ICFI - ICF International: Interesting Bet On U.S. Defense Spending Expansion

2023-09-29 13:38:05 ET

Summary

- ICF International is a consulting firm that offers services to government and commercial clients in various sectors.

- The company achieved significant revenue growth in Q2, with contributions from government and commercial energy clients.

- Despite a decline in gross margin, ICF expects improvement in the second half of 2023 and has positive financial guidance for the year.

- Based on my calculations, ICFI's upside potential by the end of FY2024 should be around 28% vs. the current market price thanks to undervaluation and end market tailwinds.

The Company

ICF International, Inc. ( ICFI ) is a $2.26-billion market cap consulting firm that offers a wide range of services to both government and commercial clients in the United States and globally. They conduct research on various policy, industry, and behavioral issues, assess the impact of their work, and provide strategic guidance to help clients navigate challenges in society, business, markets, communication, and technology. The company also develops and implements policies, programs, and data management solutions, conducts surveys, and offers business intelligence services. Additionally, they specialize in customer experience optimization, IT system modernization, cybersecurity, and technology system development.

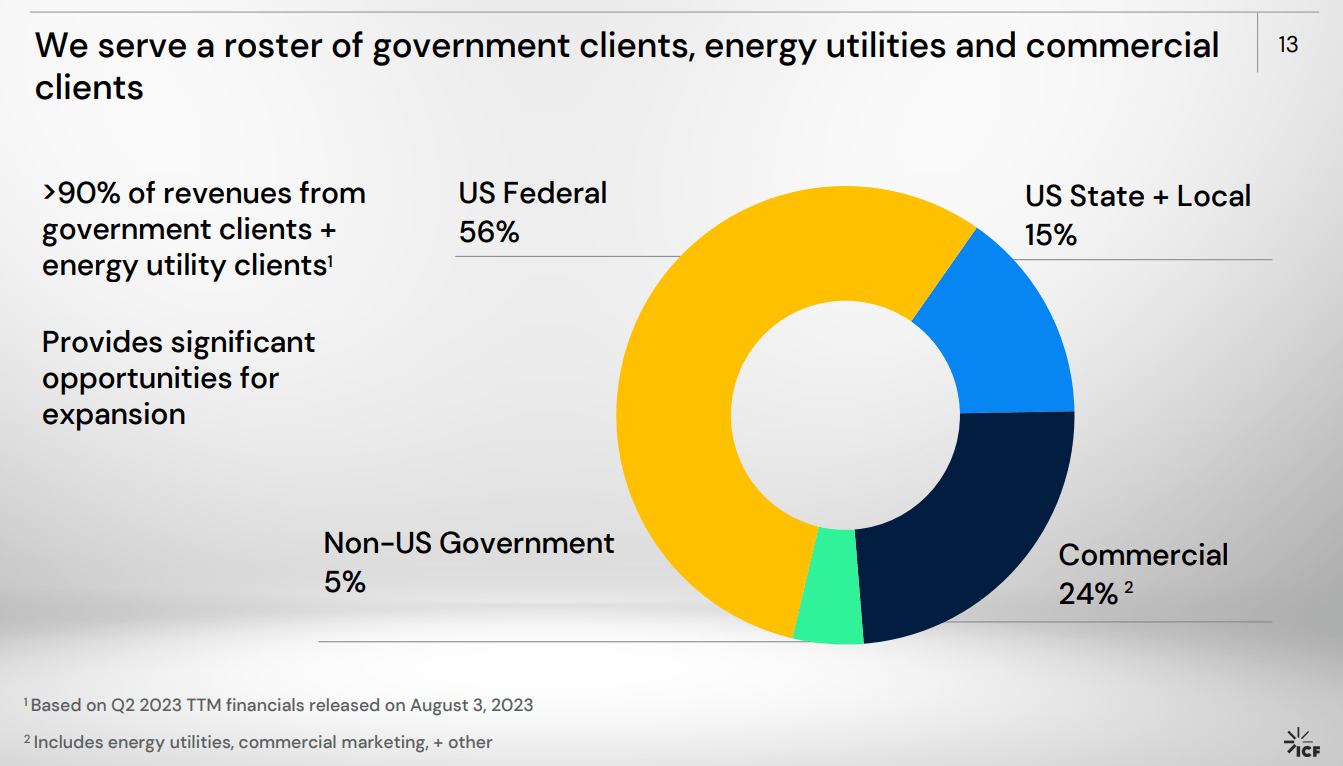

ICF International serves various end markets and sectors, including energy, environment, infrastructure, health, education, safety, security, and consumer markets.

