CGC - Innovative Industrial Properties: Dividend Safety Assessed

2024-01-21 01:08:33 ET

Summary

- Innovative Industrial Properties is a REIT with a dividend yield of nearly 8% and a unique business model in the cannabis industry.

- The company's financials are in good shape, with low debt levels and consistent historical earnings growth.

- While revenue growth has slowed due to tenant troubles, we think IIPR is in the process of righting the ship.

- Despite the improving underlying business, growth prospects appear mild, and the stock appears nearly fully valued.

- IIPR appears best suited for those attracted to the well-backed 8% dividend, as opposed to those seeking a strong capital appreciation profile.

Innovative Industrial Properties ( IIPR ) is one of the more interesting REITs on the market today.

With a hefty dividend of nearly 8% and a business model that derives its income from an 'off the beaten path' industry, some may be wondering whether or not this company has what it takes to earn a spot in their portfolio.

Today, we'll take a closer look at IIPR, and determine whether or not the company is well positioned from a financial standpoint.

Can the REIT keep up its impressive distributions? Is there room for capital appreciation? Let's dive in and figure it out.

Financials

The first stop to consider here is the company's financials, which are in pretty good shape, all things considered.

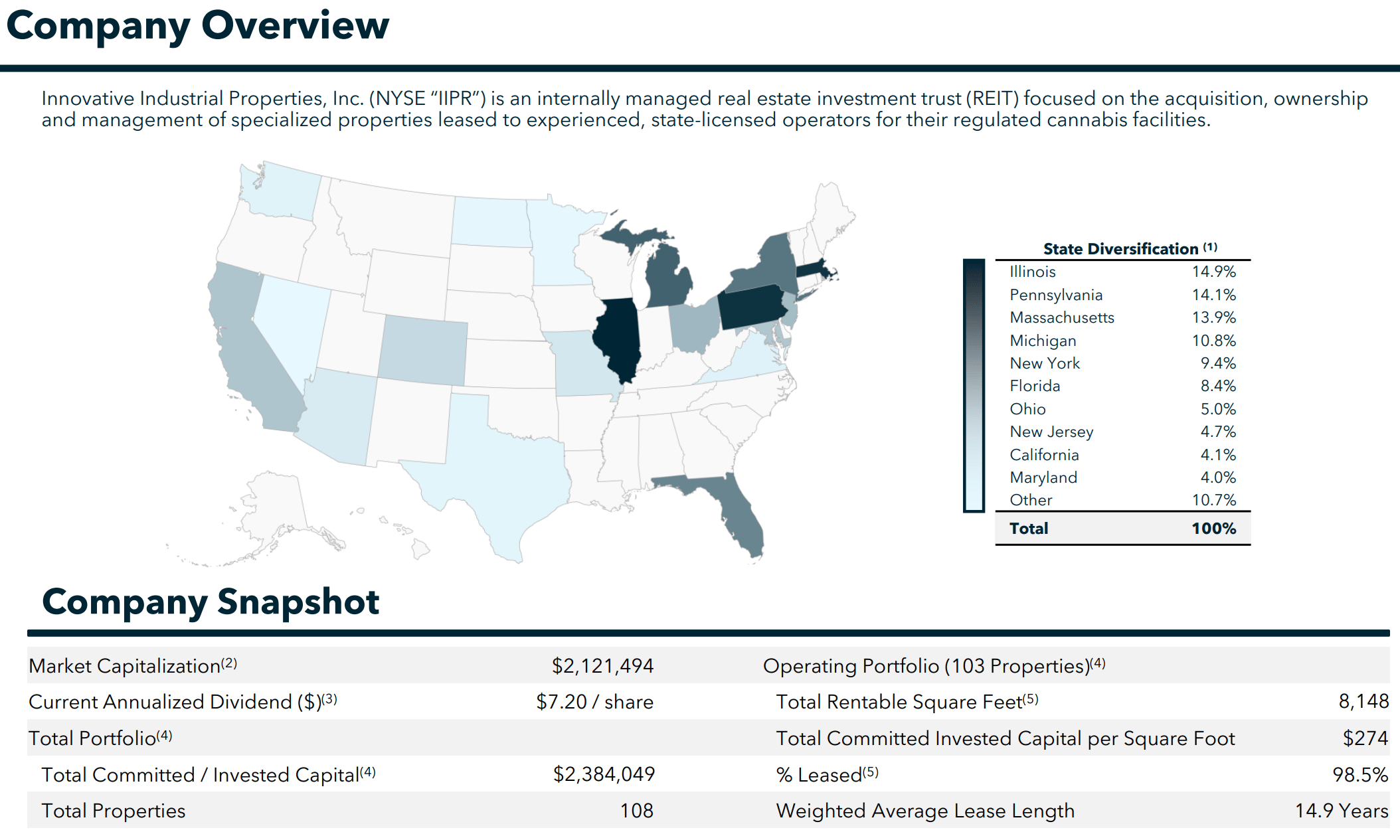

In case you're new to IIPR, the company is a REIT, whose real estate holdings are mostly comprised of specialized properties geared towards cannabis production and processing:

{kind=link}

This includes 103 facilities across 18 states and 8.1 million in total square feet.

On the plus side, the firm has a very low LT Debt / Capital ratio of only 13%. This low level of indebtedness means that the majority of IIPR's revenues can drop right to FFO, and thus, to investors' pockets.

