NOC - I Just Made Northrop Grumman My Second-Largest Investment

2023-10-12 17:17:36 ET

Summary

- Northrop Grumman has seen a 12% increase in its share price in the past month, making it one of the best performers in my portfolio.

- The company's focus on high-tech capabilities and innovation sets it apart from its competitors in the defense industry.

- Northrop Grumman expects strong growth in areas like nuclear modernization and space programs, supported by a robust backlog and international contracts.

Introduction

I wasn't planning on writing another article so soon on Northrop Grumman Corporation ( NOC ) after I covered the company on September 10 in an article with the title Northrop Grumman: My Favorite High-Tech Investment.

Since then, shares have risen 12%, making it one of the best performers in my portfolio.

I'm not writing this article just to tell you how well NOC is doing. That would be a waste of everyone's time.

No, since early September, a lot has happened that requires coverage.

- The company presented at the annual Morgan Stanley Laguna Conference, which revealed a lot of relevant data and comments for long-term (dividend growth) investors.

- The conflict in Israel has added another complicated layer to an already complex and increasingly insecure global geopolitical picture.

- While budget uncertainties have pressured all major defense companies, NOC may be in the best position to benefit from targeted funding for next-gen technologies and services.

As a result, I added so aggressively to my position that NOC is now my second-largest investment.

- Four of my top five dividend growth investments are now defense contractors.

- My total aerospace & defense exposure is 26%.

While these numbers will change, as I'm planning new investments in non-defense industries, I have used the past few months to load up on investments that, I believe, will allow me to grow my dividend income and beat the market on a prolonged basis.

Northrop Grumman is one of these stocks.

As we have a lot of new developments to discuss, let's dive right in!

Outperformance Through Innovation

As I have mentioned in almost all of my defense-focused articles, I am not buying defense companies to benefit from war. The opposite is true, as I invest in defense companies with high-tech capabilities that keep people safe and prevent war in the first place.

One of the reasons why most defense analysts are so optimistic about the Ukraine war remaining contained is the fact that it's surrounded by NATO nations with capabilities that would make any attack from Russia too costly to even attempt.

This is an example I used in my prior article to show that " defense through innovation " beats " safety through combat ."

The US has an overwhelming advantage over Russian troops . This month, Joe Biden said he would request an additional $24 billion from Congress for Ukraine, “and other international needs related to the war”, said Al Jazeera.

Biden and his team have said the US will help Ukraine “as long as it takes” to remove Russia.

For all his threats, said Tisdall, “ Putin fears Russia-Nato conflict ”. For him, it would be “political and military suicide”.

Additionally, the other day, a defense insider told me that defense companies themselves prefer peacetime. While that may not sound logical, wartime is not beneficial for defense companies. In times of peace, it is much easier to hike prices and focus on key areas without being forced to research or produce certain products. It's also much easier for supply chains and margins.

Having said that, Northrop Grumman is a technology company.

