SPY - HYT: A Worthwhile CEF But May Have To Cut The Distribution

2023-04-12 17:07:53 ET

Summary

- Investors are desperately in need of income due to the rising cost of living.

- BlackRock Corporate High Yield Fund, Inc. invests in a portfolio consisting primarily of junk bonds and then applies a layer of leverage to boost the effective yield to provide this income.

- The HYT closed-end fund should be well-protected against most risks other than interest rates.

- The fund might be over-distributing and might have to cut its payout if it cannot reverse its financial problems in the near future.

- The fund is currently trading at a reasonably attractive valuation.

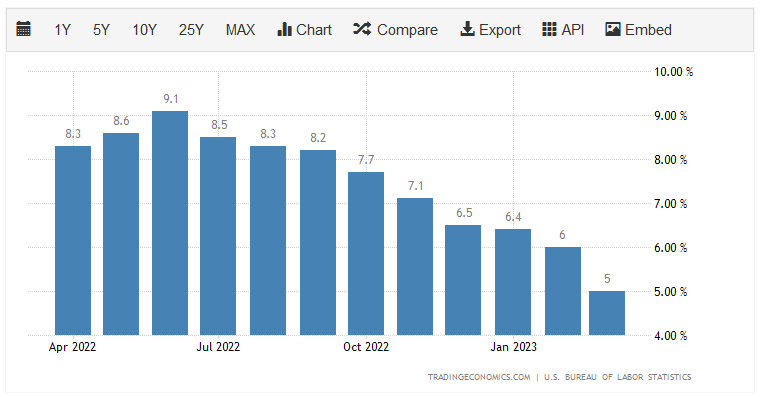

It is hardly an exaggeration to say that the biggest problem facing the average American today is the incredibly high inflation rate that has pushed up the cost of living. This is evident by looking at the consumer price index, which fell to 5% in March but has otherwise been at least 6% higher year-over-year in each of the trailing months:

{kind=link}

This has been going on for quite some time and as of today, real wages have declined for 24 straight months. This situation has forced many people to take on second jobs or enter the gig economy as a wage to supplement their incomes and maintain their standard of living. We have seen other people run up their credit card balances and deplete their savings simply to get by. In short, people are desperate for extra money simply to maintain their standard of living.

Fortunately, as investors, we do not have to resort to such methods in order to obtain extra money to support ourselves. This is because we are able to put our money to work for us. One of the best methods through which this can be accomplished is by purchasing shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are admittedly not very well-followed by the investment media and likewise, many financial advisors are not familiar with them. This makes it harder for us to find information about these funds than we might like. This is unfortunate because closed-end funds offer a number of advantages over open-ended funds and exchange-traded funds. One of the most significant of these is that they are able to use certain investment strategies that result in them having a much higher yield than just about anything else in the market.

In this article, we will discuss the BlackRock Corporate High Yield Fund, Inc. ( HYT ), which is a fund that investors can purchase in order to earn an income. This is perhaps most evident in the fact that the fund yields 10.72% at the current price. That is well above the 1.58% yield on the S&P 500 Index ( SP500 ) and even well above the 2.57% yield on the Bloomberg U.S. Aggregate Bond Index ( AGG ).

I have discussed this fund before, but a few months have passed since that time so naturally there have been some things that changed. This article will therefore focus specifically on these changes as well as provide an updated analysis of the fund's financial performance. Let us proceed onward and see if this fund could be a good addition to a portfolio today.

About The Fund

According to the fund's webpage , the BlackRock Corporate High Yield Fund has the stated objective of providing its shareholders with a high level of current income. This is not surprising considering that this is a fixed-income fund. As we can see here, 96.03% of the fund's assets are invested in bonds alongside small allocations to preferred stock and various other things:

CEF Connect

Generally speaking, any bond fund will have the goal of providing its investors with a high level of current income. This is because this is the method through which bonds deliver essentially all of their investment return. After all, a bond will be issued at face value, make regular interest payments to its investors, and then pay off the face value at a set date in the future. These securities have no link to the performance of the issuing company and do not benefit from its growth and prosperity. After all, a company will not increase the payments that it makes to its creditors just because its profits go up. As such, bonds have very limited potential for capital gains.

