WW - In The Murky MLM Space Medifast Might Actually Hold Some Promise

2023-07-21 14:28:53 ET

Summary

- Medifast, a health and wellness company, has seen its stock price decline by 76% since 2021, despite its Optavia platform helping over 2 million customers with weight loss.

- The company's earning power value (EPV) and adjusted asset value (AV) suggest the stock is undervalued, with potential for significant returns for value-oriented investors.

- However, risks include competitive entry, potential malinvestment, MLM regulations and prejudice, and health and sustainability concerns around Medifast’s products.

- Medifast is cheap relative to their MLM peers despite avoiding many of the issues which drag the reputations of other MLM firms.

- We estimate that the upside potential is approximately 69%.

OVERVIEW OF THE BUSINESS

Obesity poses a range of dangerous health risks, both physical and psychological. Physically, obesity significantly increases the likelihood of developing chronic conditions such as cardiovascular disease, diabetes, cancers, and disorders. It places a burden on vital organs and leads to reduced mobility, resulting in a diminished quality of life. Moreover, obesity takes a toll on mental health, contributing to depression, anxiety, and low self-esteem. Not only is the widespread epidemic a major problem for the health and finances of obese individuals, but it is also a $173 billion financial strain on the U.S. healthcare system. In the U.S., more than 2 in 5 adults are classified as obese, and nearly 76% of adults are overweight. This is where Optavia steps into the picture. Medifast, Inc. ( MED ) is a MLM health and wellness company behind the growing coach-driven community known as Optavia. The goal with the Optavia platform is to change the lifestyle of those who are overweight by developing small and healthy micro-habits, such as dieting, better sleep, proper hydration, etc.

To date, the Optavia network has more than 58,000 coaches, and it has helped more than 2 million customers. Through the use of coaches as sales representatives, Medifast sells directly to consumers an interchangeable range of meal replacement plans, kits, and products with the aim of helping customers lose weight. Scientifically speaking, their products work, and there is nothing groundbreaking about them. The efficacy of their products lies in the simple principle of creating a caloric deficit through portion control, helping customers consume fewer calories than they burn. These meal plans are customizable, allowing customers to personalize their selections. Optavia’s products include plans for weight loss, weight maintenance, and plans for people with medical conditions, such as diabetes. Each kit provides a month's supply of lean protein, low-carb meals, and snacks. With prices ranging from $395 to $442 per month, Medifast's kits are affordable compared to the estimated monthly food plan expenditure of the average one-person adult household, which falls within the $300 to $420 range according to the U.S. Department of Agriculture .

For the majority of Optavia coaches, their role serves to supplement their income. Their compensation is primarily tied to client purchases made directly through the Optavia website. Coaches earn a standard commission of 15%, but their commission can increase up to 31% based on factors such as ongoing education with Optavia and sales volume. Many are passionate about Optavia, as more than 90% of active coaches have been in their clients’ shoes and used the meal kits themselves. As a result, coaches can share their personal success stories with their clients, and this energy assists with keeping the client motivated, which is a significant chunk of the battle when losing weight. Having someone to hold clients accountable increases a client’s probability of success. Later down the road, successful clients are offered the chance to join on as a coach.

