ICFI - ICF International: Solid Performance Sturdy Fundamentals Stock Price Quite High

2023-05-18 17:03:10 ET

Summary

- ICF International, Inc. remains robust with its sustained revenue growth and stable margins.

- Its decent financial positioning is one of its strongholds.

- It remains a staple across different sectors as recession woes persist.

- Dividends continue to increase, but yields are underwhelming.

- The stock price uptrend is starting to exceed the intrinsic value of the company.

Macroeconomic headwinds intensified as inflation set a new all-time high in 2022. It stretched faster and further than expected, prompting policymakers to stabilize prices. In turn, interest rates soared and enticed savings rather than borrowings and investments. Unsurprisingly, demand softened, matched by the clearing supply chain bottlenecks. This noticeable change curtailed purchasing power and production volume across industries. But for some, it became an opportunity to shine and expand.

ICF International, Inc. ( ICFI ) used the situation to its advantage. It became a staple as businesses and policymakers had to rethink their policies. And now, it continues to flourish and expand as its expertise remains crucial for the market. It practices what it preaches, given its well-balanced growth and viability. It capitalizes on its strategies to stabilize revenues and margins amidst inflation. Even better, it maintains a decent financial positioning to ensure sustainability. This aspect allows it to cover its operating capacity, borrowings, and capital returns. Likewise, the stock price remains consistent with the sound fundamentals. However, the uptrend appears quite excessive, leading to limited upside potential.

Company Performance

The past three years have been a series of crests and troughs for the US economy. The unprecedented events in 2020 led to a huge downturn. Also, the pandemic restrictions made it challenging to sustain economic recovery. In 2021, things were far different, characterized by a robust economic rebound. But not a year later, things turned almost a hundred and eighty degrees. Macroeconomic volatility was evident in the past three quarters. As inflation rose 9.1% , the demand and production capacity decreased. Some industries saw well-maintained growth with their pent-up demand. However, the overall impact was unfavorable. To combat the rising prices, The Fed raised interest rates by 75 bps in four quarters. It proved helpful, but macroeconomic headwinds persisted. Today, recession fears remain intense, prompting businesses to adjust their operating capacity. Yet, ICF International stock continues to capitalize on its growth and expansion. It still shows enticing growth prospects amidst mixed market conditions.

