CA - Hudbay Minerals: Quality Business But Lacking Some Incentives For A Buy

2024-01-10 08:10:02 ET

Summary

- Hudbay Minerals Inc. focuses on mining copper, gold, silver, and zinc, with copper and gold showing positive financial results.

- The company's dividend yield is currently low, and its valuation is relatively high, making it less attractive for investment.

- Hudbay Minerals has a diverse portfolio and owns the Constancia mine in Peru, with tailwinds from increased demand for copper and zinc in green energy ventures.

Investment Rundown

Mining companies can be a risky venture sometimes to invest in. They are often heavily driven in terms of earrings by favorable commodity prices. One such company is Hudbay Minerals Inc (HBM) which is operating out of Peru and Arizona in the States. The types of minerals the company focuses on are copper, gold, silver, and zinc. Both copper and gold are steadily trending higher and have been positively shown in the financial results for the company as they achieved record quarterly revenues.

With a lot of mining companies, they tend to have a very solid dividend yield to reward shareholders. With HBM, you are not getting that right now, unfortunately. The yield is under 0.3% right now and with a relatively high valuation as well for a commodities company I think there isn't enough justification here to make for a buy. The company will experience strong demand I think as copper and silver are crucial elements in our path towards green energy. As for copper, there are some estimates of a significant shortage which could drive up prices and benefit HBM very well over the medium term. Until the price comes down or the dividend is raised to a more attractive level I think a hold here is best suited.

Company Segments

HBM has a rather diversified business model that directs its efforts toward the exploration, development, operation, and optimization of properties spanning North and South America. The company's diverse portfolio includes the production of copper concentrates enriched with copper, gold, and silver, as well as zinc concentrates, zinc metal, and gold and silver doré. Additionally, HHBM extracts molybdenum concentrates, showcasing the depth and breadth of its mining capabilities.