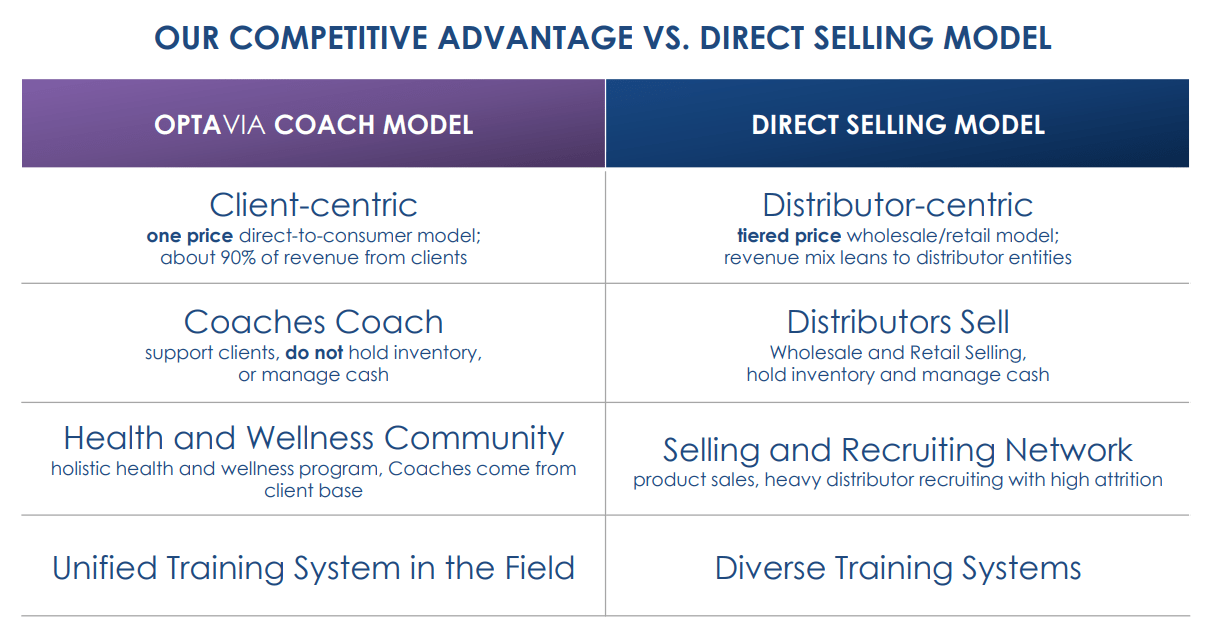

Despite being categorized as a multi-level marketing ((MLM)) firm, Medifast upholds better practices compared to many other MLM companies (refer to Figure 1). For instance, Optavia coaches do not purchase or hold inventory, receive discounts, or set prices on products, which are all common controversial practices in typical MLM models. Such practices often lead to predatory behavior among associates. In contrast, customers purchase products directly from Optavia's website, with coaches serving to support the client.

{kind=link}

Scrutiny of the MLM model often centers around whether a company prioritizes recruitment over product sales. The focus on recruitment can raise concerns over potential pyramid schemes. While the recruitment of coaches is an important aspect for Medifast, as they serve as sales agents and help keep advertising costs low, the company asserts that its growth is not reliant on recruiting many distributors and burdening them with inventory for sale. However, the recruitment of new coaches remains a key metric when assessing Optavia's future growth potential. The number of active and earning coaches has experienced remarkable growth, increasing by 352% from 13,000 in 2017 to 58,700 in 2023. Moreover, during the same period, revenue per coach has shown a notable increase of approximately 33%.

SETTING THE SCENE

Despite experiencing rapid growth in the last few years, Medifast has encountered challenges with customer retention and acquisition since 2022, likely stemming from the inflationary environment. As a result of this problem, the company has had issues with retaining coaches as well. There is a silver lining, however. Customer retention and repurchase rates have recovered back to historical levels. Based on past transcripts, I presume that this is around 77% relative to the 62% retention rate in 2022.

Even still, Q1 2023 revenue has fallen 16.4% from $417.60 million the prior year. Management has attempted to downplay these issues by highlighting the quarter-over-quarter revenue and coach productivity improvements in Q1 2023 compared to the past two quarters. However, it is important to consider the seasonal nature of sales in the health and fitness industry. Typically, there is a surge in sales and activity in Q1 due to New Year's Resolutions, followed by a decline in subsequent quarters as more people fail their resolutions. So of course, Medifast had better results relative to Q3 and Q4 of last year. But if the Q1 2023 results are what sets the trend for the upcoming year, decreased YoY performance in Q1 is not an encouraging sign for the business in the short-term.

Furthermore, there are increasing concerns regarding the potential impact of GLP-1 drugs on Medifast's future sales. Although FDA-approved weight loss medications have been available for some time, GLP-1 drugs are recognized as highly effective options in the market. However, it is crucial to acknowledge that there has always been a consistent market for individuals seeking pill-based solutions rather than opting for dietary changes. Therefore, it is my belief, in part, that the individuals who are enthusiastic about these drugs are not necessarily the same individuals inclined to stick to a consistent diet.

Moreover, despite the significance attributed to GLP-1 drugs, it is important to note that they have yet to achieve widespread adoption. Their costs remain high in the short term, and uncertainties persist regarding insurance coverage for these expenses. For instance, drugs like Wegovy and Ozempic can exceed $1,000 per month in cost. Moreover, these drugs are often perceived as temporary fixes, and the consequence of their long-term use remains questionable. According to research by Prime Therapeutics , a majority of GLP-1 drug users discontinue their usage within a year due to some combination of affordability and side effects.

