CA - HPF: Take Some Gains But Do Not Abandon This CEF Completely

2024-01-16 10:48:45 ET

Summary

- John Hancock Preferred Income Fund II aims to provide high current income by investing primarily in preferred securities.

- The fund has a 9.02% yield, higher than most investment-grade bond funds and other preferred stock funds.

- The fund's share price has declined over the past five years, but distributions have offset the decline and increased investors' wealth by 22.48%.

- The fund's shares are looking expensive right now as the shares are trading at a higher-than-normal premium.

- There is a risk of a near-term fixed-income repricing situation, so it could be a good idea to take some recent gains off of the table.

The John Hancock Preferred Income Fund II ( HPF ) is one of John Hancock's many closed-end funds for income-focused investors. As the name suggests, this fund aims to achieve its goals by investing primarily in preferred securities, which are a fixed-income security that act somewhat like a bond with no maturity date. These securities are frequently considered a hybrid between common stock and bonds because they sit between the two levels in a company's capital stack, but they actually have much more in common with bonds. For example, preferred stocks do not usually benefit from the growth and prosperity of the issuing company, nor do they confer voting rights upon their holders. They do typically have higher yields than bonds issued by the same company though, which can make them rather appealing to income-focused investors. These higher yields when compared to bonds have benefited this fund and its shareholders as it has a 9.02% yield at the current price. This is a very reasonable yield even in today's high-yielding environment and it compares very well to most investment-grade bond funds and even to most other preferred stock funds.

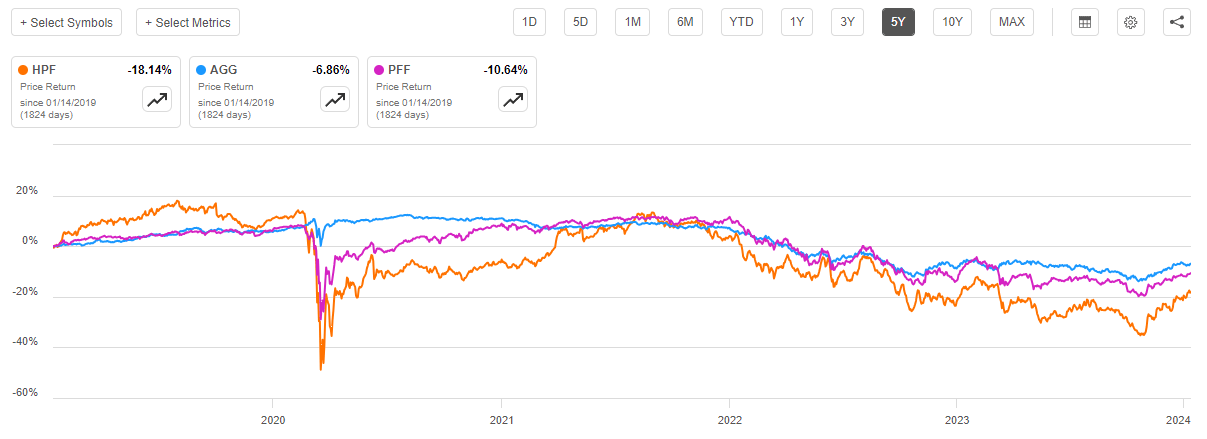

Anyone who takes a look at the fund's price history is unlikely to be impressed, however. As we can see here, the fund's share price has declined 18.14% over the past five years. That is a worse performance than either the Bloomberg U.S. Aggregate Bond Index ( AGG ) or the iShares Preferred and Income Securities ETF ( PFF ):

