CA - HSBC Holdings: Take Profits Despite Its 8% Dividend Yield

2023-10-18 07:49:54 ET

Summary

- HSBC Holdings' earnings are likely at the top of the cycle, prompting investors to take profits after a strong share price rally.

- The bank's financial performance has improved, with increased revenues and good cost control.

- HSBC's dividend payout is sustainable, but further earnings growth may be challenging, and its valuation is near the top of its historical range.

HSBC Holdings Plc ( HSBC ) is trading near the top of its historical range and its earnings are likely to be at the top of the cycle, thus investors should take profits after a strong share price rally over the past year.

My last article on HSBC was about one year ago when I recommended its shares due to the bank's leverage to higher interest rates and its potential to become a high-dividend yielder in the coming months. Since then, its total return has been close to 70%, clearly outperforming the market during the same period.

Article performance (Seeking Alpha)

In this article, I review the bank's most recent financial performance and update its investment case, to see if it remains a good income pick after its recent share price rally or not.

Financial Update

HSBC is a global bank that is based in the U.K. but has a presence across more than 60 countries around the world. Its largest region is Asia, of which Hong Kong is the bank's most important market. One of its major strengths is its global presence and long history of being a major banking supplier for global commerce, having a leading position in global trade finance.

This means the bank is largely exposed to the U.S. dollar and USD rates, even though its U.S. business is not large within the group. Most global commercial trade is done in USD, thus keeping direct access to U.S. dollars is key for HSBC's business model, particularly in the commercial banking division.

Taking into account that U.S. rates have been on a rising trend over the past eighteen months and Hong Kong as a peg to the USD, HSBC has benefited greatly from higher U.S. rates in recent quarters.

Indeed, in 2022, HSBC reported a much improved operating performance supported by rising interest rates given that its net interest income ((NII)) increased by 31% year-over-year (YoY) to $32.6 billion. Its revenue related to fees and other (non-NII) amounted to $22.7 billion in the past year, up by some 3% YoY.

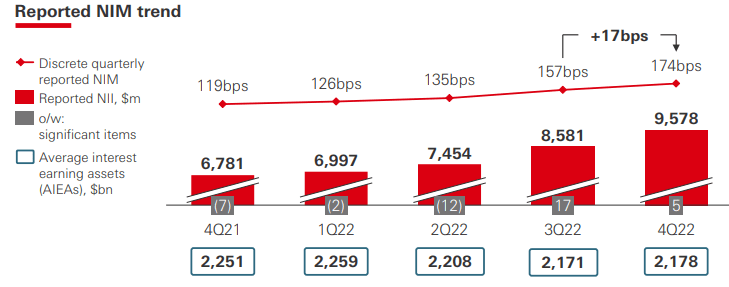

Overall, its total revenues amounted to $55.3 billion in 2022, up by 18% YoY, with NII representing some 59% of total revenues and its net interest margin improving to 174 basis points in the last quarter of 2022, showing that HSBC is not among the bank most exposed to interest rates, as there are other banks that have a NII contribution in the range of 75-80%, such as BBVA ( BBVA ) for instance which I've covered recently and it's part of my personal income portfolio.

{kind=link}

Nonetheless, within the European banking sector, HSBC has a different profile because it's much more exposed to U.S. rates than its peers, which are currently higher than Eurozone rates and lead to higher customer spreads than European banks that are mainly exposed to EUR rates.

Regarding costs, the bank has maintained good cost control despite its investments in digitalization, leading to adjusted cost growth of only 1% in the year, and an efficiency ratio of 55%.

Regarding asset quality, the bank booked significant provisions related to its commercial real estate exposure in China, amounting to some $1.3 billion, leading to total credit charges of $3.6 billion. This represented a cost of risk ratio of 35 basis points, while in the previous year, the bank had performed provisions reversals following the big jump in provisions in 2020 related to the pandemic. For 2023, HSBC expects the cost of risk to be about 40 bps, which is within its medium-term goal of between 30-40 bps, even though its commercial real estate exposure in China and elsewhere may be problematic and lead to higher losses than expected.

Due to strong top-line growth and good cost control plus strong credit quality, HSBC's net income increased to more than $16 billion in 2022, while its return on tangible equity (RoTE) ratio was 9.8%, a strong improvement from the previous year, but still below its medium-term target of at least 12%.

