CA - Hydro One: There's Better Opportunities Than This Overvalued Utility

2024-01-12 04:18:35 ET

Summary

- Hydro One is a government-owned electricity transmission and distribution company in the province of Ontario.

- The company has a stable and predictable business as a regulated utility in Canada.

- Despite this, with shares close to 52-week highs, the stock is overvalued with a high P/E ratio and a lower dividend yield compared to peers.

Please note all $ figures are in , not , unless otherwise stated.

Company Overview

Hydro One ( H:CA ) is a the largest electric transmission company in Ontario, Canada, and transmits and distributes much of the province's electricity. Its network delivers electricity to nearly 1.5 million households which represents a little more than a quarter of the province. Most of its customers are rural customers who live outside the main cities like Toronto.

Hydro One was previously a government-owned company, but in 2015, the province of Ontario sold 60% of the company in an IPO to sell to private investors. The IPO allowed the government to fund various transit and infrastructure projects and allowed investors to share in the profits of Hydro One's business operations by investing in the stock.

Since its IPO, Hydro One has had a history of paying a growing dividend of about three-quarters of net income, with a quarterly dividend that has grown at a 5% CAGR. At present, the current yield on the stock is about 3.0%.

Dividend History (Q3 Presentation)

{kind=link}

Q3 Results

While we should expect to see Q4 results early next month in February, let's take a look at the Q3 results in November to get a sense of the recent business performance.

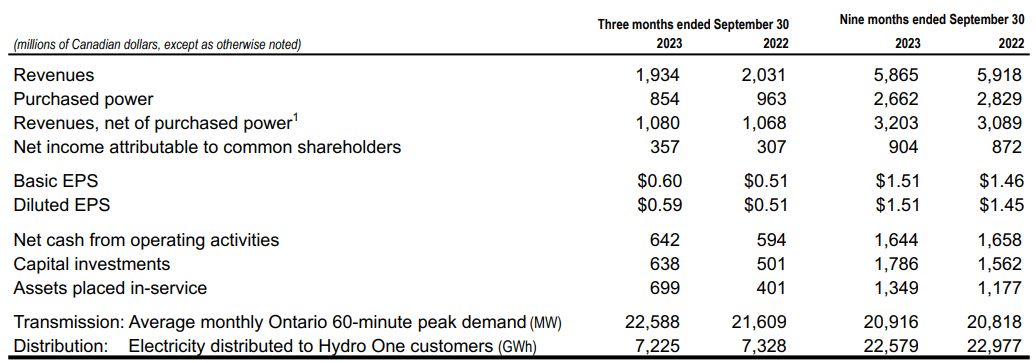

Hydro One operates very steady business, as is true for almost all regulated utility companies, so this quarter's consistent results were no surprise. For the third quarter, revenues net of purchased power came in at $1.080 billion, up 1.1% from $1.068 billion for the same quarter last year.

{kind=link}

The increase in revenue was mostly driven by higher OEB approved rates, but was partially offset by lower purchased power costs. All in all, this led to an increase of 16% in diluted EPS. Subsequent to quarter-end, the company also announced 3 new priority transmission lines in Northeast and Eastern Ontario to service the growing demand for electricity in this region.

On the earnings call , the company also mentioned that through its equity partnership model, they may sell a 50% stake to First Nations for the 3 transmission line projects. I believe these transmission lines are significant for the province as they are expected to support the production of steel, reduce carbonization for the industry, and also fuel the province's economic development and growth.

The company also mentioned that they signed three collective agreements with their workforce. One was with the Power Workers Union and the other was with the Society of United Professionals.

In my view, this is significant as it will provide certainty on the company's SG&A figures (particularly labor expenses) until 2025 and also reduces the near term risk of strikes and other labor-related disruptions. By successfully negotiating these collective agreements, Hydro One has fostered a more stable labor environment which leads to predictability in the company's earnings for the foreseeable future.

Investment Thesis

One thing I can say for sure about my bear thesis, is that it's not a result of higher than average debt on the balance sheet or its ability to refinance current debt at attractive rates.