In addition, a survey conducted by Medifast revealed that customers overwhelmingly favor a lifestyle and behavioral change approach (3:1) for managing their weight, rather than relying on drug therapy. However, it is essential to approach these survey results with a level of skepticism, as market research can sometimes be influenced by the pre-existing beliefs and biases of the management team.

It’s also worth noting that the market has a strong prejudice against MLM firms, and MLM companies today trade at substantial discounts relative to non-MLM firms. Some for good reason. For many, there is simply no middle ground between good and bad. Despite the Optavia Coaching Model’s better practices relative to other MLM firms, they currently suffer from the effects of the MLM discount.

Since reaching their all-time high in May 2021, MED's stock price has experienced a significant decline of over 76%, leading to a market capitalization of $855 million at the time of this writing (equivalent to $79 per share). In the following analysis, I want to analyze the company’s earning power value ((EPV)) and adjusted asset value ((AV)) to see if this fall from grace is warranted. From there, we will look at the issue of growth, barriers to entry, and competitive entry, and we will attempt to arrive at a fair valuation for Medifast after accounting for several risks.

MEDIFAST’S EARNING POWER VALUE

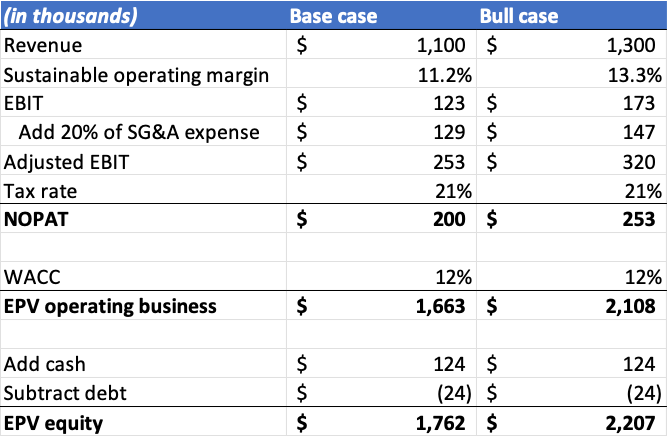

In our earning power calculation, I have considered both a base case and a bull case scenario (refer to Figure 2).

In the base case, we start by estimating a sustainable revenue figure for Medifast moving forward. Q1 2023 sales amounted to $349 million, but considering the seasonality of sales in the weight loss industry, it would be overly optimistic to multiply this figure by a multiple of 4x for the full year. Therefore, revenue numbers above $1.4 billion are unlikely to be achieved in 2023. For the base case, we assume that revenue will decline to $1.1 billion, representing a decrease of more than 31.2% from the $1.6 billion in revenue reported in 2022.

To calculate operating profit in the base case, we utilized Medifast’s average operating margin over the past 22 years, which stands at 11.2%. This margin is slightly lower than the 11.6% operating margin reported in 2022. With $1.1 billion in revenue and an 11.2% operating margin, we arrive at an estimated EBIT of $123 million.

Medifast's SG&A expenses are less sticky compared to other firms because coaches are contractors, not employees. Therefore, if revenue declines, commission payments to coaches should decrease. For the base case, assuming gross margins remain around 70%, we estimate SG&A expenses to be approximately $647 million. However, it is important to note that companies often spend more on operational costs than what is necessary to maintain their current book of business. Additional spending is typically aimed at revenue growth – i.e., extra incentives for coaches or elevated depreciation expenses due to growth CAPEX. Given that we are interested in estimating a sustainable level of earning power, we want to estimate and add back the additional growth spending to our EBIT estimate. In this case, we have added back 20% of the $647 million SG&A expense, amounting to $129 million. As a result, we adjusted the EBIT figure to $253 million.

With a 21% corporate tax rate, Medifast's net operating profit after tax (NOPAT) amounts to $200 million. Discounting this figure by the weighted average cost of capital ((WACC)) estimated at approximately 12%, the EPV of the operating business is calculated to be $1.66 billion. After adding the $124 million in cash and subtracting the $24 million in debt, the current EPV of the equity stands at $1.76 billion for the base case.

For the bull case, assuming a reasonably realistic revenue target of $1.3 billion, which represents an 18.7% decrease from 2022, and utilizing the average operating margin of 13.3% since Optavia's launch in 2017, we arrive at an estimated EBIT of $173 million. With a 70% gross margin assumption, SG&A expenses are estimated to be around $737 million. After adding back 20% of this expense for growth initiatives, the adjusted EBIT amounts to $320 million. Applying the 21% tax rate, NOPAT is calculated at $253 million.

