CA - Hudbay Minerals: Looks Like A Tough Year Ahead

2023-03-14 07:09:31 ET

Summary

- The performance of HBM over the next year or so will be determined by demand.

- With the global economy on the brink of recession, if not already in one, it's probably going to get worse before it gets better for the miner.

- One possible positive for the company could be if it's able to execute on its gold guidance.

- Under that scenario, if investors flee to gold as a safe haven, it'll likely push the price of the yellow metal much higher.

Hudbay Minerals ( HBM ) is facing a tough year ahead in my opinion, as the economic conditions are certain to get worse, and it's very doubtful China is going to come to the rescue as it has in the past, because it's facing its own economic slowdown.

In my first bullet point above I mentioned the performance of HBM over the next year will be determined by demand, and that of course is true under any circumstance. The reason I mentioned it is because when doing research on the company, I found a lot of investors suggesting demand is going to improve going forward, which would push up the price of copper. I don't believe that's how it's going to play out; in reality, it's probably going to do the opposite.

The assumptions I'm working from in making that statement is we're going to have a recession in 2023 (I believe we're already in one), and that is going to shrink demand for base metals like copper. We already know that's happening in the construction industry, and that's going to get worse as the Federal Reserve continues to raise interest rates and the cost of capital and mortgages increase.

In this article we'll look at a few of the numbers, but more importantly, the role the weakening economy will play on the performance of HBM during the next year or so.

{kind=link}

Some of the numbers

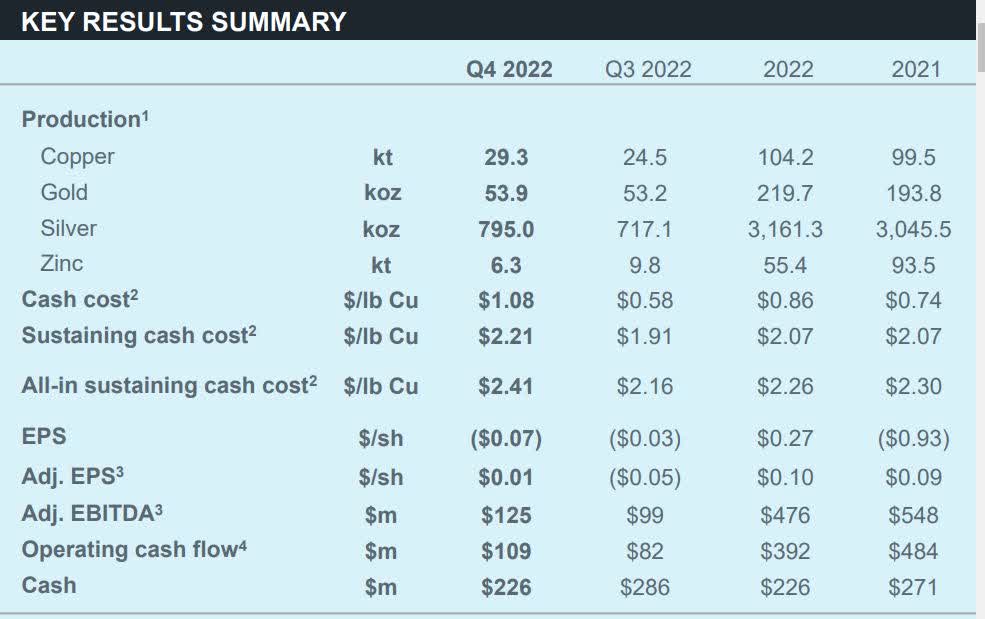

Revenue in the fourth quarter of 2022 was $321.2 million, down 24 percent year-over-year, missing by $74.43 million.

Adjusted EBITDA in the reporting period was $125.00 million, compared to $180.8 million in the fourth quarter of 2021. Full year adjusted EBITDA was $476.00 million, compared to full year 2021 adjusted EBITDA 0f $548.00 million.

Net loss in the fourth quarter of 2022 was -$(17.4) million, or -$(0.07) per share, compared to a net loss of -$(10.4) million, or -$(0.04) per share in the fourth quarter of 2021.