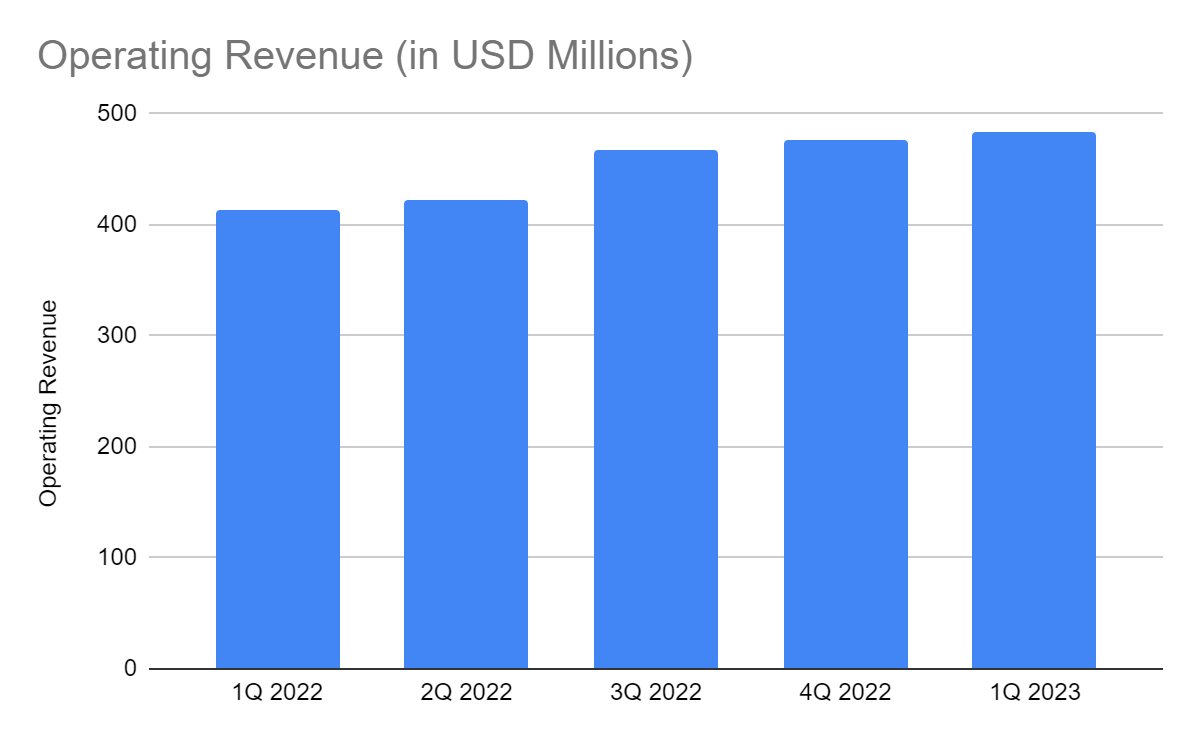

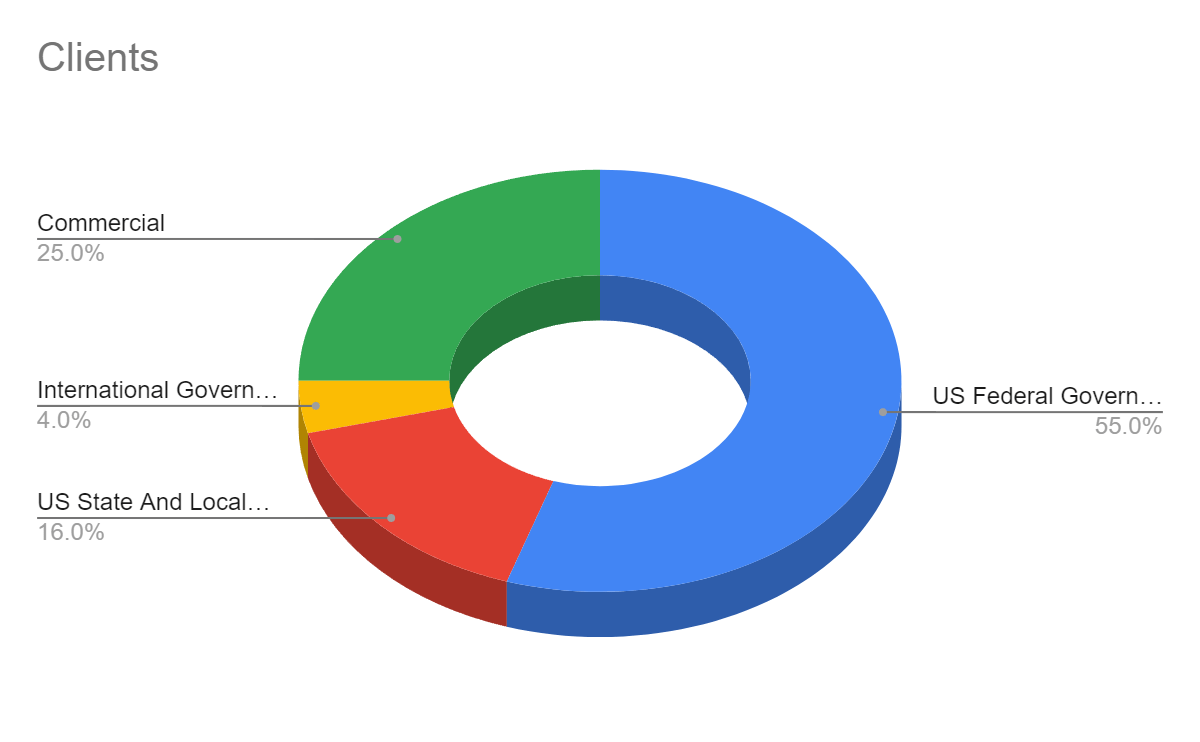

It started the year strong with its operating revenue of $483.28 million , a 17% year-over-year increase. It was impressive, given the bleak market prospects in the previous quarters. We can attribute its successful business executions to various factors. Its broad-based growth was driven by the robust demand from its clients. The federal and local government institutions are the cornerstones of its operations. In fact, these are company strengths, especially during periods of volatility and downturns. Government clients are more fixed, leading to a more secure revenue stream. Let's face it. Many businesses may go bankrupt in some industries, even the industry giants. But more often than not, government institutions and enterprises will remain safe. After all, their income comes from taxes, FDIs, portfolios, exports, and many more sources. These also vary with macroeconomic trends, but these are safer. But what's more impressive is the 19% increase in the commercial segment. So except for the international government, all remaining segments had a double-digit increase.