{kind=link}

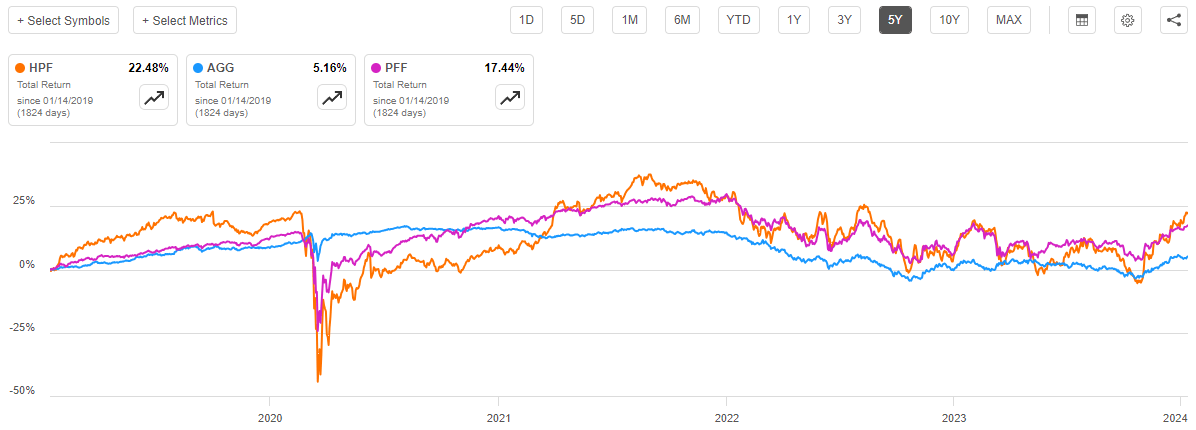

However, the share price performance alone does not tell the entire story when it comes to this fund. As is the case with most closed-end funds, the John Hancock Preferred Income Fund II pays out essentially all of its investment profits to its shareholders via distributions and aims to maintain a relatively stable net asset value. This is why this fund has a much higher yield than either of the indices. As such, we should consider the distributions in any analysis of the fund's performance because these distributions can actually offset declines in the fund's share price. When we do this, we see that investors in the fund have actually increased their wealth by 22.48%, which is better than either of the indices managed to deliver over the trailing five-year period:

{kind=link}

This is not exactly atypical, as fixed-income closed-end funds usually outperform their benchmark indices. Unfortunately, there are some signs that the fund may struggle in the near term. This is mostly because most preferred stocks have become highly overvalued over the past three months and that could cause this fund to give up some or all of the 14.26% gain that it has experienced since the start of the fourth quarter of 2023. We will naturally discuss this over the remainder of this article.

About The Fund

According to the fund's website , the John Hancock Preferred Income Fund II has the objective of providing its investors with a very high level of current income while preserving the value of its capital. This is a very reasonable and common objective for any fixed-income fund because fixed-income securities tend to be fairly safe securities that deliver nearly all of their total investment return in the form of direct payments to the investors. In the case of bonds, an investor who purchases the security and holds it until maturity is guaranteed not to lose money unless the issuer defaults. This is because bonds are both issued and redeemed at face value. However, this is not true with respect to preferred stocks, which is what this fund invests in. As the website states, the fund's strategy is:

Focusing on preferred stocks and preferred convertible securities, which share characteristics of both equities and bonds.

In many cases, a preferred stock does not have a maturity date, so investors are never guaranteed to receive a full return of principal at some point in the future. However, preferred stocks tend to be fairly range-bound instruments that do not exhibit an excessive amount of volatility. As such, an investor who purchases a preferred security and holds it for long enough will probably end up making a profit between the dividend payments and the eventual share price no matter what happens during the intervening period. The caveat here, of course, is that the dividend payments made by issuers of these securities are not considered mandatory as they are with bonds. However, most companies will do everything in their power to make the promised payments to the preferred equity holders, so bankruptcy is the only real concern for very long-term investors.

In a recent article on the John Hancock Preferred Income Fund III ( HPS ), a sister fund from the same manager, I pointed out that most preferred stock funds have a very high exposure to the banking and financial services sector. The John Hancock Preferred Income Fund II claims on its website that it has exposure to a very wide range of sectors, which would appear to suggest that it is very diversified:

John Hancock Funds

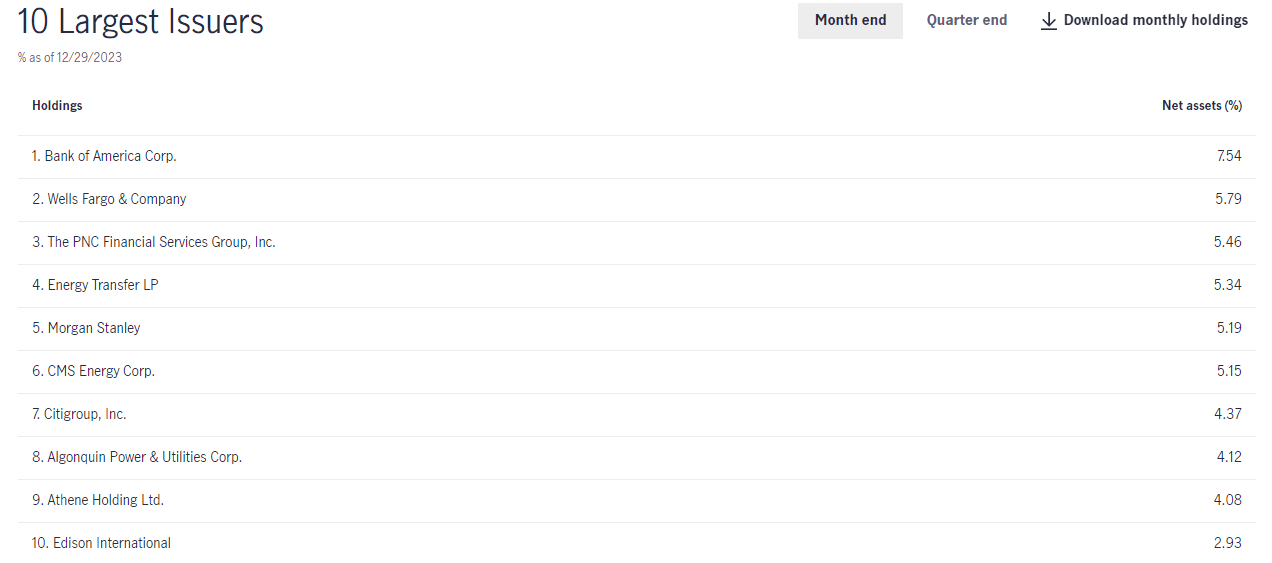

However, a look at the fund's largest positions reveals a number of banks just like its sister fund:

{kind=link}

We do see a few non-bank companies here:

| Company |

| Sector |

| Bank of America Corporation ( BAC ) |

| Banking |

| Wells Fargo & Company ( WFC ) |

| Banking |

| The PNC Financial Services Group, Inc. ( PNC ) |

| Banking |

| Energy Transfer LP ( ET ) |

| Energy |

| Morgan Stanley ( MS ) |

| Banking |

| CMS Energy Corporation ( CMS ) |

| Utilities |

| Citigroup Inc. ( C ) |

| Banking |

| Algonquin Power & Utilities Corp. ( AQN ) |

| Utilities |

| Athene Holding |

| Insurance |

| Edison International ( EIX ) |

| Utilities |

However, the majority of the companies that comprise the fund's largest holdings are banks. As I explained in the article on the similar John Hancock Preferred Income Fund III,

The first thing that we notice here is that all of the companies in the fund's largest positions list are either utilities or banks. This is not uncommon for a preferred stock fund because banks and utilities are the largest issuers of preferred stock in the market. As a result, almost any preferred stock fund will be very heavily weighted towards these two types of companies. With that said though, usually the overwhelming majority of companies in the top ten list are banks. This is due to international banking regulations that require banks to hold a certain percentage of their assets in the form of Tier One capital. Tier One capital refers to that proportion of a bank's assets that are not simultaneously a liability to somebody else (such as a depositor). When regulators require that a bank increase its Tier One capital, its only option is to issue either common or preferred stock. The bank will often choose to issue the preferred stock in order to avoid diluting the common stockholders. A utility does not have these regulations to follow but they become heavy issuers of preferred stock due to the cost of their infrastructure. The utility company will often finance the construction of this infrastructure with debt, but the company will usually want to avoid taking on too much debt and becoming overleveraged. Thus, it will often issue preferred stock to partially cover the expenses so that it can avoid too much debt or common stock dilution.

