SPY - Icahn Enterprises: Shares Are Not The Best Yield Play

2023-05-04 11:18:55 ET

Summary

- Icahn Enterprises crashed as the short seller report surfaced.

- The yield has gone to an incredible 25%.

- Can the legend Carl Icahn maintain this and take on Hindenburg?

- Let's find out.

The market has a way of turning tables on the best of us. The recent short report by Hindenburg research put billionaire investor Carl Icahn's company, Icahn Enterprises ( IEP ) on the defensive. The stock has lost more than a third of its value within two days.

We look at the allegations and suggest the best plays here.

The Report

There are several points made in the short report and we go over the ones that have the most bearing on the outlook from here.

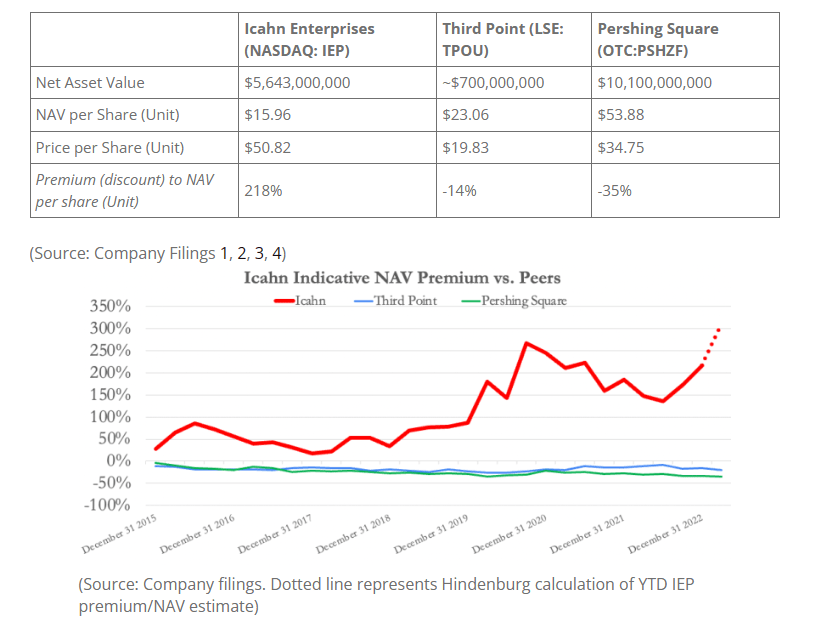

1) Overvaluation relative to peer funds

Hindenburg states that IEP is overvalued relative to closed-end funds and other funds managed by top investors. Both Third Point and Pershing Square are cited as examples.

{kind=link}

Hindenburg Research.

This one is the easiest to opine on. There are no "allegations" here and this is simply a matter of fact. Here, we're using IEP's provided NAV as a starting point so there can be little doubt that this is true. One extension of accepting this is that one gets to see how much the return over a total timeframe depends on ending valuation. For example the 10-year return profiles in March 2000 and March 2009 look radically different for all companies. The former was boosted as ending valuations were out of touch with reality and the latter was decimated for the same reason (but in the opposite direction).

So when you see a chart like this, showing IEP has outperformed the market, you need to get your thinking cap out.

What would this return profile be if IEP was trading at its own stated NAV? That's right folks, it would have underperformed the S&P 500 ( SPY ).

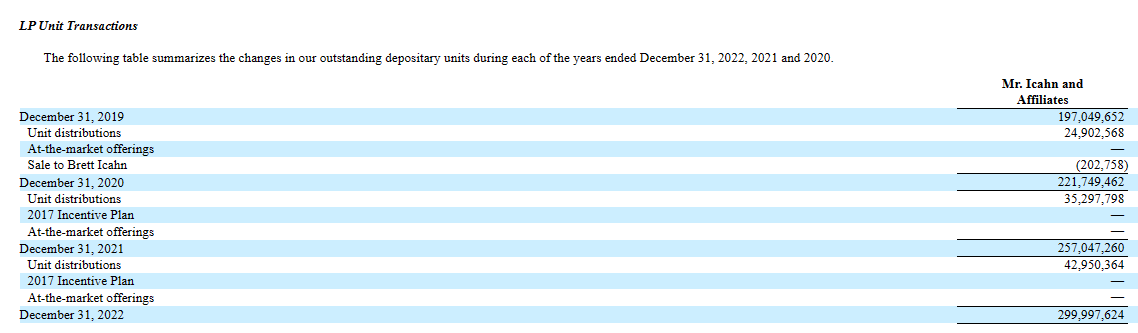

2) Selling Units To Fund Distributions

The allegation here is that the fund has not earned the mammoth distribution being paid (25% yield currently) and has to sell units to fund that. On the surface this apparently looks accurate as well. The fund's own reported NAV has dropped by 50% over the last six years and the distributions have continued unabated. There are two nuances here though.