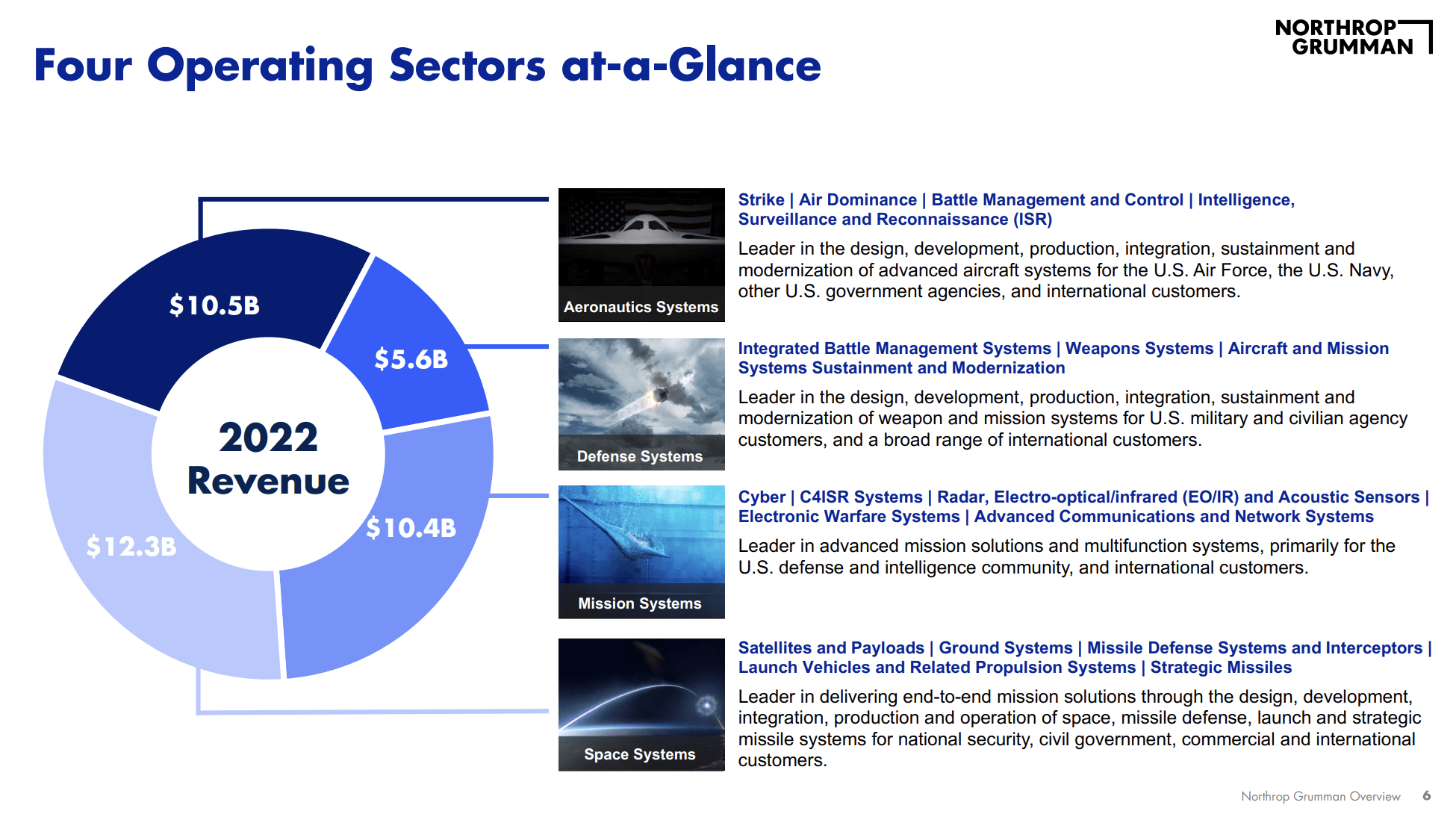

The company generates more than half of its money from Space Systems and Mission Systems. Just a quarter of its revenue last year came from Aeronautics Systems, which includes the next-generation bomber, B-21 Raider.

{kind=link}

Essentially, NOC is involved in everything ranging from missile defense and commercial space operations to multi-domain warfare support, F-35 fuselage production, Advanced AI, supercomputers, and related services.

While innovation is hard to quantify, I sometimes joke that NOC is more innovative than all FANG stocks combined.

{kind=link}

These capabilities have set NOC apart from its peers.

Over the past ten years, NOC shares have returned 470%, beating the S&P 500 by a huge margin. NOC has also beaten all of its major defense-focused peers. However, it needs to be said that both L3Harris Technologies ( LHX ) and RTX ( RTX ) went through major mergers over the past four years.

A big part of its returns were buybacks and dividends.

