IMMX - Immix Biopharma: A Mid-To-Late Stage CAR-T Biotech Quietly Gaining Momentum

2023-09-19 07:00:00 ET

Summary

- In-licensing of NXC-201 transforms Immix into a mid-to-late stage BCMA-targeting CAR-T therapy with a differentiated tolerability profile.

- First and only CAR-T therapy in clinical development for AL amyloidosis.

- Recent months have seen the construction of an impressive Board and the addition of scientific advisors, including Memorial Sloan Kettering director of amyloidosis.

- Clinical trial expansion to the US is expected in the 4Q23.

Intro

Immix Biopharma (IMMX) came public via a small IPO in 2021 as an early-stage oncology biotech developing therapeutics to deliver small molecules deep into the tumor microenvironment. Then, in December 2022, the company quietly transformed itself by in-licensing NXC-201, a BCMA-targeting CAR-T therapy developed by Hadassah Medical Center in Israel, which has so far demonstrated a significantly differentiated clinical profile versus similar approved therapies Carvykti (Janssen/J&J) and Abecma (Bristol Myers). While Immix’s original lead program IMX-110 is intriguing and worthy of exploration in a future writeup, it is Nexcella, the subsidiary of Immix formed to advance NXC-201, that is the focus of our investment thesis as a unique opportunity that appears to be completely overlooked by the market.

Currently enrolling in an Israel-based Phase 1b/2a in both multiple myeloma [MM] and AL amyloidosis [ALA], NXC-201 has reported data from 58 late-stage patients (50 MM, 8 ALA) that suggests comparable (and potentially superior) efficacy compared to approved BCMA CAR-Ts, but with a dramatically improved tolerability profile. In MM, interim results of NXC-201 have shown post-treatment hospital stays of 2-3 days versus the 1-2 weeks normally required due to severe side effects.

Not only could NXC-201’s safety profile significantly improve patients outcomes and the practicality of CAR-T treatments, it has also enabled NXC-201 to be the first and only CAR-T in development for ALA, a rare disease characterized by the deposition of amyloid fibrils in tissue leading to organ failure and extreme frailty. ALA is the company’s most eminent opportunity, with an estimated 20,000 patients in the US and major European countries and only one therapy approved for newly-diagnosed patients and no approved therapies for relapsed or refractory (r/r) patients, the patient population NXC-201 is currently dosing. ALA is also Nexcella’s quickest path to market, with only 30-40 patients expected to be sufficient for a BLA submission. The company believes it could submit a BLA in the 1H25.

With a potentially highly-differentiated mid-to-late stage program now in hand, the Immix and Nexcella teams, which are still somewhat overlapped, have made considerable progress in moving NXC-201’s development to the US and building momentum at Nexcella over the last few months, including:

-

Completion of pre-IND meeting with FDA; IND approval and US expansion expected in 4Q23.

-

Orphan Drug Designation [ODD] granted for NXC-201 in MM in August 2023; we expect ODD in ALA in the coming months.

-

The construction (which only began in June 2023) of a well-experienced five-person Board of Directors, including the former CEO of Pfizer.

-

Beginning construction of Scientific Advisory Board [SAB], including the director of Memorial Sloan Kettering’s amyloidosis program, a leader in the cell therapy space.

-

$10 million private placement announced on August 22nd.

-

~$500k in insider buying since September 1st.

-

Scheduled presentation of additional ALA patients data at the International Myeloma Society [IMS] Annual Meeting in Athens, Greece (September 27-30th).

-

Scheduled participation in the Bank of America 2023 Healthcare Trailblazers Private Company Conference in late October.

Despite recent momentum, Immix remains a nano cap with just ~$57 million of market capitalization, trading in the same $2-3/share range it has traded in since before the NXC-201 in-license, despite the transformation of the company from an (interesting) early-stage solid tumor biotech to a mid-to-late stage and differentiated CAR-T biotech. We believe the market is still largely unaware of the Nexcella story due to the unorthodox/stealthy nature of the deal with Hadassah, which we expect to change as early as this fall/winter as the company presents additional data, expands its trial to the US, and participates in investor conferences and meetings.

On its current trajectory, we think that the market’s ignorance of Nexcella constitutes a special situation with ~5-10x upside potential based on other CAR-T companies at similar stages of development like Arcellx ($1.6 billion market cap) and Gracell ($215 million). We also think Nexcella could eventually become an attractive candidate for a strategic partnership, or even potentially pursue an IPO spinout from Immix (discussed below), as company filings related to the NXC-201 in-licensing mention Nexcella’s intention to be an independently-financed entity.

Regardless, we believe the $10 million private placement in August is an early sign that some (still smaller) investors are beginning to learn the Nexcella story and believe the stock will inevitably gain momentum as the pieces continue to come together over the next 6-12 months.

Nexcella Transaction

In December 2022, Nexcella was formed as a subsidiary of Immix to acquire the rights to Hadassah Medical Center’s plasma cell CAR-T platform, which includes NXC-201 as well as preclinical programs NXC-301 and NXC-401, which both have undisclosed binding targets but are intended to eventually treat other plasma cell malignancies like acute lymphocytic leukemia [ALL] and acute myeloid leukemia (AML).