The first being that Carl Icahn is taking his entire distribution in the form of new units.

{kind=link}

IEP 10-K

Now, obviously he, more than anyone else, can see the big gap in valuation as stated by calculated NAV and the price of the shares/units. Yet, he takes the distribution in "overvalued" units. If nothing else, that does show some alignment of interest. This is not some small gesture either. Carl Icahn and his affiliates own about 85% of the units. So the cash distributions are only required on a small portion of the total.

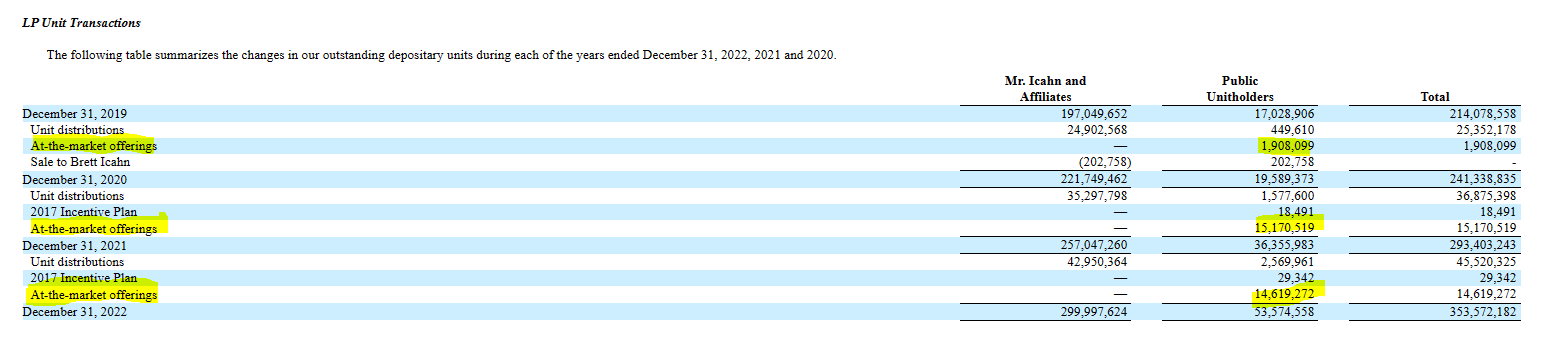

The second point is that why would anyone not make offerings for a company trading at this valuation?

Cornerstone Strategic Value Fund ( CLM ) and Cornerstone Total Return Fund ( CRF ), two funds with really mediocre long-term track records , use their high premium to regularly make secondary offerings. A related point here that both funds trade at about a 20% premium to NAV. So these at the market offerings are pretty small, in our opinion.

{kind=link}

IEP 10-K

If we had a fund with this type of NAV premium we would be hitting the bid every single day. Remember that each unit sold like this also raises NAV of the remaining shares. So this is a good thing.

3) Overvaluing private companies owned by IEP

Here the allegations are that multiple private companies owned by IEP are inflated in value. If this is the first you're hearing about private investments being marked to fantasy, then you need to pay more attention. Here's one we viewed with skepticism.

While Ontario Teachers’ public equities declined 12.5% and bonds dropped 5.9%, its infrastructure holdings gained 18.7% and private equity rose by 6.1% . As of Dec. 31, private equity assets totaled $58.3 billion of the plan’s $244.1-billion total, compared to $21.9 billion in public equities.

Source: Investment Executive (emphasis ours)

Private equity outperforming by almost 20% during 2022? OK, would you like a bridge we have to sell? Here's one better and this is comparing Blackstone's ( BX ) BREIT outperforming key benchmarks. The article quoted below misses the entire irony of the fund limiting redemptions while posting an apparent alpha of 35%.