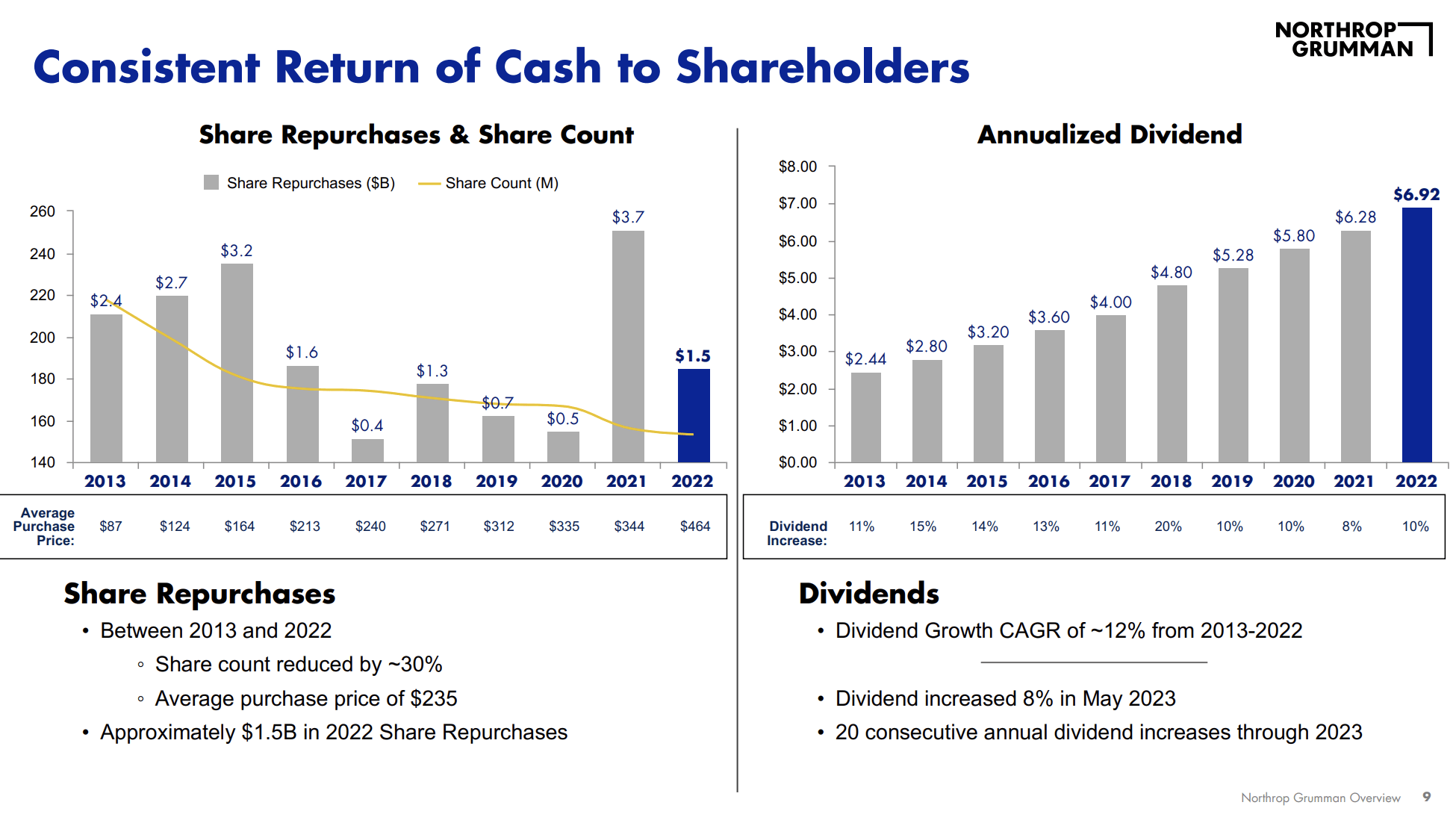

- Since 2013, NOC has bought back close to a third of its shares, spending more than $1.5 billion on buybacks in 2022 alone.

- Its dividend has been compounded at an annual rate of 12% during this period. For what it's worth, NOC is less than five years away from becoming a dividend aristocrat.

{kind=link}

With everything said in this article so far, now is a great point to dive into what the company said during last month's Morgan Stanley Laguna Conference , which was attended by Northrop CEO Kathy Warden.

While some companies often reveal just a bit about their future during these conferences, Northrop pretty much discussed any topic that I have covered in the past, which is one reason why I'm writing this article.

For example, the company highlighted its strong sales growth of 7% year-to-date, with a projected 5-6% sales growth for the year at the midpoint of its guide.

Warden also emphasized the company's strategy to expand margins, aiming for a 20% compound annual growth in free cash flow over the next two years through 2025 and doubling the free cash flow by 2028. Double!

- This year, NOC is expected to generate $2.0 billion in free cash flow. This translates to an FCF yield of 2.8% using its $72 billion market cap. This is also one of the reasons why so many people believe that NOC is overvalued. After all, a 2.8% 2023E FCF yield is nothing to write home about.

- If the company doubles its free cash flow to $4 billion by 2028 (I believe it will be higher), it will have a 5.6% free cash flow yield.

As one can imagine, this substantial free cash flow expansion creates opportunities for capital deployment and value creation for shareholders.

Northrop mentioned a focus on returning 100% of free cash flow to investors this year, including share repurchases and dividend increases.

I have little doubt that most of its free cash flow in the years ahead will also end up in investors' pockets (both directly via dividends and indirectly via buybacks).

It also helps that the company has a net leverage ratio of less than 2x EBITDA and a BBB+ credit rating, meaning it does not need to prioritize its balance sheet over shareholder returns.

The Need For NOC Services Is Growing

During the conference, Kathy Warden expressed confidence in Northrop Grumman's growth prospects.

