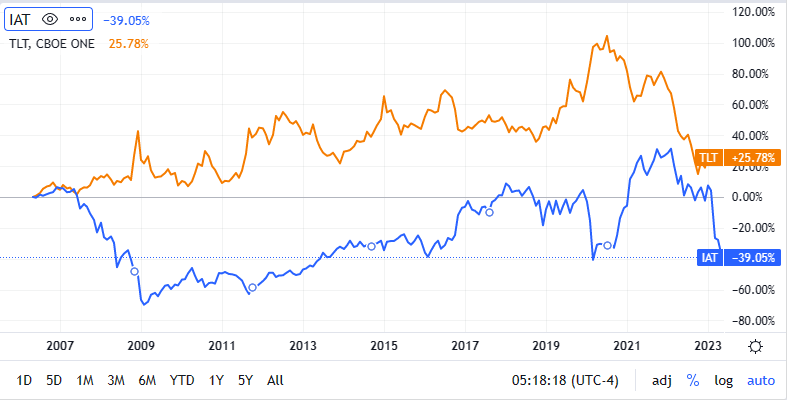

TLT - IAT: Buy The Dip And Using TLT As A Hedge

2023-05-07 19:00:00 ET

Summary

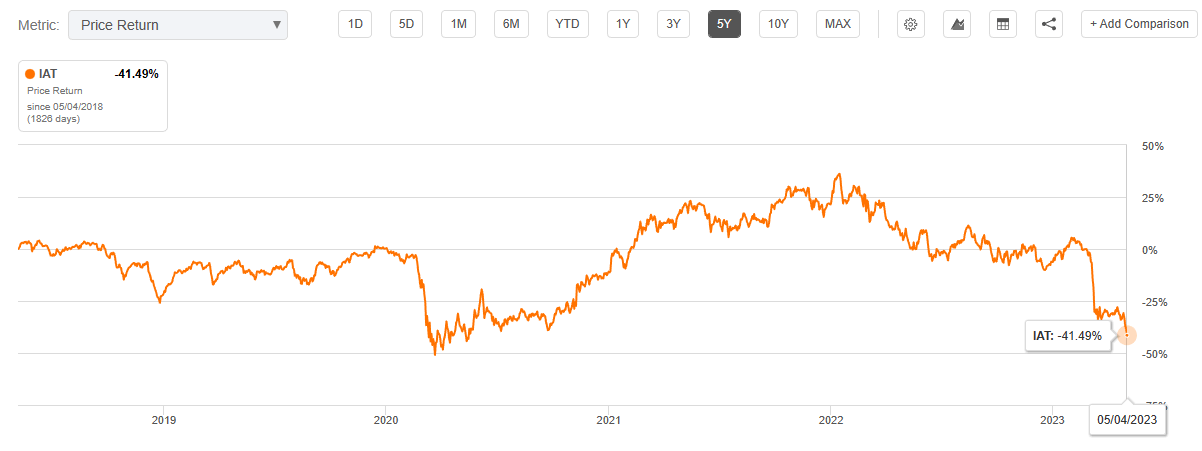

- With nearly a 40% YTD decline, IAT is now nearing its Covid-19 low, presenting an attractive risk and reward for long-term investors.

- By hedging IAT with TLT, investors can not only reduce volatility but also earn a yield of 4.2% while waiting for a potential rebound.

- Rolling hedges with put options over the long term can be expensive as there is no way to predict when IAT will drop further.

Investment Strategy

The recent failures of two large regional banks in mid-March have left investors feeling pessimistic about the near-term outlook for the sector. This week, the rout in bank stocks deepened, with PacWest ( PACW ) and Western Alliance ( WAL ) both sinking almost 50% on Thursday after the sale of First Republic Bank to JPMorgan Chase & Co ( JPM ) last weekend. As a result, the regional banks ETF ( IAT ) has tanked 13% in just five days and is approaching a 40% drawdown on a year-to-date basis. While some regional banks have seen deposit inflows in recent weeks, many investors remain concerned about potential credit risks in the US regional banking system. It may take some time for the sector to recover.

