CA - Imperial Oil Stock: In The Buy Zone (Rating Upgrade)

2023-11-13 08:00:00 ET

Summary

- Imperial Oil's Q3 results showed lower YoY results and margins, leading to a bearish trend in trading.

- The company benefits from cost-cutting measures, a large reserve base, and a commitment to reducing share count.

- Notable initiatives include the introduction of autonomous trucks, waste heat recovery at Kearl, and entry into the biodiesel market.

- We rate IMO a buy at current levels with as much as 30% upside.

Introduction

In this article, we will review Imperial Oil Limited's ( IMO ) third quarter earnings and determine where they fit in the Pantheon of heavy oil companies. IMO reported on Oct, 27th, and investors immediately bolted for the door. It's had up and down days since, with a big move toward the exits just yesterday, thanks to lower YoY results and margins.

{kind=link}

Against that backdrop, we will plow through the latest report . Recent trading has trended toward the bearish side, with red lines outnumbering green lines 2:1. The stock is still well above support at $49.20 and appears to be approaching the 200-day SMA.

The analyst cadre is modestly constructive on IMO with an Overweight rating and price targets ranging from $57 to $79. We should note the median is $61, inferring the bulk of the 18 seagulls following the stock see limited upside.

In our last article in mid-Feb, 2023, we passed on it at $52, but time's moved on and we may come to a different conclusion this time around.

The thesis for IMO

Upstream IMO is in the bitumen business, clawing up huge hunks of sandy goo at Kearl, injecting steam and chemicals into SAGD drainage wells at Cold Lake, and upgrading syncrude at Fort McMurray through the Suncor ( SU )-operated JV. Altogether IMO produced 423K BOPD from all sources in Q-3, 2023.

Downstream, IMO is also Canada's largest refiner and has a retail arm with over 2,400 Esso and Mobil-branded convenience and fueling stations across the country. It also has a chemicals business producing petroleum-based intermediates - HDPE, with output targeted at durable plastic resins. Finally, it is entering the biodiesel market with a conversion of some existing assets at the Strathcona refinery to produce 20KB/Day, starting in 2025.

{kind=link}

The company has been benefiting in recent quarters from higher prices for products and cost-cutting measures that have reduced opex by 20% year over year. One initiative that has the potential to significantly control costs at Kearl, the company's primary source of revenue is the introduction of autonomous trucks. Brad Corson, CEO comments :

We have been working on this now for several years, and to finally complete all of the conversion of the trucks allows us to really make a step change and all of those kind of beneficiary components that have been driving us. I mean, things around truck productivity, things around unit operating costs.

The company also benefits from a large 2P reserve base that allows for many years of steady production at current extraction rates. This stability is at variance with many shale operators with only 6-8 years of drillable inventory.

Finally, as with many other Canadian companies we cover, IMO is committed to reducing their share count, theoretically enhancing shareholder value at some point. Over the past year IMO's float - what isn't owned by Exxon Mobil ( XOM ) at ~69% - has been reduced from 626 mm to 579 mm, or about 7.5 %.

Q3 2023 and guidance CAD

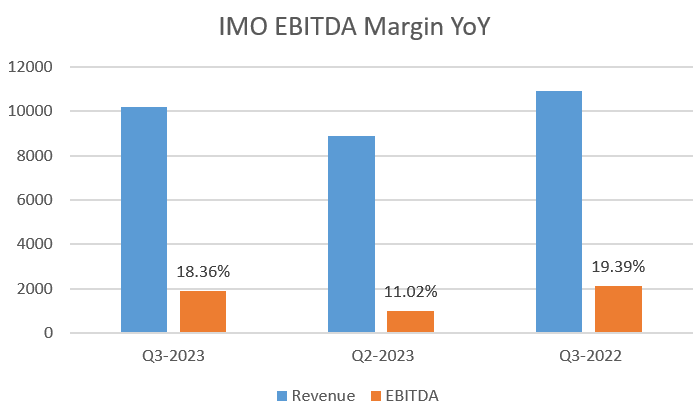

IMO reported net income of $1.601 billion, down about $400 million from the third quarter of 2022. This reflected the impact of excluding the $200 million impact of XTO Canada sale in the prior year. The decrease was primarily driven by lower refining margins in their Downstream business.