Operating Revenue (MarketWatch)

{kind=link}

ICFI's unique business model is suitable for the current market landscape. Aside from its demand, a contract-based business guarantees long-term partnerships. It is more crucial today amidst the tight competition. The only downside is the lower pricing flexibility. Yet, it applies to contracts before 2022. The company can also have more freedom to conduct projects with improved efficiency. Pricing and marketing strategies work well with its business model. This move allows ICFI to retain clients or cover the change in the number of clients through pricing. In 4Q 2022 and 1Q 2023, the company got fifteen contracts, as shown in its press releases . Another core strength of ICFI is its capitalization on accretive acquisitions. In the second half of 2022, it made two acquisitions to expand its capacity. It paid off in the next two quarters through increased revenues. Its investment in technologies can also help improve efficiency and increase its market appeal. As the call for more sustainable and eco-friendly business operations intensifies, ICF must adapt to it. It is part of its services. But more importantly, it must maintain customer ties and partnerships. It is vital as it caters to IT modernization, disaster management, and ESG services.

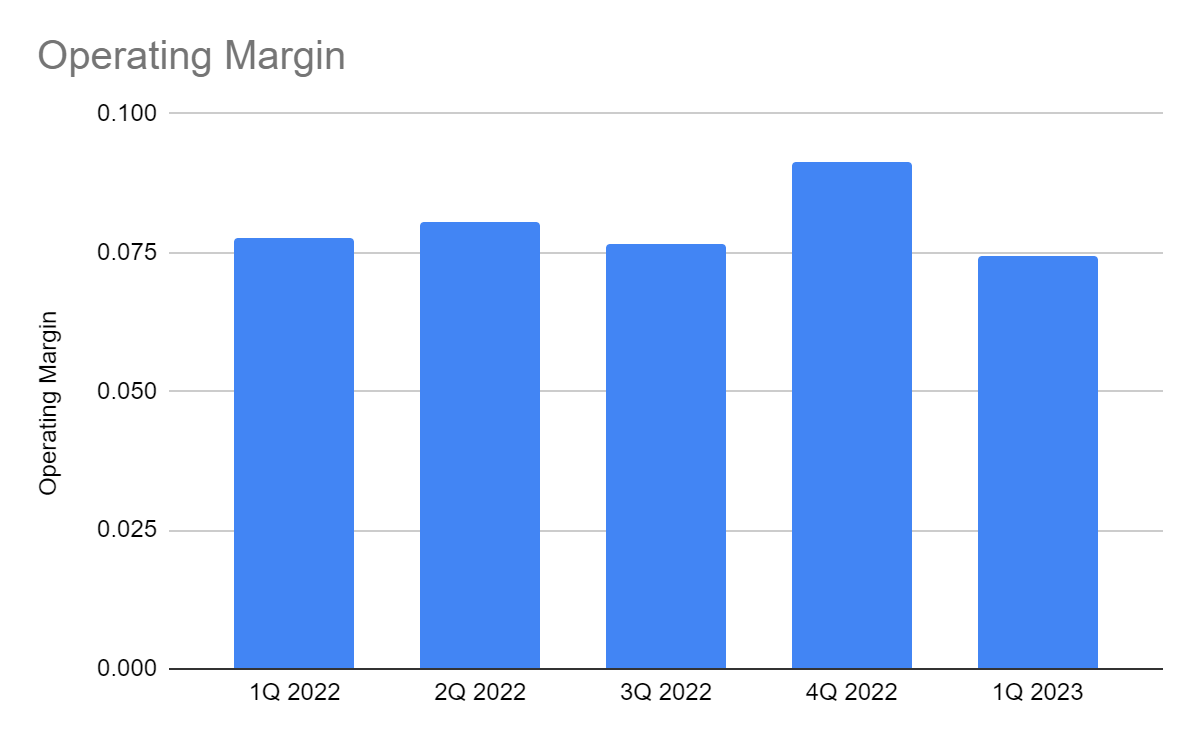

But what makes ICF a solid company is its efficient asset management. Amidst the rising prices, it kept its expenses manageable in 1Q 2023. Its SG&A expenses remained flat, showing efficiency in handling its labor and technology. This aspect also demonstrated the commitment of the company to helping clients make strategic business policies and decisions. As such, its margin stayed stable at 7.4% versus 7.7% in 1Q 2022. It was also the lowest in the past five quarters. We can attribute it to the increase in direct operating costs. Despite this, the actual operating income of $36 million was better than in 1Q 2022, with $32.12 million. It was also the second-highest operating income. Indeed, its expansion remained fruitful, given the increasing revenues and operating income.