{kind=link}

Despite these challenges, I believe that now is a good time to gradually build up regional bank positions through ETFs like IAT to avoid idiosyncratic risks, as the ETF is getting closer to the 2020 pandemic low, which I consider to be a strong resistance level from a technical standpoint. While some investors, including Bill Ackman , may argue that US regional Banking system is still at risk, I think the portfolio will be less volatile by implementing hedging strategies such as the 20 Plus Year Treasury Bond ETF ( TLT ). I chose TLT because its long duration and high convexity make it a more effective hedging instrument (but less effective in a high inflation backdrop), as the bond-stock correlation went back to the negative territory in early March. Moreover, IAT provides an annualized yield of 4.2% while TLT offers an annual coupon rate of 2.44% . Therefore, I believe the risk and reward is high in the long term.

{kind=link}

Low Efficacy of Options-Based Hedging

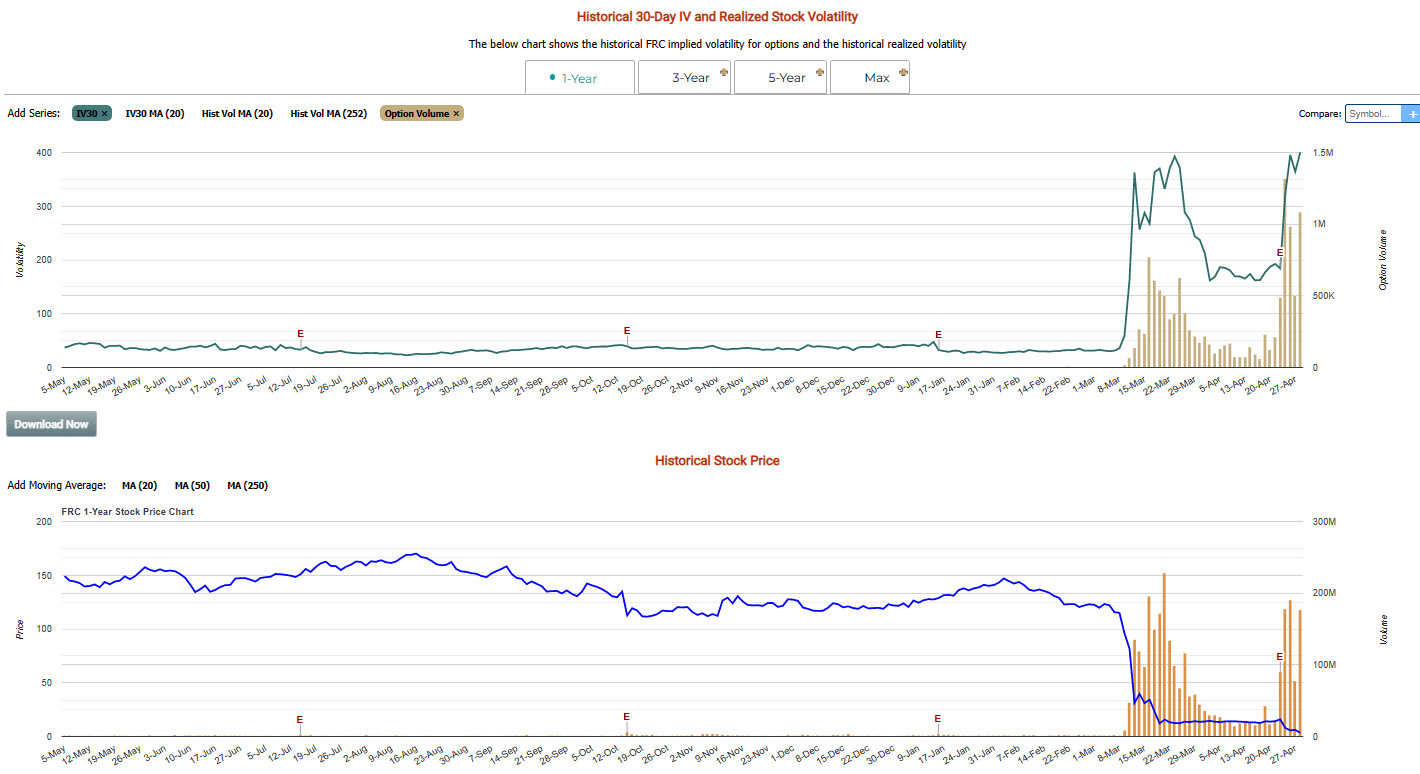