That seems strange at first glance, given that public REITs are having a terrible year. Through October, the MSCI US REIT index was down 25.42%, and the Vanguard Real Estate ETF ( VNQ ) was down 26.78%. That makes publicly-traded REITs worse performers than the S&P 500 index, which was down 17.7% for the year through October. The average fund in Morningstar’s Real Estate category has posted a 26.2% loss over that time, with only four of the 63 funds in the peer losing less than 20%, and they include one fund that invests in energy master limited partnerships and two real estate income funds.

Morningstar

Source: Morningstar Direct / Data through October 31

Source: City Wire

So private and level 3 investments have always been a black box and we view all of them with great skepticism. See this article for a more detailed example.

How To Play: Don't Go Yield Chasing

We repeatedly warn investors to not chase yield. The key reason is that even one or two of these blow-ups in a portfolio of 30 stocks can cost you that extra yield on the entire portfolio. So if you want to buy IEP, do so because you believe in the investment strategy and do so if you can live with the dividend going to zero tomorrow. Would you want to buy a closed end fund at a 100% premium to NAV if it had no dividends? We didn't think so either.

If we had to generate a "yield" here we would first wait for the bleeding to stop. You generally don't want to get in front of a stampede of selling. The S&P 500 also looks overbought and held together by a few stocks. So a turn down there could add to IEP's woes. Once we some stability, we could venture to sell the $17.50 cash secured puts. We think the current premium will expand in the days ahead and you could get as high as $3.00 for these options.

Author's App

The key point here is that this is a far higher yield on the stock and also allows you to get long near the current NAV. The second choice is also intriguing. The near-term bonds just traded near 9% yields to maturity.

{kind=link}

Interactive Brokers

Obviously if you believe in the long-term future of the common shares, you cannot doubt the ability of the company to pay these off. The 2024's have only $1.1 billion in total and this amount is exceeded by the cash on hand nearly two fold.

IEP 10-K

This point in the capital structure also is likely to benefit from a dividend cut or elimination.

Verdict

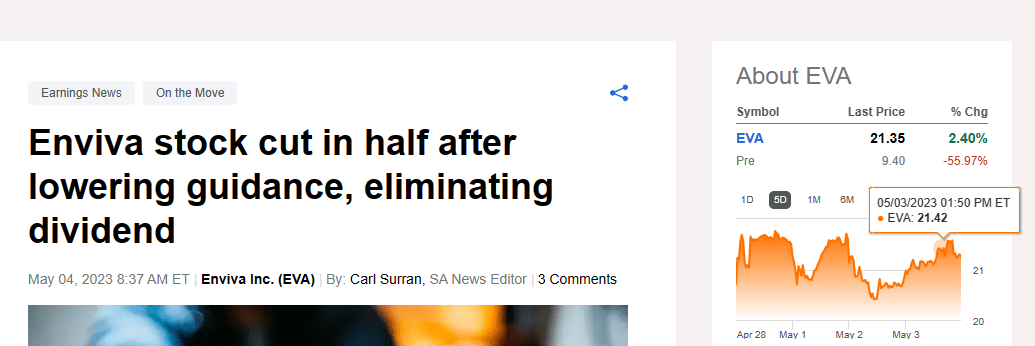

Shorting is a complicated skillset and can be tough in up trending markets. Regardless of the ultimate impact on the stock, investors should investigate each claim without emotion. Don't dismiss any claims based on thinking they are "talking their book." Everyone talks their book and this comes from the long and the short side. Investors made the same fourth grader counterarguments to Blue Orca's short report six months back on Enviva Inc. ( EVA ). They're waking up this morning to the following setup.

{kind=link}

Seeking Alpha

The reverse can be true as well. The short report on Farmland Partners Inc. ( FPI ) turned out to be a bunch of garbage ultimately.

Our verdict here is that there's no denying that IEP is overvalued relative to its NAV and it will be next to impossible to fund distributions if the premium evaporates. This is especially true with looming debt maturities. So we think the price moves lower just based on that. The allegations on the other aspects are relatively weak and don't impact the outcome. Even by their own numbers the $5.6 billion NAV is inflated by 22%. The market cap difference between the price and NAV, is far greater than this alleged inflated markup. Investors bullish on Carl Icahn should read and understand the report and then consider one of the two choices presented above. A direct purchase in the common shares is just too risky, even after the drop.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Icahn Enterprises: Shares Are Not The Best Yield Play