{kind=link}

In Q2 , ICFI achieved substantial revenue growth of 18% YoY, an expansion of contract awards, particularly in new business, and maintained a robust business development pipeline worth ~$10.3 billion, the management noted during the earnings call . Notably, revenue growth was broad-based, with significant contributions from federal, state, and local government, and commercial energy clients, accounting for 88% of Q2 revenue.

Despite the revenue growth, the gross margin for Q2 FY2023 was 34.9%, a decline of 150 basis points YoY. This decrease was attributed to factors such as the acquisition of SemanticBits and timing-related project factors. However, ICF expects a sequential improvement in gross margins in 2H 2023, the firm's CFO shed some light during the call.

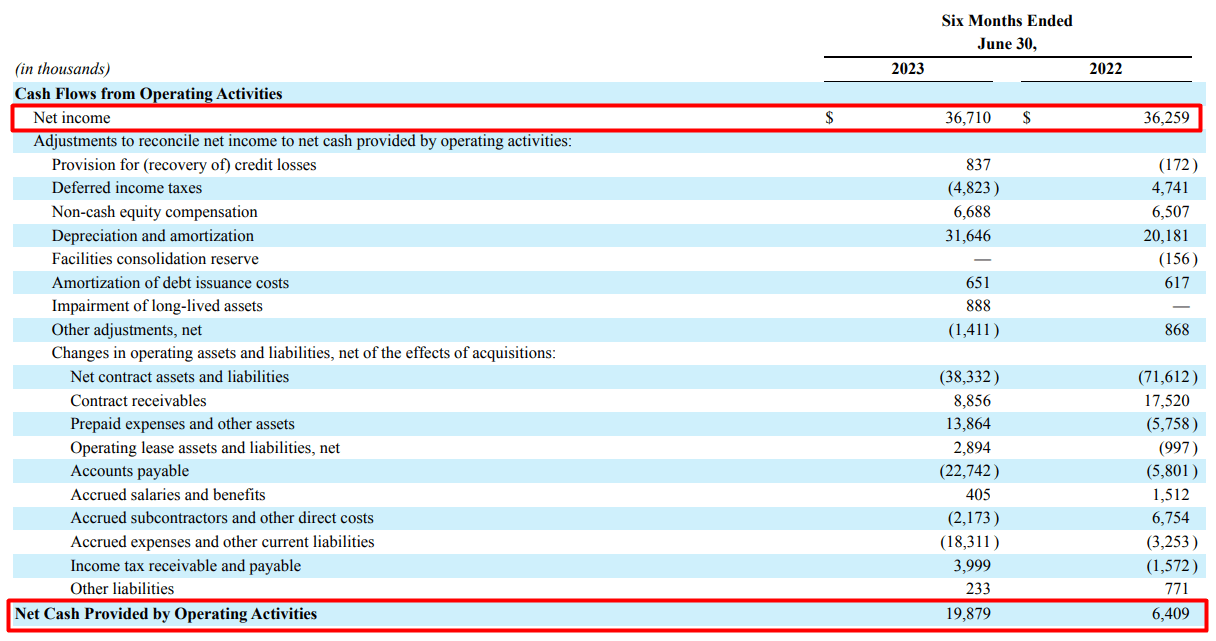

The company reported EBITDA growth of 19.2% to $47.5 million in Q2, with adjusted EBITDA increasing by 15.3% to $51 million year-over-year. Additionally, ICF generated strong cash flow from operations, with $36.7 million in Q2 and $19.9 million year-to-date - an improvement of 210% mainly because of net working capital changes:

{kind=link}

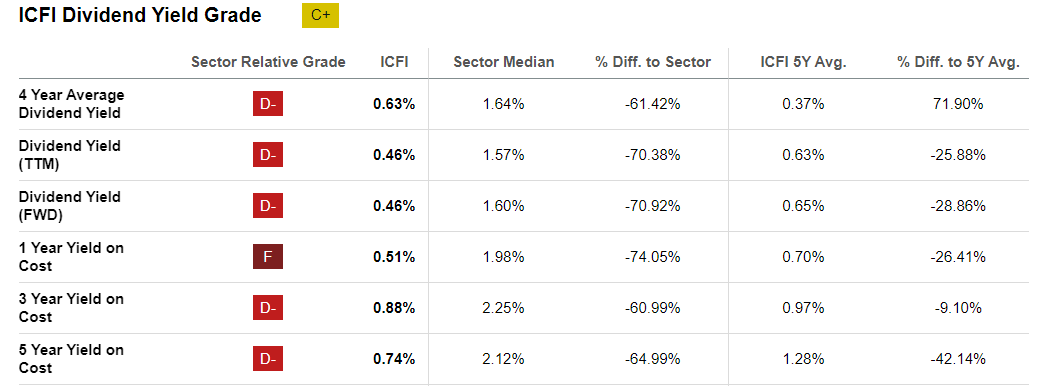

They also announced a quarterly cash dividend of $0.14 per share [payable in October 2023], making ICFI's dividend yield of 0.46% quite modest.

{kind=link}

ICF's financial guidance for FY2023 remains positive, with total revenue expected to range from $1.93 billion to $2 billion, EBITDA projected at $215 million in the mid-range, and a focus on continued growth and strategic initiatives in key markets.