Despite NXC-201’s relatively established clinical profile across 58 patients treated to date, Nexcella agreed to in-license NXC-201 for only $1.5 million up front, mid-single digit royalties, and a $20 million milestone payment upon NXC-201 achieving $200 million in sales. In general, the terms of the deal are quite favorable to Nexcella, and we would be interested in knowing how Immix got access to NXC-201 from Hadassah. It is possible there is some connection to Immix’s Israeli CEO, Dr. Ilya Rachman.

The 8-K filed on 12/14/22 regarding the deal also stated that Nexcella is “planned to be an independently financed company”. As discussed below, Immix and Nexcella have been working to establish Nexcella from a clinical and leadership perspective, including the construction of a Board and SAB of experienced and esteemed professionals in the hematology as well as broader biopharma spaces.

NXC-201 Differentiated Safety

While BCMA-targeted CAR-Ts like Carvykti (Johnson & Johnson) and Abecma (Bristol Myers Squibb) have dramatically improved outcomes for MM in recent years and are consequently moving to earlier lines of treatment, they have experienced a number of challenges, including supply shortages and, most importantly, severe and persisting side effects that often require hospital stays of 1-2 weeks.

The most common of these side effects are neurotoxicity, which can induce confusion, seizures, and Parkinson’s-like symptoms in severe cases, and cytokine release syndrome [CRS], which occurs in varying severity and causes fever, low blood pressure, and respiratory distress requiring external ventilation. While neurotoxicity occurs in 5-25% of patients, CRS is essentially a given in CAR-T-treated MM patients, occurring in 90%+ of patients. While most MM CAR-Ts aim for low rates of Grade 3 CRS, even Grade 1 CRS necessitates hospitalization.

CRS can take multiple days to develop following treatment and can persist for over a week. In MM, Carvykti’s CARTITUDE-4 Phase 3 trials reported CRS in 95% of patients with a median time of onset of 7 days (ranging from 1-12 days), and neurotoxicity in 26% of patients, including Parkinson’s-like symptoms in 20% of patients. Abecma’s pivotal trial in relapsed/refractory (r/r) multiple myeloma reported 85% of patients experienced CRS with a median time of onset of 1 day (ranging from 1-23 days) and a median CRS duration of 7 days (range 1-63 days). Abecma also caused neurotoxicity in 28% of patients.

Arcellx—which achieved its strategic agreement with Gilead/Kite ($325 million upfront, $3.9 billion aggregate milestones) based largely on the notion that its lead candidate, CART-ddBCMA, had a novel, more specific binding domain with reduced off-target effects—reported CRS in 94% of patients and neurotoxicity in 18% of patients in interim data from its ongoing iMMagine-1 Phase 2 trial. Arcellx’s CART-ddBCMA patients experience CRS that onset 2 days post-treatment and last for 5-8 days, leading to hospital stays of 7-10 days in most cases. CART-ddBCMMA was also placed on a clinical hold by the FDA in June 2023 following the death of a patient, which was lifted in August, with the company announcing it had made changes to the study protocol.

Arcellx Slide Deck

Conversely, NXC-201 (shown below) has reported no cases of ICANs (a measure of neurotoxicity) of any severity, no cases of Parkinson’s-like symptoms, just one Grade 3+ CRS across 42 MM patients, and resolution of CRS in 1-2 days. While NXC-201 triggered overall CRS at comparable rates to other BCMA CAR-Ts, resolution is achieved dramatically (up to 80%+) faster than with other BCMA-targeted therapies.

Nexcella Slide Deck

The Nexcella slide deck (shown below) summarizes the safety profiles of each BCMA CAR-T. Not only could NXC-201’s safety profile improves patient outcomes, but it could also significantly reduce the costs and resources required to support patients after treatment. Including hospital costs, the total cost of CAR-T treatment in MM can exceed $1 million in many cases. A 2021 study Finds Total Cost of Care for CAR-T, Post-Treatment Events Can Exceed $1 Million by Prime Therapeutics in B-cell lymphoma, which is associated with shorter hospital stays than MM, found CAR-T therapy cost over $700k on average, despite the CAR-T treatment itself costing only $370k.

Nexcella Slide Deck

Importantly for patients, NXC-201’s efficacy appears to be generally comparable to other BCMA CAR-Ts in MM, with especially strong and potentially favorable early signs in patients that have previously received and failed a BCMA-targeting therapy. NXC-201’s results in MM to date are summarized below and we intend to conduct a deeper dive into MM efficacy in the future.

Nexcella Slide Deck

While presumably related to the specifics of the CAR construct and its binding epitope on BCMA, it is unclear exactly how NXC-201 is able to deliver commensurate efficacy and significantly better tolerability compared to other BCMA CAR-Ts. A study published in Haematologica by Hadassah researchers describes the design of NXC-201’s CAR construct which it states is optimized for improved specificity and function. Slide 15 of the Nexcella slide deck (which was added in the most-recent version of the deck) shows a rendering of the binding construct next to competitors, but without an explanation of its advantages.