We see that with this fund, and indeed many of its holdings are identical to those that we saw in the John Hancock Preferred Income Fund III. In particular, the weightings of the various securities in this fund are vastly different from those in its sister fund. The John Hancock Preferred Income Fund II is a bit less top-heavy, for example, as its second-largest position only accounts for 5.79% of the fund's assets compared to 6.03% in the other fund. We also see that this fund has a non-banking company among its top five positions while the other fund does not. This could make the John Hancock Preferred Income Fund II more attractive than its sibling for those investors who are uncomfortable with the banking sector exposure that the John Hancock preferred stock funds possess. Unfortunately, this fund's documentation does not state what its current exposure to bank preferred stock is, and neither does the website. That is very disappointing, as it would be nice to have some idea of the fund's sector weightings so that we can ensure that we have adequate diversification across our portfolios. Other sources that will frequently be consulted for additional information about a fund's sector exposure likewise offer no help, so this is disappointing.

The Thesis

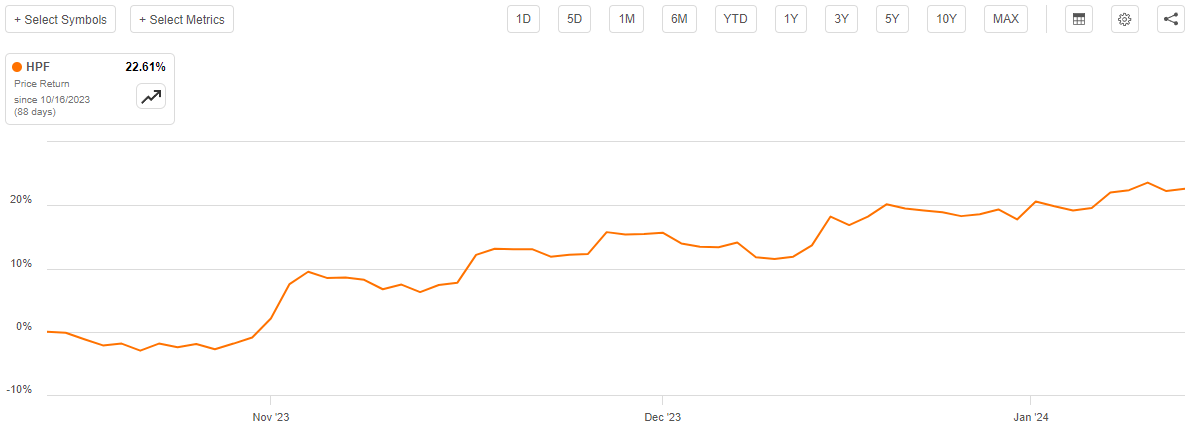

It cannot be denied that investors in the John Hancock Preferred Income Fund II have been quite richly rewarded over the past few months. As we can see here, the shares of the fund are up a whopping 22.61% since October 15, 2023:

{kind=link}

This is a very impressive performance for any fund, let alone one that invests in fixed-income securities like this one. The biggest reason for this is that market participants have been attempting to front-run a series of interest rate cuts by the Federal Reserve this year. As I explained in a number of previous articles, the Fed funds futures market has been pricing in a 1.384 percentage point decline in the effective federal funds rate by the end of 2024:

{kind=link}

That scenario would require an incredibly severe recession to hit within the next three or four weeks. That is, to put it mildly, highly unlikely considering that most economic indicators are showing that the economy has been quite resistant to the monetary tightening that has occurred since the start of 2022. This is partly due to the very loose fiscal policies coming out of Washington, D.C., which are effectively undoing some of the Federal Reserve's efforts to rein in inflation and keeping the economy from going into the recession that economists have been expecting for quite some time now.

As I pointed out in a recent article , there was only one time in history that the Federal Reserve cut interest rates by 125 basis points or more in the absence of a recession, and that was in the middle of the 1980s. Recent inflation data suggests that a great deal of work still needs to be done to beat inflation. For example, consider three items from the most recent inflation report that have a significant impact on many consumers: annual services (+5.3%), shelter (+6.2%), and transportation services (+9.7%). That clearly shows that the narrative about the defeat of inflation is far from accurate. That data suggests that the Federal Reserve should not begin a monetary loosening cycle in March, as the market expects. Indeed, last week a few officials from the Federal Reserve suggested that there would be no rate cuts in the first half of 2024, which means that there is not enough time for the requisite number of rate cuts to satisfy the market.

