IIPR - Innovative Industrial Properties: Deeply Undervalued 10% Cannabis REIT

2023-04-01 04:36:15 ET

Summary

- The US cannabis sector has suffered through a long crash with no end in sight.

- Innovative Industrial Properties is beginning to feel some pain, with some tenants defaulting on rent.

- I expect a significant recovery, but the stock is undervalued even assuming no recovery.

- This is a 10% yield with fast-growth ahead.

Innovative Industrial Properties (IIPR) remains a compelling investment on the growth of the cannabis industry. As a cannabis real estate investment trust (‘REIT’), IIPR does not directly sell or process the plant, but it earns high-quality rental income from its tenants. As cannabis operators across the country deal with price compression amidst a tough macro backdrop, IIPR has seen some tenants default on their rent obligations. Yet with the stock trading below 2019 levels, much of that pessimism has already been priced in. I expect IIPR to continue offering above-sector growth rates and eventually earn back a premium valuation multiple.

IIPR Stock Price

Cannabis stocks were all the rage in 2021, but the entire cannabis sector has undergone a vicious crash as margins deteriorated and valuations were reset. Being higher on the capital stack has not insulated IIPR from the pain, as the stock is down 70% from highs.

I last covered IIPR in December where I rated the stock a buy on account of the attractive 7% dividend yield and low valuation even under pessimistic assumptions. The stock is down 25% since then, as more troubled tenants have emerged. While it may take some time to work through near term headwinds, IIPR remains an attractive growth story for the long term.

IIPR Stock Key Metrics

IIPR owns 110 properties spread across 19 states. The vast majority of these properties are cultivation facilities and 85% of its tenant base operate in more than one state. IIPR is arguably the most well-known cannabis REIT in the nation and has been a crucial provider of capital for the cannabis industry.

2022 Q4 Presentation

Because cannabis has been and remains illegal on the federal level, cannabis operators have very limited access to capital. This enables IIPR to earn above-market returns on its investments. For reference, whereas Realty Income ( O ) might earn around a 6% cap rate with 1% annual lease escalators on its net lease assets, IIPR on the other hand earns a 13% cap rate with 3% annual lease escalators on its cannabis assets. That has huge implications for both internal and external growth potential.

Those attractive lease terms plus high appetite for real estate capital has helped IIPR deliver incredible growth, with its dividend per share growing at a 40% CAGR over the past 5 years.

2022 Q4 Presentation

Yet as seen above, the higher investment yields are not without risk, as rent collection has finally dipped below 100% in 2022. The latest quarter saw IIPR deliver $2.12 in AFFO per share, representing 14.6% YOY growth, but investors have justifiably focused instead on the growing list of troubled tenants. King’s Garden was the troubled tenant of the prior quarters but management has disclosed that the tenant was now paying rent and is in the process of selling off some of its properties. It is not clear if King’s Garden is paying its rent in full or if there was some markdown in rent.

But as the issues at King’s Garden are more or less resolved, new tenant issues have emerged. Rent collection was 94% for the fourth quarter but dipped to 92% for the month of February. On the conference call , management noted that it had applied $413,000 in security deposits towards rent from tenant Holistic for its California and Michigan properties. Tenant Green Peak has defaulted on a property in Michigan and tenant Parallel has defaulted on a property in Pennsylvania, but IIPR has not yet applied those security deposits. Management noted that sometimes taking that security deposit can get in the way of the legal process but emphasized that it could and would take the security deposit when it made sense to do so. Parallel also has defaulted on a property in construction in Texas, of which IIPR has already funded $8.2 million of the $27.4 million original commitment. An interesting point regarding these two tenants is that while they have defaulted on these two properties, they are current on rent on their leased properties in other states. IIPR had not added “cross-default” provisions on these leases, making it possible for these tenants to default on select properties while still operating other properties. Management noted that just around 38% of its revenues were subject to cross-default provisions. Management stated that the legal process to resolve these cases may take as long as 2 years.

It is not all bearish. IIPR ended the quarter with just $295 million in debt, representing a debt to EBITDA ratio of just over 1x, far lower than the typical 5.5x to 6.0x leverage ratio typically employed in the NNN REIT sector. For the full 2022 year, IIPR invested $394 million across 9 properties and 12 leave amendments. These included lease amendments with tenants Ascend Wellness, PharmaCann, and Goodness Growth to fund their expansion projects in New York ahead of the adult-use rollout. IIPR noted that it had added cross-default provisions on all leases for these 3 tenants.

Looking ahead, management declined to issue guidance regarding its acquisition pipeline, citing access to capital as being the main roadblock. While IIPR’s balance sheet remains under-leveraged relative to peers, lenders may not be so willing to extend more capital given the pricing pressures seen in the industry. Meanwhile, the stock is trading at low equity valuations, making its equity a more expensive currency than in the past (though arguably still a possible source of capital).

Is IIPR Stock A Buy, Sell, or Hold?

At recent prices, IIPR was trading at only 9.4x forward AFFO. Between the 3% annual lease escalators and high acquisition cap rates, I view consensus estimates for forward growth to be too conservative.

