GO - Ingles Markets: Still Attractive Despite Recent Weakness

2023-05-08 01:26:34 ET

Summary

- Recently, shares of Ingles Markets came under pressure, in large part because of bottom line weakness.

- This may deter some investors from buying into the retail chain, but shares still look cheap even if we assume this weakness will continue.

- In all, this is a great prospect for value investors who have some patience.

Value investing can be tricky. Sometimes, it is difficult to know when to buy into a stock and when to sell. The bargain buyer likes to buy shares of companies even as they decline, with the idea being that if the stock was attractive at a higher price, it should be even more attractive now that it's falling. Although it is true that stock price declines are sometimes unwarranted, they are also sometimes deserved. One good example of the latter involves retail chain Ingles Markets ( IMKTA ). Although revenue generated by the company continues to increase, profits have come under pressure. But this doesn't necessarily mean that investors would be wise to unload their positions. I, in fact, continue to own my shares of the company and that is because, in addition to being a high quality operator, the company is trading at levels that make it fundamentally cheap. This is true on both an absolute basis and relative to most competitors.

Recent performance has been weak

The last article that I wrote about Ingles Markets was published in early January of this year. In that article, I mentioned that the company had been a solid play relative to the broader market. Although profits had struggled a bit leading up to that point, revenue and cash flows continued to grow. And even though shares of the company still remained cheap, that came off the back of some rather strong upside in the units. From January of 2022 when I had written about the company initially, through the publication of this aforementioned recent article, shares had seen upside of 22.3% compared to the 15.1% drop generated by the broader market. Unfortunately, we have seen that picture change since the start of the year. Following the publication of my January 2023 article, shares of the business have plunged 16.3% at a time when the S&P 500 is up 5.8%. Since I first became bullish on the company in January of last year, shares are now up only 2.8%. But at least that is better than the 9.9% decline seen by the S&P 500.