As such, the preferred stocks that are held by this fund are overpriced and the fund could give up its gains as early as the next few weeks once the market realizes that it drove asset prices up too far too quickly. This suggests that investors should take some of the profits that they received from this fund and wait for a correction. That strategy would reduce the overall risks that any investor in the John Hancock Preferred Income Fund II is sitting on right now.

On the other hand, we are beginning to see some problems emerging in the repo market that could force the Federal Reserve to scale back its monetary tightening efforts sooner rather than later. In early December, the Secured Overnight Financing Rate spiked:

{kind=link}

That was the worst spike that the market has seen since March 2020, when fear over the novel coronavirus caused investors to pull all of their money out of anything that had even the smallest amount of risk. This suggests that liquidity in the money markets is not where it needs to be in order to ensure the stability of the money markets. Zero Hedge speculated earlier today that this is the reason why Chairman Powell appeared to take a dovish turn in December, which was the driving factor behind the "Santa Claus" rally that occurred at the end of 2023.

However, right now, it does not appear that the Federal Reserve will reduce interest rates just because of the emerging liquidity problems in the money markets. Right now, the most likely scenario is that the central bank will simply reduce the speed at which it is selling down the assets on its balance sheet and pulling money out of the economy. However, the market might still react to this situation with optimism that rate cuts are coming and continue to drive up fixed-income securities and the shares of the John Hancock Preferred Income Fund II right along with them.

The possibility of a reaction to problems could mean that investors might give up some further upside by taking profits now, but I still suspect that the market will be proven wrong about the degree to which the federal funds rate will be reduced this year. As such, it may be a good idea to take some gains off of the table, but still keep some money invested in this fund in order to continue to profit from further potential upside.

Leverage

As is the case with most closed-end funds, the John Hancock Preferred Income Fund II employs leverage as a method of boosting the effective yield that it receives from the assets in its portfolio. I have explained how this works in a number of previous articles on other closed-end funds. To paraphrase myself:

In short, the fund borrows money and then uses that borrowed money to purchase preferred stock and other income-producing assets. As long as the yield that the fund receives from the purchased assets is higher than the interest rate that it needs to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. However, it is worth noting that leverage is not as effective today at boosting a fund's overall returns as it was a few years ago when borrowing rates were basically 0%.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage because that would expose us to an excessive amount of risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the John Hancock Preferred Income Fund II has leveraged assets comprising 38.35% of its portfolio. This is unfortunately above the one-third maximum level that we would prefer to see. However, the fund's current leverage is relatively in line with the other John Hancock preferred stock funds and, as I have explained in articles on the other funds in this family, the current level of leverage is probably okay. This is because preferred stocks tend to be much less volatile than common stocks, which allows a fund that invests in these assets to carry a higher level of leverage than a common equity fund. After all, it is volatility that causes the biggest problem for a leveraged investment strategy.

Overall, investors probably do not need to worry too much about the fund's leverage right now, but it is a good idea to keep an eye on it in order to ensure that the fund does not significantly increase its leverage from its current level.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the John Hancock Preferred Income Fund II is to provide its investors with a very high level of income. In pursuance of that objective, the fund invests in a portfolio that primarily consists of preferred stocks. Preferred stock tends to boast higher yields than bonds to compensate for the fact that they sit lower on the capital stack and are thus theoretically riskier. The fund collects the payments that it receives from the securities that it purchases with its equity capital and then borrows money in order to control even more securities and collect payments from them. The fund then pays out all of this money to its shareholders, after deducting its own expenses. As such, we can probably assume that this fund's shares will have a very high yield.

