GOOGL - Hudson Pacific Properties: Downgrading Common And Preferreds To A Sell

2024-01-16 10:00:00 ET

Summary

- We had HPP and its preferred shares on a "hold" as the risks offset the potential rewards.

- Both stocks have had a sharp rally off the October bottom.

- We dissect the recent numbers and tell you why we are going in the opposite direction.

We have been covering Hudson Pacific Properties, Inc. ( HPP ) for slightly longer than a year , and our stance has generally been one of caution. In our last update, we analyzed the Q2-2023 results and told you that covenant tripping was a genuine risk for the next 12 months.

So far, we have not tripped any covenants. The two we would watch most carefully are the ones highlighted below.

HPP Q2-2023 Supplemental

{kind=link}

The stock has rallied nicely with the easing financial conditions and is up 70% since the October bottom. We look at where we stand today and why investors should not use the stock price as a barometer of what is actually happening.

Q3-2023

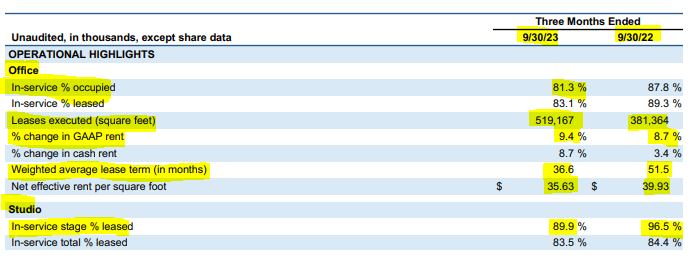

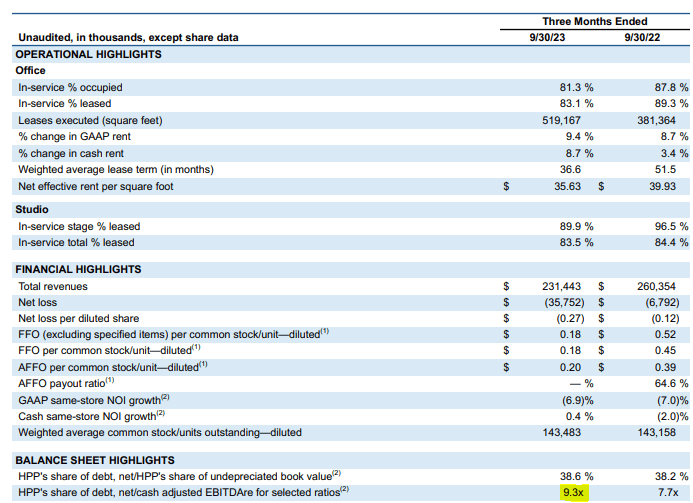

The third quarter had a lot of interesting data. Office occupancy came in at 81.3%. While the year-over-year declines are shown below, one needs to note that the occupancy fell from 85.2% in Q2-2023.

{kind=link}

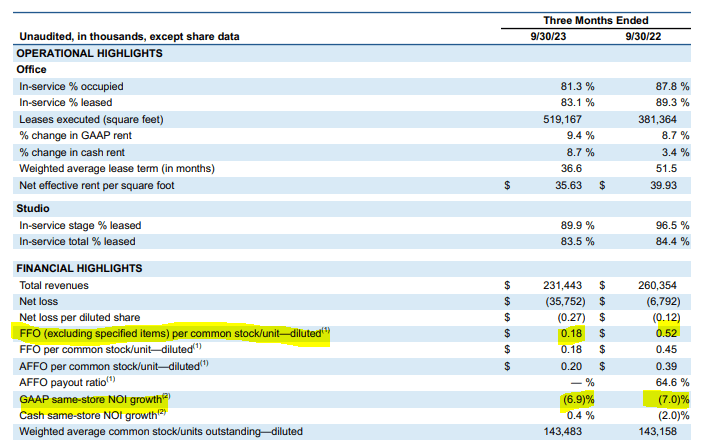

Management noted that leasing activity had picked up, and that is certainly visible in the 519,167 square feet of newly executed leases. Notable here is that the lease terms were for just three years. That is definitely on the low side for offices, and even lower than the 51.5 months seen last year. The relatively small changes in occupancy levels decreased same-store net operating income or NOI by around 7%. This follows a similar 7% drop last year. Total NOI dropped more than that as HPP sold a few small properties. But the problem for HPP is that its structure is still extremely leveraged. The simplest way to visualize this is to see the relative movement in NOI to the movement in funds from operations ((FFO)). FFO was down by about 65% year over year.

{kind=link}

Q2-2023 came in at 24 cents on FFO, so the pressures have been unrelenting here. The REIT was active in the capital markets with a few small transactions occurring.

Sold 3401 Exposition office property in Los Angeles, California for $40.0 million before closing adjustments.

Sold 604 Arizona office property in Santa Monica, California for $32.5 million before closing adjustments.