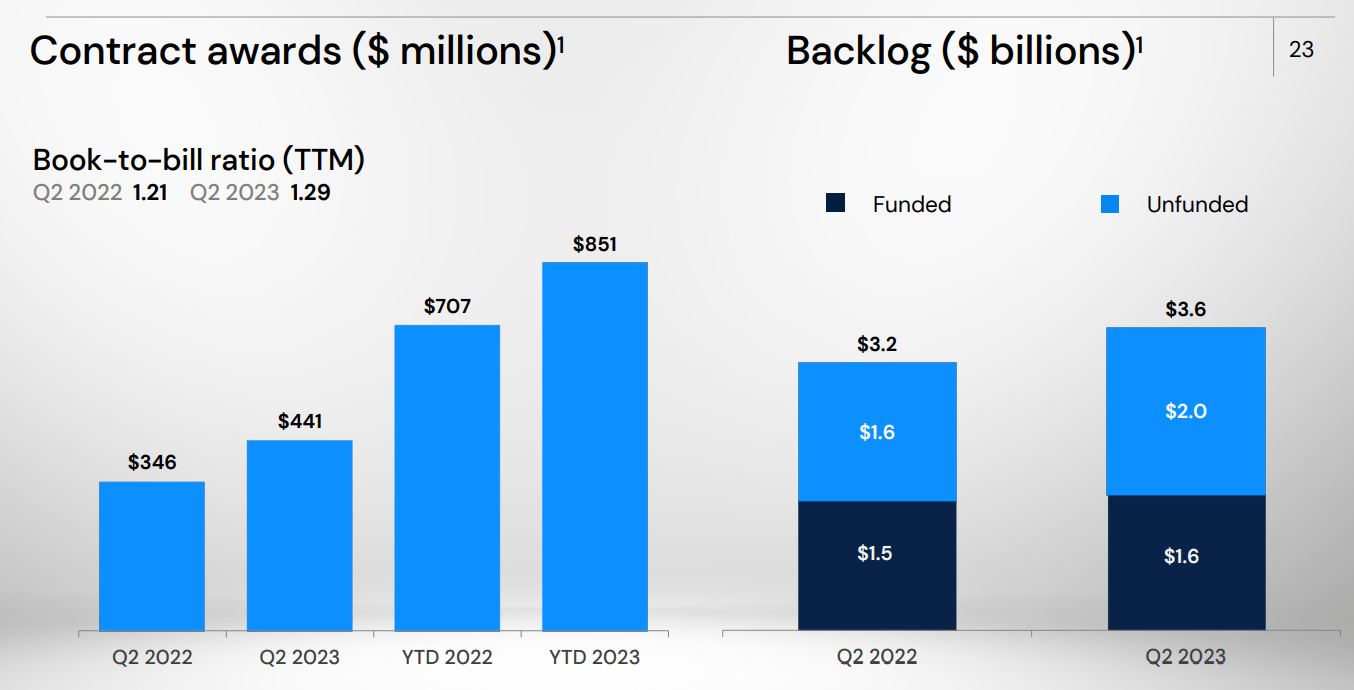

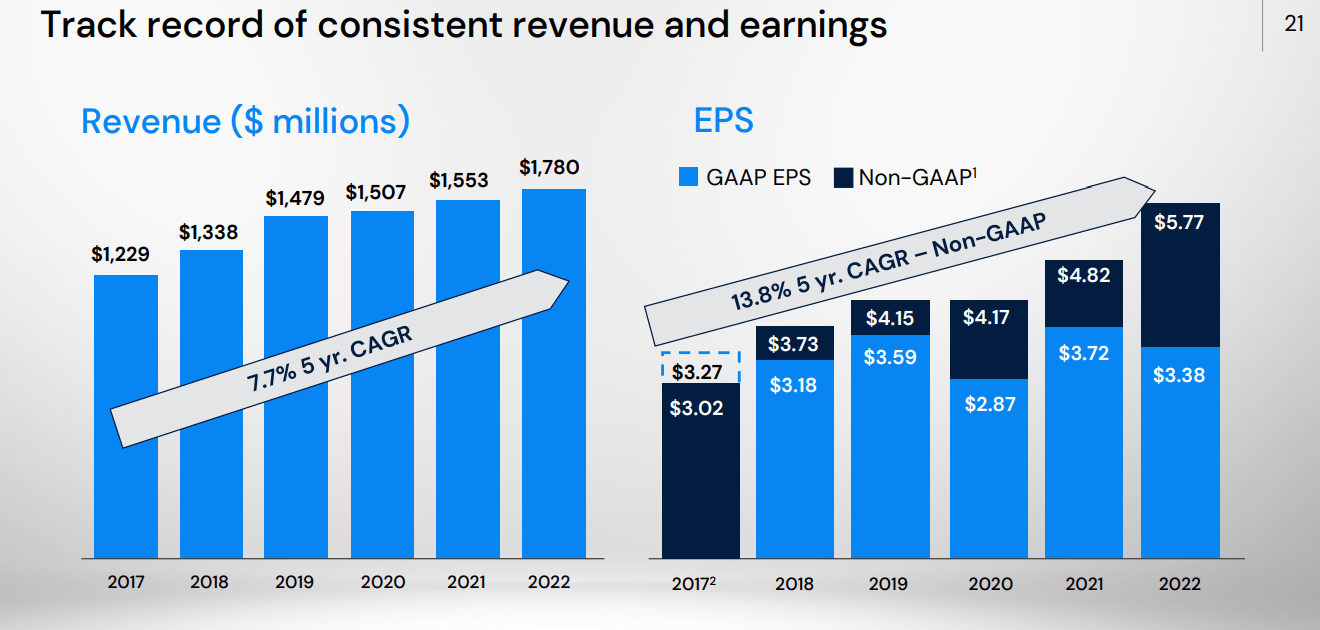

In general, I like ICFI's performance: the company focuses on innovation and new acquisitions and is heavily tied to government contracts, where its consulting services seem to be quite "sticky". This is borne out by the recent increase in backlog and contract revenue:

{kind=link}

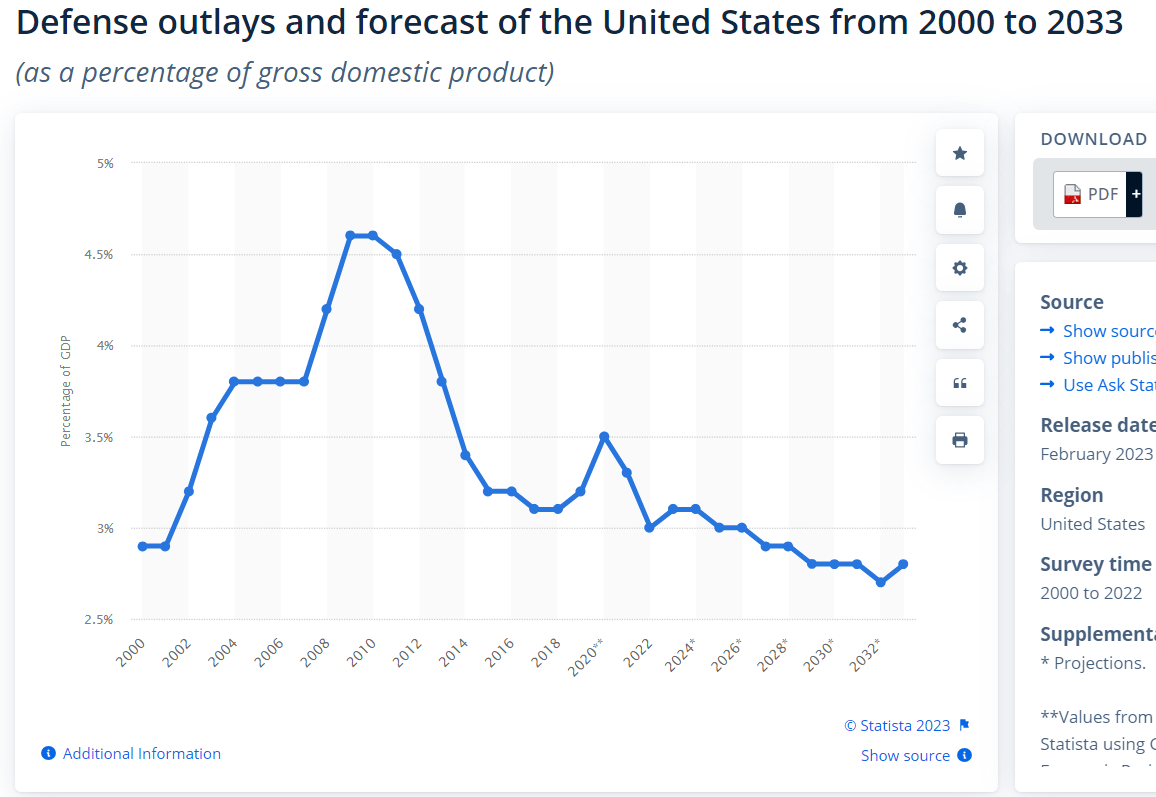

Now, as the geopolitical situation heats up in the world, I think the low defense spending as a percentage of GDP that we saw in the U.S. for the past few years is likely to increase. Here's what the projected dynamics look like now, according to Statista :

{kind=link}

And here is what NATO writes [July 2023]:

During the Cold War, defense spending for NATO Allies (even putting the United States aside) routinely averaged more than 3% of GDP, with some significant variation over time, but rarely falling below 2%.

Source: NATO , author's emphasis added

So I think Statista's forecast of ~47.5% [CAGR of ~3.6% annually] growth in defense spending over the next 10 years is slightly underestimated - there's a good chance the numbers will be much higher.

In this case, ICFI's business should continue to develop at about the same pace as in recent years due to its strong ties to innovative projects in the U.S. defense industry:

{kind=link}

All that remains is to understand how attractive the ICFI looks from the perspective of market expectations and its implied valuation levels.