{kind=link}

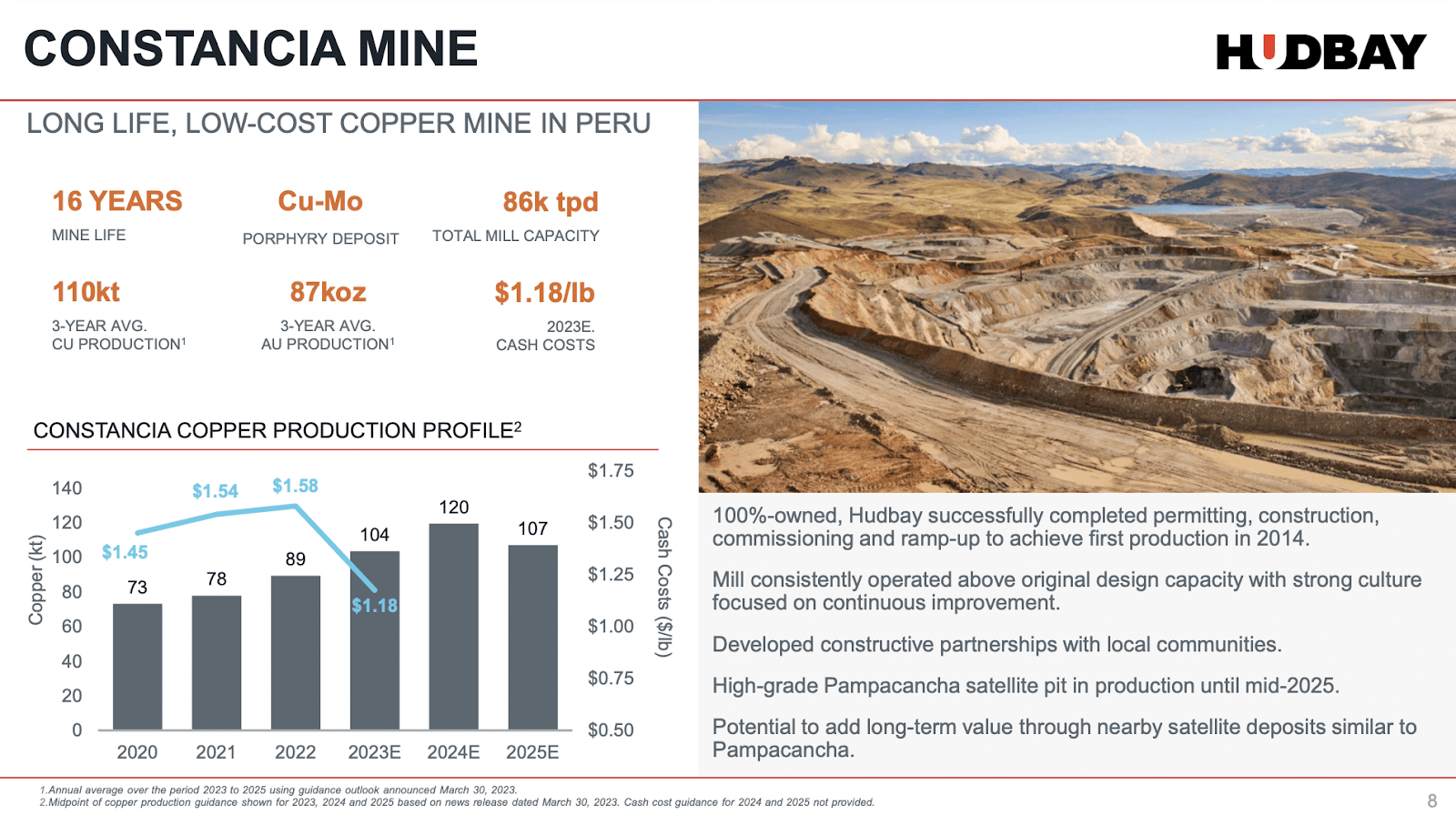

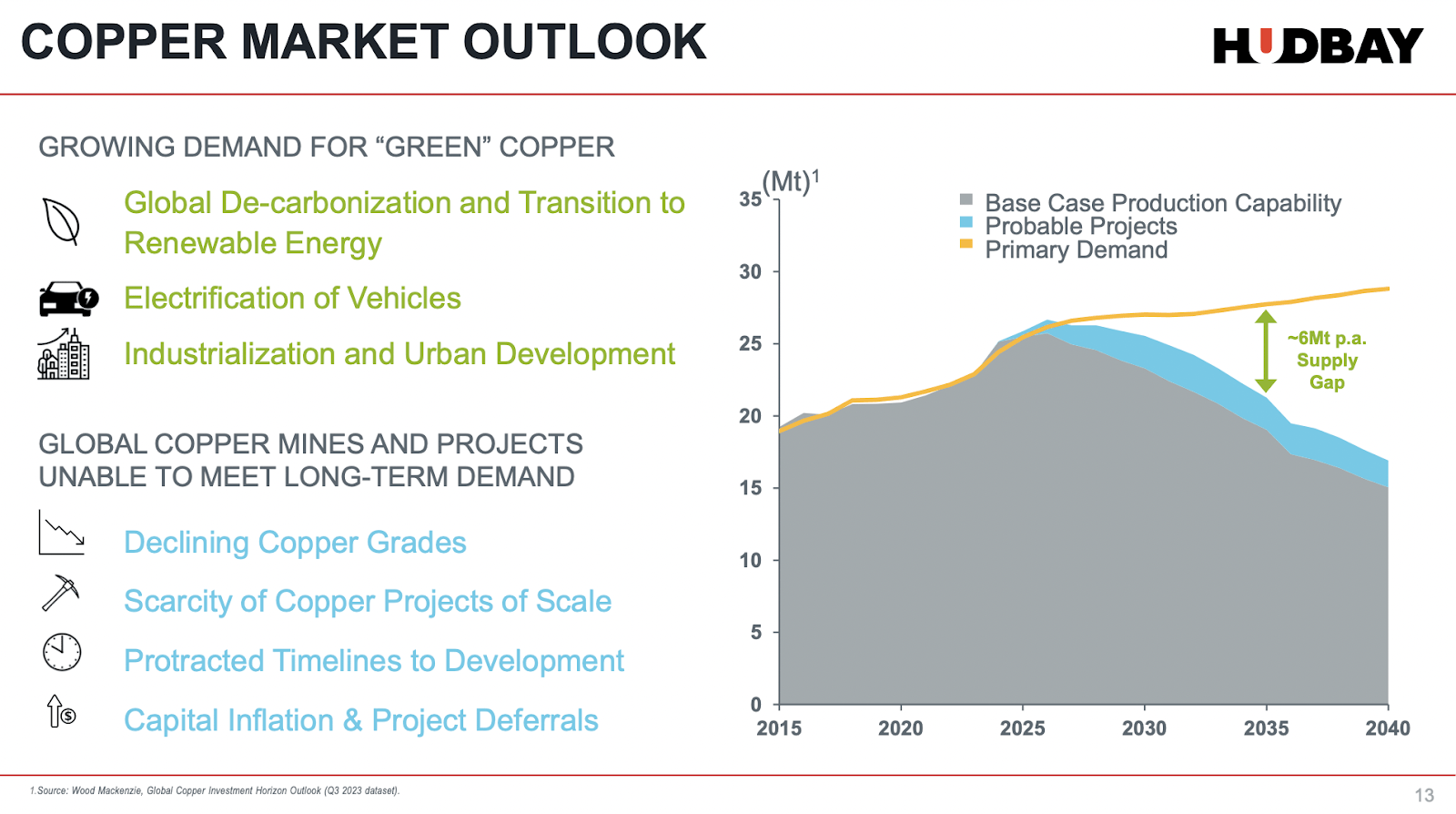

At the core of the company's operations is the flagship Constancia mine , a project fully owned by HBM. Situated in the Province of Chumbivilcas in southern Peru, the Constancia mine stands as a testament to the company's strategic focus on extracting valuable resources from geologically rich regions. Some of the major tailwinds for the company will be the increased need for materials like copper and zinc for our EV car production and other green energy ventures.

