IIPR - I Am Buying These 9% Yielding REITs

Summary

- REITs now offer historically high dividend yields.

- Some yield nearly 10% following the crash of 2022.

- I highlight two such REITs that we are buying.

Real estate investment trusts ("REITs") ( VNQ ) have dropped by nearly 30% in 2022 even as most REITs have hiked their dividend. As a result, most REITs now offer high dividend yields:

REITs like Realty Income Corporation ( O ) that before offered a 3-4% yield are now priced at closer to a 4-5% yield... and those like EPR Properties ( EPR ) that offered a ~6% yield are now priced at an 8-9% dividend yield.

The name of our marketplace service here on Seeking Alpha is " High Yield Landlord, " so we are quite familiar with the high-yield segment of the REIT sector.

We think that real estate should be an income-driven investment first and foremost. We are NOT happy with a 2-3% dividend yield. We target a sustainable and growing 5-8% dividend yield to generate high income while we wait for long-term appreciation.

We like to call this the “ Landlord ” approach to REIT investing because we buy REITs as if we were buying rental properties. We look for high and sustainable income and always try to get a good deal. Money is made at the time of the purchase by buying below fair value. We then patiently hold these undervalued REITs, earn high income, and wait for long-term appreciation.

In what follows, we will highlight two such high-yielding opportunities that we are buying at the moment:

Uniti Group Inc. ( UNIT )

UNIT is an infrastructure REIT that's been the source of a lot of controversies over the past years.

Recently, it announced that it was going to offer $300 million in convertible notes and that caused its share price to drop by 16%:

YCHARTS

It appears that investors saw the word "convertible" and quickly assumed that they were going to get diluted. The size of the offering could dilute investors by up to 20% if the notes are converted to common equity at some point in the future.

But what the market appears to have missed is that this conversion is at the company's election, not at the investor's election. If the management wanted or needed to raise equity, it would have done so straightaway, and it would have likely done it earlier.

They issued these notes in order to refinance debt that's maturing in 2024, and it seems to me that they added the conversion option just in case things get tough to have the option to access equity.

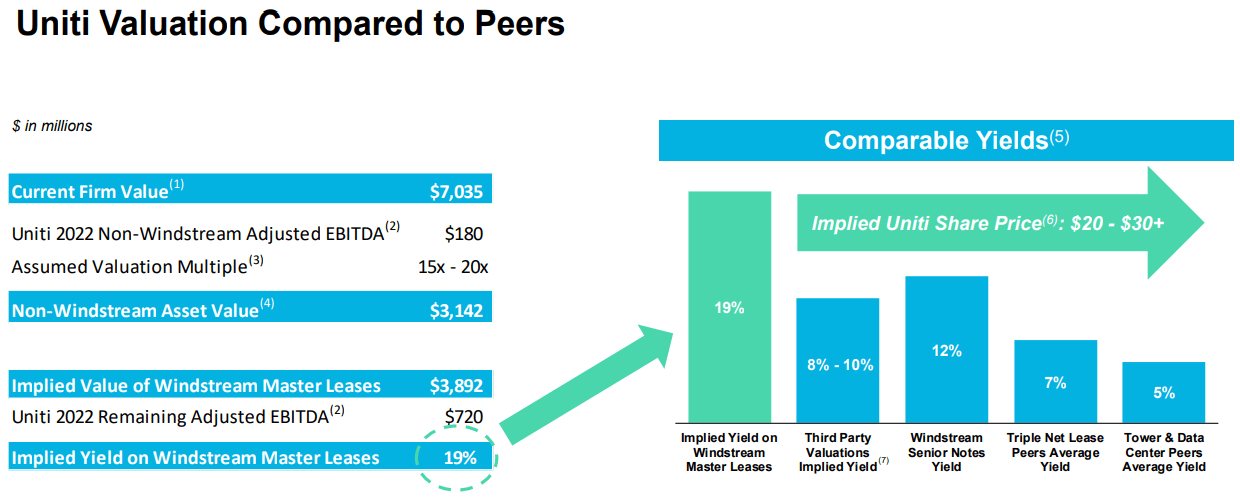

But the management has repeatedly explained over the years that their equity is discounted, and they even claimed that $15 per share would undervalue the company when it was rumored that another player had approached them to make a buyout at that valuation. Even today, they have a slide in their investor presentation that claims that they are worth $20-30 per share:

{kind=link}

So it seems unlikely to me that they would choose to convert the notes into common equity at a small fraction of that unless they really had to.

It seems likelier to me that they simply added it there to have the option, but their plan apparently is to eventually refinance this at lower rates once inflationary pressures cool down and interest rates return to lower levels.

Besides, UNIT is not about 20%. It is a potential multi-bagger with a speculative element because of the dispute with its largest tenant. Even if it got diluted by 20%, which we do not expect at this time, the long-term thesis would not be broken given how heavily discounted it is.

We are currently working on an updated investment thesis, but in short, we continue to think that UNIT's fiber assets are heavily undervalued by the market and that the upside will eventually be unlocked when the company is either bought out or when the dispute with its biggest tenant is resolved.

It is a messy situation and it will take time to be resolved, but UNIT's assets are in high and growing demand, they cannot be replaced, and they are, therefore, very valuable to the communities they serve. The replacement cost would likely be a multiple of its current share price and it is only rising further with the high inflation.

