CA - Iamgold: We Have A Second Elephant In The Room

2023-03-17 03:31:50 ET

Summary

- The Cote mine construction has proven challenging for IAMGOLD, a well-documented elephant in any room discussing the gold miner.

- Various funding initiatives seemed to have tamed this elephant last year.

- A second elephant has just entered the room.

IAMGOLD ( IAG ) released Q4 and full-year 2022 results on February 16 and interim CEO Ms Maryse Bélanger set the scene in her opening statement to the earnings call by pointing to annual record production at the Essakane mine in Burkina Faso, an asset she rightly called the "backbone" of IAMGOLD's current production. And indeed, annual gold output of 432Koz is a veritable achievement, especially under the problematic (and deteriorating) security conditions in the Northern parts of the country where this mine is located.

And just like that, in one short introductory paragraph, we arrive straight at the second elephant mentioned in the title.

Essakane

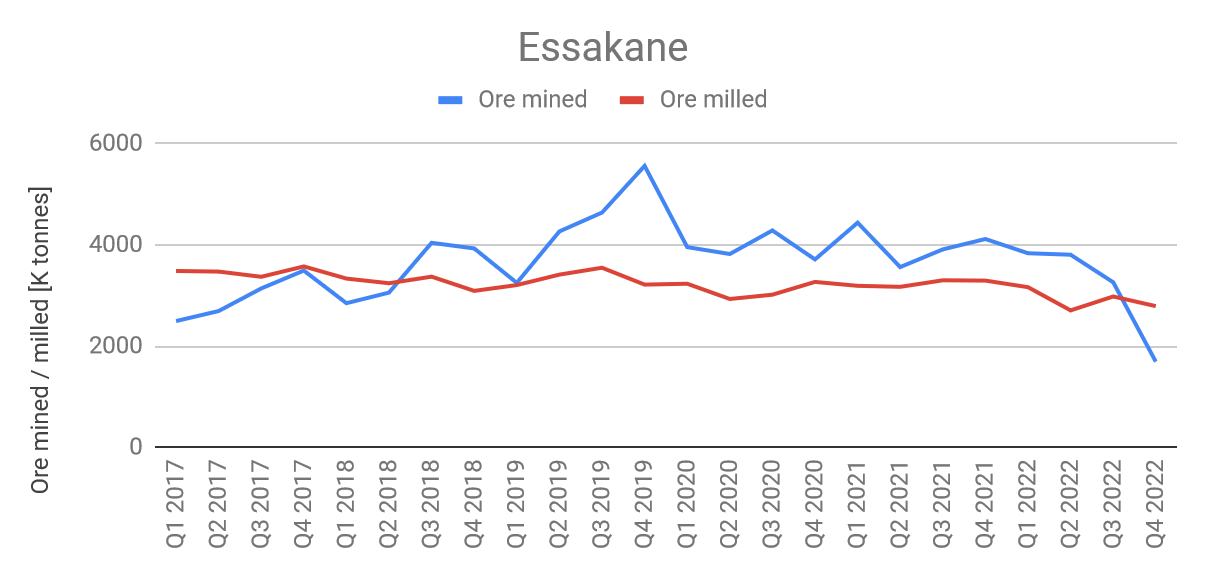

The chart below shows quarterly numbers for ore mined (blue line) and ore milled (red line). Ore mining declined by a significant margin in Q4, and production was propped up by processing stockpiled material.

Essakane ore balance. (Company filings and author's database.)

