CA - Imperial Oil Not As Cheaply Valued As It Appears

2023-09-12 10:10:50 ET

Summary

- Imperial Oil has outperformed the S&P 500 and Energy Select Sector SPDR Fund ETF this year with a 25% rally.

- The stock is trading at a forward price-to-earnings ratio of only 10.5.

- However, the shift towards renewable energy poses a significant long-term risk to Imperial Oil and the oil industry as a whole.

Imperial Oil ( IMO ) has rallied 25% this year and thus it has outperformed the S&P 500 (+17%) and the Energy Select Sector SPDR Fund ETF ( XLE ), which has gained 9%, by a wide margin. Despite its steep rally, to a new 15-year high, Imperial Oil is trading at a forward price-to-earnings ratio of onl y 10.5x . This may lead some investors to think that the stock remains cheaply valued. However, the Canadian oil producer is not attractively valued from a long-term perspective.

Business overview

Imperial Oil is an integrated oil and gas company, which is based in Canada. It is focused on the exploration and production of oil and gas but it is more diversified than pure upstream companies, as it also has refineries and a chemical segment. Exxon Mobil ( XOM ) owns 69.6% of Imperial Oil and hence the latter benefits from the unparalleled expertise of its major shareholder. It is worth noting that most of the technical procedures applied in the oil industry by all companies have been written by Exxon Mobil.

Imperial Oil also benefits from the highly prolific areas of Canada. Canada has the third-highest level of oil reserves in the world, after only Saudi Arabia and Venezuela. As a result, Imperial Oil has promising growth prospects ahead. In the latest quarter, the company posted a 12% decrease in its output over the prior year’s period but only due to scheduled maintenance activity. Management still expects to grow production in the full year thanks to strong production growth at Kearl.

Moreover, Imperial Oil enjoys another strong tailwind in its business, namely the war in Ukraine. Due to the invasion of Russia in Ukraine, the U.S. and European Union imposed strict sanctions on Russia early last year. As a result, the prices of oil and gas surged to 13-year highs last year.

The price of natural gas has plunged this year due to an exceptionally warm winter in both the U.S. and Europe, which drove global inventories to high levels. As Russia has greatly increased its oil sales to China, India and some other countries, it would be reasonable to expect the price of oil to plunge this year, just like the price of natural gas. However, OPEC and Russia have implemented several rounds of production cuts and thus they have provided great support to the price of oil. Consequently, the price of oil has remained above average this year.

The benefit from excessive oil prices is evident in the results of Imperial Oil. The company more than tripled its earnings per share last year thanks to the 13-year high prices of oil and gas, from $2.74 in 2021 to a 10-year high of $8.36 in 2022. Due to the aforementioned plunge of gas prices and a correction of oil prices this year, Imperial Oil has posted a 46% decrease in its earnings in the first half of the year. Analysts expect Imperial Oil to post a 34% decrease in its earnings per share this year, from $8.36 to $5.50. While such a decrease may seem steep on the surface, the company is on track to post its second-best earnings per share in 14 years. Overall, while the price of oil has moderated this year, it is still elevated and hence it results in excessive earnings of Imperial Oil.