Using the same 12% WACC, the EPV of the operating business is calculated at $2.11 billion. Adding the cash and subtracting the debt gives us the EPV of the equity at $2.21 billion for the bull case.

{kind=link}

Based on our calculations, the current sustainable EPV of Medifast’s equity is likely to be between $1.76 billion and $2.21 billion on the optimistic side. This equates to $162 and $203 per share. Should these numbers be accurate, the base case appears to offer upside potential of 106%. We’ll be rocking for our base case estimates of EPV for the remainder of this article.

MEDIFAST’S ASSET VALUE & ROIC

Today, too little attention is paid to the book value of assets. As a result, most investors lack a critical understanding of a company’s underlying business, resulting in an inability to properly assess expected returns if the stock is acquired at a fair valuation. Over the long run, the investor will find it difficult to perform better than the underlying business, unless the company is bought at a discount relative to its intrinsic value. As a result, attention should be focused on ROIC. We calculate ROIC by dividing our estimate of NOPAT by the total capital employed (TCE) in the enterprise (equity + liabilities – cash). This metric allows investors to gauge the efficiency of capital utilization and the returns generated by the company.

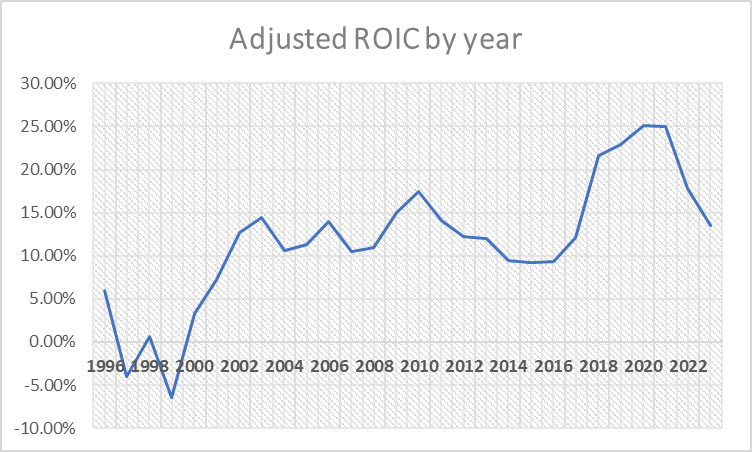

To decrease the probability of being on the wrong side of a trade, considering the book value is one of the several approaches that can be employed. But relying solely on the company's GAAP financial statements may create an illusion of consistently achieving extraordinary returns on invested capital, as seen in Medifast's case (refer to Figure 3).

Figure 3: GAAP ROIC for MED by year using our estimates of adjusted NOPAT (Z McKannan)

{kind=link}

Such consistently high levels of ROIC simply aren’t believable. This discrepancy arises from the significant understatement of Medifast's TCE due to GAAP, leading to inflated returns on invested capital. This observation is confirmed when analyzing Medifast's Q1 2023 balance sheet (refer to Figure 4).

Figure 4: MED’s balance sheet figures reproduced from the Q1 2023 10-Q (Z McKannan)

As seen above, the reported book value stands at a mere $171 million with no intangibles accounted for. However, it is clear that a business generating $1.1 billion in sales and $200 million in sustainable NOPAT, with tangible capital of only $198 million, is likely to possess intangible assets of substantial earning power and value. If a potential competitor were to replicate Optavia's network of 58,000 coaches and 2 million customers from scratch, it would require significant investment to reproduce such a valuable network.

Considering this, it is apparent that Medifast's unadjusted balance sheet only provides insights into the tangible capital employed to generate current earnings. While analyzing the returns on tangible capital employed is insightful, it is essential to estimate the value of Medifast's intangible assets and make necessary adjustments to the balance sheet. This adjustment will allow for a more realistic estimation of the company's asset value, ROIC, and value from growth.

The recognition of intangible assets is often debated, with some arguing that estimating their value lacks precision and provides little value to investors. However, I hold the opposing view and consider the inclusion of intangible assets as a conservative approach. Adjusting the book value upward to incorporate intangibles reduces the estimated ROIC and provides investors with a more accurate representation of the underlying business. It is important not to dwell on minor disparities between estimated intangible values and reported goodwill on the balance sheet but rather focus on the significant disparities, as evident in the case of Medifast.

