CA - I Am Scooping 2 Oversold Fat Dividend Stocks

Summary

- You need income, so why not buy it at a discount when it's oversold?

- We examine two opportunities with high yields to see why they are oversold.

- Consider a portfolio that pays you, not a retirement focused on forced selling.

Co-produced with Treading Softly

I've always been fascinated by juxtaposition .

Juxtaposition is the placement of two distinct objects or situations, which is meant to highlight a contrast between them.

Americans have come to accept Black Friday as a major shopping day and a great time to snag large sales and discounted prices.

Yet, it's literally the day after Thanksgiving, a holiday to celebrate thankfulness for what you have.

The immediate contrast of thankfulness to avid shopping deals is a juxtaposition that Americans often overlook and the rest of the world sees.

Furthermore, growing up, I frequently heard the saying "from the other side of the railroad tracks." it was often used to denote less economically successful areas in town or people who lived there. The idea presented is that by simply crossing the railroad tracks, you'd exit a wealthier area and immediately hit an impoverished one.

So how does that play into investing? We are frequently presented with various contrasting viewpoints on investments. You have bulls and bears. For any investment, there are differing opinions. These differences of opinion are what make a market. For every stock transaction, there is a buyer and a seller. If everyone agreed on the value of a stock, there would never be a trade!

This dichotomy of opinions becomes a juxtaposition thanks to the hard work and creativity of Seeking Alpha. Here you can easily read a bullish opinion and a bearish opinion on the same stock. Frequently, you can just read the comments and find a variety of opinions.

This dichotomy can cause strong moves in the share price of an investment. Fear, mistrust, and greed can lead to share price drops that move investments into the strongly oversold category. We often see elevated yields from these fallen angels because yield is simply an expression of dividend payments compared to share price.

Let's look at two oversold opportunities sporting fat yields.

Pick #1: MPW - Yield 8.8%

Medical Properties Trust ( MPW ) saw a large sell-off last year and is now trading at its lowest price since 2016. There have been numerous headwinds to MPW's share price. Among those we can identify are:

- The general decline in medical REITs. The closest peer in terms of hospital ownership is Global Medical REIT ( GMRE ) which had a similarly bad year. REITs that invest in medical office buildings didn't exactly have a great year. REITs, in general, declined in price.

- MPW has above-average leverage at 6.6x Debt/EBITDA. This is a big improvement from the 7.85x at the end of 2021, but it is still over the target of 6.0x. With interest rates rising, REITs with higher debt levels have experienced more downside.

- MPW has material international exposure at 40% of assets. Including 20% in the UK. Non-U.S. REITs underperformed in 2022 as European economies were harder hit and the U.S. dollar's strength surged.

- The HCA acquisition of Steward hospitals in Utah was stopped by the FTC. As a result, MPW's exposure to Steward remained high. At this time, it is unclear whether there will be any major steps to reduce MPW's concentration to Steward.

- A very vocal short position has been using the above realities, combined with numerous unsubstantiated allegations, to cast doubt on MPW.

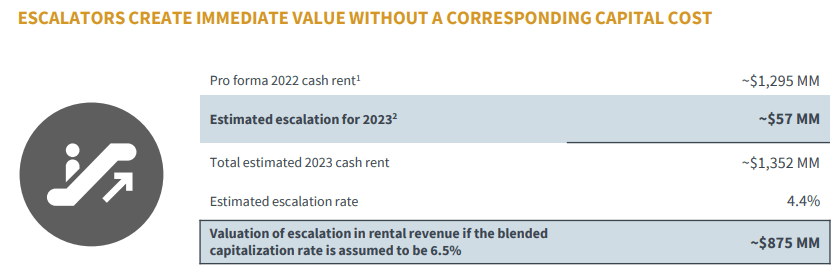

As a result, MPW's share price fell, even as the dividend was hiked 3.5% and AFFO (adjusted FFO) per share, MPW's best metric to represent dividend safety, increased by 7% year over year.

Looking at 2023, we can expect another good year as inflation escalators will go into effect, reflecting inflation from 2022. Source

{kind=link}

Additionally, MPW expects the repayment of its equity-secured loan to Springstone and three hospitals in Connecticut that are currently leased to Prospect. If these sales close, MPW's leverage will decline to 5.8x, under their target.