Sequentially, the third quarter net income of $1.601 billion was up over $900 million from the second quarter, reflecting stronger realizations and improved volumes, along with the absence of significant second quarter turnaround activity in both the Upstream and Downstream.

The Downstream net income was $586 million, up $336 million from the second quarter, reflecting the absence of planned turnaround activities at the Strathcona refinery and stronger refinery margins. Finally, the Chemicals business generated net income of $23 million, down $48 million from the second quarter, reflecting weaker margins as well as impacts from the gas cracker turnaround that commenced in September.

IMO ended the quarter with more than $2.7 billion of cash on hand and generated almost $2.4 billion in cash flows from operating activities. This was an improvement of almost $1.5 billion over the second quarter, reflecting stronger earnings and favorable working capital impacts. Excluding favorable working capital impacts of $413 million, cash flow from operating activities for the third quarter was $1.946 billion, up about $800 million from the second quarter. Long-term debt is ~$3.0 bn.

Capex totaled $387 million in the third quarter, down slightly from $392 million in the third quarter of 2022, but remaining in line with previously announced full-year guidance of $1.7 billion.

Notable initiatives from the company documented in the Q3 report include higher production that was driven primarily by strong performance at Kearl and the absence of the second quarter turnaround work at both Kearl and Sync crude. This was partly offset by planned maintenance at Cold Lake and the commencement of Syncrude's Hydro treater turnaround in late September.

Kearl's production in the third quarter averaged 295,000 barrels per day gross, which was up 78,000 barrels per day versus the second quarter and up 24,000 barrels per day from the third quarter of last year. Kearl is positioned to meet full-year guidance of 265,000 to 275,000 barrels per day. Unit cash operating costs in the quarter were just over USD $20 per barrel, a decrease of over USD $7 per barrel versus the second quarter due primarily to the absence of the planned turnaround and the higher volumes.

Year-to-date, cash operating costs at Kearl are just below US $24 per barrel, which is about USD 5.75 per barrel lower than the same period last year.

During the third quarter, IMO also completed the Autonomous Hall Program with all 81 of their caterpillar 797 heavy haul trucks now fully converted to autonomous operation.

IMO also started up the sixth and final boiler flue gas waste heat recovery unit at Kearl. This technology recovers waste heat from a boiler's exhaust to preheat process water, resulting in less steam usage and lower greenhouse gas emissions, and is one of the key initiatives underpinning are 30% greenhouse gas intensity reduction target by 2030. The six units are expected to eliminate a total of 220,000 tons of CO2 per year and also capture significant cost savings of approximately $40 million per year.

At Cold Lake, production for the second quarter averaged 128,000 barrels per day, which was 4,000 barrels per day lower than the second quarter, and 22,000 barrels per day lower than the third quarter of last year. The lower third quarter production was primarily the result of steam cycle timing and the planned turnaround at the NB plan, which was completed last month.

Maintenance work appears to be finished and expectations are for Cold Lake to trend higher and deliver full year production in the range of 135,000 to 140,000 barrels per day.

IMO's share of Syncrude production for the quarter averaged, 75,000 barrels per day, which was up 9000 barrels per day versus the second quarter and up 13,000 barrels per day versus the third quarter of 2022. Higher production in the third quarter was primarily due to the timing of the annual planned coker turnarounds. In 2022, Syncrude's coker turnaround began in the third quarter, and in 2023, work was primarily completed in the second quarter. In late September, work began on Syncrude's planned hydro treater turnaround, which is expected to be complete by mid-November.

