GO - Ingles Markets: Its Steep Discount Will Eventually Be Rewarded

2023-10-19 07:46:17 ET

Summary

- Ingles Markets, a small retail player, is undervalued and has potential for growth despite recent weaknesses in profitability and revenue.

- The company's revenue has been affected by a decline in fuel sales, but excluding fuel, comparable store sales have shown growth.

- Ingles Markets faces pressure on its bottom line due to consumer pushback against food inflation, but its solid track record and cheap valuation make it a strong buy.

Generally speaking, I am not a big fan of the retail space. This is especially true of clothing retail and similar retail companies. But it's also true of firms that sell food and other basic necessities. This is an incredibly competitive market, with margins often on the low end. And even a slight worsening of business can result in significant pain for investors. But there have been some retailers that have caught my attention in recent years. One that I last wrote about favorably in May of this year is Ingles Markets (IMKTA), a relatively small player with a market capitalization of $1.46 billion and 198 locations in operation.

In that article, I ended up rating the company a 'strong buy' to reflect my view that the stock was significantly undervalued. That was not the first time I rated the company that highly. And from the prior time to the most recent, shares had experienced some downside pressure, mostly because of weakness from a profitability perspective. Fast forward to today, and some of those weaknesses still exist. Revenue has also pulled back slightly, but that's largely to do with a drop in fuel sales. Even with this weakness, shares of the company looking incredibly cheap, both on an absolute basis and relative to similar firms. So even though the stock has underperformed the market since I last wrote about it, with shares down 3.2% compared to the 5.7% increase seen by the S&P 500 over the same window of time, I have decided to keep the company rated a 'strong buy' for now.