Nexcella Slide Deck

Either by intelligent design or good fortune, NXC-201 appears so far to be endowed with a fundamental advantage over other BCMA CAR-Ts, with the potential to both be safer for patients as well as dramatically reduce the cost and resource burden of supportive care associated with CAR-T therapy by up to ~80%.

AL Amyloidosis

NXC-201’s safety profile also allowed Hadassah researchers to advance NXC-201 as the first potential CAR-T therapy in AL Amyloidosis., which we believe to be NXC-201’s clearest opportunity. Interestingly, while ALA and MM both involve plasma cell dyscrasia (dysfunction) and are considered related diseases, the fundamental rationale for targeting BCMA in ALA did not arise until recently. In 2019 , a group at Memorial Sloan Kettering Cancer Center (including now-Nexcella SAB member Dr. Heather Landau), showed a median of 80% of plasma cells in ALA patients expressed BCMA. The finding was later confirmed by another group, which found 39% expression, as well as by Hadassah researchers.

AL Amyloidosis is a rare disease involving the production of misformed antibodies produced by aberrant plasma cells that eventually accumulate in vital organs (e.g. heart, kidneys), impairing function and eventually leading to death. In the US, there are about 2,000-4,000 newly-diagnosed patients annually, with most patients diagnosed at later stages of disease, which have very poor prognosis. Median survival of Mayo Stage III and Stage IV patients, the gold-standard AL Amyloidosis staging system created by the Mayo Clinic, was only based on the widely-used Mayo Clinic amyloidosis staging system) is only 14 months and 6 months , respectively.

ALA eventually causes extreme frailty due to organ dysfunction, which presents a challenge from a treatment perspective and is likely why there are no other CAR-Ts in development for ALA currently. For example, in an MM trial, Janssen’s Tecvayli, a BCMA-targeted T cell engager, reported cardiac-related death in 10% of the subset of patients with concomitant AL Amyloidosis. The study’s investigators called for increased monitoring of comorbid ALA/MM patients due to cardiac complications.

The most common standard of care (SoC) for ALA patients is a combination termed “CyBorD”, which is a combination of chemotherapy Velcade (bortezomib), alkylating agent cyclophosphamide, and corticosteroid dexamethasone. Though results vary across a number of studies conducted in different patient populations, one study of CyBorD in treatment-naive patients reported 62% overall hematological response rates and 67% of patient survival at 2 years, though results were significantly poorer for Stage III patients, with a median survival of just 7 months.

Autologous stem cell transplants in combination with chemotherapy have also been a treatment option for ALA patients since the 1990’s, with ORRs of 40-60%, though Nexcella estimates only 20% of patients are eligible.

The most notable advancement in treatment has been Darzalex (daratumumab), an anti-CD38 antibody developed by Genmab and marketed by Janssen/J&J, which was granted accelerated approval in combination with SoC as the first drug approved for newly-diagnosed ALA in 2021. Darzalex was originally approved in 2015 in multiple myeloma and has been an extremely successful treatment, generating $2.4 billion of sales in the 2Q23 (~$10 billion run rate).

In this video from June 2023, Dr. Paulo Milani of the University of Pavia in Italy (a world-leader in ALA) describes the current treatment landscape in ALA, which consists of Daratumumab + CyBorD in nearly all cases, termed Dara-CyBorD. As mentioned, Darzalex is approved specifically for newly-diagnosed patients, and in these patients has reported CRs of 53% and organ response rates at six months of 42% ( Kastritis, 2021 ). For context, 13% of patients experience Grade 3 or Grade 4 adverse events.

While Darzalex improves outcomes and survival for patients, most patients will eventually experience disease progression (reported median progression-free survival ranges between 17-36 months), at which point they are termed relapsed/refractory (r/r) patients. In these r/r patients, according to this review paper , Darzalex reported ~75% ORR and ~20% CR across multiple studies in r/r ALA in patients that were treated with SoC but not Darzalex (patients were probably treated with SoC before Darzalex was approved in most cases). In patients that have progressed after Dara-CyBorD, retreatment with Darzalex resulted in only 22% ORR ( Theodorakakou, 2022 ).

There are currently no approved therapies for r/r ALA, and as described by Dr. Jahanzaib Khwaja of the University College London in this Unmet needs in AL amyloidosis: treatment options for R/R patients | VJHemOnc , there are very few available treatment options. Patients are relegated to enrolling in clinical trials, which he describes as scant, or opting for compassionate use therapies. Dr. Angela Dispenzieri likened the treatment landscape in r/r ALA to the “wild west” in a recent interview with Hematological Oncology.