Entered into a joint venture with Vornado and Blackstone to own the leasehold interest for Pier 94 in Manhattan, New York, and develop and operate a 6-stage, 232,000-square-foot purpose-built Sunset Studios facility, representing an expected $38.5 million total capital requirement for Hudson Pacific.

Source: HPP Q3-2023 Supplemental

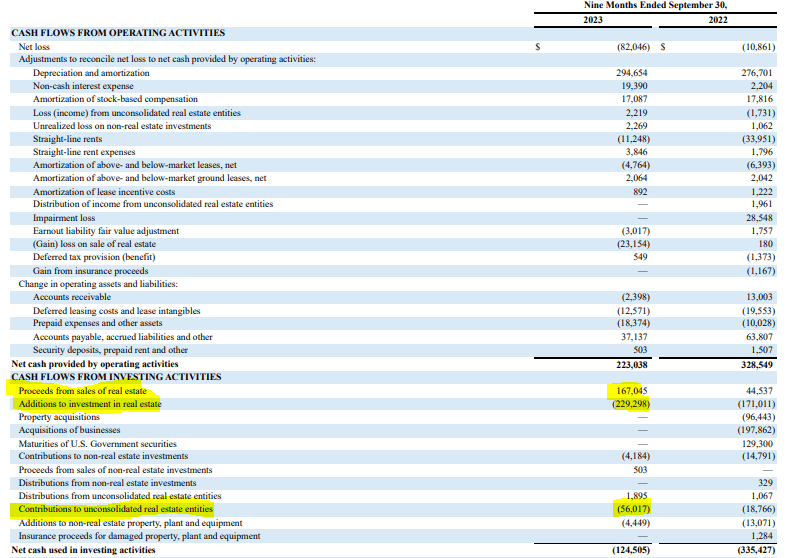

While those asset sales were definitely helpful, HPP's capital expenditures for existing properties and its development commitments still created a negative overall cash flow.

{kind=link}

Outlook

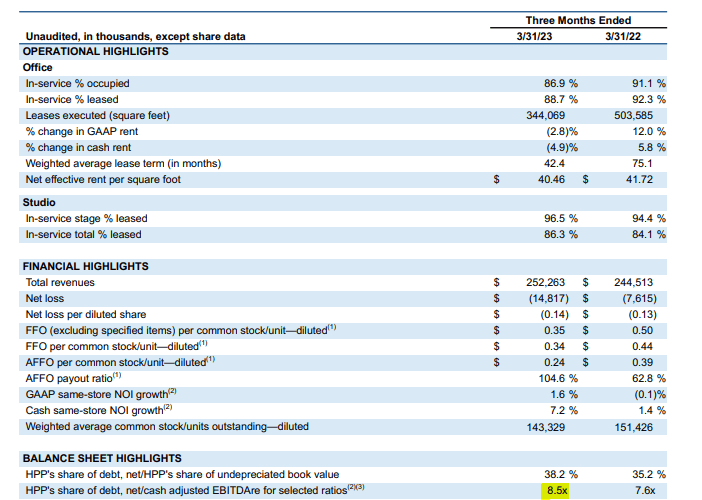

You can draw some conclusions based on these results as to just how bad things are in Fog City. A better way, though, is to see the rate of change from Q1-2023. There are two metrics we will emphasize here besides the FFO. The first is the debt to EBITDA. In Q1-2023 this had risen to 8.5X versus 7.6X last year.

{kind=link}

This quarter, we were at 9.3X.

{kind=link}

The second metric is the total liquidity. This was over $825 million in Q1-2023.

$828.3 million of total liquidity comprised of $163.3 million of unrestricted cash and cash equivalents and $665.0 million of undrawn capacity under the Company's unsecured revolving credit facility.

Source: HPP Q1-2023 Supplemental

After Q3-2023, this was down significantly.

$555.0 million of total liquidity comprised of $75.0 million of unrestricted cash and cash equivalents and $480.0 million of undrawn capacity under the unsecured revolving credit facility.

Source: HPP Q3-2023 Supplemental

This liquidity got crunched further post the Q3-2023 results.

In consideration for the enhancements afforded under the amendment, the aggregate commitments from the lenders under the unsecured revolving credit facility were reduced by $100 million, to $900 million of total commitments, with the maturity date remaining December 2026 (including extension options).

Source: Seeking Alpha

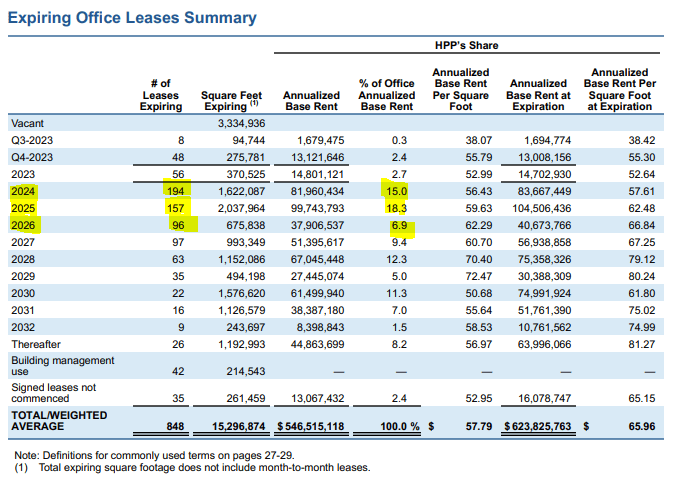

To this lowered liquidity profile, we have to add the next 3 years of lease maturities.