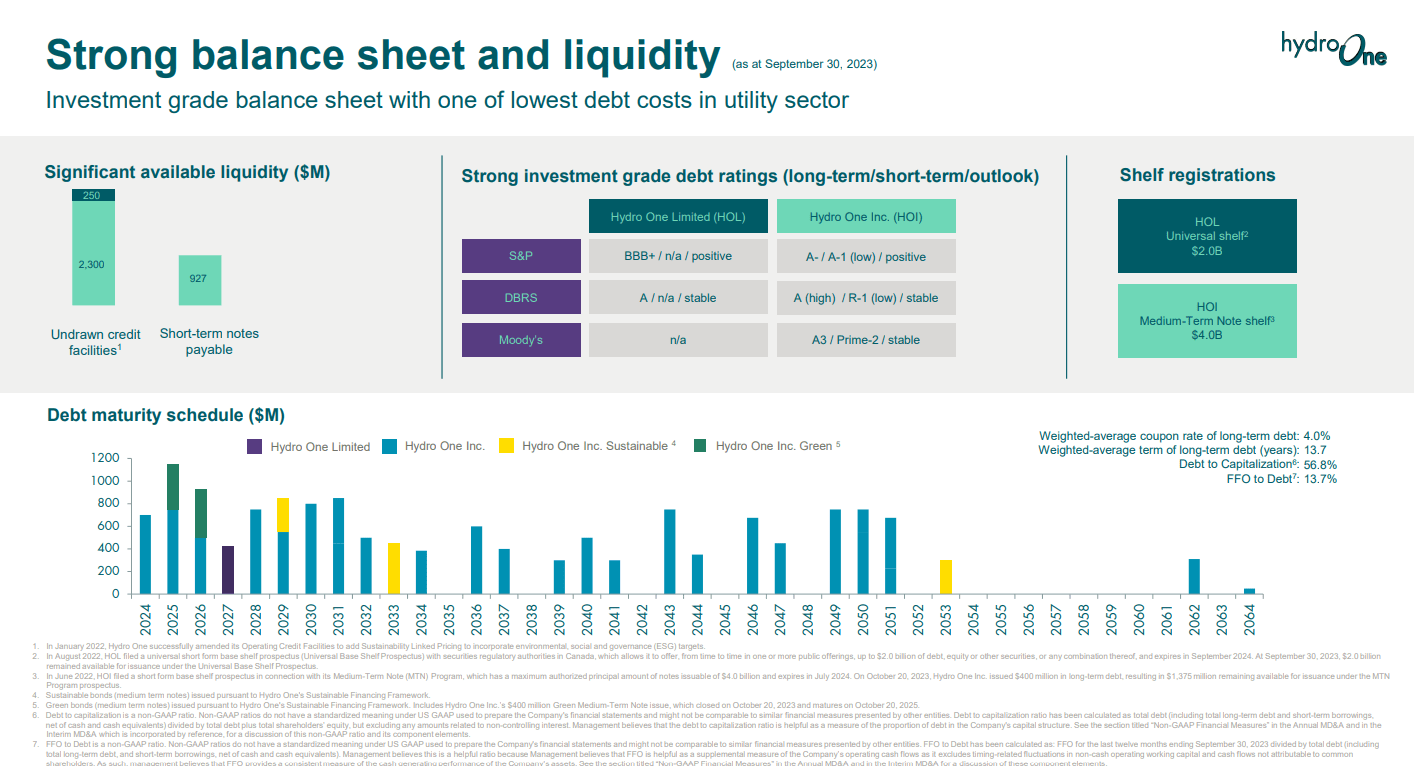

When looking at the company's financials , the company has $14.5 billion of long-term debt ($700 million of which is due in one-year) along with $927 million of short term borrowings. While its fairly typical for utilities to have a high debt load, Hydro One has a medium-high debt load at 5.6x Net Debt to EBITDA, compared with Canadian Utilities ( CU:CA ) at 5.2x and ATCO ( ACO.X:CA ) at 4.7x. Fortis ( FTS:CA ) has a Net Debt to EBITDA of 5.8x and Emera has a ratio above the pack coming in at 6.7x.

Balance Sheet Overview (Investor Fact Sheet)

{kind=link}

I also don't believe that Hydro One is grossly overleveraged or will face challenges in refinancing. The province of Ontario still has a heavy stake in the company and would likely come to aid the company if debt challenges arose (but we're not there yet). The company was still able to access an additional $425 million of floating rate notes maturing in 2026 at an interest rate of around 5.5% in November and was able to offer up $800 million of medium term notes at interest rates ranging between 3.9% and 4.4%.

This shows lenders are still willing to lend money to Hydro One at attractive rates, given its solid credit ratings around A-. The weighted average coupon rate is 4.0% and FFO to debt sits in at around 13.7%.

So why then am I bearish on the company's outlook? Well, despite having a very predictable business model with minimal disruptions, Hydro One's stock is very overvalued.

With 3 Hold ratings and only 1 buy rating, the four equity research analysts with one-year target prices on Hydro One's stock have an average target price of $37.80, with a high estimate of $42.00 and a low estimate of $35.00. From the average target price, this implies downside of 3.2% indicating that analysts don't see near term upside in the stock today.

Even by my own valuation math comparing to peers, the company seems pretty expensive. Looking at the chart below, using TD Securities' forward estimates, despite similar leverage, Hydro One has the highest P/E ratio both on a TTM basis and forward basis and the worst AFFO yield (again, even on a current and forward basis).

{kind=link}

For income seeking investors who often look to utilities for a higher than normal and safe stream of cash flows, the dividend yield is something that you'll obviously consider. Hydro One's dividend comes in at 3.0%, which is lower than the Canadian peer group at 4.7% and U.S. peer group, through the ( XLU ) ETF, at 3.3%. As shown by the graph below, the Utilities ETF now has a higher yield than Hydro One, compared to pre-2023 when the reverse was true. We can also see that the yield on Canadian 10-year government bonds is now lower than Hydro One's dividend yield, indicating that the risk premium for investing in utility stocks has likely narrowed a lot as rates have risen despite utilities (which are leveraged) having maintained their valuation multiples.

Conclusion

For a company expected to drive rate base growth at around 6% a year (albeit higher than the previous decade's growth of 5% a year), I'm not sure why anyone would pay 21.5x earnings (or 20.0x forward) for a business with such minimal growth. With the Canadian banks yielding well over 4.5% as a group, you can get better ROE businesses that actually have room to grow at half the valuations (S&P Capital IQ).

With all this considered, I'm not a buyer of Hydro One's shares today and would recommend investors avoid the company. While I wouldn't be shorting the stock, there's far better yields to be had at more attractive valuations in Hydro One's peers and more earnings growth potential and dividend growth potential in the Canadian banks. As such, I rate shares of Hydro One as a sell.

For further details see:

Hydro One: There's Better Opportunities Than This Overvalued Utility