{kind=link}

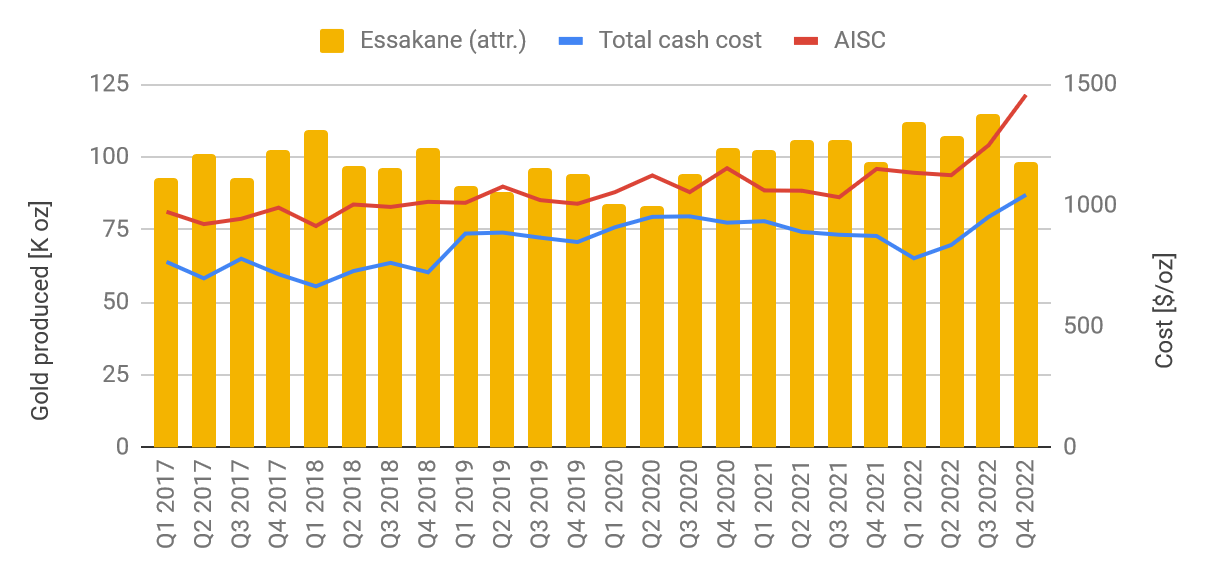

Gold output could be maintained thanks to sufficient stockpiles, but costs increased to unprecedented levels. Cash costs (blue line below) and all-in sustaining costs (red line below) printed $1,043/oz and $1,456/oz respectively for the quarter, both unwanted quarterly records for this mine.

Essakane production & costs (Company filings and author's database.)

{kind=link}

Ms Bélanger's explained the shortfall of ore mined during her earnings call remarks as follows (emphasis added).

Ore mining declined in the fourth quarter as operations prioritized stripping activities to secure access for the next phases of mining later this year, while also managing impacts from supply chain constraints related to the security environment in the country . On that, we note that the security situation in Burkina Faso continued to deteriorate in 2022 with governmental instability and terrorist-related incidents occurring in the country and the region.

We have mentioned security concerns for Essakane in our previous commentary on IAMGOLD, most recently in this article . Late 2022 was the first time these security concerns actually manifested themselves, and had a visible impact on the operations of this mine. Apparently, deliveries of consumables were hampered by terrorist activities in the area. Meanwhile, France has decided to pull most military personnel out of the country, and Russia's Wagner mercenaries seem poised to take their place. These are highly undesirable developments for a Canadian gold miner, and should be monitored very closely by IAMGOLD investors.

The company is guiding for a ~20% production decline at Essakane in 2023 (using the mid-point of the guided range). Lower grades and higher stripping requirements will cause this decline; notably, continued challenges stemming from the mentioned security situation are not factored into this guidance. All this will result in higher costs, and indeed, all-in-sustaining cost guidance of $1,625-1,700/oz doesn't bode well for free cash flow generation in 2023.

Furthermore, there seems to be a change of plan concerning the low-grade stockpiles at Essakane. The original mine plan involved heap-leaching this ore after the conclusion of open-pit mining activities in 2026; however, it now seems that IAMGOLD is toying with the idea of processing the stockpiled ore through the mill instead. An updated technical report will provide the necessary color later in the year.

In any case, Essakane seems to be entering the twilight years of its mine life, and its function as a backbone within IAMGOLD's portfolio will come to an end sooner rather than later. And this begs the question: will the Cote mine be ready to fill the void; and perhaps more pertinent: is IAMGOLD still positioned to benefit from the Cote mine once it comes online?

Q4 Results

The Westwood mine in Quebec is the only other remaining operating mine in IAMGOLD's portfolio following the sale of the Rosebel mine. Operations at Westwood were impacted by seismic events in 2020 and this mine has been running at a loss ever since. Cash costs in excess of $2,000/oz and all-in-sustaining costs well in excess of $2,500/oz have been the norm at Westwood, and difficult decisions are complicated by the fact that this mine is the only unionized mine that we are aware of in the Abitibi region.

Westwood production & costs (Company filings and author's database.)

