CA - i-80 Gold: When Top Mines In The Best Jurisdiction Are Not Enough

2023-12-13 00:42:01 ET

Summary

- i-80 Gold has mines in Nevada, the best global mining region, according to the Fraser Institute. The company is the state's second-largest holder of gold reserves.

- The company has a robust balance sheet at first glance. However, its liquidity is questionable. The interest payments significantly exceed the company's gross profit.

- IAUX valuation is too high, even at such a low price, compared to similar-sized gold miners - even profitable miners like Calibre and K92 trade at lower multiples.

- I prefer to invest in a profitable business in a questionable country instead of in a loser in a top jurisdiction. I give IAUX a hold rating.

Introduction

Last week, the price of gold broke out in a long-term resistance only to return later. Gold equities followed accordingly. Despite that, gold has delivered adequate gains YTD (10.6%). Gold miners, however, disappointed the investors. One of the worst-performing companies is i-80 Gold (IAUX).

The chart below compares IAUX with XAUUSD, Barrick Gold (GOLD), and VanEck Gold Miners ETF.

{kind=link}

IAUX has two producing mines and three projects in its pipeline. The company is Nevada's second largest gold reserves owner, next to the JV between Newmont ( NEM ) and GOLD. Its mines (open pit and underground) also have higher-than-average ore grades.

Financially, IAUX maintains an adequate balance sheet, however mediocre compared to mid-size miners. The company’s margins and returns are negative, resulting in negative investor sentiment and a steep share price decline. Despite the bottom price, IAUX is still overvalued compared to similar-sized gold miners. Share price started to form a bottom with inverted head and shoulders chart patterns. The latter offers an opportunity for speculative trade with close stop loss and top-risk reward. However, this is not enough to give a buy rating to IAUX. My verdict for now is a hold rating.

i-80 overview

IAUX is a medium size gold miner. The image below from the last corporate presentation shows IAUX's business at a glance.

{kind=link}

The company is the third largest gold producer in the US with 6.465 M oz Au and 104.3 M oz Ag Measured and Indicated resources. It plans to become the second-largest gold miner in the US. All IAUX assets are in Nevada. Fraser's annual survey declares Nevada is the leading mining jurisdiction globally.

Carlin and Battle Mountain Trend are among the world's most prolific gold mining regions, along with Abitibi in Canada and Witwatersrand in South Africa. IAUX is the second largest holder of gold resources after Nevada Gold Mines, a joint venture between GOLD and NEM.

IAUX has two producing mines: Ruby Hill and Lone Tree (refurbishment in progress). Besides that, the company developed three projects: Fad, Granite Peak, and McCoy Cove. All assets are 100% owned by IAUX.

{kind=link}

The company`s mines have top ore grades, among the best in Nevada for both open pit and underground mines. The table below compares the grades of North American underground and open-pit gold projects.

{kind=link}

The company`s Lone Tree open pit mine has a 1.77 g/t ore grade. Granite Creek underground has a 10.4 g/t ore grade.

The company shows impressive figures for resources, however, when we look at the reserves the situation is different. The graph below from GoldStock data shows IAUX resources and reserves.

{kind=link}

Reserves of 280 k oz gold do not match the company’s intentions to produce 400 k on AU per annum. The inferred resources have the lowest probability of converting into reserves and dominate the total reserve base. E

very project starts with inferred reserves and, following the Lasonde curve, converts them into M&I resources first, then P&P reserves, and eventually into mine output. To consider a midsize mining company investable, I like to see P&P reserves to be at least in the low teens as a percentage of the total resource base. IAUX is not such a case.