During the first six months of 2023, HSBC has maintained a good operating momentum, with revenues continuing to be supported by higher interest rates. This trend is expected to last for some time, as the Federal Reserve has guided for a 'higher for longer' interest rate environment in recent weeks, boding well for the bank's margins and profitability levels in the short term.

In H1 2023, HSBC's revenues amounted to $36.9 billion (+56% YoY, on a constant currency basis), a strong increase that is mainly explained by higher NII in this period (+42% YoY, to $18.3 billion). Regarding other revenues, HSBC's reported non-NII increased by 39% YoY in Q2 2023, but this includes $2.4 billion offset from central costs of funding trading income, thus adjusted for this its non-NII revenues declined by 7.4% YoY.

In Q1 2023, the bank also reported an extraordinary gain of $3.5 billion from the sale of its Canadian operation to Royal Bank of Canada ( RY ), in a deal valued at more than $10 billion, thus investors should not be much impressed by HSBC's strong non-NII growth in H1 2023, given that the reported numbers include some large extraordinary effects.

Nevertheless, the underlying operating momentum remained positive, as costs increased by 4.3% YoY, at a much lower rate than revenue growth leading to positive jaws and improved efficiency, plus credit costs also remained within the bank's guidance. Indeed, its credit costs amounted to $1.3 billion in H1 2023, of which $300 million related to its commercial real estate exposure in China, which if annualized would be a significant decline compared to 2022 ($3.6 billion credit costs last year).

This shows that credit quality is holding up well despite the pressure of higher interest rates, even though HSBC's significant exposure to CRE can be problematic in the coming quarters.

Due to extraordinary gains booked in the past couple of quarters, HSBC's reported RoTE was quite high (22.4%), much higher than its guidance of 12%+ given at the beginning of the year. Not surprisingly, HSBC raised this guidance and now expects to report a RoTE in the mid-teens, both for 2023 and 2024, which is a good level of profitability.

However, in my opinion, this is not a level that is sustainable over the long term, and it's quite likely that the bank's RoTE will decline in 2025 and afterward if interest rates start to come down during 2024, as the market is currently expecting.

On the other hand, HSBC's recent announcement to acquire Citigroup's ( C ) consumer wealth portfolio in China is a positive step toward growth in the country, especially in the wealth management segment. Citi's operation in China was mainly to serve rich clients, boosting HSBC's presence in the country in a relatively high margin business with low capital intensity, which should be positive for its profitability over the long term.

Regarding its capital position, HSBC has a strong financial profile measured by its CET1 ratio of 14.7% at the end of last June. This strong position enables it to return a good part of its earnings and 'excess capital' to shareholders, something that the bank has been doing recently.

Indeed, HSBC performed a $2 billion share buyback program at the beginning of the year, plus it's performing another $2 billion share repurchase program to be completed from August to October 2023. This represents some 2.5% of HSBC's current market value, enhancing its total capital return policy.

In addition to share buybacks, the bank also changed this year its dividend payment frequency to quarterly, making it more attractive to income investors. The bank has paid $0.43 per share in three distributions this year and is expected to make a larger final distribution related to 2023 earnings, probably during Q1 2024.

According to analysts' estimates , its total dividend related to 2023 is expected to be $0.65 per share, which at its current share price leads to a forward dividend yield of about 8.1%. This is a very high-dividend yield and sometimes this can be a sign of poor dividend sustainability, but this isn't the case regarding HSBC given that its dividend payout ratio is only 50% and the bank has a solid capital position, its dividend is clearly sustainable over the medium term.

Investors should also note that HSBC is expected to announce its Q3 2023 earnings by the end of this month, which are still expected to be strong, supported by higher interest rates. However, investors should especially look for potential weakness in credit quality, particularly related to the bank's commercial real estate exposure in China, as this sector has continued to show some issues in recent months and may be an important headwind for HSBC's earnings growth in the short term.

Conclusion

As I expected one year ago, HSBC has benefited greatly from higher interest rates and has become a high-dividend yielder. However, further earnings growth from here may be harder to achieve as rates are supposedly at their peak or near that level, plus its significant exposure to commercial real estate may lead to higher losses than expected in the coming quarters.

Moreover, while one year ago HSBC was trading at only 0.6x book value, its valuation has re-rated to close to book value currently , which is above its historical average over the past five years (around 0.8x). As earnings are expected to be at peak and valuation is also near the top of its historical range, HSBC does not offer much value beyond its high-dividend yield and investors should take profits.

For further details see:

HSBC Holdings: Take Profits Despite Its 8% Dividend Yield