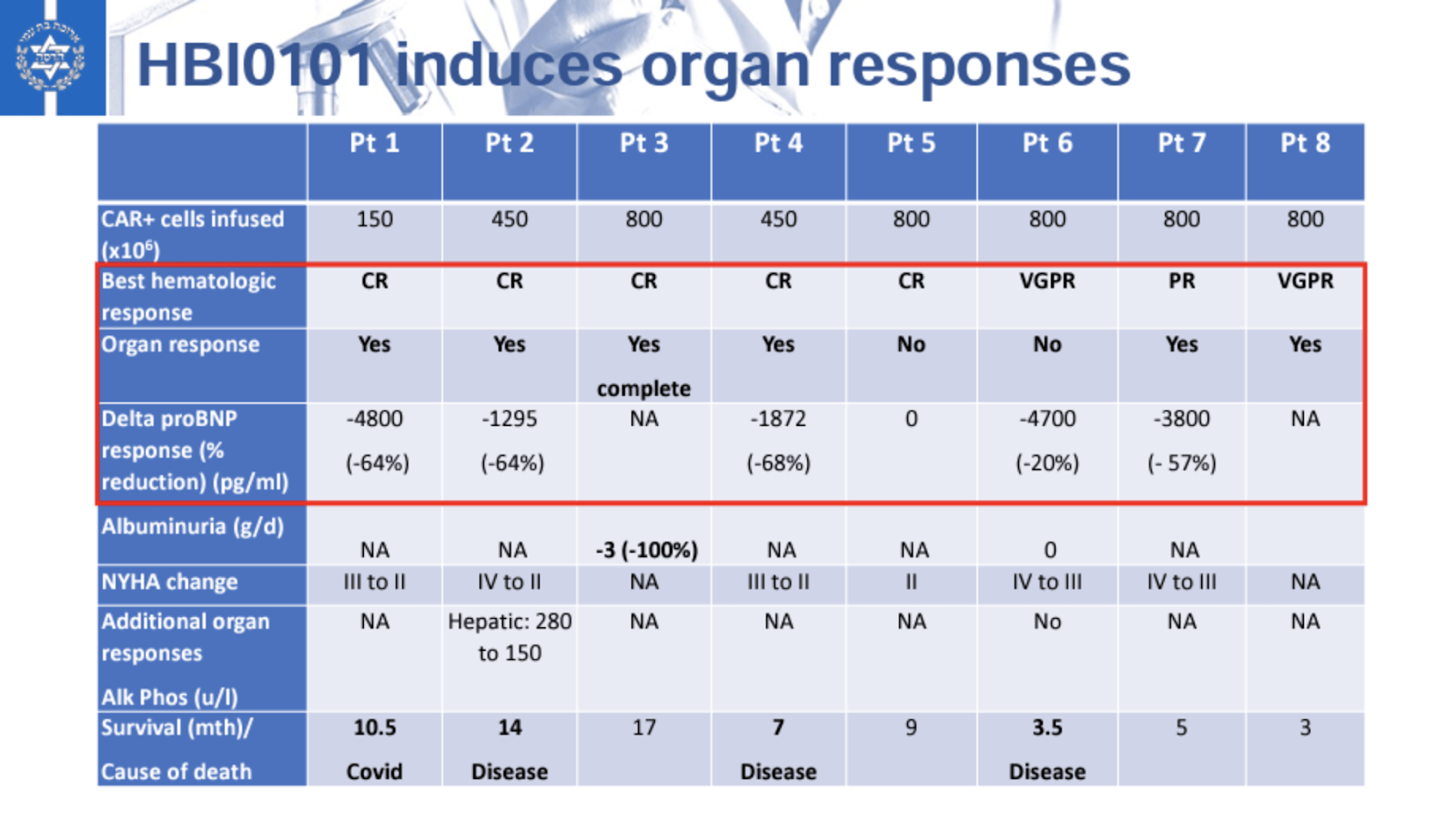

NEXICART-1 Amyloidosis Data

The NEXICART-1 trial was initiated by Hadassah researchers in 2021 and is enrolling both r/r MM and r/r ALA patients at the Hadassah Medical Center in Jerusalem, Israel. Nexcella states that NEXICART-1 enrolls ~5 patients per month, ~1 per month of which are ALA patients (though the realized ALA enrollment rate appears lower). Dr. Moshe Gatt, a researcher at Hadassah Medical Center, discussed NXC-201’s clinical profile and the NEXICART-1 study in a video interview in September 2022.

NEXICART-1’s most recent data update was given at ASGCT in May 2023 by Hadassah researcher Nathalie Asherie, PhD, which included 8 r/r ALA patients that had been treated as of February 2023, with response data up to May 2023. As shown in the full ASGCT presentation (which can be accessed via the Publications page of the Nexcella website), all patients were refractory to Darzalex, and all but two patients were refractory to 4+ lines of treatment, including four patients that had previously received autologous stem cell transplant therapy. Three of the patients had concurrent MM and one of the patients even had concurrent myelodysplastic syndrome [MDS] and had received 10 prior lines of therapy. A graphic of patients’ baseline status:

ASGCT Presentation

Notably, five of the eight patients were also refractory to belantamab (Blenrep; GSK), which is an antibody that also targets BCMA and is commonly used as a salvage therapy in ALA.