{kind=link}

You have to remember that HPP's vacancy rate is still sub-20% and its primary city's vacancy rate is now, over 35%!

San Francisco's amount of vacant office space has reached the highest level ever recorded in the city's history.

According to preliminary fourth quarter data provided by real estate brokerage CBRE, the city's vacancy rate ticked up nearly 2 percentage points from the previous quarter, reaching 35.9% at year-end. In September, that number was at 33.9%, the previous record high.

The increase was driven by several large subleases placed on the market in recent months, as well as direct spaces given back by office tenants, resulting in 1.4 million square feet of negative net absorption, or occupancy loss. For 2023, the city had a total occupancy loss of 6.7 million square feet, which is the second highest total since 2020, when the city recorded 9.9 million square feet of negative net absorption.

Source: San Francisco Chronicle

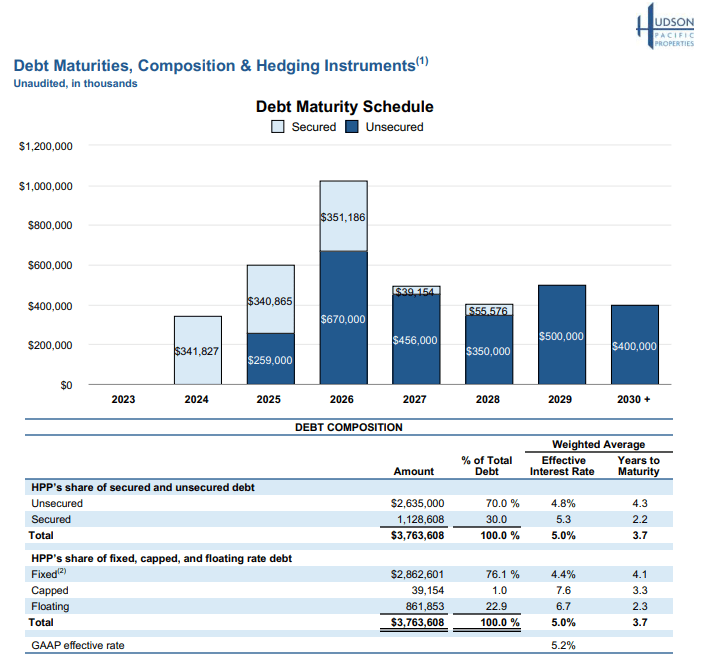

In any kind of convergence scenario, where say the two meet at even 27% in 3 years, HPP is likely going to not make it. The reason is that the upcoming debt wall is just too daunting. 2024 looks manageable, but 2025 and 2026 look very rough. We will also point out that the weighted average interest rates are just too low relative to where this debt profile would be financed today, even after the credit easing of the last 3 months.

{kind=link}

Verdict

Yes, we think the odds are high that with the credit conditions easing, and the $189 million asset sale , the company will likely make it through 2024. But in our base case of vacancy reaching 25% levels in 2 years, the company will not make it through the 2026 debt wall. Yes, the market has priced in great credit easing and BB spreads have collapsed. If you want to speculate on some junk bonds, there might be a few that offer good risk-rewards. Here, we have 35% vacancy levels in San Francisco, with some of the mega-cap techs like Alphabet Inc. ( GOOG ), just starting their layoff cycles . And don't say these won't matter to HPP eventually.

{kind=link}

We are moving the common shares to a Sell rating.

Hudson Pacific Properties, Inc. 4.750% CUM PFD C ( HPP.PR.C )

The preferred stock yields 8.22% currently. That might sound appealing to some but keep in mind that the interest expense in the most recent quarter was around $53 million and FFO was at $26 million. So if you add the interest expense back to FFO and then do an interest coverage ratio, you are close to 1.5X. 8.22% is way too little for that. Brookfield Infrastructure Partners L.P. 5.125 CL A PFD13 ( BIP.PR.A ), one we recently bought, was yielding 7.8% and has a corporate interest coverage of over 3.0X. Brookfield Infrastructure's ( BIP ) preferreds have a higher rating than the debt of HPP . So even on a relative basis, it is hard to argue that there are no better opportunities in the market. While we recognize that these could deliver a positive return over the next 6 months, we are moving this to a Sell as well.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Hudson Pacific Properties: Downgrading Common And Preferreds To A Sell