Some investors may argue to hedge IAT though put options. It's very important to remember that buying options is similar to buying insurance, as the buyer has a higher probability of losing money. You may get a jackpot sometimes, but rolling hedges through options for a long term can be very costly. Additionally, when the underlying stock such as IAT is volatile, the premium for options tends to be spiking, requiring buyers to pay more than during less volatile times. For example, as the price of First Republic Bank dropped 50% within one day, the implied volatility (IV) increased sharply, making it more expensive than usual to buy options (both calls and puts).

{kind=link}

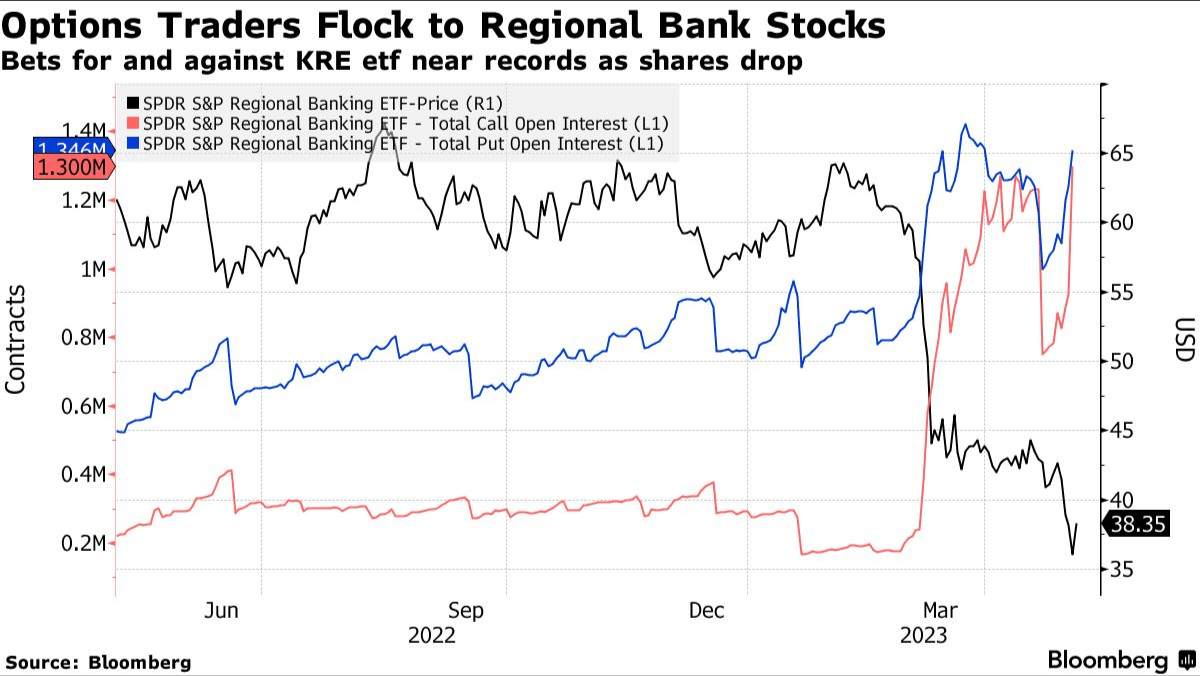

The logic is that when investors want to hedge IAT, they tend to buy more put options than call options, leading to excess demand for put options. Option traders then meet this demand by selling puts, causing the relative price of these options to increase and raising the IV. In other words, if IAT put options are bought at a high IV, its value will drop as the regional bank sector becomes less volatile and the IV declines, although the price of underlying IAT remains unchanged. Lastly, while selling IAT put options can provide higher premium when the IV is spiking, it's not an efficient method to hedge your underlying.

