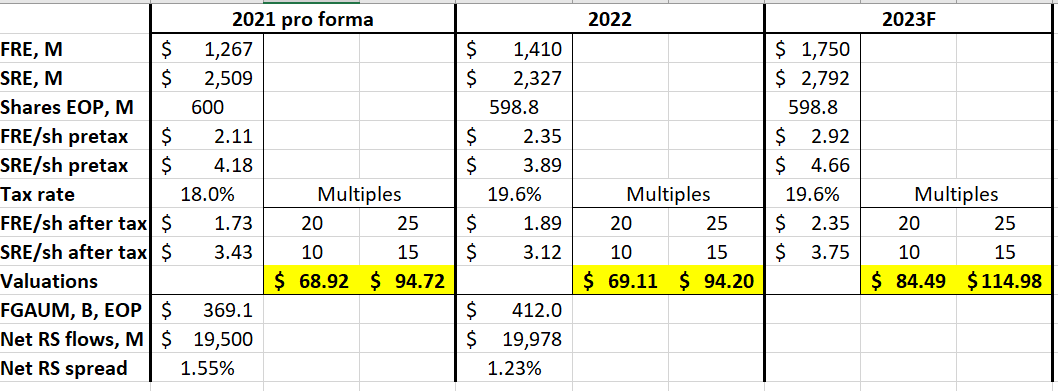

The slide below shows the calculations. For 2023, we used the company's forecast announced on the Q4 earnings call.

{kind=link}

The table requires some explanations. Today, asset-light and management fee-centric managers like BAM or ARES are trading at ~25x FRE multiples. Correspondingly, We are using 20x and 25x for low and high values. Short of the market crash, with growth of ~20%, FRE should be worth at least 20x. This is rather straightforward.

The critical issue is how to value SRE and we will start from the basics. Imagine an insurance company with $100 of equity and an ROE of 10% that does not pay dividends. Since the stock market on average returns 10% annually, our insurer, in equilibrium, should be trading at its book value. Then its return is on par with the stock market expected return. This corresponds to a forward P/E ratio of 10 and a trailing P/E ratio of 11.

If our insurer's ROE is 15% (similar to Athene's low point), it will generate $15 in net income in one year. At the same 10% discount rate, this $15 translates into the current value of $15/0.1=$150, or 1.5x of its equity. Its forward P/E ratio is 10 and its trailing P/E ratio is 11.5.

Based on these two examples we can safely assume that Athene's P/E trailing ratio should be at least 10. Let it be our low-end multiple.

The calculations above do not take into account compounding which is easy to show. At a 15% ROE, our insurer's book value after 2 years will be 100*1.15*1.15=$132.25 and it should be worth 132.25*1.5=$198.38. Then its present value is equal to $198.38/(1.10*1.10)=$156.82 which is HIGHER than $150!

Looking 3 years forward, the same calculations produce the present value of $163.95 and so on. Consequently, both forward and trailing P/E ratios will be higher as well. For example, trailing P/E reaches 15 if we look 6 years forward. For practical purposes, we will use a trailing P/E ratio of 15 (in line with the book value and net income growth rate) as the high-end multiple.

The realistic multiple is supposed to be somewhere between 10 and 15 depending on the actual ROE and payout ratio among other things.

From our table, Apollo is trading precisely at the very low end of its value range and it is rather safe to buy it. Besides the 20% growth forecast for 2023 and beyond, we can also count on multiples expansion closer to the middle of our value range.

Combined, SRE and FRE produced $5.01 in after-tax earnings in 2022. Still completely ignoring PII, APO is trading at a 14 P/E ratio with an expected 20% growth rate in 2023. Apollo is, perhaps, the only alt manager trading on a value basis!

The market seems overly cautious regarding Athene and some participants still mentally position Apollo as private equity. Here is some evidence of it. In early February, Apollo reported its results for Q4 22. I considered the earnings release quite strong but the stock was down 7%. Later, it occurred to me that PII (i.e. carry) earnings miss was the likely culprit (the segment earnings were two times smaller than planned). That might have been more or less important for the old Apollo but is almost irrelevant now. It took several days for the market to come back to its senses.

Besides low costs, disciplined underwriting, and superior investing, Athene is driven forward by population aging. It is easy to bet on this trend due to inexorable medical advances. Retirees need income and some of them will inevitably opt for annuities. Each dollar in annuities' premiums will grow both FRE and SRE for the new Apollo. This growth will be organic and self-sustaining.

Apollo has other lines besides retirement services. For example, its private equity funds are among the best and the biggest. But make no mistake: it is retirement asset growth and related high-grade fixed-income strategies that make the company unique. The bottom three lines in the table show the most important numbers to track performance - FGAUM (fee-generating AUM) with most of them from credit strategies, net Retirement Services flows, and net Retirement Services spread. The last number was higher than it is supposed to be in both 2021 and 2022. Due to the growing interest rates, it will probably stay that way in 2023. With time, it may fluctuate slightly. But as I showed in the previous post, it has been remarkably stable since 2010 and is expected to stay that way.

Apollo also controls (and owns partially through Athene's balance sheet) private Athora, which is a retirement services company focused on Europe. For simplicity, you can think of Athora as Athene ten years ago, still building momentum. The efforts in Asia/Australia are in earlier stages with Athene holding stakes in several regional retirement companies.

In the previous post, I also explained that high-grade fixed-income origination is the key strategy for Athene/Apollo with the current run rate of about $100B annually. However, Apollo is closing a set of transactions to acquire the Credit Suisse securitization group (the first transaction already closed). This group alone is supposed to add ~$50B in originations. The origination rate is becoming much higher than needed for Athene's and Athora's balance sheets and will be used to supply other insurers and grow FGAUM and fees further.

Conclusion

The industry growth depends on investors' allocations to alternative assets. Based on different estimates, demand for alternatives from both institutional and retail investors is very far from saturation. All big alt managers seem destined to grow quickly for many years ahead. Still, the biggest risk for the industry is a sudden and unexpected investors' loss of appetite for alternatives. Among all alt managers, Apollo is better insulated from this risk because its growth is self-sustaining. Demand for its investment-grade private credit is mostly internal, secured by Athene's retirees.

Apollo also has a decent chance to get included in the S&P 500 index. It is eligible for it due to its size and corporate governance (corporate governance is a stumbling block for many alt managers). If it happens, Apollo will not only receive a one-time jolt but will also become better known to the wide circle of investors. In this regard, it is less popular than Blackstone or Brookfield.

Apollo's strategy is rather complex and not so digestible for investors. I know it from my own experience. After my initial research, I bought the stock 1.5 years ago and have authored several articles on it since. Writing articles and perusing Apollo's filings have gradually advanced my understanding of the company. It takes time.

High insider ownership (about 30% based on Apollo's presentations) can alleviate some investors' concerns. They eat their cooking.

For further details see:

How To Supercharge Your Portfolio With Apollo And Other Alt Managers