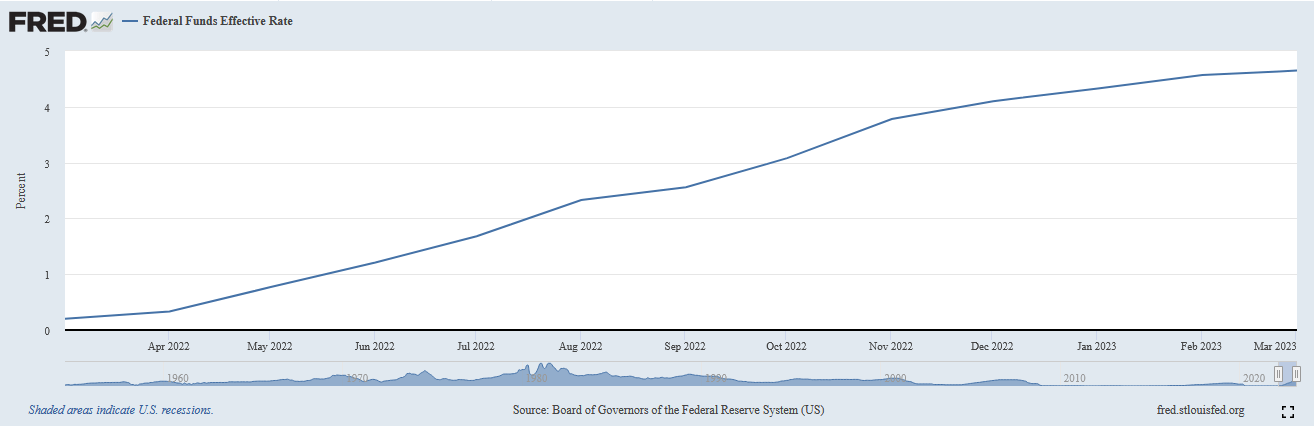

At this point, there are certain to be some readers that point out that bonds are indeed capable of capital gains. That is not true if you hold them to maturity, but it is possible to get some capital gains from bonds by selling them prior to maturity. This is because bond prices vary based on the market interest rate in the economy. In short, when interest rates go up, bond prices decline. The reverse is also true. As everyone reading this is no doubt well aware, the Federal Reserve has been aggressively hiking interest rates for quite some time. In March of 2022, the effective federal funds rate was 0.20% but today it is 4.65%:

{kind=link}

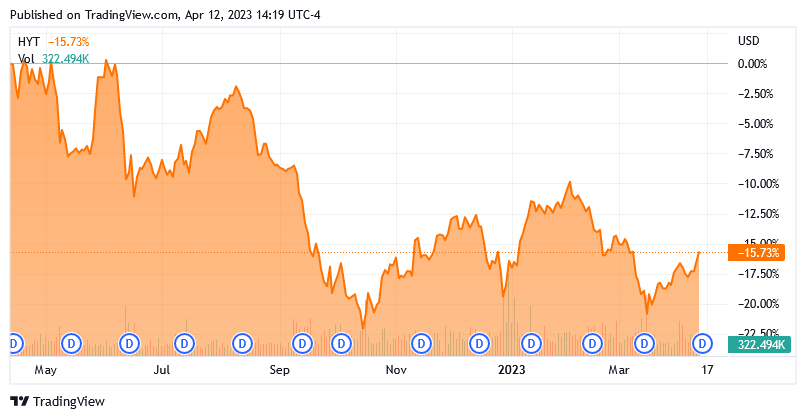

This is one of the fastest series of rate hikes in history, but the Federal Reserve felt that it was necessary due to the high inflation rate in the economy. Truthfully, the Federal Reserve was probably correct in this because the long-running 0% interest rate policy had caused all sorts of economic distortions throughout the United States and abroad. This did have the effect of pushing down bond prices though, as the Bloomberg US Aggregate Bond Index is down 4.79% over the past twelve months. The BlackRock Corporate High Yield Fund is down much more, falling 15.73% versus its year-ago price:

{kind=link}

The reason for these declines is that brand-new bonds will be issued with a yield that is based on the market interest rate at the time of issuance. As today's rates are higher than they have been in more than ten years, this means that most existing bonds have a lower interest rate than newly issued ones. Thus, there is no reason for anyone to buy an existing bond when an identical brand-new one is a higher-yielding investment. As such, the price of the existing bond must decline in order for it to deliver a competitive yield to maturity. It is important to note though that this does not necessarily mean that the fund lost any money. After all, the bond will still pay out its face value at maturity. All it has suffered are unrealized losses unless it actually sells some of the bonds in the portfolio.