Operating Margin (MarketWatch)

{kind=link}

This year, the company may face the same challenges as recession woes continue. But given its historical performance and current business model, I believe the company can get through them. It decreased its international operations after exiting UK lines. But the contract won in Puerto Rico can partially offset it. Also, it was immaterial to the international segment of the company since many clients are in Canada. Even better, it has already won two contracts this quarter. It can also better manage its expenses as prices become more stable. We will cover it in more detail in the following section.

How ICF International May Stay Afloat This Year

We already saw how ICF International, Inc. remained unperturbed amidst macroeconomic volatility. The fact that it was crucial for strategic business decisions amidst the rising prices and socio-environmental issues drew more demand for its services. However, we must recognize the risk surrounding the business. Interest rate hikes remain the primary risk that the company faces. As The Fed maintains its conservative approach to combating inflation, it raises interest rates. It continues to affect the business, as we see in the substantial increase in interest expense. It must also be careful since it has high financial leverage. Its borrowings are equivalent to 40% of the total assets. If interest rate hikes continue, the cost of borrowing may increase more. The consolation is that only 8% of borrowings have current maturities. Also, the increase in interest rates has slowed down recently.

Fed Funds Rate (Trading Economics)

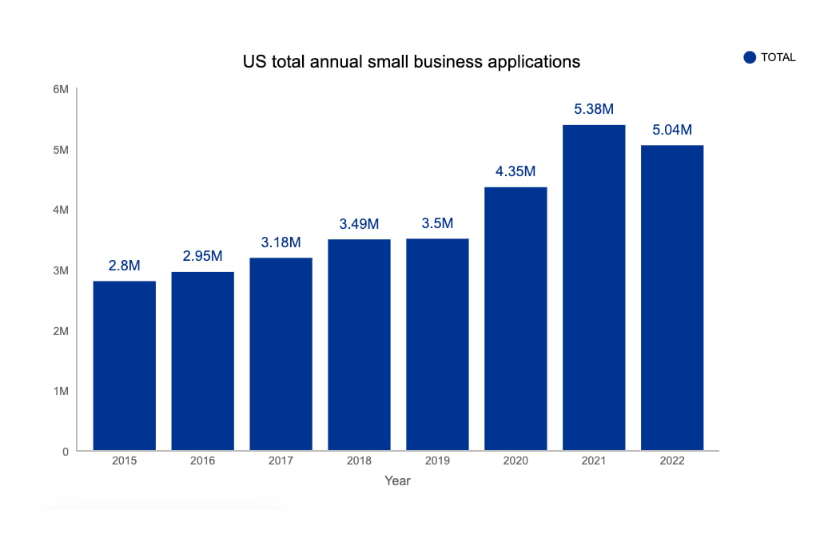

On the contrary, potential opportunities outweigh risks. The simplest way is by looking at the current inflation rate. At 4.9% , inflation has slowed by 46% from its 2022 peak. Although demand may take more time to adjust, positive spillovers may materialize. If the downtrend continues, interest rate hikes may continue to cool down or at least stay flat at 25 bps. It will be easier for the company to win contracts and adjust expenses to sustain its growth and improve margins. It can also lead to more business openings and help ICFI penetrate the commercial segment more. As of 1Q 2023, the portion of the commercial segment increased from 24% to 25%. It indicates the increased presence of ICFI in the private sector and its enhanced commercial market appeal. Given its capitalization on prudent acquisitions, it may be easy to sustain its expansion. It can increase its concentration on the commercial segment in the US. After all, business openings have increased recently. In the SMB sector, SMEs rose from 32.5 million to 33.2 million in 2Q 2022. Also, new business openings remained high at 5 million applications. It was lower than in 2021, with 5.4 million, but the total number of businesses kept increasing. With the continued decrease in inflation, recession woes may decrease at some levels. It can also sustain business formations. According to doola, the average cost of forming a private business is only $197 plus state fees. If we combine the impact of lower inflation with the digital and fintech revolution, the business sector may regain momentum.