Despite the 3% cap in the Department of Defense ("DoD") budget, NOC foresees strong growth, especially in areas like nuclear modernization and space programs.

International opportunities, especially in Europe, are expected to further strengthen growth. The strong backlog and international contracts provide a robust foundation for Northrop Grumman's positive outlook. The company went into this year with a $79 billion backlog.

NOC also expects that the continuing resolution will end up going into next year, meaning it expects higher approved defense spending.

Based on this context, last week, Israel was attacked, leading to a further complication of global geopolitics. Western nations are now involved in two conflicts: the one in Ukraine and one in Israel, which could launch a ground offensive into Gaza soon.

We're seeing exactly what I was afraid of a while ago. While I didn't predict that these exact things would happen, we're seeing increasing tensions between nations supporting Russia and China and NATO allies. While it needs to be seen how bad things get in the Middle East, we're not at a point where defense spending has to be a priority, even if it's just to modernize existing equipment.

UBS seemed to agree when it upgraded NOC shares this week.

As reported by Seeking Alpha (emphasis added):

"The global prioritization of national security has altered and will accelerate defense spending ,” Gavin Parsons, analyst at UBS, said in a report. “Bipartisan support for defense persists despite U.S. austerity, though political gridlock could cause near-term stock volatility.

UBS recommends Northrop ( NOC ) because its role in “high-priority” programs for the U.S. Department of Defense, such as the B-21 Raider stealth bomber and the Ground-Based Strategic Deterrent (GBSD), an intercontinental ballistic missile (ICBM) system that will replace the Minuteman III .

“Military spending is rising due to the Russian invasion of Ukraine and Western geopolitical friction with China,” according to UBS. “That said, the political outlook remains volatile near-term, with austerity discussion in D.C., the potential for a shutdown, and an upcoming election year and debt ceiling debate.”

As we can see, the bank highlighted some points that I have been focusing on as well, including NOC's advanced products and services and the need to increase targeted defense funding.

The bank also showed that it expects NOC to outperform its peers in terms of growth. While the stock is trading at the highest multiple among its peers, it is expected to erase that premium over the next four years.

Seeking Alpha

Furthermore, as part of risk management, the company is not bidding for the contract to build the next-generation air dominance program ("NGAD"), as it believes it is better suited to be a supplier. As I already own a company that generates a lot of money from a single project (Lockheed Martin's ( LMT ) F-35), I'm very happy with this decision.

Instead of focusing on the NGAD, Northrop Grumman used the aforementioned conference to express confidence in various opportunities within the aerospace and defense sector.

Warden highlighted their involvement in programs like F/A-XX and collaborative combat aircraft ("CCA") as potential growth areas.

The F/A-XX is going to be the successor of the F/A-18, which can often be found on aircraft carriers as the backbone of the Navy's air capabilities. Northrop is competing with Lockheed and Boeing ( BA ), which is building the current F/A-18 fighter.

They also noted the potential for growth and competitive advantage in autonomous aircraft, leveraging the company's expertise and experience in the field. While it needs to be seen how much funding emphasis autonomous defense products get, I believe this will turn into a cash cow for NOC over the next few decades.

Valuation

Given NOC's growth trajectory, there's no point in using the company's current valuation. After all, UBS data showed that the company is currently trading at a huge premium.

Using the company's expected 2028 free cash flow yield, the stock is trading at 17.9x free cash flow. This would bring the valuation back to the pre-pandemic normal.

Even beyond that, it is highly likely that NOC maintains high-single to low-mid-digit annual EBITDA and free cash flow growth.

The current consensus price target is $500, which is 6% above the current price. UBS gave the stock a $555 target, which is 17% above the current price.

I agree with that target and will add to my NOC position on potential corrections down the road.