To determine the value of Medifast's intangibles, we can draw inspiration from the cost-of-production theory of value initially proposed by Adam Smith. Although this theory has inherent flaws since the value of an asset is subjective to consumer preferences rather than production cost, estimating the earning power associated with a company's intangibles is speculative and challenging. However, utilizing production cost as a proxy for value is better than using no estimation at all. Even with potential deviations in estimates, a reasonable approximation provides a better understanding of the total capital employed by the enterprise and offers insight into the true underlying economics and expected returns of Medifast.

In the case of Medifast, significant expenditures related to SG&A expenses have likely contributed to the creation of their intangible assets, which can be treated as quasi-assets. Advertising expenses and compensation paid to coaches have played a crucial role in the development of the Optavia brand and network. To determine the value of these identifiable intangibles, we pose a simple question: How many years of SG&A spending would a potential competitor have to invest to reproduce this value? One to three years' worth seems reasonable, with one year being too little and three years being excessive for Medifast's size.

Based on historical SG&A expenditures from 2018 to 2022, which averaged $637 million, we have applied a 2x multiple to estimate the value of Medifast's intangibles at approximately $1.28 billion. Adding this estimated value of intangibles to the reported tangible equity of $171 million results in an adjusted book value of $1.45 billion, or $133 per share (refer to Figure 5).

Figure 5: AV calculation for MED (Z McKannan)

Our estimate of book value is closer to what I’d expect a competitor to pay in order to replicate the earning power of Medifast. Dividing our estimate of sustainable NOPAT of $200 million by the TCE, Medifast's true ROIC is around 13.5% (refer to Figure 6).

Figure 6: TCE and ROIC calculation for MED (Z McKannan)

Although slightly above our estimate of Medifast's WACC of 12%, the 13.5% ROIC presents a different perspective compared to the GAAP figures (refer to Figure 7). The GAAP ROIC provides a better measure of Medifast's return on tangible capital employed, which is impressive and demonstrates the company's ability to operate with minimal tangible capital. However, incorporating intangibles significantly lowers Medifast's ROIC for both previous and current years, and I believe that the adjusted figure offers a more accurate representation of the underlying business.

Figure 7: Comparing MED's GAAP ROIC and adjusted ROIC (Z McKannan)

{kind=link}

VALUING MEDIFAST’S GROWTH

To assess Medifast's growth potential, we first examine their market share in the $7 billion online weight loss market in the U.S., which currently stands at approximately 20%. However, the sustainability and potential growth of this market share are questionable. Historically, Medifast's share of the market has been volatile, indicating a challenge in maintaining a consistent position in the market. A company that cannot protect its market share will likely struggle to generate superior returns on invested capital over the long term. This casts doubt on whether Medifast's intrinsic value is significantly higher than their current EPV.

While there has been a positive spread between our estimate of Medifast's ROIC and their 12% WACC from 2018 to 2022, indicating value creation from management's growth initiatives, I am skeptical about their future ability to deploy capital at positive spreads. History shows that superior returns attract hungry competition, which is likely to cause any superior returns on invested capital to revert to the mean. Indeed, Medifast has historically struggled to consistently deliver an ROIC above their WACC, confirming the competitive nature of the industry with limited barriers to entry. From 2001 to 2017, the average adjusted ROIC for Medifast was approximately 12% (refer to Figure 8).

Figure 8: MED's adjusted ROIC by year after estimating intangibles (Z McKannan)

{kind=link}

In the period following 2017, Medifast was able to generate a superior ROIC for a brief stretch. It’s difficult to pin down causation. It coincided with changes in leadership following activist involvement, with the current CEO, Daniel Chard, taking the helm after replacing the previous CEO in 2016. Chard's focus on the Take Shape For Life segment, rebranded as Optavia in 2017, played a role in their superior returns. During this period, it appeared that Medifast's moat, if it existed, stemmed from a customer demand advantage in the form of customer captivity.

However, the key question is whether Medifast can sustain this customer captivity and effectively ward off competitive entry going forward. Past issues with customer retention raise doubts about the company's ability to maintain a strong moat. Therefore, for the purposes of our analysis, we will assume a conservative approach and assign zero value to Medifast's growth potential. We anticipate that future returns on invested capital will align with Medifast's WACC.

Taking a conservative stance is advantageous in this case, as it allows us to avoid overestimating the presence of competitive advantages. If we are mistaken in assuming mean reversion and the positive spread remains, investors who purchase the stock at current prices would essentially receive the growth for free.

MEDIFAST’S AV & EPV THROUGH HISTORY

Through an analysis of Medifast's annual filings and historical stock prices dating back to 1996, we can identify the ideal times to buy MED stock relative to our historical estimates of EPV and AV. Interestingly, there have been only four instances over the past 27 years when Medifast stock presented attractive buying opportunities.