{kind=link}

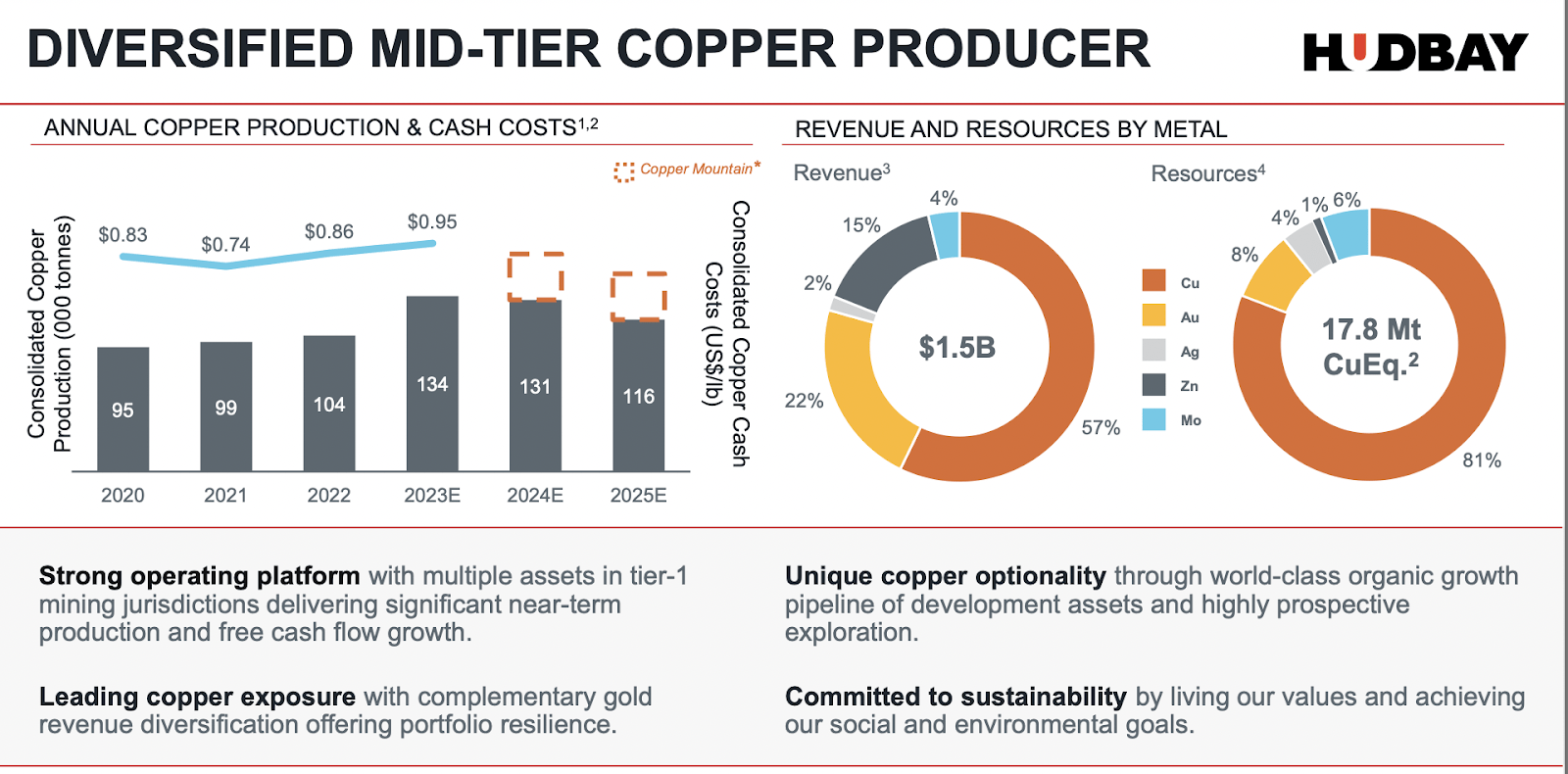

Over half of the total revenues are coming from copper with gold in second place with 22% of total revenues. What has enabled the company to continue to deliver strong revenues and financial results has been the expansion of its asset base throughout the last years. In September of 2023, for example, HBM acquired Rockcliff Metals which helped triple the land ownership in the very appealing Snow Lake region . The region contains large deposits of gold, silver, zinc, and copper, all minerals that HBM works with normally. I have mentioned that HBM trades at a pretty high premium in terms of a mineral company, and a valid cause for this might be the exceeding results from the Snow Lake region. The Lalor mine that HBM owns was originally expected to operate at 3.300 tpd but is at 4000 instead, significantly increasing the output and potential earnings. With the New Britannian mill starting operations in late 2021 the annual gold production is at 180 000 ounces new until 2029. With current gold prices, this would equal around $370 million in revenues.

Earnings Highlights

{kind=link}

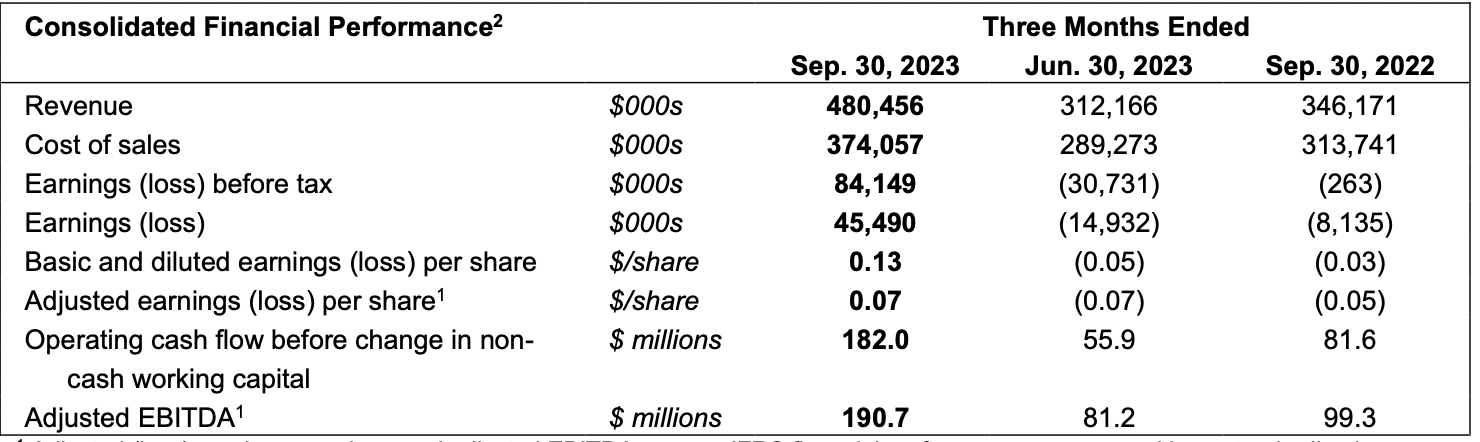

Last quarter the revenues came in at $480 million, setting a record for the company as prices of gold and copper have appreciated very well in the last couple of months. But apart from a good pricing environment, HBM has also been able to increase its production levels very well. Gold production for example reached record levels at 101 417 ounces. This was the cause of higher grades realized in two of the larger mines the company operates. With this also came increased operating cash flows as well, $182 million, up from $52 million in the second quarter of FY2023.