{kind=link}

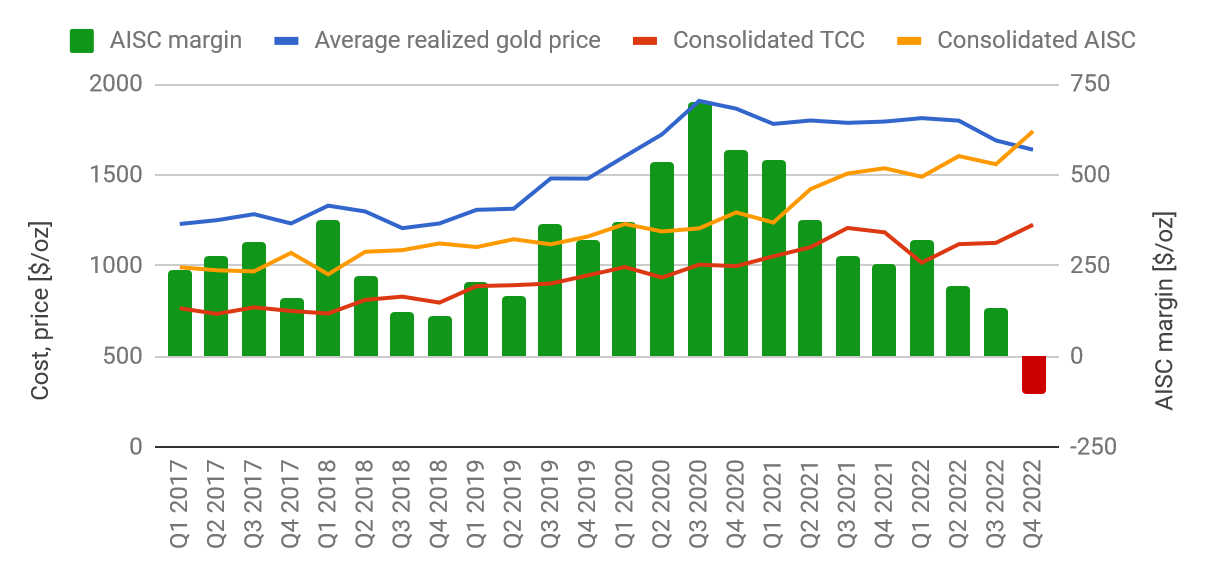

On a consolidated basis for the two continuing operations, we note that all-in-sustaining costs have exceeded the prevailing gold price in Q4, turning margins negative for the quarter as indicated by the red bar in the chart below.

Consolidated margins (Company filings and author's database.)