As shown in the results below, NXC-201 delivered a 100% overall hematological response rate (ORR), including five (63%) complete responses [CR] and two very good partial responses (VGPR). While NXC-201 has only reported data from eight patients so far, a 63% CR rate compares favorably to the 42% listed on Darzalex’s label, despite NXC-201 being dosed in patients that have failed a median of six prior lines of therapy. Recall that Darzalex is approved in newly-diagnosed, treatment-naive patients and was studied in combination with SoC.

ASGCT Presentation

NXC-201 also resulted in robust organ responses, defined by a reduction in proBNP, even in cardiac tissue. Cardiac involvement is the most significant predictor of mortality in ALA and, as shown below, four of the five patients with cardiac involvement had organ responses of ~60%.

{kind=link}

ASGCT Presentation

While four patients have passed away since being treated (shown in the swim chart below), it is important to note that these patients (patients 1, 2, 4, and 6) all had severe cardiac complications. All four of these patients had NYHA Stage 3 or 4 heart failure, including one (patient 4) that was treated on a compassionate use basis, indicating very dire circumstances. This journal article found that patients with cardiac involvement to the point of heart failure had a median survival of less than six months. It follows that the sole patient without cardiac involvement (patient 3) is still alive at 17 months after treatment with NXC-201.

The reduction of proBNP in cardiac tissue is an encouraging sign for patients as it signals NXC-201 is addressing the underlying pathology of ALA, and likely contributed to the fact that that four of the eight patients were still alive as of the May 2023 data cutoff.

ASGCT Presentation

In line with its data so far in MM patients, NXC-201 demonstrated a relatively mild side effect profile even in fragile r/r ALA patients. Shown below, six of the eight patients experienced CRS, which is actually below rates reported by BCMA CAR-Ts in presumably healthier MM patients, while two of the patients surprisingly experienced no CRS at all. Interestingly, in the interview with Dr. Moshe Gatt, he explained that while there were some instances of CRS, they occurred primarily in patients with congestive heart failure (CHF), in which patients it is hard to differentiate between CRS and CHF exacerbation.

The data did show that two of the eight patients experienced Grade 3 CRS (more than in 50 MM patients treated so far), which could be explained by the relative fragility of the ALA patients, or perhaps by the small sample size. Illustrating the manageability of NXC-201’s side effects, only one patient required vasopressor intervention, which is commonly used to counteract the dangerous hypotension of CRS, and only two patients required external high-flow oxygen.

While not as short as in MM patients, ALA patients treated with NXC-201 continued to report relatively short CRSs, with onset 1-2 days after treatment and 1-2 days in duration in most patients. This is NXC-201’s key advantage in both ALA and MM when it comes to improving patient outcomes, accessibility, and affordability of CAR-T therapy.

Importantly, no patients have died as a result of treatment with NXC-201 (which could be reasonably expected of a BCMA CAR-T treatment in late-stage ALA patients). Even with Darzalex, an antibody with theoretically milder side effects than CAR-T therapy, the label states that 8% of patients experienced cardiac failure and 11% of patients experienced fatal adverse reactions.

ASGCT Presentation

While early, data to date suggests a NXC-201 could have an attractive safety profile with potential to move to earlier lines of treatment in the medium-term. We look forward to the further characterization of NXC-201’s tolerability profile with the presentation of additional ALA patient data due at the IMS Annual Meeting in late September.

AL Amyloidosis Competition

Patient frailty and a lack of mechanistic understanding in ALA has led to a sparse clinical pipeline. The Nexcella slide deck summarizes the current clinical development landscape:

Nexcella Slide Deck

The two most prominent clinical-stage programs, AstraZeneca’s CAEL-101 and Prothena’s birtamimab, are antibodies designed to specifically target light chain fibrils that cause ALA. Prothena, which is better-known for its clinical-stage anti-amyloid neurodegenerative disease programs, terms birtamimab an “amyloid depleter”.

CAEL-101 is in a Phase 3 trial in Stage III patients that is expected to readout topline data in the 2H24, while Prothena is enrolling in Stage IV patients in a Phase 3 trial expected to readout in 2024. Both trials are enrolling in combination with SoC and are enrolling only newly-diagnosed, treatment-naive patients.

Prothena’s previous trial in newly-diagnosed ALA patients, VITAL, failed on its primary endpoint but was determined in a post-hoc analysis to have shown promise in extending the remaining lives of Stage IV patients. The VITAL trial, which recently had its post-hoc Stage IV subgroup analysis published in top hematology publication Blood , reported 74% survival at nine months in the treatment group compared to 49% in the placebo group. (While 74% survival at nine months may seem impressive for patients with late-stage disease, it is important to realize these patients are treatment-naive, meaning both the treatment and placebo groups are receiving SoC CyBorD for the first time.)

Illustrating the extreme unmet need in ALA, birtamimab was granted Orphan Drug Designation by both the FDA and EMA following the post-hoc analysis of VITAL, as well as Fast Track Designation in the US. Additionally, the ongoing and pivotal AFFIRM-AL trial was designed with a special protocol assessment [SPA], which allows Prothena to judge birtamimab’s results and determine statistical significance using an alpha of .10 rather than the standard .05.