The greatest Black Swan risk to MPW would be a Steward bankruptcy since MPW does have significant exposure to Steward. However, Steward's rent coverage has been improving, and the significant cash needed to repay its $450 million in Medicare Advances has been dealt with. That is $45-$50 million/month that Steward no longer needs to pay (rent to MPW is less than $45 million/month). Additionally, contract labor expenses were a very large part of the strain that hospital systems felt across the country. While still elevated, they have improved significantly. The full strain of needing to hire temp staff at very high prices could take years to resolve as demand for nurses remains high but will be much lower in 2023 vs. 2022.

Yet even this Black Swan isn't necessarily a risk to MPW. One tenant of MPW, Pipeline, filed for bankruptcy in October. It has since sold the two problem hospitals and will finalize its bankruptcy early this year. Pipeline will continue to honor the leases on MPW-owned properties with a 30% rent deferral that will accumulate interest at 10%. Additionally, Pipeline will reimburse up to $1 million in MPW's legal costs caused by the bankruptcy. At the end of the day, MPW will receive more cash from Pipeline than they would have received if Pipeline had never filed for bankruptcy at all.

The reality is that Steward extended its ABL facility through December 2023, which was the theoretical catalyst for a bankruptcy filing. MPW management has been open about the factors that squeezed Steward's earnings and how those are improving. Steward's rent coverage has been improving and should continue to improve in 2023.

Meanwhile, MPW will get more rent from all of its tenants through its escalators, and it will continue to work on deleveraging. At the end of the day, it is earnings that matter, and MPW's earnings have been on a steady climb up. That isn't going to change.

Pick #2: AQNU - Yield 15%

Algonquin Power & Utilities Corp. Equity Units Due 06/15/2024 ( AQNU ) is a hybrid investment. It provides a fixed return until June 2024, at which point it converts to equity. Since this conversion is forced, the price of AQNU is highly influenced by the price of AQN common shares.

Algonquin Power & Utilities Corp ( AQN ) common crashed in November at Q3 earnings when management telegraphed that the long-term plan needs to be modified.

Looking ahead into 2023, broadly speaking, we expect pressure from increasing interest rates and broader macroeconomic conditions to impact our earnings. Although we are not providing 2023 guidance, our current view is that we will continue to drive growth in our regulated operating profit, albeit with some regulatory lag, while our renewables business is expected to be relatively flat as new program growth is tempered by lumpiness in our development pipeline. In light of the changing environment, we are reviewing our plans and targets for 2023 and beyond. We expect to provide further details at our upcoming Investor Day in early 2023.