{kind=link}

R.I.P.: SBNY, SIVB, FRC

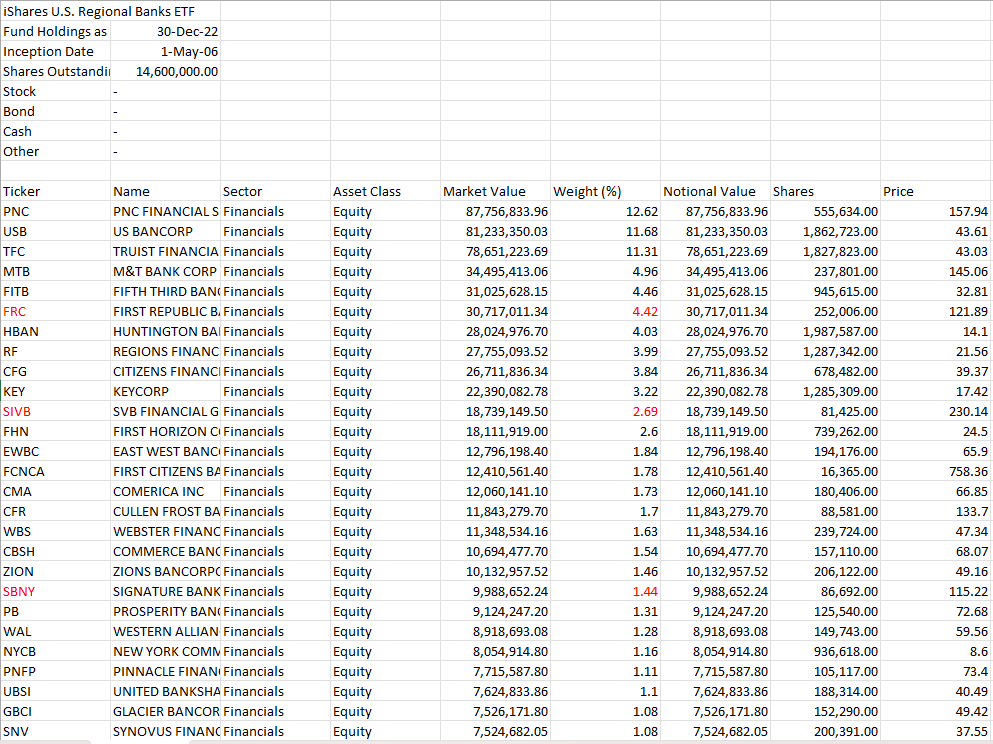

First of all, I want to clarify that IAT won't recover to its previous high without additional rallies from other constituents. As shown in the chart, on December 30, 2022, the total weight of SBNY, SIVB, and FRC combined was 8.55%, and these three names won't recover at all since they were completely wiped out due to the recent banking turmoil. In the following paragraphs, I'll discuss four possible scenarios.

iShares U.S. Regional Banks ETF

{kind=link}

Soft Landing (Less likely)