{kind=link}

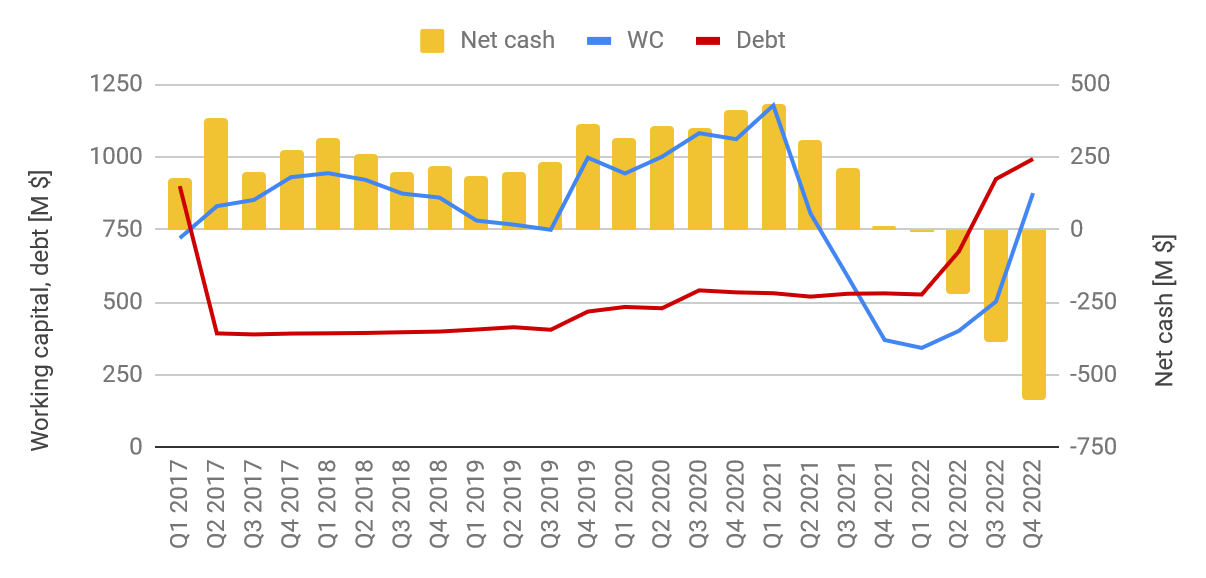

We called the balance sheet a train wreck of worrisome proportions in our last piece on IAMGOLD, and we certainly don't see much improvement on this front just yet, as illustrated by the latest data points in the chart below (noting that the dust from last year's asset sales still needs to settle). As of the end of 2022 net cash continued to plummet as free cash flow from continuing operations proved elusive in Q4, and $185.6M in cash calls to fund the ongoing Cote mine construction had to be met.

And this finally leads to the perennial first elephant mentioned in the title.

{kind=link}

The Cote Project

IAMGOLD will be required to fund ~$500M of construction costs in 2023, even after selling an additional 10% stake to its JV partner Sumitomo. Plus, IAMGOLD will need to fund $58M for equipment leases, and it will need to fund its share of working capital requirements. The first gold pour is planned for the start of 2024, followed by ramping up of production. We estimate that the grand total for IAMGOLD's contributions will most likely add up to close to $1B by the time Cote turns cash flow positive.

Ms Bélanger had the following to say during the Q&A session of the earnings call when prompted about IAMGOLD's liquidity:

If we take our cash position that we had at the end of the year of $407M and we add in the additional cash proceeds on the close of Rosebel that was included in our assets held for sale, that gets us to $450M. And then if you add in the net proceeds from the others, the other two transactions, it would get us to approximately $1B.

So judging from the above, we'd argue that IAMGOLD has sufficient liquidity to complete mine construction and ramp up production at the Cote mine. Only just, though. And only if no more costly mishaps or delays get in the way, and that's an optimistic bet to place judging from the history of this capital project so far.

Summary & Investment Thesis

Forget typical valuation metrics when it comes to putting a value on IAMGOLD. This company is all about the odds of finally bringing the company's stake in the Cote mine to account. If construction and ramp-up at the Cote mine can be accomplished without further cost overruns or delays, then investors who buy at the present share price of $2.35 stand to gain significantly (we would put forth a price target of $4.50 in this case); and if more costly issues crop up at the Cote construction site, then the equity value may well go to Zero given the immense debt load on this balance sheet.

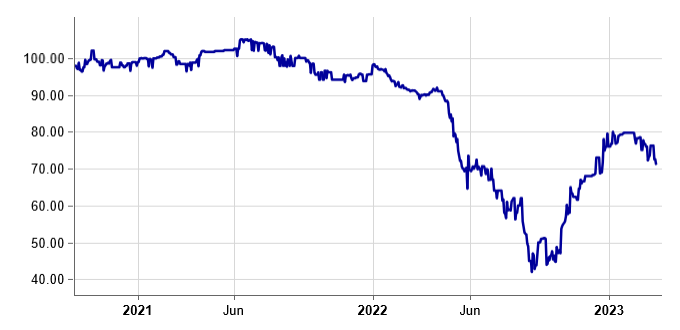

The market has been optimistic of late, but this sentiment looks as if it might be rolling over again judging from the price chart for the company's Senior Unsecured Notes shown below, probably a better gauge for market sentiment than the share price. This apparent change in sentiment to the downside may well be connected to the mentioned clouds gathering over the Essakane mine.

{kind=link}

Given the history of the Cote project so far, and given the mounting question marks with regards to the Essakane mine, we are not going anywhere near IAMGOLD's common shares at this point. The unsecured notes are slightly more interesting, however. The 5.75% coupon computes to an 8.2% yield at the current discounted price; and capital gains amount to ~40% over 2.5 years until maturity. These unsecured notes are ranked above the common equity, but below the $500M credit facility ($455M drawn at the end of 2022). However, no matter which way one looks at IAMGOLD, this is a speculative investment at the current point in time more akin to investing in a highly vulnerable development company than investing in an established gold producer.

For further details see:

Iamgold: We Have A Second Elephant In The Room