Third-Quarter Outlook

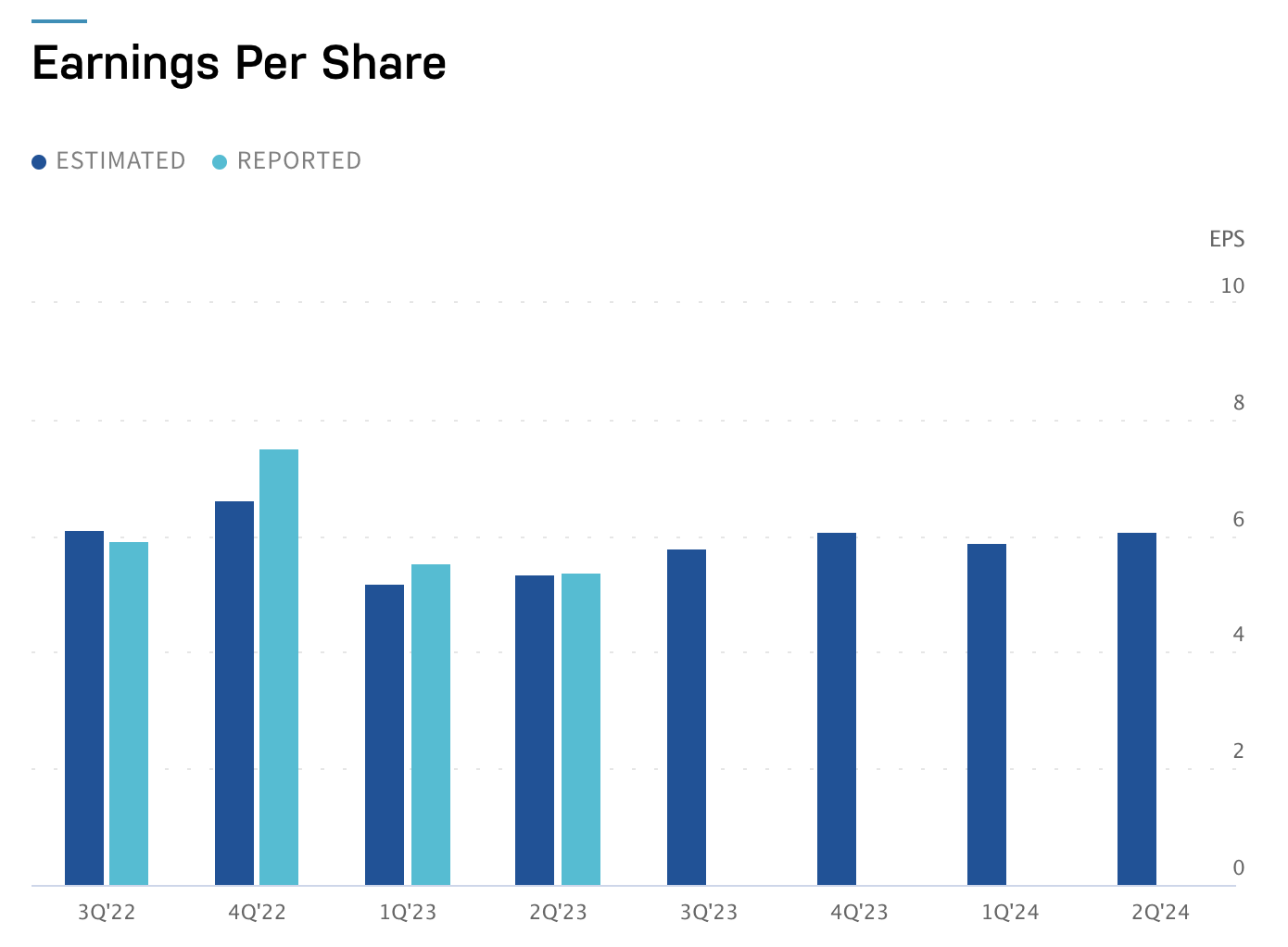

On October 26, the company is set to release its 3Q23 results. The market expects $5.75 in EPS. This is based on eight estimates. The company has gotten one downside revision and one upside revision over the past four weeks.

{kind=link}

Personally, I don't really care if the company slightly beats or misses this number. What I care about are the company's comments regarding the items listed below.

- Inflation pressure

- Supply chain bottlenecks

- Defense budget expectations

- Progress in its B-21 program

- Everything related to the above

Given that the market has priced in a lot of inflation headwinds since last year, I believe that if the company has positive comments regarding inflation and orders, we could see a stock price rally after earnings.

Takeaway

My substantial investment in NOC, making it my second-largest portfolio holding, reflects my confidence in the company's future.

NOC's innovative approach to defense, focusing on high-tech capabilities, positions it as a vital player in ensuring NATO safety and security.

Their emphasis on innovation, spanning from missile defense to AI and space systems, sets them apart from their competitors.

The company's strong financial performance, marked by consistent buybacks and a robust dividend growth strategy, underpins my confidence in its long-term potential.

With a positive outlook for growth, especially in crucial sectors like nuclear modernization and space programs, NOC remains a key component of my investment strategy in the defense industry.

Despite its current valuation premium, I see NOC as a promising investment with potential for substantial returns in the future.

For further details see:

I Just Made Northrop Grumman My Second-Largest Investment