Company Financial

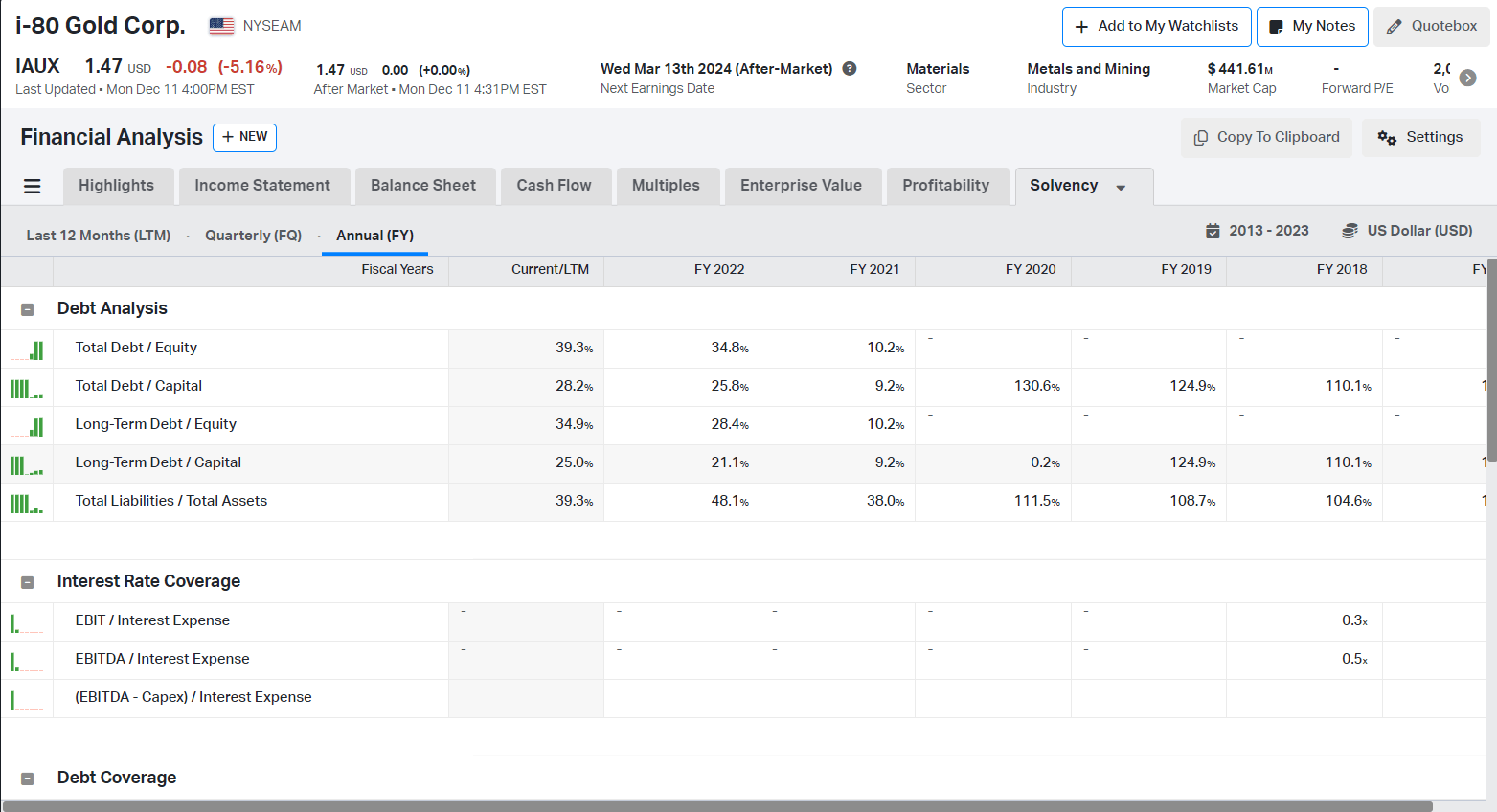

The higher gold price in recent years has improved gold miners' financial standing. Even the junior cleaned up their balance sheets. IAUX, however, has a poor balance sheet.

{kind=link}

Total Liabilities/Total Assets has dropped from 111% in 2020 to 39.3% in 3Q23. IAUX is solvent, but such a conclusion could not be drawn about the company`s liquidity.

The company`s debt structure looks as follows:

- Orion convertible loan: $45.75 million signed on Dec 31, 2021, with maturity on Dec 13, 2025, and fixed interest at 8%.

- Sprott convertible loan: $8.15 million signed on Dec 10, 2021, with maturity on Dec 9, 2025, and fixed interest at 8%.

- Convertible debentures: $47.19 million signed on Feb 22, 2023, with maturity 2027 and fixed interest at 8%.

The interest expenses per quarter have risen since the convertible debenture issue from $5.2 million in 4Q22 to $7.4 million in 3Q23. In 2025, the company must cover its obligations to Orion and Sprott.

Despite the average realized gold price of $1,895/oz for 3Q23 and $1650/oz AISC, the company had $(14.2) million in operational cash flow in 3Q23. IAUX's ability to serve its debts is questionable. What remains to create shareholder value?