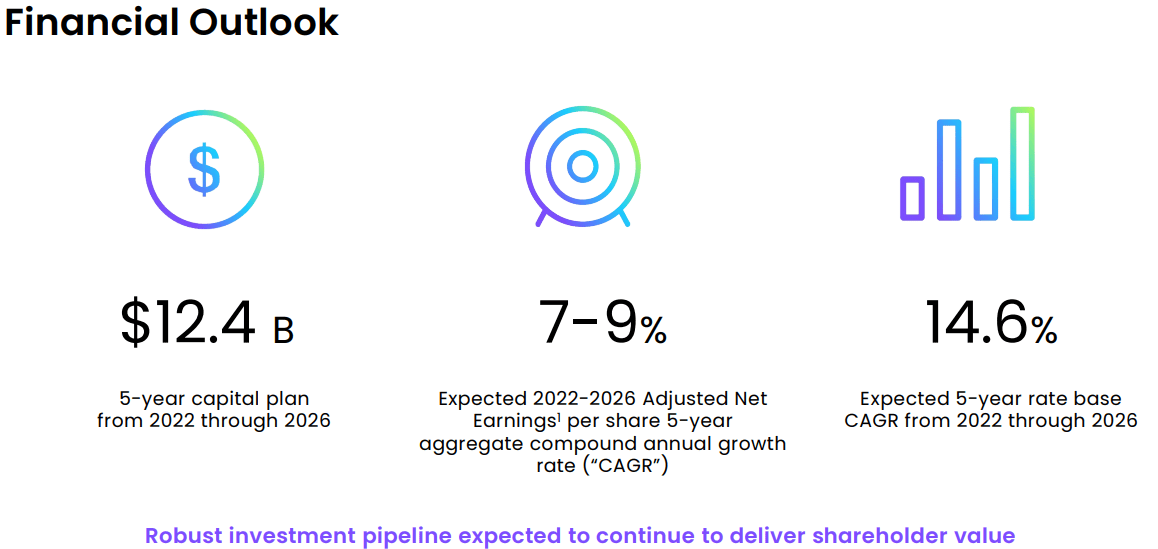

AQN had a very aggressive growth plan, which included spending $12.4 billion in cap-ex from 2022-2026. Source

{kind=link}

So what is management saying? The bottom line is that the cost of capital has risen substantially. The plan called for $5.2 billion in debt, and that is a lot more expensive today than it was when the plan was first envisioned. Therefore, the plan needed to be adjusted.

AQN provided insight into their plan on January 12th. It came with a renewed emphasis to complete their Kentucky Power acquisition, maintain a BBB credit rating, and conduct $1 billion in capital recycling (read: asset sales). The other major news item for AQN was a substantial cut to their common dividend, reducing it 42%.

We are actually pleased with the common dividend cut, as it also coincided with a stoppage of their DRIP program. AQN is stopping its routine issuance of new shares, and those who are set to DRIP with their brokerage will simply be buying the available shares on the market.

Here is a look at AQN's new plan, with retained cash exceeding the dividends by $500 million. Source

AQN January Investor Presentation

This will allow AQN to take on less net debt with their Kentucky acquisition and better position the company to resume growth in 2024.

Investors hate uncertainty, and AQN's share price was heavily oversold based on fears of the worst. Now we have the answer to what in the world is management thinking. AQN's common shares can now recover from the fears overhanging them, and likely the dividends can resume growth before AQNU's conversion in 2024.

AQNU remains our preferred way to invest in AQN because the dividend received from AQNU cannot be cut. We get a predictable amount until the units convert to equity in June 2024. The steps taken today in reducing the dividend are very unpopular with current holders, but ultimately it positions AQN to have higher earnings in 2024 than they would have had if they distributed all their cash. At the end of the day, earnings are what increase valuations.

AQN is a great utility company that was on the fast growth track, and management is stepping on the brakes when growth is no longer profitable. This should cause a revaluation - a utility that is growing more slowly should be cheaper than one growing quickly. However, at a price/earnings ratio of 10x, AQN is currently priced for zero growth and is much cheaper than peers. A revaluation was appropriate, but the current price has clearly gone too far.

Now that AQN has updated its plan, we expect that AQNs share price will stabilize and start a recovery.

We are happy to collect our oversized 15%+ yield while we wait for the market to settle.

{kind=link}

Conclusion

We believe that both MPW and AQN - and by extension AQNU - are oversold and ripe for a strong share price recovery. We also know that the dividend payments by MPW and AQNU are secure and will continue to pour into our coffers. The bulls and the bears on both sides will continue arguing. You can see the juxtaposition of those positions right here.

Personally, I'm going to grab a cup of coffee to sip while I watch the back and forth. I'm getting paid to wait for the squabbling to resolve itself.

Take a moment and consider your retirement funded by dividends vs. a retirement dependent on positive share price movements to generate the cash you need to pay your bills. How would your retirement have done in 2022 with the large drops in value the market experienced? If you were reliant on selling shares, could your retirement plan survive a drop of 30% as the market suffered?

For many, a 30% drop would be a death blow, especially in light of having endured 2020's drop. Selling shares in a down market causes a locked-in loss which compounds as you continually need to reduce your portfolio in the future for life's expenses.

Instead, embrace a viewpoint that allows the market to pay you for your retirement income. You don't need to sell a single share to survive, so a drop is not a fear-causing action, but an opportunity to grow your income more rapidly.

Thousands of High Dividend Opportunities members are enjoying that perspective, and millions of income investors do as well.

We'd love to have you join us from this vantage point.

For further details see:

I Am Scooping 2 Oversold Fat Dividend Stocks