{kind=link}

US Total Business Applications (Commerce Institute)

{kind=link}

Inflation Rate (Trading Economics)

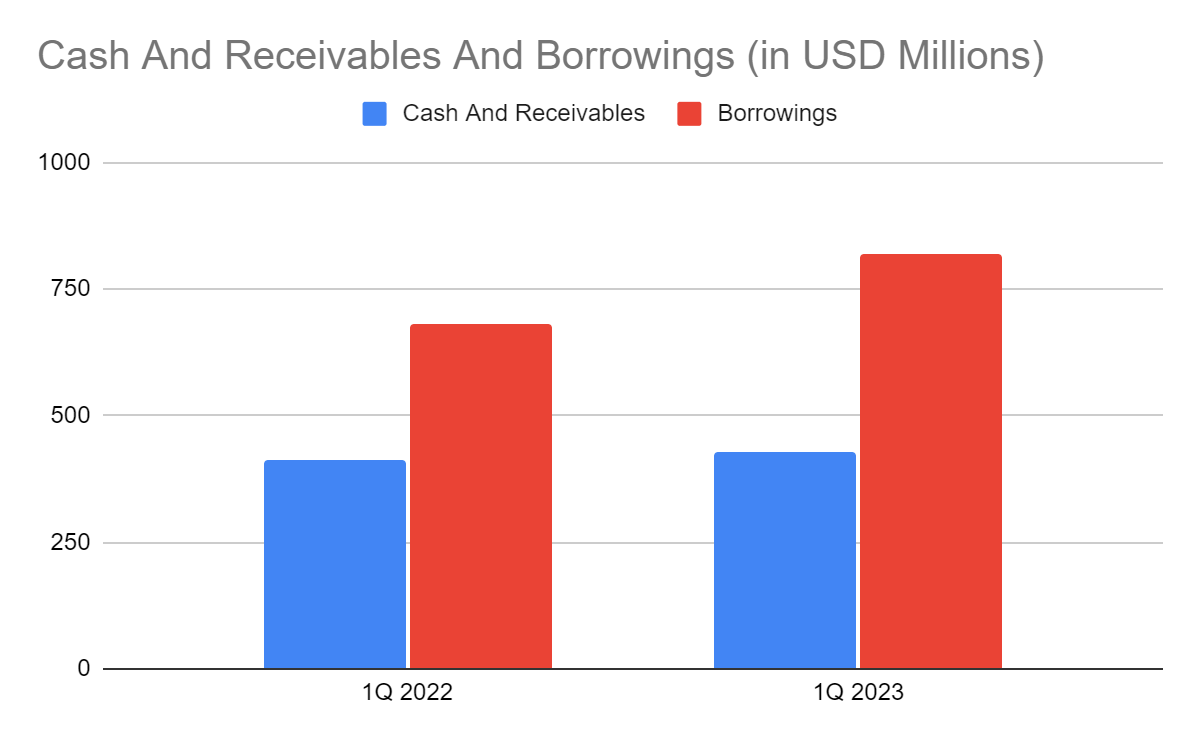

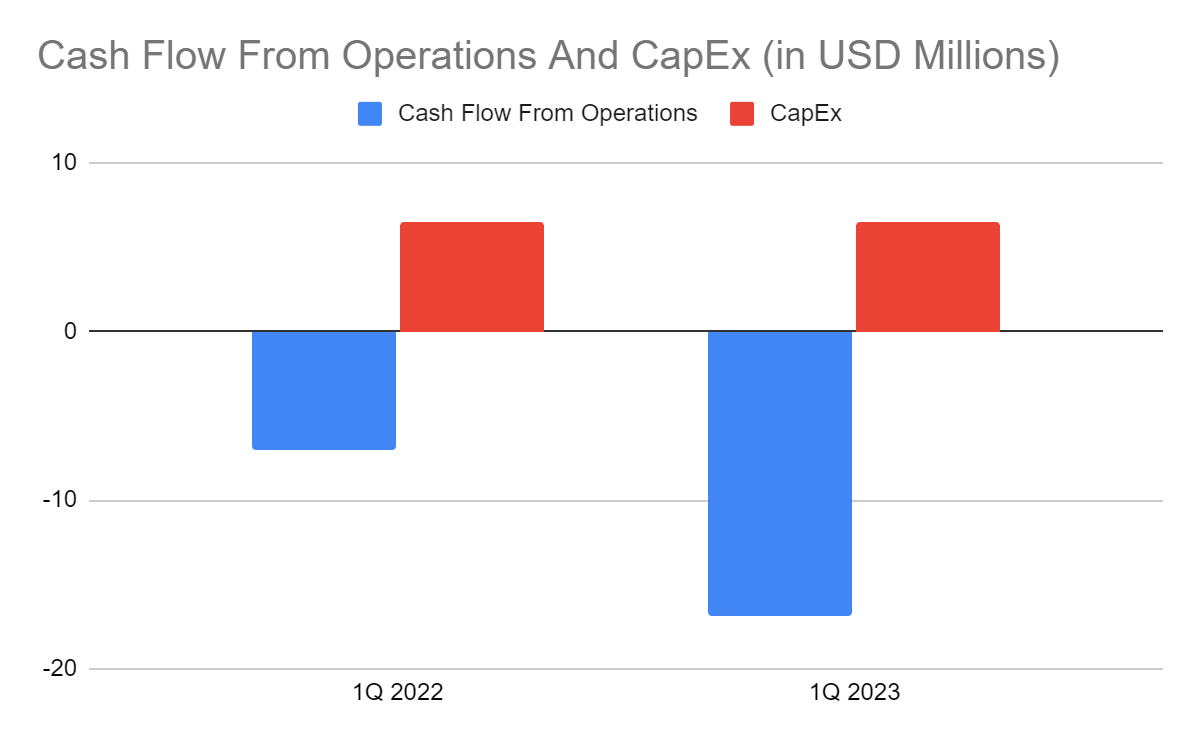

Moreover, a decent financial positioning can help ICFI navigate the current market landscape. Cash may be irrelevant at only $8.94 million , but receivables have increased to $417.58 million. It may be risky since it can lead to massive defaults and delinquencies. But we must understand that its clients are the federal and local government and private businesses of varying sizes. Their combined amount comprises 21% of the total assets, making ICFI a liquid company. Also, the Net Debt/EBITDA Ratio of 1.97x shows that the company earns enough to cover its borrowings. We can confirm the fruitful use of its resources in the Cash Flow Statement. Its Cash Flow From Operations became negative in 1Q 2023. But we can see that it paid a substantial portion of its accounts payable and accrued expenses, which we can confirm in their movements in the Balance Sheet. If the company had kept its accounts payable and accrued expenses at the previous level, it would have realized cash inflows. The thing is, the core operations of the company can cover its operations, current borrowings, and payables. We can see it in the average cash burn of $82,100. With that, the company has nine years to deplete its cash without increasing its financial leverage. It is logical since it is not a capital-intensive company. The essential thing is that the company continues to balance growth and viability with sustainability.

Cash And Receivables And Borrowings (MarketWatch)

{kind=link}

Cash Flow From Operations And CapEx (MarketWatch)

{kind=link}

Stock Price Assessment

The stock price of ICF International, Inc. has been decreasing over the years. There were some corrections, but the uptrend remained prominent. At $112.91, the stock price is already 17% higher than last year's value. It has already exceeded the intrinsic value of the company. We can confirm it using the PB Ratio, given the current BVPS of 45.01 and PB Ratio of 2.47x. If we use the current BVPS and the average PB Ratio of 2.28x, the target price will be $102.84.