IAUX has $37.7 million in cash and $176 million in debt. It is okay, but not the best, compared to similarly sized gold miners. The company`s money is enough to cover interest payments for five quarters. For reference, McEwen Mining ( MUX ) has $89 million cash and $41 million total debt; Caledonia Mining ( CMCL ) has $10.7 million cash and $21.2 million total. The best in the peer group are Calibre Mining ( CXBMF ) and K92 Mining (KNTNF), with $97 million cash/$20 million debt and $79.9 million cash/$6.6 million debt.

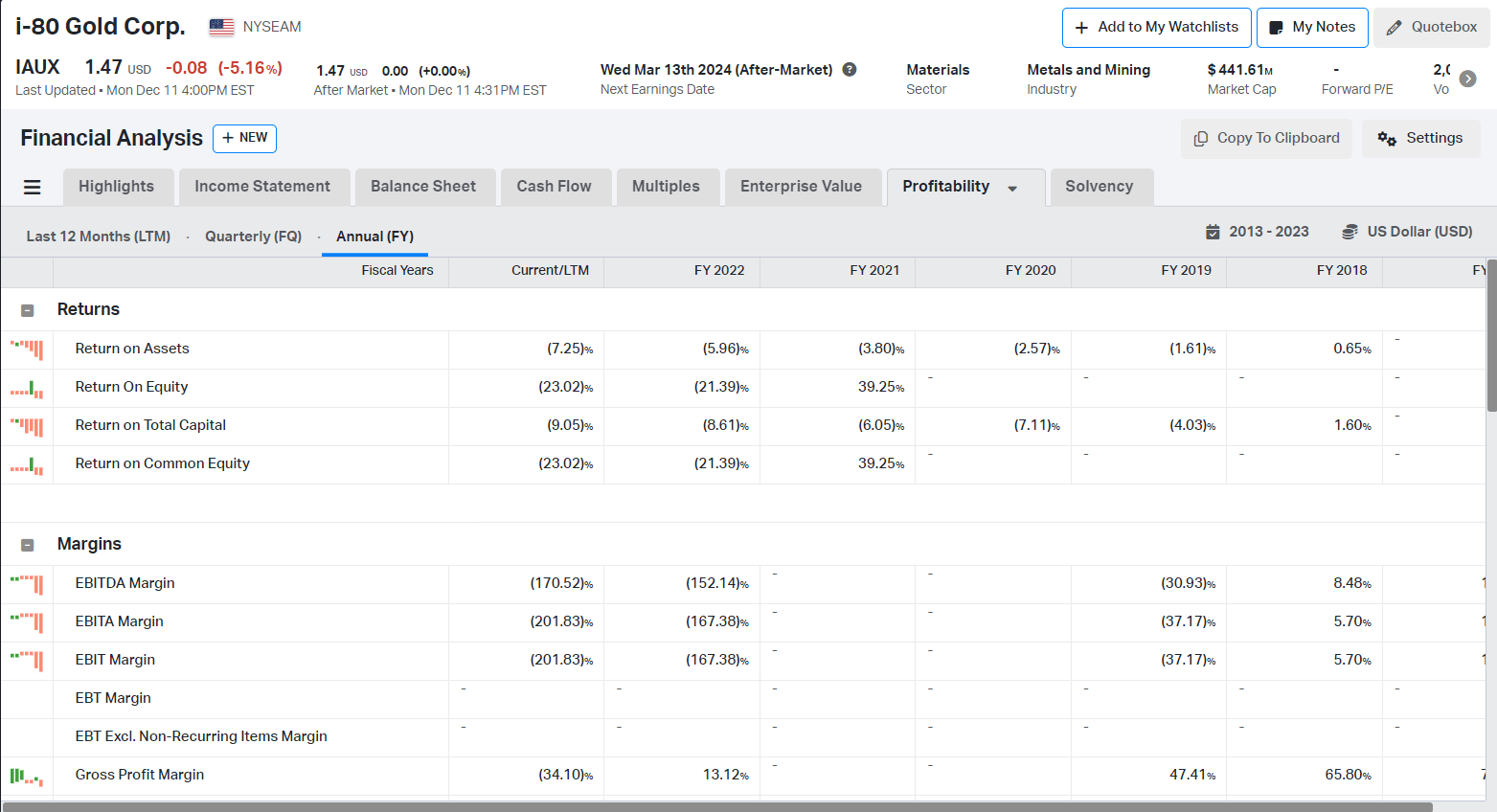

IAUX has not been profitable for the last few years, regardless of the higher gold price. The image below shows the company's profitability since 2018, the last year with positive margins and returns.