Interestingly, Dr. Morie Gertz, a clinical investigator at the Mayo Clinic for the AFFIRM-AL trial, stated in an interview that it is difficult to find treatment-naive patients given how quickly Dara-CyBorD has come to be prescribed by doctors. He also mentions Mayo Stage IV patients only represent ~15% of ALA patients.

There do not seem to be many clinical-stage programs beyond newly-diagnosed patients, echoing Dr. Jahanzaib Khwaja’s comments on the r/r treatment landscape. The most established program appears to be Zentalis Pharmaceuticals’ ZN-d5, which is described as a BCL-2 inhibitor, and which is listed on CTG Labs - NCBI as enrolling in a Phase 1/2 study in r/r ALA with a mid-2025 expected completion date.

While both CAEL-101 and birtamimab are being advanced in late-stage patients, NXC-201 appears to be relatively alone in the r/r ALA setting. From a mechanistic standpoint, CAEL-101 and birtamimab seem to be competing directly with each other as antibody light chain “depleters”, which may actually work synergistically with NXC-201’s mechanism of action. NXC-201 is designed to actually remove the aberrant light chain-producing plasma cells, while CAEL-101/birtamimab works by tagging and removing circulating and deposited light chain fibrils.

Market Opportunity

Both ALA and MM present significant market opportunities if NXC-201’s differentiated efficacy and tolerability profile continues to be borne out in the clinical data.

Nexcella believes the r/r ALA alone is currently a $3 billion market. Prothena estimates there are 20,000 AL Amyloidosis patients in the US, France, Germany, and Spain, while Nexcella estimates that ~15k people annually develop ALA globally. Dr. Morie Gertz said that physicians are still becoming more aware of ALA as a diagnosis, which could grow the addressable patient population over time.

If we estimate that 10% of the 20,000 total ALA patient estimate given by Prothena would be addressable by NXC-201 as r/r patients, a $500k/dose price tag (in-line with other BCMA CAR-Ts) would yield a $1 billion revenue opportunity. Again, there are no currently-approved treatments for r/r ALA and NXC-201 is the only CAR-T in development for any stage of ALA that we are aware of.

Nexcella Slide Deck

Nexcella also may be able to charge more than ~$500k for NXC-201 if it is able to dramatically reduce extended hospital stay costs. If roughly half of the ~$1 million total cost of CAR-T treatment in MM is made up of hospital care, NXC-201 could potentially reduce total costs by hundreds of thousands of dollars, appealing to both patients and health insurers.

In MM, there are an estimated 175-225k worldwide patients, with ~36,000 expected to be diagnosed in the US in 2023. Pending additional data, NXC-201 should compare favorably to approved BCMA CAR-Ts Carvykti and Abecma, allowing it to capture a sizable position in the MM CAR-T market which Arcellx estimates as a $12 billion opportunity. Carvykti was approved in February 2022 in r/r MM and reported $117 million of sales in the 2Q23 ($468 million run rate), despite significant manufacturing headwinds.

Interestingly, Janssen is also somewhat disincentivized to invest in Carvykti’s availability and manufacturing capacity because of the success of Darzalex. Darzalex, a CD38-targeted antibody that is much cheaper to produce than Carvykti and is dosed at regular intervals. Darzalex will generate a staggering ~$10 billion of sales in 2023, though it is unclear what portion of Darzalex revenue was generated by MM, ALA, and off-label prescriptions. We think it is reasonable to estimate 7-10%, or $700 million to $1 billion of sales comes from ALA, with the majority of the remainder coming from MM.

Immix’s current market cap of ~$57 million (as of close on 9/15/23), accounting for the additional 3.2 million shares and 1.9 million pre-funded warrants from the August private placement, does not reflect NXC-201’s prospects in the well-established MM and highly-underserved ALA markets.

Recent Momentum and Catalysts

Building on its promising clinical data, Nexcella has made considerable and rapid progress since in-licensing NXC-201 just nine months ago that appears to be going completely unnoticed by the market. The company is clearly focused on moving NXC-201 into the US and getting it on the radars of researchers, KOLs, and regulators. We think the developments outlined below and those expected in the near future represent significant progress that will eventually result in a significant increase in investor interest and could eventually support Nexcella’s aspirations to be independently financed, either through IPO or strategic collaboration.

Impressive Leadership

Beginning just four months ago, Nexcella has already constructed an impressive Board of Directors and Scientific Advisory Board, including an impressive first two additions to the SAB: Dr. Heather Landau, the Director of the Amyloidosis Program at Memorial Sloan Kettering Cancer Center, one of the global leaders in cell-based therapy; and Dr. Suzanne Lentzsch, Director of Multiple Myeloma and Amyloidosis at Columbia University and New York Presbyterian Hospital. The Board of Directors has also already grown to five members and is led by the former CEO of Pfizer, Henry McKinnell.

