CA - Hudbay Minerals: Copper Mountain Merger Injects Timely Cash Flow

2023-07-20 14:51:21 ET

Summary

- Hudbay's Copper Mountain acquisition is a strategic victory with demand set to soar and a massive shortfall expected by 2030.

- The move also looks brilliant in light of the fact finding new copper deposits is becoming more challenging due to rising costs and regulatory hurdles.

- That said, Hudbay's valuation still hinges on the timely opening of Copper World in Arizona, where political winds seem favorable, but resistance by some interest groups remains fierce.

Hudbay Minerals Inc ( HBM ) raised annualized copper output by almost 40% practically overnight by acquiring Copper Mountain, a merger that went into effect at the end of June - and one that will immediately contribute to the bottom line. The addition will in the next few years provide welcome cash flow as the company makes deep investments in its Copper World assets in Arizona. This will be an uncertain balancing act, to be sure. Hence, although the stock looks undervalued, my buy recommendation is a very cautious one. Investors will be betting that Hudbay gets local mining permits in a reasonable timeframe and Copper World begins producing in 2027.

Expanding Copper Portfolio

The IEA in a report released last week revealed that the projected gap between copper demand and supply is only growing. The IEA estimates that the gap could reach over 10mln tons by the end of the decade in the net zero by 2050 scenario. As demand soars given copper's key role in the green transition, concerns rise over supply constraints, something Hudbay has repeatedly stressed. Depletion in high grade resources, less frequent discoveries of deposits of sufficient scale, and regulatory issues delaying the permitting process are among some of the major issues.

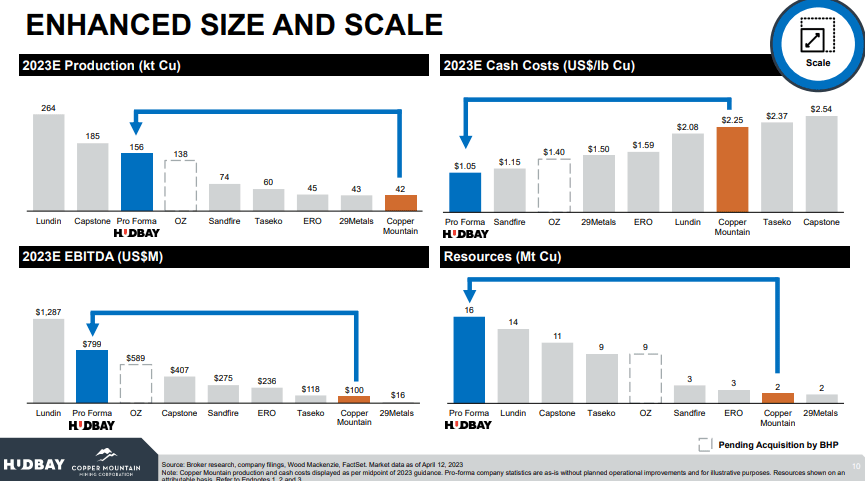

This only underscores the importance of Hudbay's Copper Mountain acquisition, which became effective June 20. The move raises the company's annualized copper output from 114kt to 156kt per year on a pro forma basis, an increase of 37%. In addition, it will add about 30koz of gold and over 350koz of silver, per Copper Mountain's 2023 guidance . The combined entity resulting from the agreement will make Hudbay the third-largest copper producer in Canada.

Hudbay-Copper Mountain Merger Upside (HBM April Investor Presentation)

{kind=link}

In addition, the merger could unlock $30 million in annualized savings including $20 million from Hudbay simply implementing efficiency processes at the Copper Mountain mine. In the merger pitch, the company suggests that Copper Mountain's cash cost of $2.25/lb can be reduced to the $1.05/lb target at Hudbay's Constancia mine in Peru.