{kind=link}

Author - SEC EDGAR Data

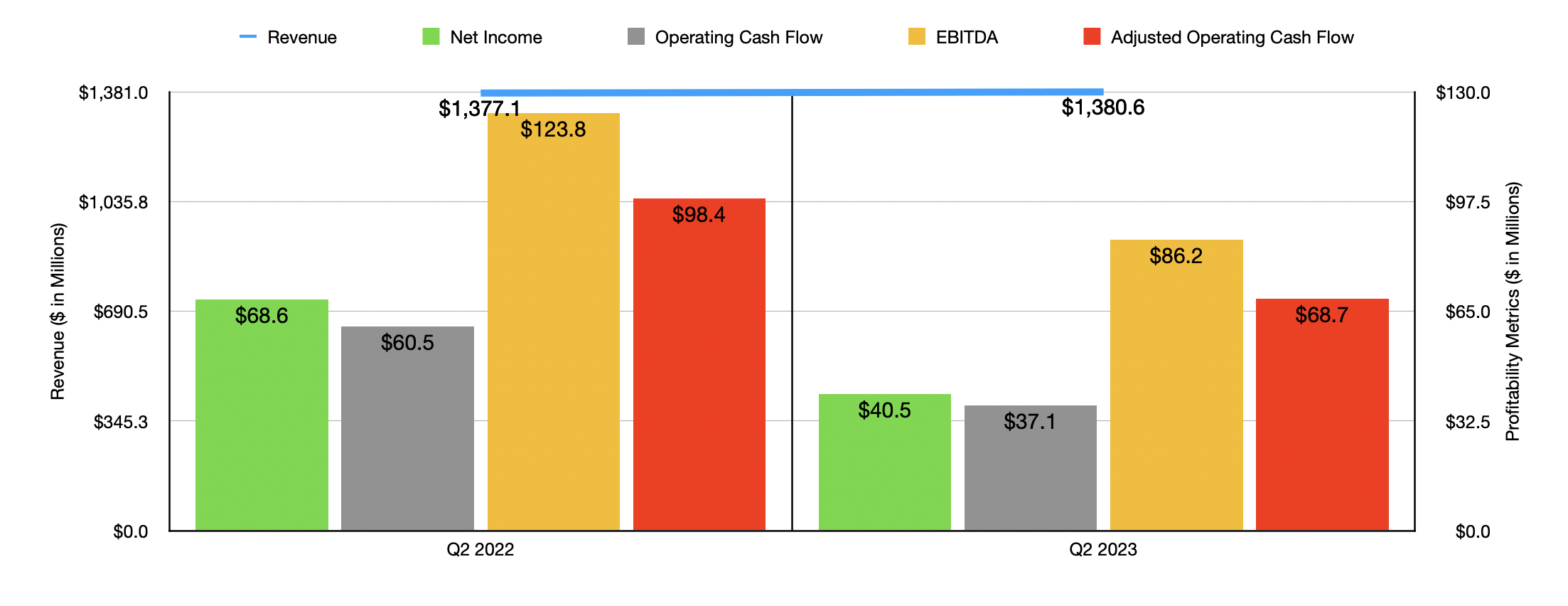

Recent weakness from a share price perspective is almost certainly being driven by fundamental weakness. Consider how the company performed during the second quarter of its 2023 fiscal year. These results just came out on May 4th. During that time, revenue came in at $1.38 billion. This is only $3.5 million higher than what the company generated one year earlier. Interestingly, actual retail sales for the company dropped from $1.33 billion down to $1.32 billion. If we remove fuel from the equation, comparable store sales would have grown by about 3.4%.

It's great to see any sort of sales increase in this environment. But unfortunately, the company did suffer rather materially on its bottom line. Net profits went from $68.6 million in the second quarter of the 2022 fiscal year to only $40.5 million the same time this year. A key driver behind this decline was a drop in the company's gross profit margin from 25.3% down to 23.6%. This, according to management, was driven by inflation and raw material shortages that ultimately caused an increase in its cost of products. Unfortunately, other profitability metrics followed a very similar trajectory. Operating cash flow was nearly halved from $60.5 million to $37.1 million. Even if we adjust for changes in working capital, we would have seen it drop from $98.4 million to $68.7 million. And finally, EBITDA for the enterprise fell from $123.8 million to $86.2 million.

{kind=link}

Author - SEC EDGAR Data

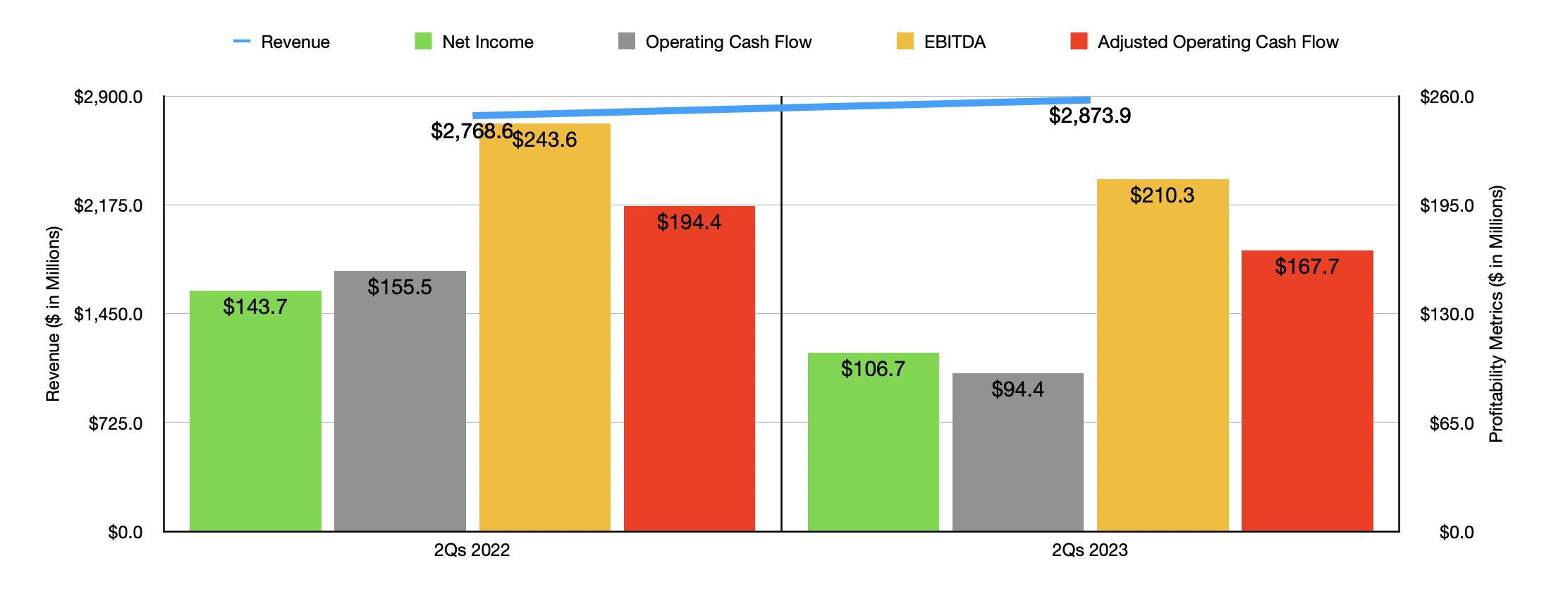

The second quarter of the year was definitely the most painful. But it wasn't the only time in which the company saw some weakness. If you look at the first half of the 2023 fiscal year as a whole, the picture showed some bottom line pain. Even though revenue rose from $2.77 billion to $2.87 billion, profits plunged from $143.7 million to $106.7 million. Looking at the chart above, you can see that all the other profitability metrics that I looked at for the company also worsened during this time. For instance, operating cash flow fell from $155.5 million to $94.4 million. On an adjusted basis, it shrank from $194.4 million to $167.7 million. And finally, EBITDA managed to decline from $243.6 million to $210.3 million.