In response to increases in input costs and a drop in the price of copper, the company reduced discretionary costs by $30.00 million in the fourth quarter.

At the end of calendar 2022 the company held cash and equivalents of $226.00 million, with $350.00 million undrawn under its revolving credit facilities.

As for production guidance, the company projected a ten percent boost in consolidated copper production to 114,000 tons, but that was below previous guidance of 133,000 tons it stated in January 2023. Concerning gold production, the company projects it to jump to 285,000 oz for full year 2023, a gain of 30 percent. But again, that is down from previous guidance of full year 2023 gold production of 290,000 oz. Even though production may improve, the key to the performance of HBM for 2023 will be how demand plays out.

{kind=link}

Demand outlook

There are two ways to look at 2023 demand for copper, and that is whether there will be a recession or not. I've seen quite a bit of commentary around the Internet concerning how demand from China will increase copper demand while being a price catalyst for the base metal. I don't hold that view. I think the global economy is going to continue to deteriorate, the housing market come under more pressure, and demand for copper in the near term to decline. That will put downward pressure on the price of copper, and of course the share price of HBM.

With the Federal Reserve determined to battle inflation by continuing to raise interest rates, it'll cool down the U.S. economy, as will other central banks engaging in similar practices in other parts of the world. This will, as mentioned above, have a significant impact on the construction market, which according to Statista , accounts for 46 percent of copper usage in the U.S. in 2022.

The other major use of copper in the U.S. market is in electric and electronic products, which accounts about 21 percent of U.S. demand, according to Statista.

With consumers already prioritizing spending, I believe electronic products will probably decline in demand throughout 2023, and possibly early 2024 as well, which combined with reduced demand in construction, should result in lower copper prices going forward.

In my view, how HBM will do over the next year or so will be determined by the price of gold, and if it increases in price in response to investors seeking safety in the uncertain economic environment we face. I think it could go higher, but it hasn't been behaving as it has under these types of economic scenarios in the past, so we'll have to wait and see there.

If gold does jump, it'll at least offset some of the expected underperformance of copper.

Share price movement

Looking at a 5-year chart of HBM, its share price has gone nowhere. It has been very volatile during that time, although from November 9, 2020 through May 16, 2022, it did hold at approximately $5.18 per share as a bottom, before finally capitulating and falling to its 52-week low of $3.08 on July 11, 2022.

It has been moving up since then, but I see no catalyst at this time that would suggest it's a sustainable upward move.

Based upon my thesis that the global economy is going to get worse in 2023, I see copper demand shrinking more, along with its prices, and that will put downward pressure on the share price of HBM.

For those that are looking for the time when the Fed finally pivots and the construction market rebounds, there should be a good chance to get an attractive entry point that will reward patient shareholders over time.

But at the current price level, I see it as elevated in contrast what I believe is coming ahead of us economically.

Conclusion

Management is making the correct decision in deciding to cut costs in light of higher input costs and weakening demand for copper.

If guidance holds out concerning gold production and the price of gold cooperates with the company by jumping significantly higher, HBM could surprise to the upside; at least in the sense that gold revenue and earnings makes up for the expected decline in copper revenue and earnings.

And if the price of gold soars, the company could even surprise in revenue and earnings, even if copper doesn't do well. That's the very best-case scenario, one that I think isn't likely to happen. I see gold probably offsetting some of copper's weakness, but probably not reaching high price levels.

How high the price of gold could go will depend on the length and depth of the recession, and what else the Federal Reserve may break in the economy before it reverses direction.

At best, I see HBM as being an opportunity for investors looking for a favorable entry point that mitigates some of the downside risk if having a position in the miner.

The worst-case scenario would be if copper demand remains low along with copper prices, and shareholders end up under water for a prolonged period of time. I think it's best to wait for a much lower entry point if interested in HBM, as there just isn't enough upside at its current price level to justify the risk.

For further details see:

Hudbay Minerals: Looks Like A Tough Year Ahead