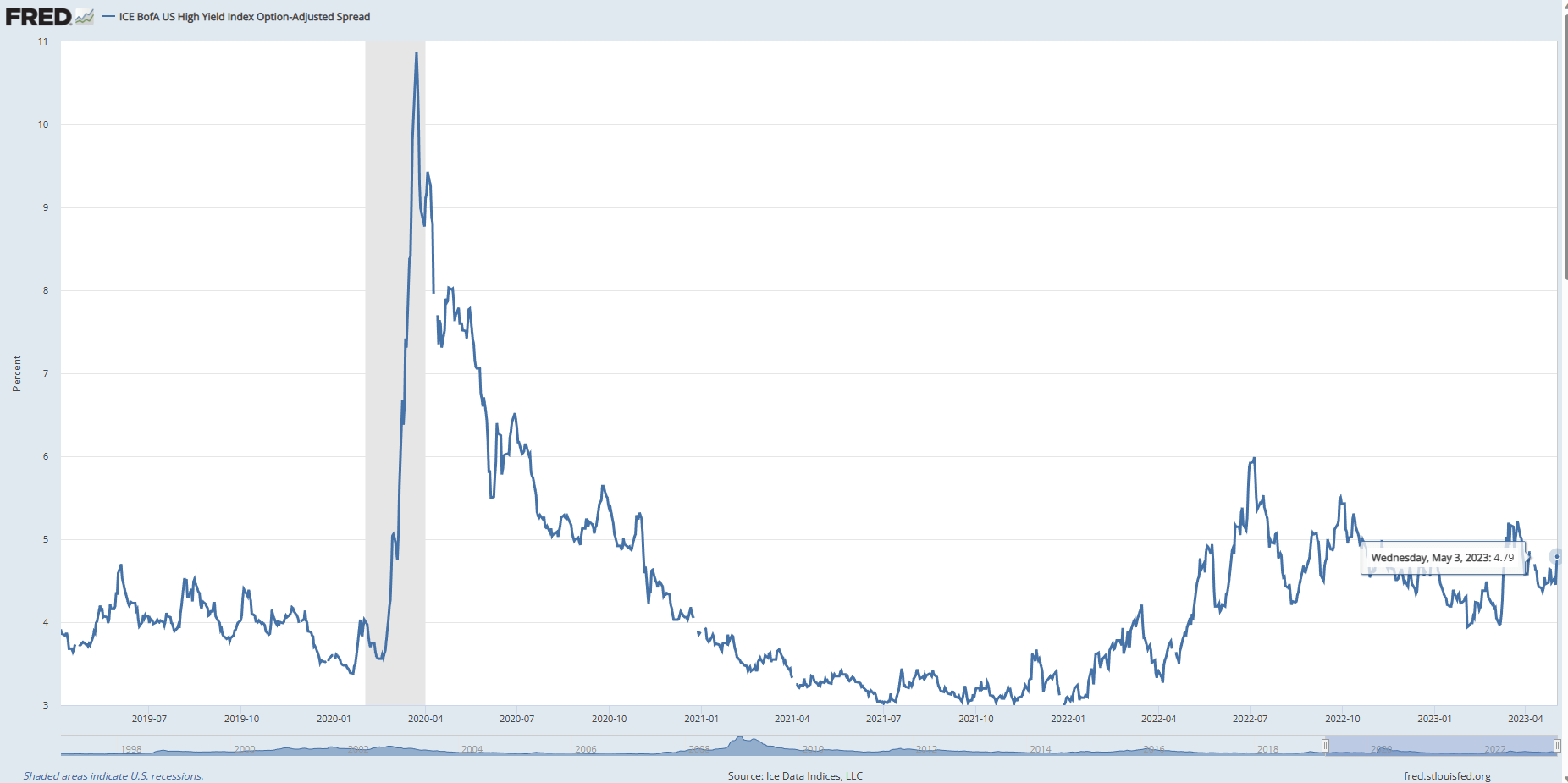

If the Fed engineers a soft landing, the credit risk may not materialize, and IAT could see a significant rebound soon. I believe that if the US economy remains resilient, with low unemployment and robust consumption, the Fed may be hesitant to cut interest rates despite reports of job cuts in the news. If inflation gradually decreases, it could create a "goldilocks" scenario for the stock market. Regional banks could recover earlier than anticipated in this environment. However, even in this scenario, the hedging position TLT may still generate a positive return through coupon payments, despite the Fed's current "high for longer" attitude towards interest rates. While the April Core CPI still remains 5.6% YoY, I believe the current federal fund rate of 5% is not sustainable if the "sticky" service inflation continues to decelerate in the coming months. As we can see from the chart below, the current high yield spread is not at a distressed level, which means the credit risk still remains relatively low, despite the recent banking turmoil.