Downstream in the third quarter, IMO refined an average of 416,000 barrels per day, which was up 28,000 barrels a day versus the second quarter, and down 10,000 barrels per day versus the third quarter of 2022, reflecting a utilization of 96%. Year-to-date utilization of the refinery sits at 94%.

Petroleum product sales in the quarter were 478,000 barrels per day, which is up 3000 barrels per day versus the second quarter and down 6000 barrels per day versus the third quarter of 2022. The company continues to see gasoline demand around 90% to 95% of historical levels and jet at about 110% of historical levels. On diesel, demand in the quarter was between 80% to 85% of normal.

Crack spreads and diesel margins strengthened quarter-over-quarter and remained on the high end of the five-year band. Motor gasoline cracks softened toward the end of the quarter, and summer driving season ended with cracks now sitting around the low end of the five-year band.

In the third quarter of 2023, IMO paid $292 million in dividends. IMO also completed their most recent accelerated NCIB program on October 19th, returning a total of $2.3 billion to shareholders over the last four months. The company also intends to launch a substantial issuer bid returning up to an additional $1.5 billion to shareholders in the fourth quarter of 2023. Lastly, this morning, IMO announced a fourth quarter dividend of $0.50 per share, consistent with the third quarter dividend.

A few possible catalysts for IMO

IMO's focus on cost control could start bearing fruit in coming quarters. Notably, the variance between Q2 and Q3 was driven by a turnaround and higher volumes. The implementation of autonomous hauling at Kearl should also promote higher margins here. The waste heat recovery project at Kearl should also show contributions to improved margins as it is implemented.

{kind=link}

Longer term, the biodiesel and sustainable aviation fuels initiative should also make significant contributions to the bottom line.

Finally, as we have mentioned a number of times before, hanging out there is the multi-million barrel line fill and daily shipping requirement of the Transmountain line-TMX.

Risks

The volatility of WTI and the WCS discount represent the greatest near-term risks for the company, as noted in the call .

On the refining end, strong crack spreads for distillates should be beneficial, but this may be offset by lower crack spreads for gasoline in the next couple of quarters.

Your takeaway

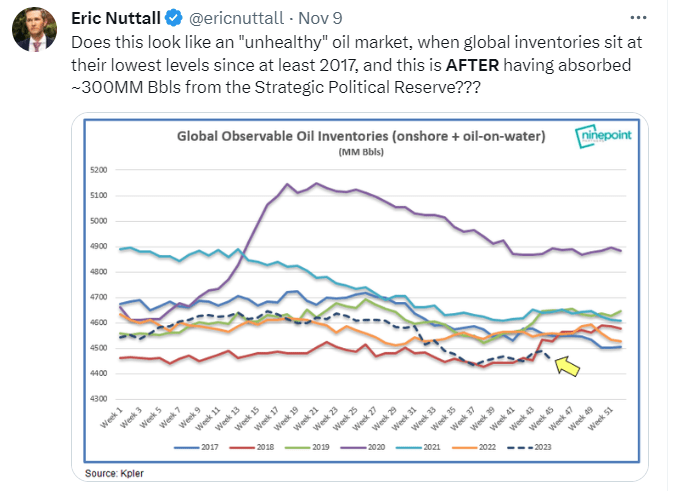

IMO is trading at an attractive multiple of 3.75X EV/EBITDA and $70K per flowing barrel. This is competitive with other companies participating in this space. The current softness in oil prices has created an opportunity that will quickly reverse when a stronger buy signal is sent to the oil markets. That can come at any time, as global inventories remain tight, as this X post from Canadian oil soothsayer Eric Nuttall points out :

{kind=link}

I think IMO has a place in investor portfolios that have a modest risk tolerance. The key risks as noted revolve around oil prices, and investors should be prepared to live with fluctuations in value as a result. The payoff, of course, is increasing shareholder returns as we go deeper into the commodity cycle.

For further details see:

Imperial Oil Stock: In The Buy Zone (Rating Upgrade)