{kind=link}

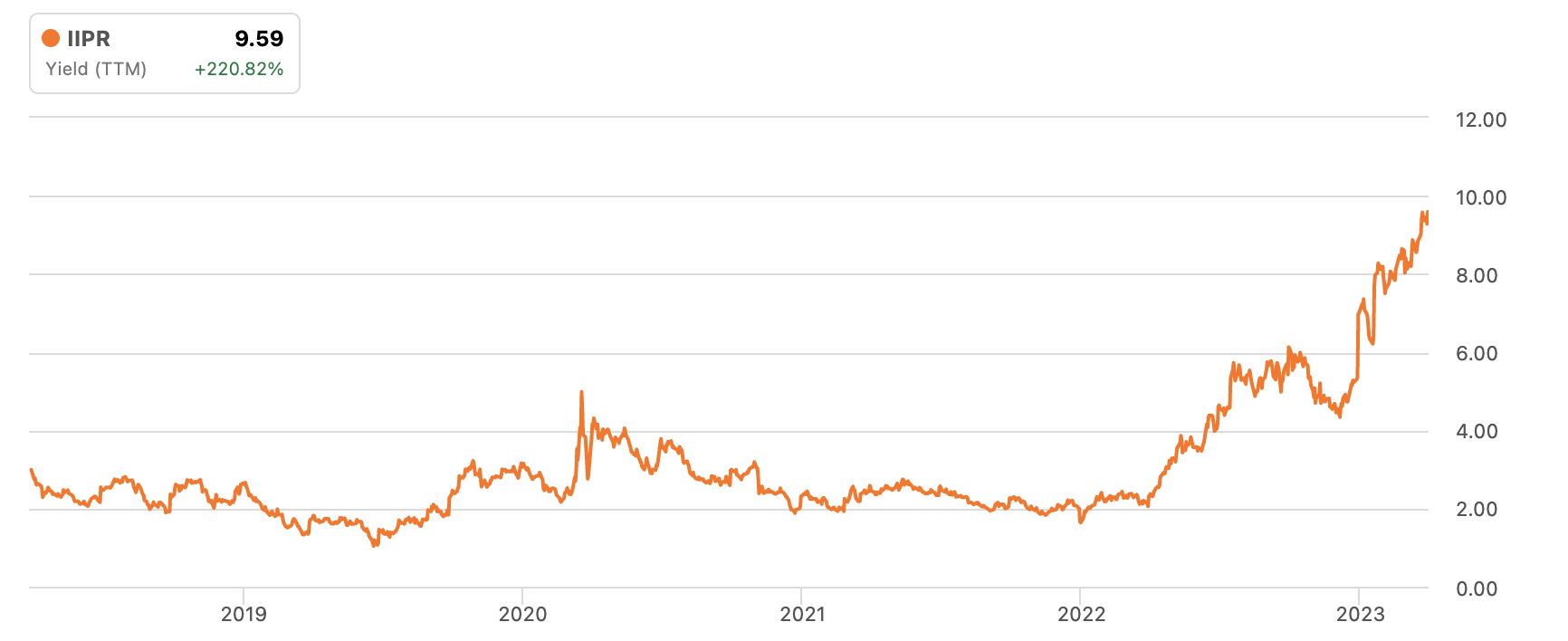

Meanwhile, IIPR is trading at its highest dividend yield it has ever traded since it came public in 2016.

{kind=link}

Due to the high margin profile of the business, reductions in revenue would not lead to significantly greater drops in cash flow. IIPR had a 92% rent collection rate in February. If we assume that IIPR gets no recovery on those defaulted leases and sees even greater losses at 15% in total revenues lost, then AFFO would drop by a maximum of 17.8%. IIPR would be earning $1.74 in AFFO per share. The company would likely have to reduce its $1.80 per share dividend payout, but the stock would be trading at just 10.7x AFFO. That is significantly lower than the 15.2x FFO multiple at Realty Income. Yet IIPR offers superior growth potential than O, and thus deserves to trade at a premium multiple. IIPR benefits from being agnostic to cannabis legalization. The longer it takes for legalization to take place, the longer IIPR benefits from above-market financing terms. Upon legalization, the credit profile of its tenants improves, with the associated multiple expansion being more than enough to offset any eventual reductions in rent (I note that IIPR maintains a 15.3 weighted average lease term). I am doubtful that IIPR will see 15% reductions in rent without any recovery, but the stock looks cheap even if that scenario occurs. I could see IIPR trading at 15x forward AFFO, representing a stock price of $120 per share - but note that there is a wide range of fair value for the stock considering the high growth potential and nagging perception of risk.

What are the key risks? The most critical risk is the long term viability of the US cannabis business model. Normalization (broader acceptance of cannabis) is taking longer than expected, as our politicians have taken their time in passing regulatory reform. This means that legal operators are having to compete against illicit operators in an artificially small market. As a passionate cannabis user myself, I am amazed by the great potential for the plant to address a variety of medical applications such as pain, insomnia, and anxiety. But if the broader public is not yet aware or comfortable with the plant, then demand for the plant remains low relative to the supply. I do not expect pricing pressures to resolve themselves until normalization takes hold. This means that many operators may not survive until then, as many cannabis operators have taken on too much debt to fund overconfident ambitions. IIPR is likely to face significant near term volatility as it works through the storm, and sentiment for cannabis operators and IIPR may not improve so quickly. In the meantime, shareholders would enjoy being able to reinvest dividends at low valuations, but the catalyst for multiple expansion might be elusive. I continue to find IIPR highly buyable for those looking for a profitable name in the cannabis investor that offers exposure to the long term growth potential of cannabis while paying dividends along the way. I note that Cannabis Growth Portfolio favorite NewLake Capital (NLCP) is also a competitive choice, with a higher 12% dividend yield and greater cross-default protection.

For further details see:

Innovative Industrial Properties: Deeply Undervalued 10% Cannabis REIT