A great firm that's being hit by a soft spot

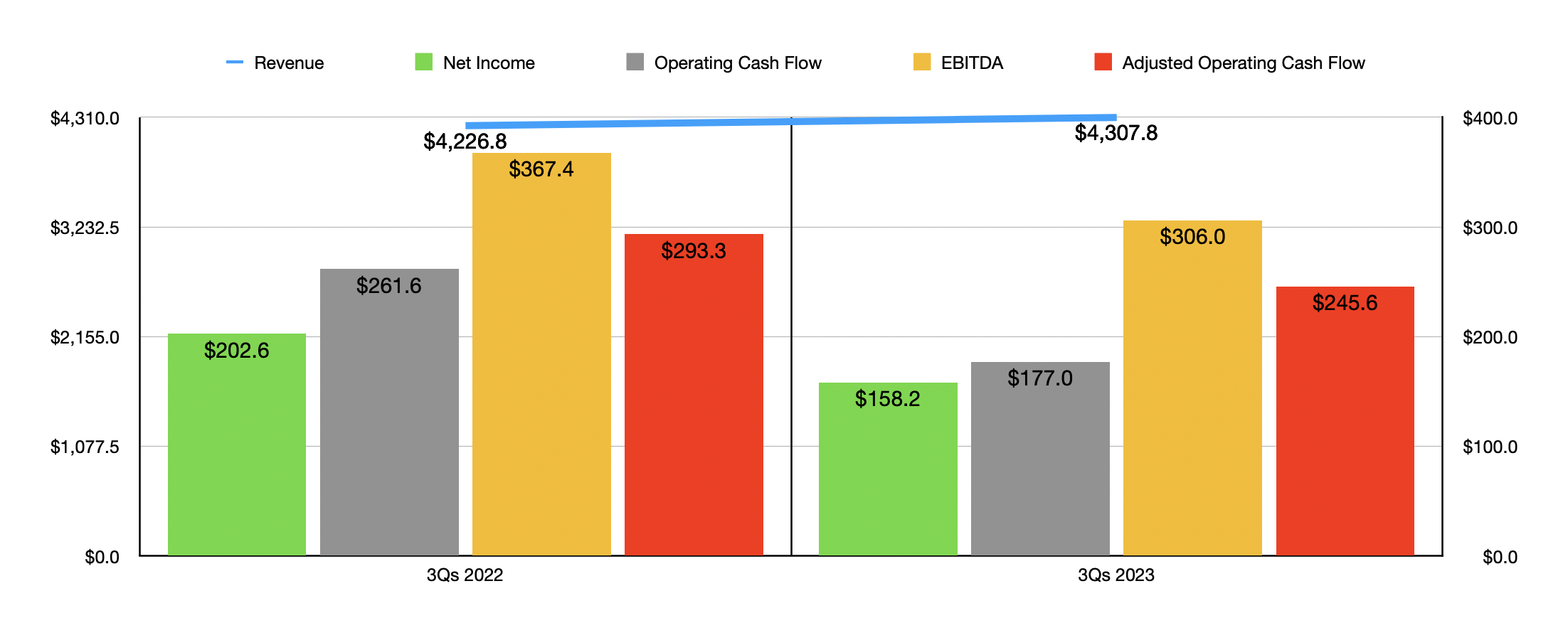

Historically speaking, Ingles Markets has done quite well for itself. Even for the first nine months of the 2023 fiscal year, revenue at the enterprise has grown compared to the same time last year. Sales of $4.31 billion came in 1.9% above the $4.27 billion generated one year earlier. But the bottom line has been an issue. Net income fell from $202.6 million last year to $158.2 million this year. Operating cash flow was slashed from $261.6 million to $177 million. Even if we adjust for changes in working capital, we would get a decline from $293.3 million to $245.6 million. And finally, EBITDA for the company plunged from $367.4 million to $306 million.