The company has also already added a Chief Medical Officer with decades of experience in cell therapy, as well as Dr. Gerard Bauer, who is listed in the Nexcella slide deck as the “former” Director of Good Manufacturing Practice at UC Davis, but is still listed on the school’s website in that role, and who designed and directed a state-of-the-art GMP laboratory at Washington University before transferring to UC Davis.

Nexcella Slide Deck

Dr. Ilya Rachman and Gabe Morris, who have headed Immix since before its IPO and who deserve credit for constructing a strong leadership team, are listed as CEO and President of Nexcella. It is conceivable that the team may look to add a CEO or President with more direct experience in cell therapies in the coming months.

We think the management team, especially the two recently added Scientific Advisors, make it very likely that almost all major ALA practitioners (and many MM practitioners) are either becoming aware or are already aware of NXC-201. ALA, as a rare disease, has a tightly-knit community of practitioners and KOLs, in Scientific Advisor Dr. Heather Landau, which could aid in efficient US trial site enrollment and investigator-initiated clinical trials at large amyloidosis medical centers. We also believe Dr. Landau’s spot on the SAB makes it feasible that Memorial Sloan Kettering would be one of the early clinical trial sites for NXC-201.

Nexcella’s Board and SAB in just a matter of months has risen to a caliber usually seen at much larger biopharma companies, and the willingness of these Board and SAB members to join Nexcella is a validation of the unique clinical opportunity.

US Trial Expansion

Nexcella has also made progress in onshoring NXC-201 to the US, announcing the completion of a pre-IND meeting with the FDA in late June. We expect IND acceptance by the FDA sometime in the next 3 months and activation of the first US clinical trial site in the 4Q23, which should at least double enrollment by the 1H24 to ~10 patients per month by mid-2024.

Additionally, in August, NXC-201 was awarded ODD for MM. It is safe to assume that Nexcella is also pursuing ODD in ALA, a truly orphan designation, which we expect will be granted sometime in the next couple months, unless the FDA is waiting for a specific number of patients in ALA. The ODD in MM shows the FDA’s level of engagement with Nexcella’s story, and we believe that if Prothena’s birtamimab was awarded ODD in ALA, NXC-201 should also be seen favorably.

Private Placement and (Modest) Insider Buying

In August, Immix announced a $10 million private placement to an individual investor named Yekaterina (Kate) Chudnovsky , a lawyer who is described as a frequent investor in clinical cancer research and is on the Board of the GI Research Foundation in Chicago. She was awarded a seat on the Immix (not Nexcella) Board, likely as a condition of the private placement. The deal included stock and pre-funded warrants resulting in a total of ~32% dilution, which is not great for existing investors, but will give Immix a ~$22 million cash balance that should provide sufficient runway to advance NXC-201 and increase the share price significantly higher before raising additional capital.

There have also been a number of insider purchases by Immix Board members in recent weeks. Since September 5th, Immix Directors Helen Adams, Jane Buchan, Dr. Magda Marquet, and Carey Ng have made eight purchases ranging from $20k to over $300k.

While it is nice that management is signaling confidence in the company and at least one individual investor taking notice, Immix and Nexcella will need to get on the radars of institutional investors in the next 6-12 months to support the development of NXC-201.

Investor Engagement

Encouragingly to that end, Nexcella announced that it is presenting at the Bank of America 2023 Healthcare Trailblazers Private Company Conference in late October. The conference is designed to introduce companies to institutional investors and potential strategic pharmaceutical partners. The company also participated in the HC Wainwright Global Investment Conference last week, which may or may not move the needle. We expect that if Nexcella is on BofA’s radar, Immix will be invited to their global healthcare conference next year, and that similar institutional conferences and investor days may extend an invite to Immix in the coming months.

Data Readouts

The company announced that it will present data from additional ALA patients at the International Myeloma Society IMS) Annual Meeting taking place in Athens, Greece September 27-30th. Dr. Polina Stepansky, the Hadassah Medical Center researcher whose lab designed NXC-201, is set to present the additional data. It does not appear from the wording of the press release that Nexcella will be reporting additional MM data.

The most up-to-date data that Nexcella has shared is as of a February 2023 cutoff date, meaning the data presented at IMS could include up to an additional 4-5 ALA patients (based on the company's enrollment guidance of ~1 patient per month), depending on the new data cutoff date.

As for additional MM data, it is a bit odd that Nexcella would not present updated data at an international myeloma conference. It is possible the company is looking for the most impactful way to release additional data in MM, which may be in the form of a scientific publication, among other possibilities.

Going forward, we would conservatively expect that Nexcella will have treated 12 ALA patients by the end of 2023, at which point it will be initiating enrollment in the US. We would expect enrollment of ALA patients to increase gradually to 2-3 patients per month in 2024, which would put Nexcella at 24-40 patients by the end of 2024. The company has guided 30-40 patients being sufficient for an accelerated BLA submission, which the company has estimated for the 1H25, which seems to be in an achievable ballpark. The company also believes it will be able to file a BLA in MM after treating ~100 patients, which could fall along the same 1H25 timeline.