So, I don't buy into the argument that these assets aren't highly valuable... (more on this coming soon).

But even if its biggest tenant, Windstream, managed to get its way and the rent is cut significantly, we would still have 7 years of high cash flow ahead of us before the lease expires in 2030. This cash flow has been contractually agreed and it will keep rising according to the contractual escalations.

This is a significant risk mitigator because UNIT is currently priced at a 29% AFFO yield, which essentially means that you get earn your equity back in about three years.

It also means that UNIT has 7 years to keep diversifying its business and grow other revenue sources. The consensus view of analysts is that UNIT will manage to grow its AFFO per share quite significantly by then, and this should also compensate for any loss in Windstream revenue when the lease expires in 2030:

{kind=link}

This cash flow is largely recession-resistant (essential fiber infrastructure) and UNIT retains most of it to reinvest in growth and deleveraging (the payout ratio is only 35%).

So that provides some downside protection and it also leaves UNIT plenty of time with Windstream to hopefully find a mutually beneficial solution. After all, Windstream is highly reliant on UNIT as well and can't operate its business without access to its assets.

Is UNIT risky?

It sure is.

But priced at a small fraction of its net asset value, and having so much cash flow already under contract until 2030, I like the risk-to-reward a lot.

If we eventually get the positive resolution that we expect, UNIT could rapidly become a multi-bagger. And if the worst-case scenario plays out, we should earn significant cash flow by then, mitigating our losses.

The dividend yield is also 9.2% and it helps us to remain patient.

NewLake Capital Partners, Inc. ( NLCP )

NLCP is a small REIT that went public in 2021. The timing of its IPO was very unfortunate, as shortly after, the REIT market began to slide to crash:

And NLCP dropped a lot more than the average of the REIT sector because it is a small REIT that lacks a loyal following.

It also didn't help that it invests in cannabis cultivation facilities and the whole cannabis sector ( WEED ) is seen as a "growth" sector, and growth performed worse than average in 2022.

NewLake Capital Partners

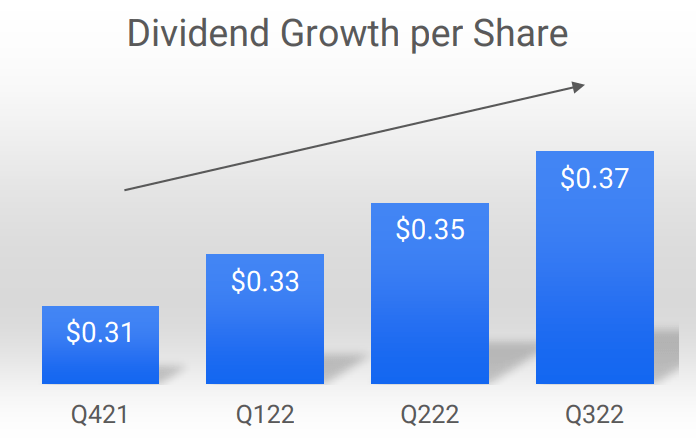

But despite the crash in its share price, NLCP has actually performed really well, and this has allowed it to hike its dividend in every quarter since going public:

{kind=link}

A lower share price... coupled with a materially higher dividend... has now resulted in a near-9% dividend yield.

Typically, REITs that are priced at such high dividend yields are experiencing some severe difficulties. They are either overleveraged, poorly managed, or own properties with declining rents.

But that isn't the case here.

NLCP has no debt at all.

The management has done everything right since going public.

And the company's cash flow keeps growing steadily as its rents are hiked each year by 2% on average, and it continues to acquire more assets at high spreads over its cost of capital. As I noted earlier, the company has not taken any debt so far, but in the future, it could start to use some to grow even faster. That alone should provide it with a "bank of future" that it still hasn't capitalized on.

What are the risks?

The tenants of the cannabis sector are more speculative than average and so occasional lease defaults are inevitable. So far, NLCP has not had any, but it will eventually. Its closest peer, Innovative Industrial Properties ( IIPR ) has recently had quite a few issues with its tenants. Fortunately, NLCP has done a good job of mitigating risks here. It focuses mainly on limited-license states, and its tenants are mostly larger companies like Curaleaf ( CURLF ) and Trulieve ( TCNNF ).

I think that as the market sentiment for cannabis stocks improves, NLCP will rerate at closer to 12-14x FFO, unlocking around 50% upside from here.

The management agrees that the stock is undervalued and they are buying back shares at the moment:

“While there continues to be attractive investment opportunities across the cannabis real estate sector, we think there is also compelling value in our stock. The authorization of a $10 million share repurchase program underscores our confidence in the quality of our portfolio, robust pipeline and growth opportunity of the cannabis industry for many years to come,” stated Anthony Coniglio, NewLake’s President and Chief Executive Officer (emphasis added).

While you wait for the upside, you earn a 9% dividend yield.

Bottom Line

High yield typically also means higher risk, and these two REITs are not exceptions to that. But today, there are a lot of such high-yielding REIT investment opportunities and so you can build a diversified portfolio to diversify risks and maximize returns.

For further details see:

I Am Buying These 9% Yielding REITs