{kind=link}

Author - SEC EDGAR Data

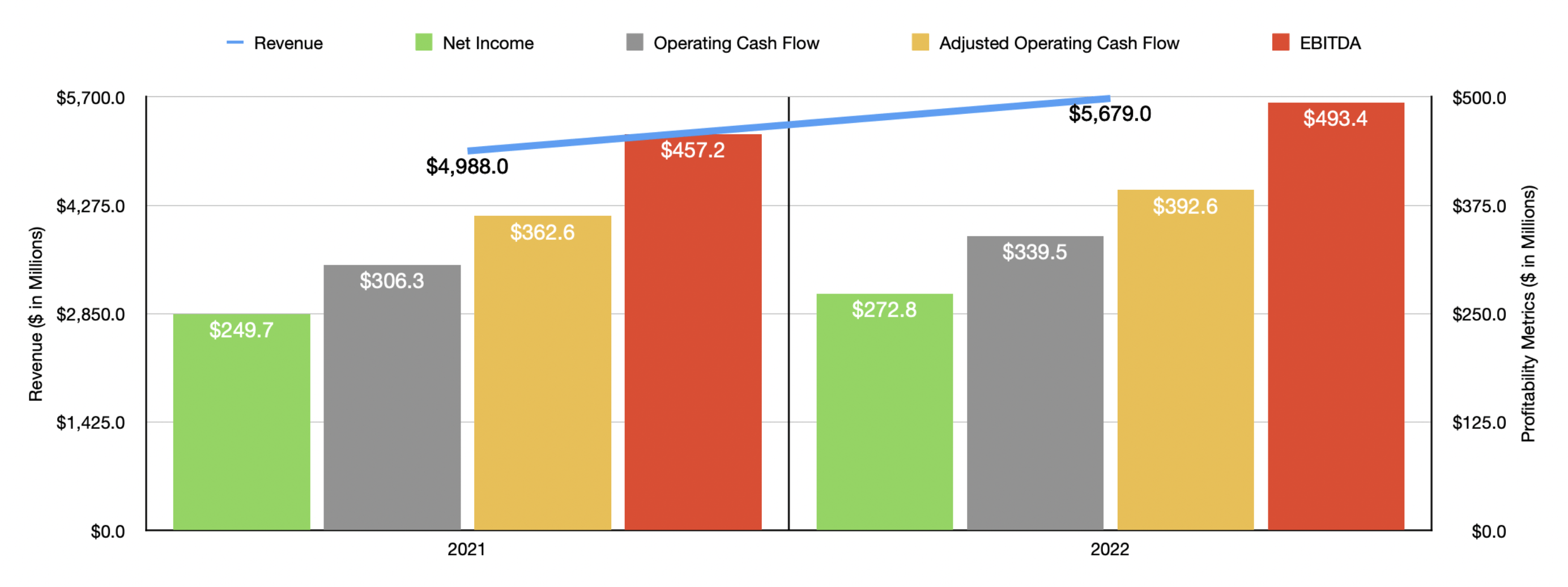

This, combined with an absence of guidance from management, makes it very difficult to understand what the 2023 fiscal year in its entirety might look like. Following a rather simplistic approach, we can project out what financials might be by annualizing the results experienced during the first half of the year. Doing this, we would end up with net income of $202.6 million, adjusted operating cash flow of $338.7 million, and EBITDA of $425 million. As you can see in the chart above, which I took from the last article that I wrote about the company, this would imply some meaningful weakness on the bottom line compared to what the company generated in 2021 or 2022.