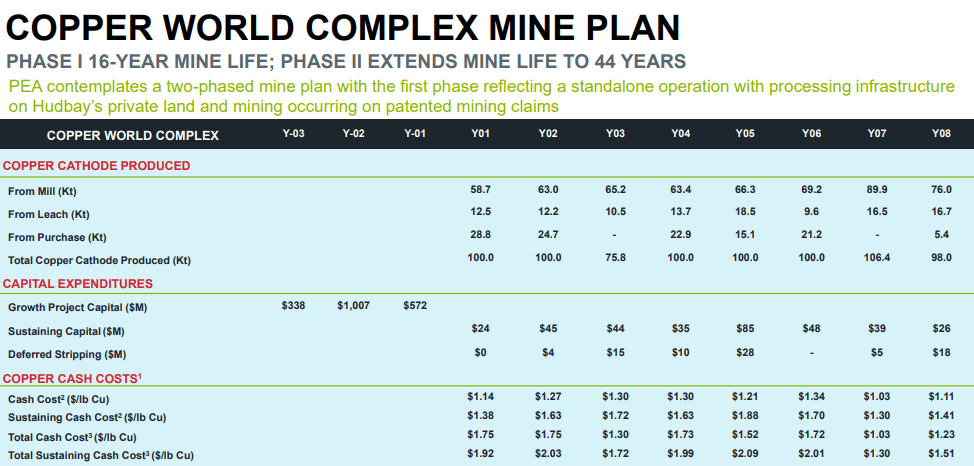

When they announced the agreement, Hudbay said the merger would deliver sustainable cash flows and a stronger balance sheet to allow the company to focus on growth projects, specifically the development of Hudbay's Copper World project in Arizona. The Copper World Complex has a total mine life of 44 years, average annual production of 86kt, with an after-tax NPV ranging from $741 million to $1.29 billion.

The capex investment for phase I will be more than $1.9 billion over the three years prior to production, which Hudbay, per the FAQs , is hoping to start in 2027. If the company gets the hoped-for local and state permits this year, the Copper World capex spending should begin flowing in 2024.

HBM Copper World Years 1-8 of Phase I 16-Year Plan (Hudbay June Investor Presentation)

{kind=link}

The first phase is a standalone project consisting of four open pits with a 16-year mine life. Hudbay has stressed that the pits are located entirely on private land and require only state and local permits . Hudbay expects to receive two outstanding state permits in 2023: the Aquifer Protection Permit and an Air Quality Permit. On receipt of these state-level permits, Hudbay said it intends to initiate a minority joint venture partner process to help fund definitive feasibility study activities in 2024.

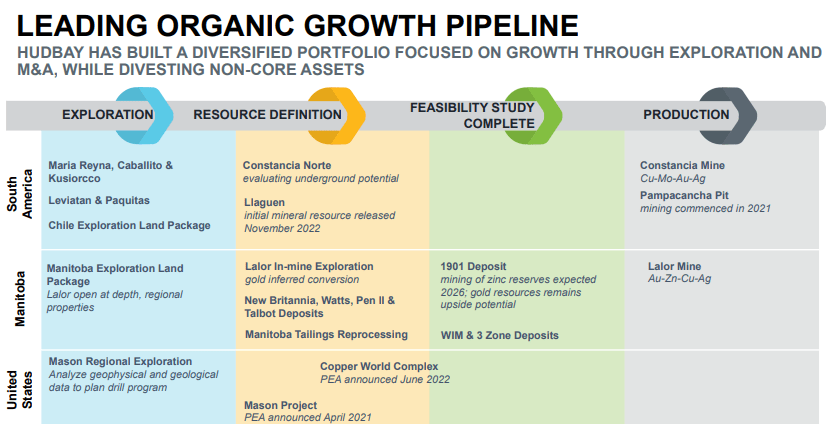

Other Projects

Although there was not enough information to incorporate into the valuation, there are a few other projects in the growth pipeline investors might be interested in.

- The Mason project in Nevada could add 112kt of annual copper production. Mason has a 27-year mine life and NPV of nearly $1.2 billion.

- Constancia underground mining could begin in 2029 to supplement open pit production. A 2021 study resulted in adding 6.5Mt at 1.2% Cu to reserves.

- Llaguen in Peru has indicated resources of 271mln at .33% Cu.

- Exploration at Constancia satellites Maria Reyna and Caballito, the latter of which could have 91Mt with 2.3% Cu.