{kind=link}

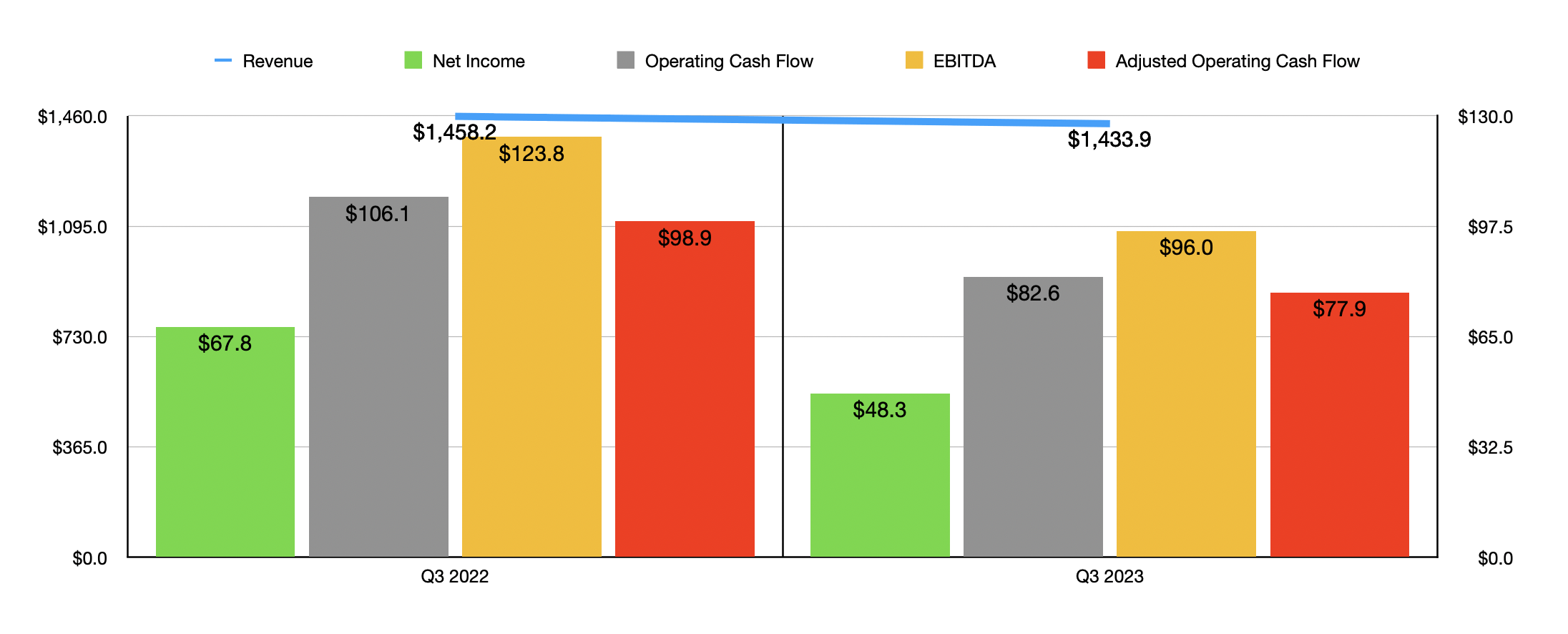

The weakness lately seems to be worsening. As an example, during the third quarter of this year, sales actually came in lower than the same time last year. Revenue of $1.43 billion ended up being 1.7% below the $1.46 billion reported for the third quarter of 2022. At first glance, this might look awfully bad. But it does come with a caveat. And that caveat is that all of the drop in revenue for the company came from a decline in fuel sales. Management does not break up the data to show us volume compared to price. But we do know that fuel prices can be very volatile. If we exclude fuel sales from the mix, the company actually enjoyed comparable store sales growth of 3.8%. Grocery sales were strong, rising 3.6% year over year. But even more impressive was the non-food category, which jumped 8.3% from $303.8 million to $329.1 million. Even the perishables category did okay, inching up 0.4% from $360.7 million to $362.2 million.

{kind=link}

Even though the adjusted revenue figures were positive, the company has faced continued pressure on its bottom line. The fact of the matter is that consumers are pushing back against food inflation and other types of inflation. This materializes in the company being unable to push all of its increased costs onto its customers. As a result, net income fell from $67.8 million to $48.3 million. The firm's gross profit margin contracted because of inflation and raw material shortages, declining from 24.1% to 23.6%. Although this may not seem like much, when applied to the revenue the company generated in just the third quarter alone, it translates to $7.2 million in missed bottom line performance. Operating and administrative costs actually jumped from 17.7% of sales to 18.9%. But much of that increase came from higher payroll associated with fuel operating expenses and fuel costs themselves. Excluding this, operating and administrative costs would have inched up only modestly from 21.4% of sales to 21.7%.

Unfortunately, other profitability metrics for the company have also worsened. Operating cash flow, for instance, managed to fall rather significantly from $106.1 million to $82.6 million. If we adjust for changes in working capital, we would get a decline from $98.9 million to $77.9 million. And finally, we have EBITDA. This dropped from $123.8 million last year to $96 million this year.