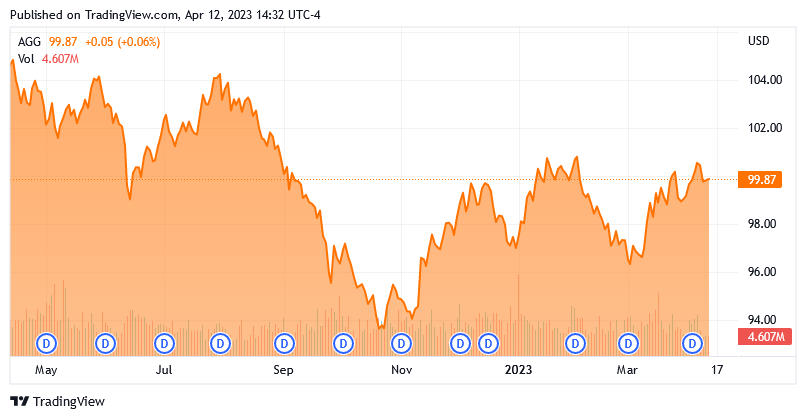

Unfortunately, it does appear that the BlackRock Corporate High Yield Fund is actively trading bonds. Its annual turnover was 45.00% during 2022, which is higher than the average for a fixed-income fund. The reason that this is important is that it costs money to trade bonds or other assets, and these expenses are billed directly to the shareholders of the fund. This creates a drag on the fund's total returns and makes it more difficult for the fund's managers to earn a competitive return. After all, they need to generate sufficient excess returns to both cover these extra costs and still give the fund's shareholders an acceptable return. Few management teams are able to do this consistently, which tends to result in actively-managed funds underperforming their benchmark indices over extended periods. In the case of this fund, the trading activity appears to have resulted in the fund realizing losses that otherwise would have faded if it had waited a few months. We can see that in the fact that the Bloomberg US Aggregate Bond Index recovered much of its 2022 losses in the first three months of this year:

{kind=link}

Thus, it appears that BlackRock's trading activity actually prevented the fund from recovering from its losses.

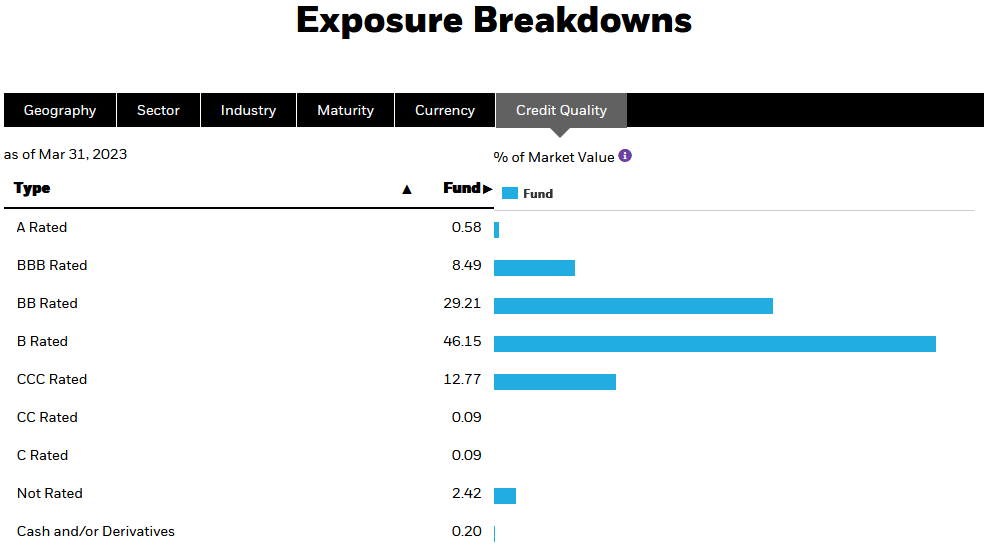

As the name of this fund implies, the BlackRock Corporate High Yield Fund invests heavily in high-yield bonds. These are the securities that are colloquially known as "junk bonds." This is something that might be concerning to more conservative investors that want to ensure the preservation of principal. After all, we have all heard about how it is very likely that the issuer of a junk bond will default on the issue. We can gain a bit of comfort by looking at the credit ratings that have been assigned to the securities in the portfolio. Here is the high-level summary:

{kind=link}

Anything that is not rated A or BBB is considered a junk bond, so we can clearly see that this is the majority of the fund's portfolio. However, we also see that 75.36% of the portfolio is invested in BB or B-rated securities. These are the two highest possible ratings for junk bonds. According to the official bond ratings scale , a company whose securities are awarded these ratings do have the financial capacity to cover its debt and should be able to withstand a short-term economic shock without defaulting. While they are more vulnerable to a long-term downturn than an investment-grade company, such events are quite rare and far between, so we probably do not need to worry too much about a default with respect to the overwhelming majority of the portfolio. In addition to this, the fund has 1,369 unique securities in its portfolio so any individual default will only have a minimal effect on the portfolio. Thus, we do not need to really worry about the risk of defaults. The biggest risk with this fund is interest rates.

Leverage

As stated in the introduction, closed-end funds like the BlackRock Corporate High Yield Fund are capable of employing certain strategies that have the effect of boosting their yields beyond that of any of the underlying assets. One of the methods through which this can be accomplished is the use of leverage. In short, the fund is borrowing money and then using that borrowed money to purchase high-yield bonds and other income-producing assets. As long as the interest rate that the fund has to pay on the borrowed money is less than the yield of the purchased securities, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are significantly lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. This may be one reason that the fund underperformed the index as severely as it did over the past year, in addition to the reasons that we already discussed. As such, we want to ensure that the fund does not employ too much leverage since this will expose us to too much risk. I usually like to see a fund's leverage stay under a third as a percentage of its assets for this reason. Fortunately, the BlackRock Corporate High Yield Fund satisfies this requirement as its levered assets comprise 28.09% of the portfolio as of the time of writing. Thus, this fund appears to be striking a reasonable balance between risk and reward.