{kind=link}

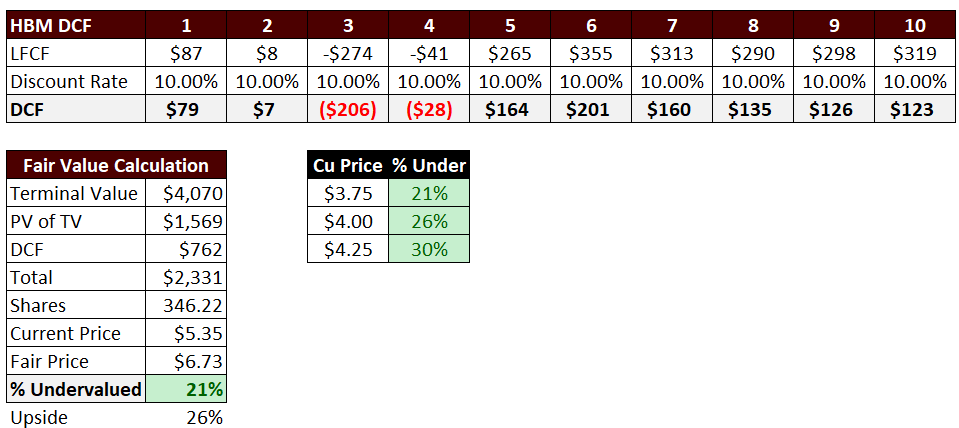

Valuation

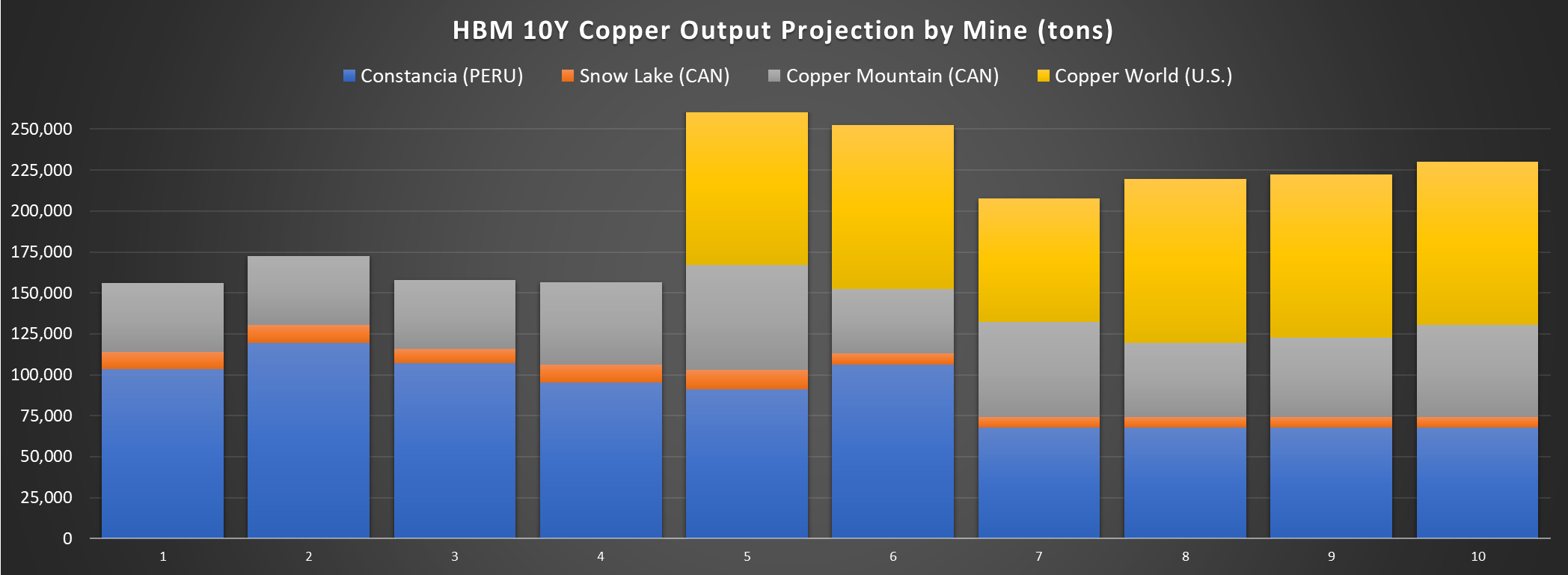

Based on Hudbay's presentation and Copper Mountain's mine plan from a technical report published in September 2022, we can project copper production volumes for the next ten years. When Copper World comes online in year 5, total annual copper output surpasses 260kt. For the years in our model, Copper World's annual production is 100kt except in year 7 where it dips to 75kt.

Author's 10Y Projection of HBM Copper Production (MH Analytics)

{kind=link}

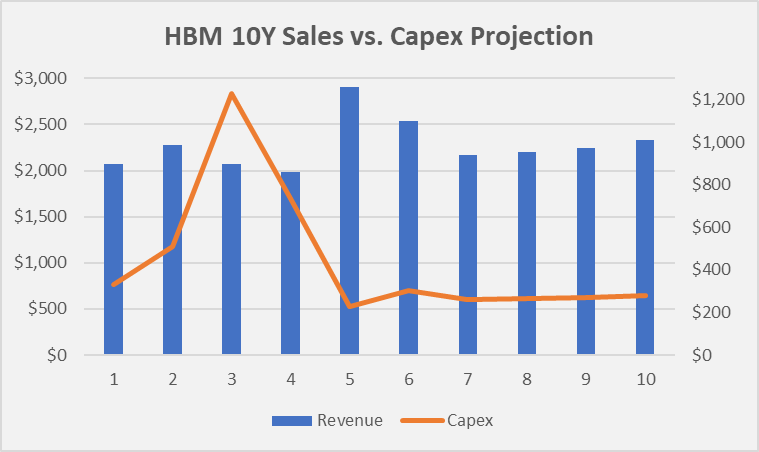

One issue worth noting is that the $1.9 billion invested in Copper World has a five-year payback period. And Hudbay calculated the NPV based on ROI generated over a 16-year timeframe. In our DCF model, the three years of significant capex spending occurs in years 2-4 and Copper World output does not impact the bottom line until years 5-10. So, only a small portion of the intended ROI is captured in our valuation.