Takeaway

The continued illustration of NXC-201’s strong tolerability profile in both MM and ALA is the key driver of Nexcella’s upside potential. Nexcella’s development to this point has been rapid, and continued positive clinical readouts as well as an expansion into the US in the coming months should put the company on the map with clinicians, researchers, and investors alike.

Valuation and Price Target

Based on the clinical data for NXC-201 to date and the progress Nexcella has made over the past several months, we believe Immix is significantly undervalued at its current market capitalization of approximately $57 million.

Immix is still trading in the same $2-3/share range that it was trading in for all of 2022 (though its market cap is higher as a result of dilution), despite the in-licensing of a program that we believe most investors would regard as more differentiated, and certainly nearer-term, than its IMX-110 program. The low-profile in-licensing and on-the-fly buildout of Nexcella have been unorthodox, certainly compared to the normal private funding-to-IPO route for clinical stage biotechs but have also provided a unique situation in which a fairly well-defined and potentially differentiated mid-stage cell therapy is flying under the radar.

At a certain point, when US clinical sites are enrolling, clinical data continues to readout, and the prospects of a BLA filing for NXC-201 in 2025 draw closer, it will become impossible for the market to ignore the Nexcella story.

We believe Immix, based on the value being created at Nexcella (ignoring IMX-110), should at the least trade in-line with CAR-T biotech Gracell Biotechnologies at ~$215 million of market capitalization, which would represent 277% upside. Gracell has most of its clinical operations in China but is conducting a Phase 1 of its rapid expansion CAR-T in r/r MM in the US.

As another benchmark, Caelum was acquired by AstraZeneca in 2021 for $150 million up front and $350 million of regulatory and commercial milestones. The $150 million valuation would represent 163% upside for Immix, while the total $500 million consideration would be 777% of upside.

On the higher end, Arcellx, which has one clinical-stage program targeting BCMA in MM, trades at ~$1.6 billion, and traded as high as $2 billion prior to the clinical hold on CART-ddBCMA. Arcellx came public at a $583 million market cap in January 2022 after reporting a 100% ORR in a 19-patient Phase 1 trial, an example of the excitement that can be generated in the CAR-T space in the right circumstances.

While Arcellx’s current valuation is underpinned by its partnership with Kite/Gilead, we think $1+ billion of market capitalization is achievable as a best case scenario for Immix/Nexcella in the longer-term, a valuation that would likely require a strategic partnership from a big pharma. In the nearer-term, we think Kite’s $325 million up front payment to Arcellx could be a reasonable guidepost for Nexcella once it expands to the US and reports additional patients, which would represent 470% upside from current levels and a ~$15 share price.

Taking into account each of these data points, we think ~$300 million market capitalization is achievable at some point in 2024 as all of the pieces start to come together, assuming continued positive data, which would represent $13.96 per share (420%) upside.

Risks

As a clinical-stage nanocap biotech, Immix also comes with significant risk, some of the most important of which are listed below:

-

Very slow enrollment (4-5 patients/month) at a single trial site in Israel.

-

Only 58 patients total treated to date, including only 8 patients in the important r/r ALA

-

A diversion from the currently strong tolerability profile of NXC-201 in future data could significantly impact its value proposition.

-

Immix/Nexcella have only ~$22 million in cash with multiple clinical trials ongoing. They will need to raise additional capital to support these programs, which could become more difficult depending on clinical data and/or market conditions.

-

The management team of Immix is juggling two separate biotechnology entities, and without specific knowledge in the cell therapy space. They will likely need to add additional executives to Nexcella.

-

As a small biotech, Nexcella may struggle to hit its guided timelines, including IND acceptance in the 4Q23 and a potential BLA in the 1H25.

-

CAR-T therapies have experienced significant manufacturing challenges leading to long wait times for patients, which could impact enrollment rates even when NXC-201 moves to the US.

-

A group at the University of Barcelona published a case report treating an ALA patient with a BCMA-targeted CAR-T therapy in 2021, which could compete with NXC-201.

-

The 30-40 estimated patient requirement for a BLA in ALA may be low. Prothena is enrolling 150 patients (100 treated and 50 control) in its ongoing AFFIRM-AL trial.

Conclusion

In summary, we believe the market has yet to recognize Immix Biopharma's transformation via the in-licensing of NXC-201 and formation of Nexcella. Immix has rapidly assembled an impressive leadership team at Nexcella and made strong progress toward advancing NXC-201 in the well-established MM and severely underserved AL amyloidosis markets. NXC-201 data so far presents an exciting combination of efficacy and tolerability that could help to further unlock the growing CAR-T in MM as well as be the first potentially disease-modifying treatment in ALA.

We believe Immix is a strong buy and assign a ~$14/share 2024 price target. We look forward to additional ALA data due at the end of September, which should be the first step in an eventful 2H23 for the company.

For further details see:

Immix Biopharma: A Mid-To-Late Stage CAR-T Biotech Quietly Gaining Momentum