Distribution Analysis

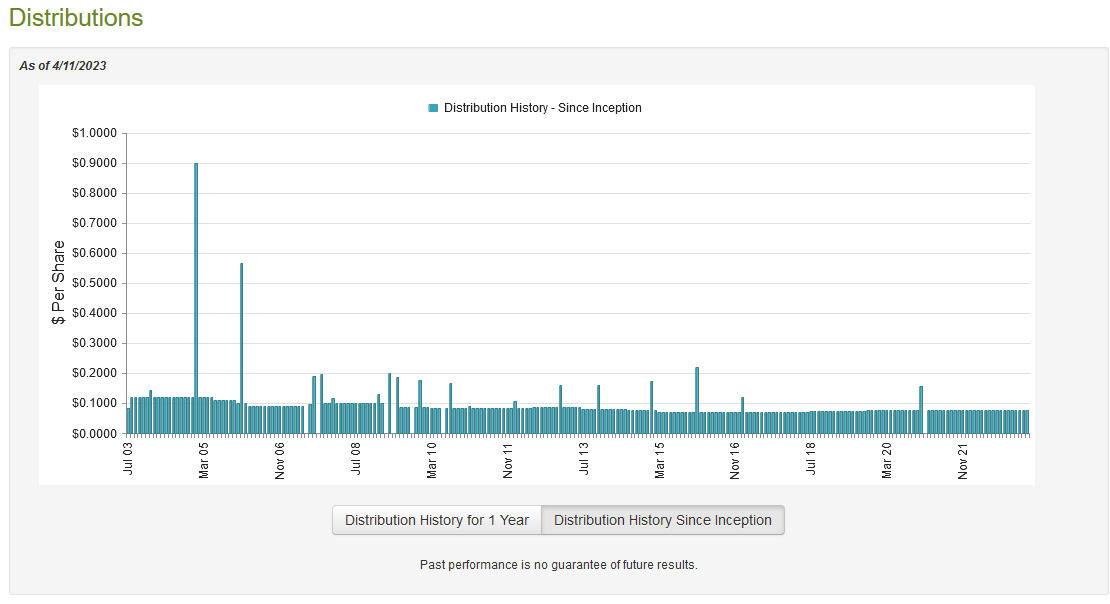

As stated earlier in this article, the BlackRock Corporate High Yield Fund has the stated objective of providing its investors with a high level of current income. In order to achieve this objective, the fund invests in a portfolio consisting primarily of junk bonds, which have a fairly high yield by virtue of their higher risk relative to investment-grade securities. The fund then applies a layer of leverage to boost the effective yield of the portfolio. As such, we can assume that the fund likely boasts a fairly high yield itself. This is certainly the case as it pays out a monthly distribution of $0.0779 per share ($0.9348 per share annually), which gives it a whopping 10.72% yield at the current price. The fund has not been completely consistent about its distribution over the years, but it has done as well or better than most other fixed-income funds:

{kind=link}

The variation in the fund's distribution might reduce its appeal in the eyes of those investors that are looking for a safe and secure payout to use to pay their bills or finance their lifestyles. However, every fixed-income fund varies its distribution with time as the income of these funds tends to vary considerably with interest rates. This one seems to do better than most as far as its consistency, though. The biggest concern here is that anytime the market assigns a double-digit yield to any fund, it is concerned that the fund will be forced to cut its distribution in the near future. Therefore, let us have a look at this fund's finances to attempt to determine the risk of that.

Fortunately, we have a very recent document that we can consult for the purposes of our analysis. The fund's most recent financial report as of the time of writing corresponds to the full-year period that ended on December 31, 2022. This is a much more recent report than what we had available the last time that we discussed this fund and as such it should give us a good idea of how well the fund performed in the second half of 2022. This is important because 2022 was a challenging time for bond funds due to the rising rate environment. During the full-year period, the BlackRock Corporate High Yield Fund received $1,081,187 in dividends and $108,273,649 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, the fund reported a total income of $109,642,819 over the year. It paid its expenses out of this amount, leaving it with $85,310,028 available to the shareholders. Unfortunately, this was not nearly enough to cover the $107,967,726 that the fund actually paid out in distributions over the year. At first glance, this is certain to be concerning as the fund did not have sufficient net investment income to cover its distributions.

However, the fund does have other methods through which it can obtain the money that it needs to cover its payout. The most important of these is capital gains, but as can be expected from the challenging environment for bonds last year, the fund failed miserably at this task. It had net realized losses of $48,802,949 along with net unrealized losses of $243,082,240 during the period. The fund did conduct a share offering that brought in $167,749,786, but it still saw its assets decline over the year. Overall, the fund's assets went down by $145,727,235 over the course of the year after accounting for all inflows and outflows. Clearly, the fund is failing to cover its distributions, which certainly explains the market's fear here. It may ultimately be forced to cut the distribution if it cannot turn this situation around, but the strong bond market so far this year may help it accomplish exactly that.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the BlackRock Corporate High Yield Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of April 11, 2023 (the most recent date for which data is currently available), the fund had a net asset value of $9.46 per share but the shares currently trade for $8.86 a piece. This gives the fund's shares a 6.34% discount to the net asset value at the current price. This is not nearly as attractive as the 7.72% discount that the shares have averaged over the past month, but it is also not a terrible price to pay. It may be a good idea to watch the shares for a few days to see if a better price is presented, but honestly, as long as the shares are purchased at a discount, it is probably fine.

Conclusion

In conclusion, the BlackRock Corporate High Yield Fund, Inc. is an interesting fund that can be used to generate income. The fund has a very well-diversified portfolio of high-yield assets that should be insulated from most risks other than those related to interest rates. The biggest concern here is that the fund appears to be overdistributing and may be forced to cut the payout if it cannot reverse its losses soon. The BlackRock Corporate High Yield Fund, Inc. is trading at a discount, though, which means that the price may still be acceptable even if it does have to cut the payout. Overall, the BlackRock Corporate High Yield Fund, Inc. may be worth buying, particularly considering that the Federal Reserve probably will not raise rates much more, if at all.

For further details see:

HYT: A Worthwhile CEF, But May Have To Cut The Distribution