{kind=link}

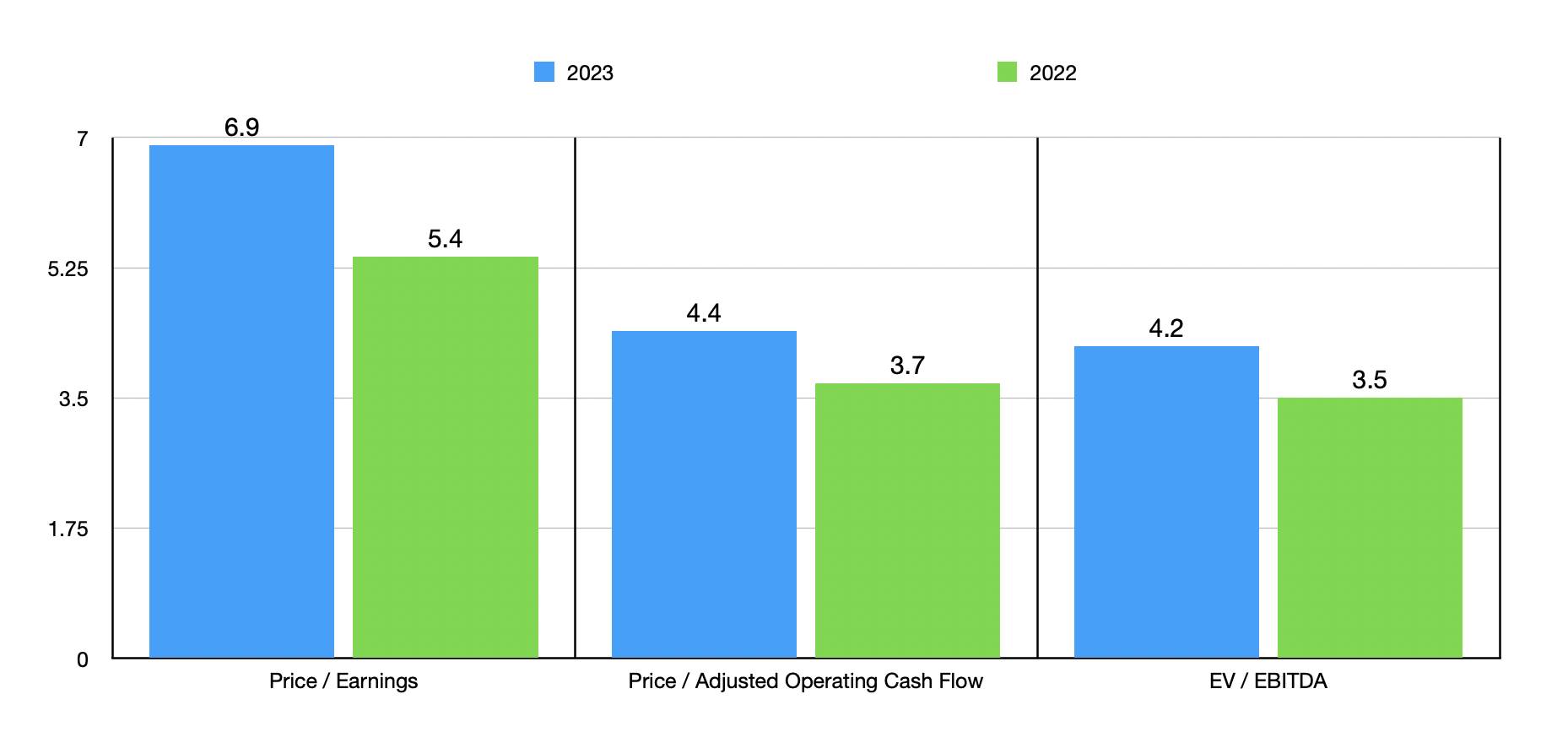

Management has not provided any real guidance for the rest of this year. In fact, management is quiet most of the time. But if we annualize the results experienced so far, we would get net income of $213 million, adjusted operating cash flow of $328.8 million, and EBITDA of $410.9 million. Using these figures, it becomes fairly easy to value the company. As shown in the chart above, Ingles Markets is trading at a forward price to earnings multiple of 6.9. This is up a bit from the 5.4 reading that we get using data from last year. A similar trend can be seen when looking at the other profitability metrics, with the price to adjusted operating cash flow multiple rising from 3.7 to 4.4, while the EV to EBITDA multiple increased from 3.5 to 4.2. Meanwhile, in the table below, I compared the retailer to five similar firms. Using each of the profitability metrics, I found that it was the cheapest of the group. This is true even if we use the more expensive forward estimates.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Ingles Markets |

| 6.9 |

| 4.4 |

| 4.2 |

| Grocery Outlet ( GO ) |

| 38.8 |

| 10.7 |

| 14.8 |

| Natural Grocers by Vitamin Cottage ( NGVC ) |

| 15.4 |

| 6.5 |

| 5.3 |

| Casey's General Stores ( CASY ) |

| 21.8 |

| 12.1 |

| 11.4 |

| Sprouts Farmers Market ( SFM ) |

| 17.4 |

| 9.7 |

| 7.2 |

| Albertsons Companies ( ACI ) |

| 11.0 |

| 4.7 |

| 4.5 |

Takeaway

From what I can tell, Ingles Markets is indeed experiencing some pain at the moment. But I would argue that this pain is very likely transitory. The firm has a solid track record over a long window of time and shares look very cheap, both on an absolute basis and relative to similar enterprises. The retailer does have some debt on hand. But on a net basis, it's fairly modest at $272.7 million. That's a low enough level that I don't need to worry much about the company. When all of this is added up together, it makes me still feel comfortable with the 'strong buy' rating I previously assigned the company.

For further details see:

Ingles Markets: Its Steep Discount Will Eventually Be Rewarded