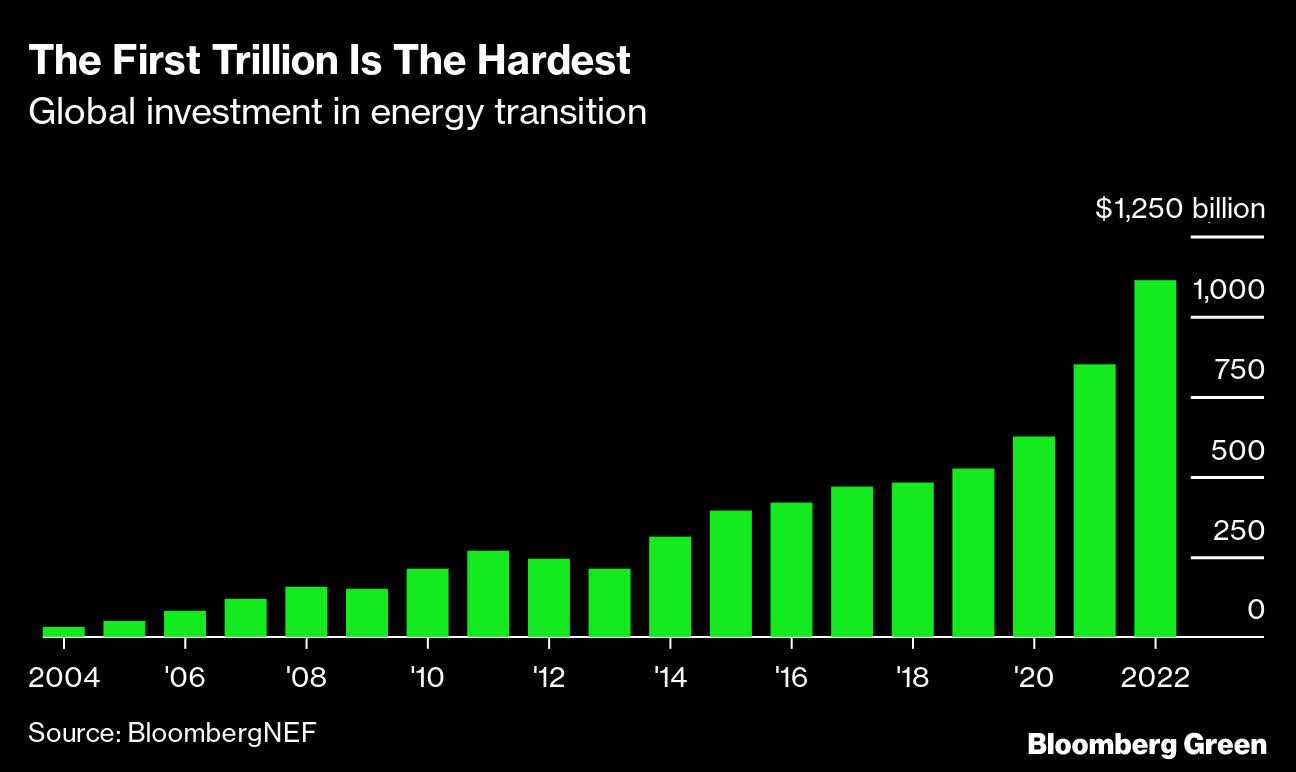

On the other hand, Imperial Oil is likely to face a significant headwind in the upcoming years, namely the shift of the entire world from fossil fuels to renewable energy sources. The coronavirus crisis and the fierce energy crisis, which showed up last year as a result of the war in Ukraine, have greatly accelerated the shift from oil products to solar and wind power. To be sure, 2022 was the first year in history in which the global investment in renewable energy projects ($1.1 trillion) equaled the global investment in fossil fuels.

{kind=link}

Source: TIME magazine

As shown in the above chart, the global investment in green energy has accelerated at an unprecedented pace over the last three years. Given also the devastating effect of the energy crisis on millions of households worldwide, most governments will almost certainly continue to diversify away from fossil fuels at full throttle in the upcoming years in order to protect themselves against a potential future energy crisis.

When all the green energy projects that are being developed right now begin to generate energy, in 2-4 years, they are likely to have an impact on the price of oil. This is a material risk for oil and gas producers, including Imperial Oil. The company is well managed, with management doing its best in the factors it can control, but it is inevitably vulnerable to the threat from the boom of green energy projects.

Valuation

Despite its 25% rally this year, to a new 15-year high, Imperial Oil still has a low price-to-earnings ratio. The stock is trading at a forward price-to-earnings ratio of 10.5x, which is less than half of the price-to-earnings rati o of 23.5x of the S&P 500.

However, investors should be aware that oil stocks almost always trade at much lower earnings multiples than the broad market due to their dramatic cyclicality. It is also important to note that the price of oil has almost certainly passed its peak, which materialized shortly after the onset of the Ukrainian crisis last year, and is likely to face a downturn whenever the numerous green energy projects begin to take their toll on the global consumption of oil. Given the 15-year high stock price of Imperial Oil and the high cyclicality of its business, I don't see the stock as attractive from a long-term point of view.

Dividend

Due to its steep rally this year, Imperial Oil is currently offering a nearly 4-year low dividend yield of 2.4% .

Given the solid payout ratio of 21% , the dividend has a wide margin of safety. It is also worth noting that Imperial Oil has grown its dividend by 11.5% per year on average over the last decade, much faster than the 1.4% median growth rate of the energy sector during this period. Moreover, Imperial Oil has taken advantage of its excessive free cash flows in the last two years and thus it has eliminated its net interest expense.

Given all these facts, the dividend of Imperial Oil has a wide margin of safety. In fact, the company can continue raising its dividend meaningfully for years. On the other hand, the nearly 4-year low dividend yield of 2.4% do not justify an investment in the stock for its dividend. In other words, the above mentioned risk of the stock outweighs the benefit that comes from reliable dividend growth.

Upside risk

Experience has shown that the oil industry is characterized by wild cycles. A rally of the oil price to a multi-year high, just like the one experienced last year, is usually followed by a collapse of the oil price after a few years. Therefore, the odds favor a plunge of the oil price from its current level in the upcoming years, particularly given the expected impact of numerous clean energy projects.

On the other hand, nothing is written in stone. If OPEC and Russia execute even deeper production cuts to support the price of oil, the latter may remain above average for much longer than would normally be expected. In such a case, Imperial Oil will continue thriving for years. Nevertheless, the aggressive strategy of OPEC and Russia is likely to approach its limits at some point. The cartel cannot keep reducing its output infinitely because most of the lost barrels of the cartel are replaced by increased output of the U.S. and Canada and hence the cartel is losing market share every time it implements a new production cut. To cut a long story short, the short-term path of oil prices is always unpredictable but experience has always shown a plunge of oil prices after an extended period of above average prices.

Final thoughts

Thanks to elevated oil prices, Imperial Oil is likely to continue thriving in the short run. In addition, the company is doing its best in the factors of its business that it can control. However, all the oil companies are vulnerable to the dramatic swings of the price of oil. Whenever the numerous green energy projects that are in their development phase come online, they are likely to weigh heavily on the price of oil. Therefore, Imperial Oil is not as cheap as it seems from a long-term point of view.

For further details see:

Imperial Oil Not As Cheaply Valued As It Appears