This is certainly the case, as the John Hancock Preferred Income Fund II pays a monthly distribution of $0.1235 per share ($1.4820 per share annually). This gives it a 9.02% yield at the current price. As stated earlier, that is relatively in line with John Hancock's other preferred stock funds, and it is quite a bit higher than the yield of preferred stock funds from other managers such as the Flaherty & Crumrine preferred stock funds. The fund has also been reasonably consistent with respect to its distribution over the years, although it has not been perfect. As we can see here, the fund has both increased and decreased its distribution payment over the years:

{kind=link}

For the most part, this fund's distribution history is somewhat more consistent than many other peers and as such might appeal to those investors who are seeking to receive a safe and secure income from the assets in their portfolios. However, at the same time, it does present some concerns as it does not make sense that this fund could enjoy this level of consistency when many other preferred stock funds were unable to achieve the same level of performance. As such, we should have a look at the fund's finances, as it is possible that it is overdistributing and destroying its net asset value in the process. That is not sustainable over any sort of extended period.

Fortunately, we have a relatively recent document that we can consult for the purposes of our analysis. As of the time of writing, the most recent financial report for the John Hancock Preferred Income Fund II corresponds to the full-year period that ended on July 31, 2023. As such, it will not include any information about the fund's performance over the past five months or so. That is disappointing, as there were a few things that happened during the interim period. In particular, there was both a bear market and a bull market in fixed-income securities that undoubtedly had an impact on the fund's portfolio and could have resulted in either losses or gains. This report will not give us any insight into how well the fund performed during either of these environments. However, it will still give us some good insight into how well the fund sustained its distribution payments during the second half of 2022 and the first half of 2023. This could be valuable insight as 2022, in particular, was one of the most challenging environments for fixed-income securities that was seen during the entire careers of some younger traders.

During the full-year period, the John Hancock Preferred Income Fund II received $23,502,257 in dividends alongside $14,692,366 in interest from the assets in its portfolio. We subtract out the foreign withholding taxes and arrive at a total investment income of $38,100,778 during the period. The fund paid its expenses out of this amount, which left it with $23,291,969 available for shareholders. That was, unfortunately, not nearly enough to cover the $31,814,309 that the fund paid out in distributions over the period. At first glance, this is likely to be concerning as we ordinarily would prefer that a fixed-income closed-end fund fully cover its distributions out of its net investment income. This one obviously failed to accomplish that task.

However, there are other ways through which the fund can obtain the money that it needs to cover its distributions. In particular, the price of preferred stock tends to move in response to interest rate changes. That can create an opportunity for traders to earn some profits by exploiting these price changes. These profits are considered realized capital gains and are therefore not included in net investment income, but they clearly represent money coming into a fund that can be paid out to the investors.

Unfortunately, the John Hancock Preferred Income Fund II failed miserably at earning money from these alternative sources during the period in question. Over the course of the full-year period, the fund reported net realized losses of $26,914,713 and had another $21,339,076 net unrealized losses. Overall, the fund's net assets declined by $55,831,166 after accounting for all inflows and outflows. During the previous full-year period, the fund's net assets declined by $57,615,461 after accounting for all inflows and outflows. Thus, the fund's net assets have declined for two consecutive years, which is concerning and suggests that the fund could struggle to sustain its distribution going forward. This is especially true if the fixed-income market does correct in the near future.

Valuation

As of January 12, 2024 (the most recent date for which data is currently available), the John Hancock Preferred Income Fund II has a net asset value of $15.46 per share but it trades for $16.43 per share. That is a 6.27% premium, which is substantially higher than the 2.53% premium that the shares have had on average over the past month. While this certainly implies that now is not a good time to buy the fund, it does work well with the thesis presented earlier as it provides an opportunity to sell some shares and realize profits before either the premium declines or the market corrects.

Conclusion

In conclusion, the John Hancock Preferred Income Fund II is looking very expensive right now and investors may want to take some of their gains. There is a very real possibility that the market is wrong about the extent to which the Federal Reserve will reduce interest rates this year, which could cause the fund to give up some of its recent gains on the table. At the same time, the turbulence in the repo market could be a wildcard that causes the central bank to abandon its inflation fight and start quantitative easing once again. As such, the best move with respect to this fund could be to realize some gains and reduce your overall risk while not abandoning it completely just in case there does end up being further upside.

For further details see:

HPF: Take Some Gains, But Do Not Abandon This CEF Completely