{kind=link}

As I mentioned, the gold miners are doing great, although not all. IAUX falls into that category. Let`s compare the company`s profitability to the same peer group:

- IAUX: (34)% Gross Margin, (170)% EBITDA Margin, (23)% ROE, and (9)% ROTC

- MUX: (58)% Gross Margin, (85)% EBITDA Margin, (36)% ROE, and (19)% ROTC

- CMCL: 41.2% Gross Margin, 24.7% EBITDA Margin, (2.8)% ROE, and 5.2% ROTC

- CXBMF: 43% Gross Margin, 40% EBITDA Margin, 18.4% ROE, and 17.2% ROTC

- KNTNF: 43.7% Gross Margin, 34.3% EBITDA Margin, 8.5% ROE, and 9.1% ROTC

IAUX and MUX have the lowest margins and returns in the group. On the other side of the spectrum are Calibre and K92, realizing impressive margins and returns.

Let’s dig deeper into the company`s income statement. The chart shows income figures over the last six quarters.

{kind=link}

The revenue has been erratic, though improved in the last two quarters. Gross profit has been negative, except in 3Q22, resulting in a 5.4 PE ratio.

In my opinion, IAUX managers are not the best capital allocators. The table below compares metal miners (predominantly gold) with a market cap of $200-$1000 million by Total Debt/Total Capital and ROTC.

{kind=link}

IAUX's total debt-to-capital ratio is low compared to other companies. However, its ROTC is negative. To have low leverage is not enough. The point is how efficiently the company uses it. IAUX is among the poor capital allocators in the group.

Valuation

Despite its low price, IAUX is still overvalued compared to its peers. For comparison:

- IAUX trades at 14.2 EV/Sales, - EV/EBITDA, and 1.0 Price/Book

- MUX trades at 2.91 EV/Sales, - EV/EBITDA, and 1.03 Price/Book

- CMCL trades at 2.06 EV/Sales, 8.32 EV/EBITDA, and 1.0 Price/Book

- CXBMF trades at 0.69 EV/Sales, 1.7 EV/EBITDA, and 0.80 Price/Book

- KNTNF trades at 5.01 EV/Sales, 14.59 EV/EBITDA, and 3.07 Price/Book

IAUX trades at higher multiples than profitable miners like Calibre and K92.

Now, let’s look at the company`s valuation differently. The chart below represents ROE ((LTM)) on the Y axis and EV/Sales ((LTM)) on the X axis for gold miners with a $200-$1000 market cap.

{kind=link}

To obtain negative ROE, I must pay 14.2 EV/Sales. Wise investing means to allocate your capital where it is best treated. To produce high multiples for negative returns is the opposite.

Price Action

IAUX price has been in a bear trend for the last 12 months. It seems now the price is forming a bottom.

{kind=link}

The blue line is significant resistance acting as a potential neckline of an inverted head and shoulders chart pattern. A trend reversal is possible if the price closes above the line. The SQN indicator shifts between bear quiet (red) and neutral (yellow). The neutral SQN regime and trend reversal patterns, such as invested head and shoulders, are an excellent combo for speculative (not investments) positions. A confirmed breakout above the neckline allows entry with close stop loss and excellent risk reward.

Risks

IAUX has assets only in Nevada, US, the best jurisdiction globally for the mining business. In other words, the country's risk is almost nonexistent. Financial risk, on the other hand, is the most pronounced. The company`s insufficient liquidity questioned IAUX's ability to cover its debts and run its operation smoothly. I am not saying the company will go bankrupt. My point is that IAUX is a poor capital allocator with low leverage but is an inefficient business, resulting in poor liquidity.

Last but not least is the gold price decline risk. Gold mining stocks lagged behind the gold price bull run. However, I expect the miners to “outperform” the gold spot in a steep bear trend, reaching new lows.

Investors Takeaway

To have assets in one of the best regions for gold mining is not enough. IAUX has excellent mines with high ore grades and a vast resource base. However, I am not impressed by the company's financials. At first glance, capital structure is adequate to guarantee a company`s solvency. Digging deeper, problems arise; IAUX has not been profitable for years, and interest expenses are a constant burden. The current cash position is enough to cover five quarters of interest payments. IAUX valuation is too high, even at such a low price, compared to similar-sized gold miners—even profitable miners like Calibre and K92 trade at lower multiples. The mines are in Nicaragua (Calibre) and Papua New Guinea (K92). Still, I prefer to invest in a profitable business in a questionable country instead of in a loser in a top jurisdiction. I give IAUX a hold rating.

For further details see:

i-80 Gold: When Top Mines In The Best Jurisdiction Are Not Enough