The Valuation & Expectation

In terms of FCF generation, ICFI is currently at about the average level of the last 10 years:

According to the next-year price-earnings ratio, the stock looks slightly undervalued - by ~17.2%, compared to the 10-year average:

However, it is worth considering that ICFI has reduced the number of outstanding shares by ~6.18% in the last 10 years, which does not look very significant, but given that the buybacks were systematic, this should explain the eventual increase in valuation multiples, so we should better use a shorter horizon for comparison.

With a shorter time horizon of 5 years (instead of 10 years previously), ICFI stock appears strongly undervalued in terms of P/E ratio despite its YTD rise of ~22%:

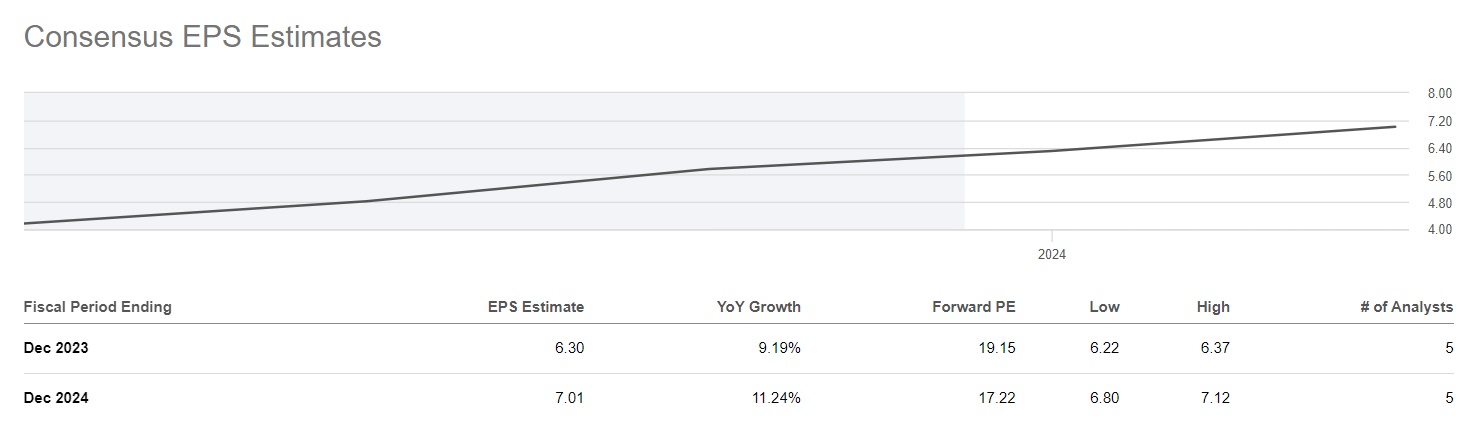

Moreover, according to Wall Street analysts , ICFI's P/E ratio must continue to decline despite renewed EPS growth in FY2024, which seems illogical to me:

{kind=link}

The Bottom Line

Investing in ICF International, Inc. comes with inherent risks that everyone should be aware of. The company's heavy reliance on government contracts exposes it to potential budgetary constraints and regulatory changes. Competition in the consulting and technology services sector may lead to pricing pressure. Acquisitions introduce integration challenges, and economic downturns or policy shifts can impact revenue. Market volatility and interest rate changes also pose stock price risks - ICFI is a small cap that is especially exposed to this kind of risk. So potential investors should conduct thorough due diligence and consider these factors before investing in ICFI.

Nevertheless, I'd like to note that the company continues to grow and develop, expanding its order book and investing in innovative projects and mergers. The company's systematic buybacks explain its multiple expansions and low dividend yield. In turn, the FCF yield indicates that ICFI is quite resilient and healthy above 6%.

The potential growth of the U.S. defense budget is a good catalyst to maintain a healthy background - the addressable market has a chance to grow faster than the current consensus, in my opinion.

If Wall Street analysts are correct about ICFI's FY2024 EPS, then at the P/E of ~22x, which seems reasonable, the upside potential should be ~28% by the end of 2024 - that's my base case.

So based on the above, ICFI stock is a Buy, in my view.

Thanks for reading!

For further details see:

ICF International: Interesting Bet On U.S. Defense Spending Expansion