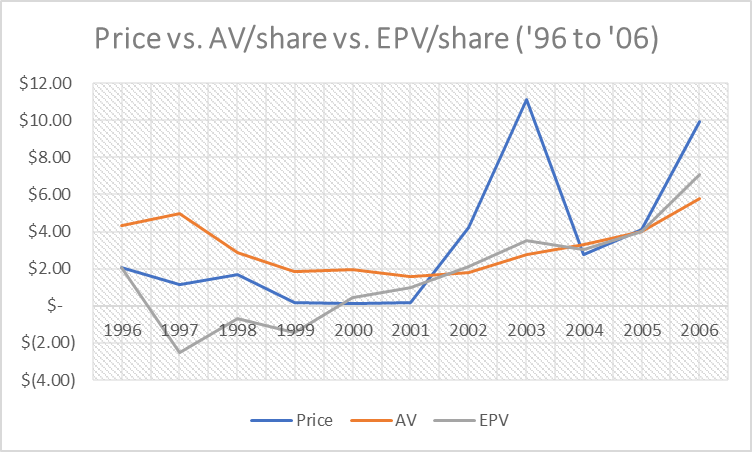

The first such instance occurred in 2000 (refer to Figure 9), prior to which Medifast operated under the name HealthRite. At that time, the company had two subsidiaries: Jason Pharmaceuticals (Jason) and Montana Naturals International (MTNA). Jason was the profitable owner of the Medifast product line, while MTNA appeared to service the herbal industry and was unprofitable. Prior to 2000, HealthRite stock appeared to be a classic value trap, with management allocating large amounts of capital to the unprofitable MTNA.

However, a catalyst emerged in 1999-2000 when management announced the closure of MTNA. This decision marked a strategic shift, with HealthRite refocusing its efforts on its profitable asset, Jason, and the Medifast branded products. By 2000, HealthRite was showing operating profits after adjusting for one-time restructuring charges. Had a contrarian turnaround investor recognized this fact, the stock could have presented a lucrative opportunity.

Investors who bought shares during the 2000-2001 window and sold in 2003, when the shares became overvalued, would have realized significant returns, with nearly 37 times their initial investment. In contrast, the S&P 500 delivered a -11.3% return over the same period. Realistically, however, the diligent investor would have likely sold prior to 2003, as the stock was inflated relative to the value of the underlying business by 2002.

Figure 9: MED's price, AV, and EPV from 1996 to 2006 (Z McKannan)

{kind=link}

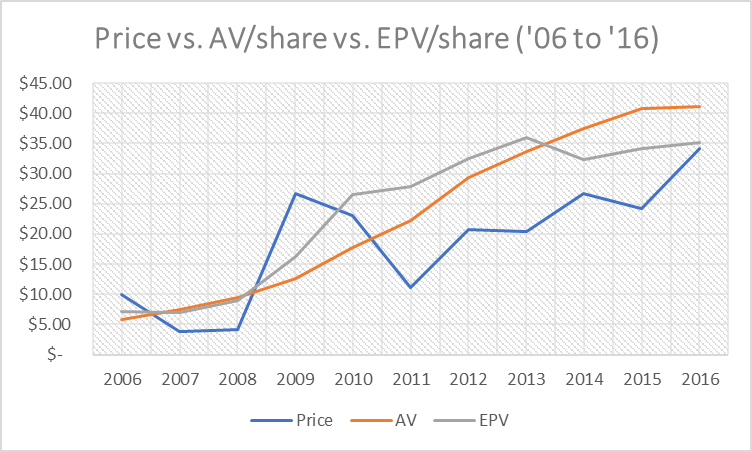

The next two instances where our model indicates undervaluation of Medifast stock occurred in 2007 and a period between 2011 and 2015 (refer to Figure 10). During both periods, Medifast was a profitable business operating in a highly competitive industry. Investors who bought shares between 2007 and 2008 would have witnessed a gain of 583% by 2009, significantly outperforming the -19.4% return of the S&P 500 during the same period. Similarly, shares bought at the end of 2011 would have compounded 205% by 2016, while the S&P 500 delivered a return of 99.4%.