Ice Data Indices, LLC, ICE BofA US High Yield Index Option-Adjusted Spread

{kind=link}

Mild Recession Without a Credit Crisis (Likely)

In this scenario, I believe IAT's 40% drawdown has largely been priced in, even though the recovery period may take longer than expected. The financial industry is traditionally a cyclical sector that underperforms the S&P 500 during past recessions but outperforms during early recovery stages. On the other hand, TLT could generate a positive return based on its price actions alone when the economy is slowing down, as the market expects the Fed to cut interest rates to stimulate the economy. However, the magnitude of the price actions may be weaker in a high inflation environment, particularly as the current inflation rate of 5% is still higher than the target rate of 2%. As a result, the Fed may not cut interest rates quickly. Currently, the Fed Fund Futures are priced for three 25 basis point cuts by the end of 2023, indicating a concern for economic slowdown in 2H 2023 and a possible recession.

{kind=link}

Despite a longer recovery period for IAT in this scenario, investors still can collect dividend and coupon payments from both long positions. Normally, investors need long and short positions to create a hedge, and dividends or interests from short positions have to be paid out by investors. However, in this case, investors can generate a decent return while waiting for IAT to recover.

Hard Landing Scenario with a Credit Crisis (Likely)

{kind=link}

If the US falls into a severe recession due to banking failures, I believe IAT would continue to fall as credit spread widens, leading to financial instability and higher unemployment rates. The Fed would be forced to cut interest rates faster to stimulate the economy, but the recovery period for IAT would take longer than other scenarios. Therefore, investors should focus on hedging positions through TLT, which historically saw significant rallies, particularly in low inflation environments. In this scenario, the magnitude of the hedging position will be stronger. During both 2008 GFC and 2020 Covid-19 era, TLT posted strong rallies of up to 28% and 21% respectively within just a few months.

Furthermore, some investors may consider a tactical allocation by gradually selling TLT and buying more IAT during the recession, if their risk tolerance is high. This strategy could provide a more attractive return, as the market turmoil begins to muddle through. However, this could potentially lead to more significant losses in the portfolio. As a result, it's essential to balance the risk and reward profile when implementing this strategy.

"Paul Volcker" Scenario (Unlikely)

If the U.S. experiences an unexpected rebound in inflation, which I consider less likely, the Fed may hike interest rates above the current rate of 5%. Jerome Powell doesn't want to repeat what Paul Volcker did in the 70s, when he slammed the brakes on the economy by raising interest rates to 20% and triggered a more severe recession. Long-duration bonds like TLT would suffer the most in this scenario, and both TLT and IAT may trigger a sell-off at the same time. The gain may only come from interest and coupon payments from the ETFs. In theory, the higher the interest rate the Fed raises, the higher the probability that the U.S. will experience a hard landing. As a result, TLT will regain its hedging ability during a severe recession.

{kind=link}

Conclusion

In summary, there are the possible scenarios that could play out for IAT and TLT. If the U.S. experiences a soft landing and the credit risk does not materialize, IAT is likely to have a significant rebound, while TLT can still generate a positive return through coupon payments. If the U.S. slips into a severe recession triggered by banking failures, IAT may continue to fall, but TLT can rally strongly as a hedge against the market turmoil. However, if the U.S. experiences high inflation and the Fed continues to raise interest rates, both IAT and TLT may sell off. In all scenarios, a tactical allocation strategy, such as gradually selling TLT and buying more IAT or other assets during a severe recession, can be attractive to investors who have higher risk tolerance.

For further details see:

IAT: Buy The Dip, And Using TLT As A Hedge