{kind=link}

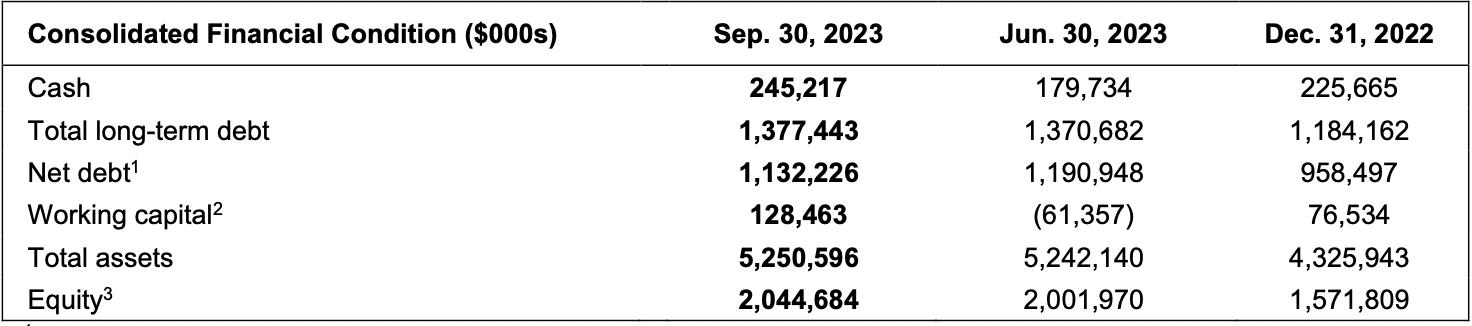

On the financials of the company, I think HBM remains in a good place right now. The cash has improved since late 2022 and is providing the business with the ability to pay down a significant portion of its debts, valued at $245 million. With the equity at $2.04 billion, you are buying the company at a below-equity value, which I think is positive, but not enough to make it a buy. I still find that the margins need to stabilize and for them to remain positive for a longer period. If they fall even slightly HBM will begin to very quickly look very expensive.

{kind=link}

Copper will continue to be a big part of HBM and the recent price improvement for gold has meant that strong financial results have been possible, but over the long term, I think most of the value will be derived from copper demand. HBM states that some of the tailwinds are the electrification of vehicles and the industrialization and development of urban areas, all of which need strong copper supplies. Copper grades are falling and this is creating a shortage of high-grade ones which are needed for more high-end technological uses. I think this is a space where HBM can efficiently enter and be a supplier. Until the price falls to a more reasonable level, somewhere around the 15 - 16x earnings multiple ranges, which is in line with the sector, I won't be making it a buy.

Risks

Trading at a notable premium compared to many mining companies, HBM faces heightened expectations to sustain its impressive performance, particularly with the imperative for Snow Lake to exhibit robust production levels. The company operates under the weight of this premium, which for the FWD p/e non-GAAP is at 40% right now, placing it under increased scrutiny to deliver strong results. On a book value though, HBM looks more attractive, trading under 1, which is something I value quite highly as I think the asset base of the business is solid, and getting a discount on it is of course very good. The financial performance of HBM is intricately tied to commodity prices, and any downturn in these prices could exert considerable pressure on the company's fiscal outcomes, potentially triggering a decline in share prices.

{kind=link}

Another notable risk for HBM lies in the relatively slender profit margins it operates within. Over the past 12 months, the net margins have hovered just under 1.3% , reflecting a level that may be perceived as relatively thin within the industry. It's worth highlighting that the company benefited from some additional operating incomes last year, contributing to a positive impact on the bottom line. However, the burden of interest rates has posed a significant challenge, with expenses reaching a total of $75 million . In the coming reports, I want to see a steady line upward for the et margins. It's of course a little out of the company's control as their earnings are tied to commodity prices, but ensuring they don't take on unnecessary amounts of debt or see their assets depreciate rapidly, then I think they will be good.

Final Words

Mining companies can be quite volatile in terms of their earnings. They are heavily dependent on strong pricing environments. I think HBM has made strong strides in the last few years and right now the asset base they control holds a lot of potential, especially the Snow Lake region. However, I want to see more shareholder value here like a raised dividend or a lower entry price before making it a buy. Because of this, I think HBM is better suited as a hold for now.

For further details see:

Hudbay Minerals: Quality Business But Lacking Some Incentives For A Buy