Meanwhile, it is a secure dividend stock with consistent payouts. However, its yields are only 0.49% versus the S&P 600 and NASDAQ average of 1.72% and 1.55%. We can attribute it to the potential overvaluation and low dividends. Despite this, dividends remain well-covered, given the Dividend Payout Ratio of 16%. Also, the company makes up for it through consistent share repurchases. We can also compare the cumulative EPS and average stock price change since 2019 to check the investment returns. Using the cumulative EPS of $13.56 and the stock price change of $19.37, the difference will be $5.81 or $1.37 per year. For every $1 increase in EPS, the stock price increased by $1.37. The company gives decent investment return prospects, making it an ideal stock. To assess the stock price better, we will use the DCF Model.

FCFF $144,095,000

Cash $8,940,000

Borrowings $831,340,000

Perpetual Growth Rate 4.4%

WACC 9.2%

Common Shares Outstanding 18,788,000

Stock Price $112.91

Derived Value $107.02

The derived value shows that the stock price has potential overvaluation. There may be a 5% decrease in the next 12-18 months. Given the impressive company fundamentals, I am adding ICFI to my watchlist. But given the stock price, we may have to wait before purchasing shares. There may be limited upside potential.

Bottom Line

ICF International, Inc. is a solid company with a robust performance amidst macroeconomic volatility. Its unique business model, prudent expansion, and operational efficiency are its cornerstones. It also has a decent financial positioning that shows sustainability. Even better, it continues to make capital returns through dividends and share repurchases. Meanwhile, the stock price keeps increasing and remains consistent with the fundamentals. But the actual stock price is higher than the intrinsic value of the company. The stock is a good bargain at $102-105. The recommendation, for now, is that ICF International, Inc. is a hold.

For further details see:

ICF International: Solid Performance, Sturdy Fundamentals, Stock Price Quite High