Author's 10Y Projection of HBM Sales and Capex (MH Analytics)

{kind=link}

The other big challenge was trying to project operating margins. To truly benefit from potential synergies, Hudbay initially might face an uphill battle in lowering Copper Mountain's cash costs so quickly. In our theoretical year 1 we could use the pro forma targets proposed by Hudbay which would imply starting at about a 23% EBIT. This seems a stretch based on historical trends, even taking into consideration the expected synergies. Hudbay's EBIT in 2021 was 21% but in the trailing twelve months it fell to 17%. And its ten-year average is below 10 percent. Copper Mountain, meanwhile, saw negative operating profit last year and has a 12% 10-year EBIT margin average.

In the end, I decided to start with a 15% EBIT margin in year one, which I gradually raised over the next few years, assuming efficiencies gained, before hitting 23% when Copper World comes online with its own low cash costs, which averages about $1.20/lb during the years in our model. The ten-year average EBIT ends up at 21%.

Key model assumptions:

- EBIT Margin: 21%.

- Key Commodity Prices = Cu @ $3.75/lb, Au @ $1,800/oz.

- Tax Rate: 27.8% (blended Canada/Peru/U.S.).

- Capex as % of sales: 20% (30% in years 1-5).

{kind=link}

Risks

Despite only needing local permits, thereby avoiding a run-in with the EPA, Copper World's production timeline still faces risks. Although they have cleared some legal hurdles and won some court battles, environmental groups and the tribes appear ready to continue the fight .

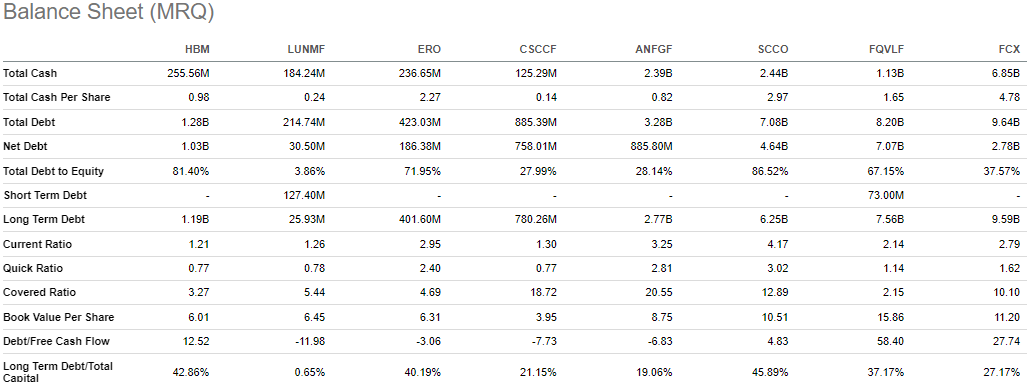

Hudbay's debt is arguably too high - its debt/equity ratio has risen from nearly 50% to over 80% since 2018, short-term assets do not cover long-term liabilities, its current ratio is a mere 1.21, and Altman Z score is .73. Hudbay's covered ratio of 3.27 seems sufficient, but low compared to seven pure-play peers, whose median is 10.

{kind=link}

The company in the presentation explaining the deal said the merger will help lower its net debt/EBITDA ratio of 2 to as low as 1.3. However, the median across the other seven aforementioned copper players is 0.91. The bottom line: how Hudbay manages its debt going forward is something investors should keep a close eye on.

Conclusion

Hudbay's Copper Mountain acquisition is just in time to fill cash flow needs as the company prepares to spend close to $2 billion in capex on the Copper World project in Arizona. I sense the market has priced in much of the merger upside, but I am willing to bet doubts around the timing of Copper World have left the stock undervalued, which is why I give it a cautious buy rating.

I am rolling the dice that the desperate need to fill the looming copper gap amid the green transition will prevent delays and even accelerate the initiative. And the political winds in the copper state are swirling lately in favor of development - and this is true on both sides of the political aisle.

On the other hand, because copper is not formally classified as a critical mineral by the U.S. government, it might be an unlikely candidate for a fast-track. South32's Hermosa project in Arizona is the first fast-track initiative, but two of the metals involved are listed as critical minerals by the USGS: zinc and manganese.

A buy recommendation also comes with great caution because although only local and state permits are needed to execute phase 1, Copper World's timeline is still at risk amid much resistance from the green movement and tribes. Not to mention, there is a long road ahead.

For further details see:

Hudbay Minerals: Copper Mountain Merger Injects Timely Cash Flow