Figure 10: MED's price, AV, and EPV from 2006 to 2016 (Z McKannan)

{kind=link}

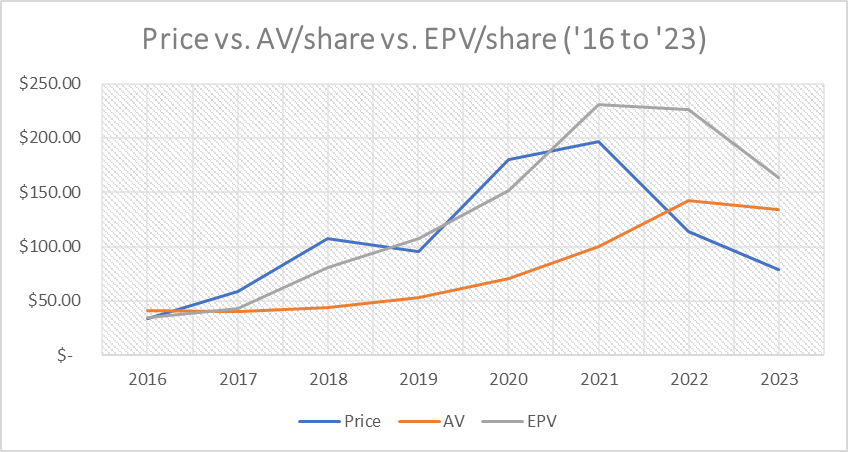

As already discussed, the fundamental shift for Medifast occurred in 2016, when an activist fund acquired a board seat and implemented changes. Daniel Chard was installed as CEO and turned his focus to the Take Shape For Life segment (rebranded as Optavia). The underlying business thrived, and the company achieved an average adjusted ROIC of 22.5% from 2018 to 2022.

While the market initially reflected the value of Medifast's earning power from 2016 to 2021, the stability of the EPV and ROIC turned out to be lacking. The EPV has now reverted closer to the AV, just as the ROIC has reverted to the WACC. It could be argued that the market has overreacted to this mean reversion, as there exists a significant discrepancy between Medifast's current stock price and the value of the underlying business (refer to Figure 11).

It’s important to note that repurchases are also being made at prices below our estimate of Medifast’s EPV and AV. As of the start of 2023, more than 1.4 million shares are eligible for repurchase, and the company repurchased stock at prices ranging between $110 and $120 per share in 2022. And while insider ownership is low, executives and directors have been buying shares since August 2022 when MED’s prices were well above $120 per share. This suggests confidence in the stock’s undervaluation. However, one must properly weigh the risks first before buying.

Figure 11: MED's price, AV, and EPV from 2016 to 2023 (Z McKannan)

{kind=link}

RISKS

When considering the risks associated with investing in Medifast, it's important to acknowledge that many of these risks are already reflected in the current stock price, as evident by the substantial price decline since 2021. While I like the valuation of the stock at current price levels, there are still many things which could kill the returns of shareholders.

- Competitive entry . Medifast operates in a competitive industry with no significant barriers to entry. While companies in such industries are expected to earn returns in line with their WACC in theory, the reality can be different. Overexpansion during favorable periods can lead to malinvestment and lower returns in the future. If this occurs, Medifast's EPV could fall significantly below its AV. While such events can bring opportunities for investors if the situation is expected to normalize, it certainly doesn’t feel that way when the stock is getting punished.

- Impairment of intangible assets. The value of Medifast's intangible assets, which form a significant portion of their AV, would be easily impaired if the company's earning power permanently declines. These intangibles are valuable so long as they contribute to the firm’s overall profitability. They are also difficult to value, and therefore, the investor should remain wary about the level of asset protection in the stock at current prices.

- Health and sustainability concerns. While skepticism is warranted regarding GLP-1 drugs, there are also concerns about Medifast's diet plans. Specifically, Optavia's 5&1 plan, which involves a low-carb, high-protein diet with caloric restrictions of 800-1,000 calories per day, raises questions about the long-term health and sustainability of their products. It seems that the focus is to show clients results as fast as possible to ensure their retainment. With that said, the focus on showing rapid visible progress to retain customers doesn’t necessarily align with the best interest of the client.

- MLM prejudice and regulation. The MLM model, including Medifast's business model, faces scrutiny and regulatory challenges. While Medifast itself doesn't have any lawsuits related to its MLM structure, other MLM companies like Herbalife have war-torn litigation departments. Ongoing prejudice and regulatory scrutiny against MLM may result in Medifast's stock being undervalued relative to its intrinsic value, even if they manage to keep their nose clean.

- Potential accounting shenanigans . Investors should also remain vigilant for any accounting shenanigans. For example, in Q1 2023, Medifast made a policy change that positively impacted revenue by adding $9.1 million that would have otherwise been reported in Q2 2023. While this may seem relatively minor, the manipulation of financial statements is a slippery slope.