{kind=link}

Author - SEC EDGAR Data

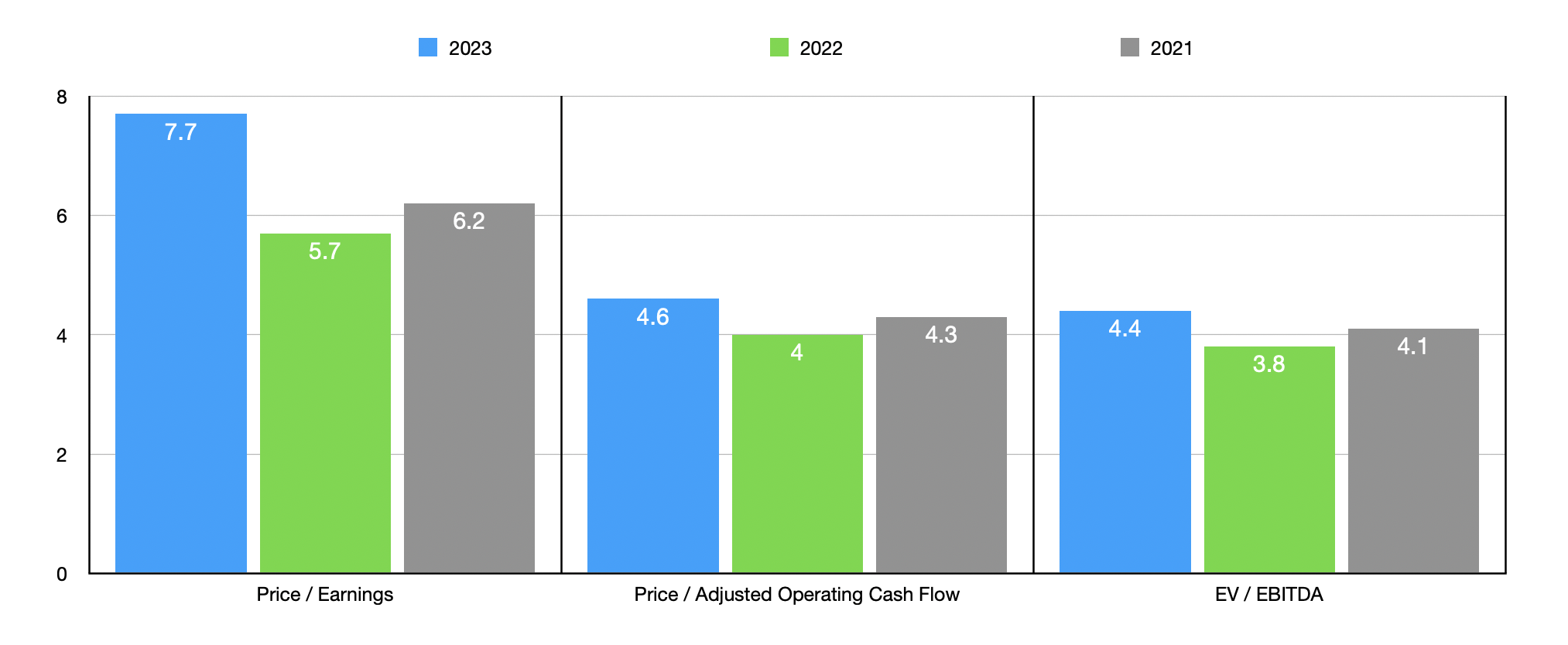

Even if we assume that this weakness will end up being correct, shares of the company look quite cheap at this time. On a forward basis, the company is trading at a price to earnings multiple of 7.7. The price to adjusted operating cash flow multiple is 4.6. And the EV to EBITDA multiple comes in at 4.4. In the chart above, you can see how the company is priced using data from 2021 and 2022 as well. As part of my analysis, I also, in the table below, compared the company to five similar firms. On a price to earnings basis, it was the cheapest of the group. Using the price to operating cash flow approach, I found that only one of the five companies was cheaper than it. And when it comes to the EV to EBITDA approach, two of the five firms are cheaper than it.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Ingles Markets |

| 7.7 |

| 4.6 |

| 4.4 |

| Grocery Outlet Holding Corp. ( GO ) |

| 45.6 |

| 16.0 |

| 18.2 |

| Natural Grocers by Vitamin Cottage ( NGVC ) |

| 16.2 |

| 5.5 |

| 4.3 |

| Casey's General Stores ( CASY ) |

| 19.4 |

| 9.8 |

| 10.6 |

| Sprouts Farmers Market ( SFM ) |

| 15.6 |

| 9.8 |

| 6.2 |

| Albertsons Companies ( ACI ) |

| 9.6 |

| 4.1 |

| 4.1 |

Takeaway

Operationally speaking, there is no doubt that Ingles Markets is experiencing a bit of pain right now. I fully expect this trend to continue for at least the rest of this year. Depending on market conditions, it could persist into next year as well. But this doesn't necessarily mean that the market is right by pushing shares down. The fact of the matter is that units are quite cheap at this time and, in the long run, the company should continue to fare quite well. Given these factors, I have no problem keeping it at the ‘strong buy’ level that I had it at previously.

For further details see:

Ingles Markets: Still Attractive Despite Recent Weakness