DOWNSIDE VS. UPSIDE POTENTIAL

Based on the valuation alone, MED stock appears attractively valued relative to its history and the overall market at a market cap of $855 million. The downside would appear limited, as an 8% dividend yield provides a floor for the stock price in the short term. In terms of dividend stability, there is sufficient cash on the balance sheet to sustain dividend payments for 1.8 years assuming that no additional cash is being generated internally from operations.

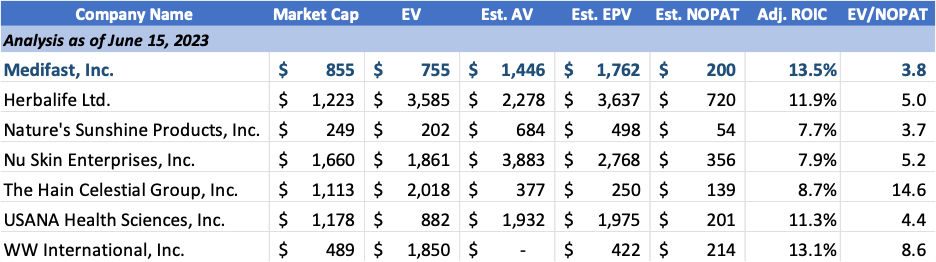

Furthermore, a market comps analysis reveals that Medifast is cheap relative to their peers, leading me to believe that the downside risk is partially mitigated. However, it’s important to approach my market comps analysis with caution, as each business is unique and warrants a thorough valuation. In this case, we used a similar method of valuation for the estimates of AV and EPV of Medifast’s competition. Note, however, that I was much harder on Medifast’s AV and EPV calculation compared to their peers. Even still, they have the boast the highest adjusted ROIC and one of the lowest EV/NOPAT multiples relative to the competition. The MLM discount also becomes evident considering that HAIN and WW are the only non-MLM firms listed.

{kind=link}

Despite the attractive valuation, we need to consider the different ways that their intrinsic value can be severely impaired – i.e., competitive entry and disruption, potential malinvestment by management, MLM regulations and prejudice, health and sustainability concerns around Medifast’s products, etc. These risks have always been present; however, most people choose to assign the risks a heavier weighting during periods of prolonged negative returns.

Eyes should be on customer retention going forward. While back at historical levels, customer retention could be impacted by recent price increases. Given the seasonality of sales, special attention should be given to Q1 2024 results for evidence of significant deterioration in revenues and adjusted ROIC, as Q1 sets the trend for revenues and coach recruitment in subsequent quarters.

Lastly, something interesting was mentioned in Medifast’s Q1 2023 earnings call which could impact the upside of the stock. In July 2023, Medifast is expected to unveil a new product line for coaches, which the CEO estimates will triple the size of their total addressable market. If this is true, and the company can maintain adequate returns on invested capital amid expansion, the stock could be a compelling opportunity especially considering its low valuation.

CONCLUSION

After experiencing a significant decline of 76% since 2021, MED stock appears cheap relative to the estimated value of the underlying business, a rarity observed only four times in the last 27 years. Its attractive dividend yield of around 8% provides a potential floor for the stock at prices below $80 per share. Additionally, despite operating with better practices compared to other MLM firms, MED stock remains the cheapest relative to its MLM peers (revisit Figure 12).

At a market capitalization of $855 million, our valuation analysis suggests that value-oriented investors at these levels have the potential to achieve superior returns compared to the broader market. However, it is crucial to acknowledge that our AV and EPV calculations, standing at $1.45 billion and $1.76 billion, respectively, do not guarantee that the stock will move to reflect this value in the short term. Persistent prejudice against MLM companies or unforeseen risks could lead to the permanent impairment of the company's value. As such, caution is advised, particularly for investors considering purchases at prices that lack a reasonable margin of safety.

Currently, we believe that it is prudent to use our AV estimate of approximately $133 per share as our measure of Medifast's intrinsic value. At the current stock price of around $79 per share, the stock trades at a 40% discount with upside potential of about 69%. To ensure a reasonable margin of safety of at least 30%, Medifast stock is recommended for purchase up to around $93 per share. Investing above this price level may expose investors to a higher degree of risk without sufficient protection.

We would like to thank Zach McKannan for this piece.

For further details see:

In The Murky MLM Space, Medifast Might Actually Hold Some Promise