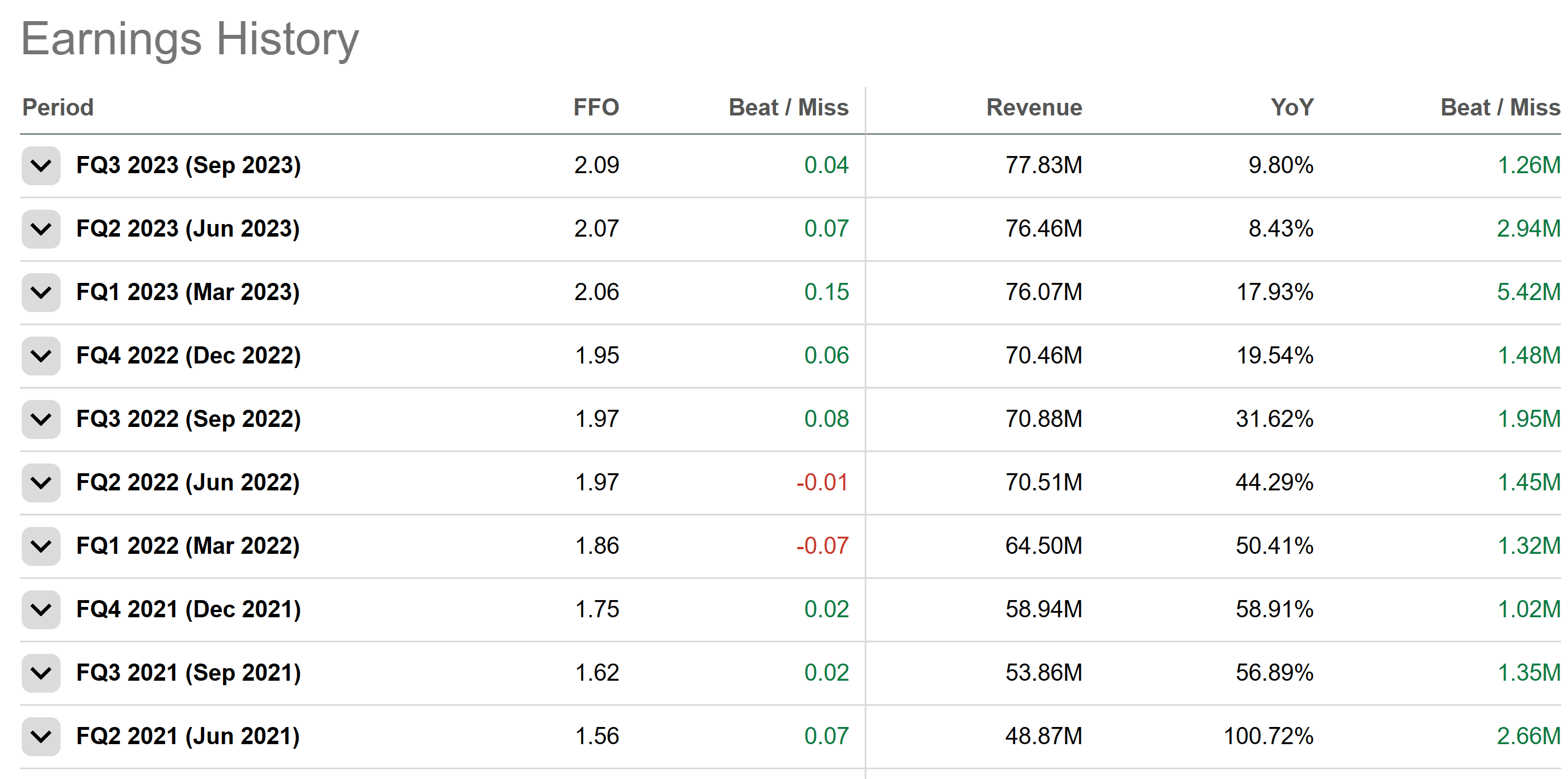

Earnings-wise, the company has done very well over the last several years, beating top line sales consistently and only missing on EPS twice:

{kind=link}

On the flip side, revenue growth is slowing considerably, from 58% in Q4 of 2021 to upper single digits over Q2 and Q3 of 2023.

This slowing revenue is largely due to the lack of new capital being invested into the space, along with tenant troubles which have been hurting financial performance.

Here's a nice summary of that from The Dividend Collectuh in their recent article :

Innovative Industrial has been dealing with tenant troubles for a while now. Earlier this year, the REIT had tenants Parallel & Green Peak Industries default on properties. They also had affiliates of Medical Investor holdings default on one of their California properties. During the last quarter management stated they had taken back properties from Parallel, Green Peak, and King's Garden.

In regards to Green Peak, IIPR regained possession of two small retail properties leased to the company and expects to regain possession of one more at the end of this month. Management did state they sold Green Peak's assets to a buyer this past October. These troubled tenants caused occupancy rates to drop over the past few quarters.

In sum, it's been a somewhat volatile time for IIPR's tenants, but things are expected to improve going forward, now that IIPR is back in possession of its properties and should be able to re-rent those facilities.

This was underscored on the recent earnings call, where Chairman Alan Gold said the following:

We have one of the strongest and most experienced teams of real estate professionals in the cannabis industry, a high-quality portfolio and arguably a conservative and flexible balance sheet, with a 12% debt to total gross assets, no variable rate debt, no meaningful debt maturities until May 2026.

...

To recap the quarter, we generated total revenues of $78 million in Q3 and adjusted funds from operations of $65 million. Rent collection for IIP’s operating portfolio was 97% for the quarter. The financial performance continued to drive dividend returns to our investors with $7.20 of dividends declared per share in the past 12 months, an increase of 6% over the prior 12-month period.

From many angles, the ship appears to be righting.

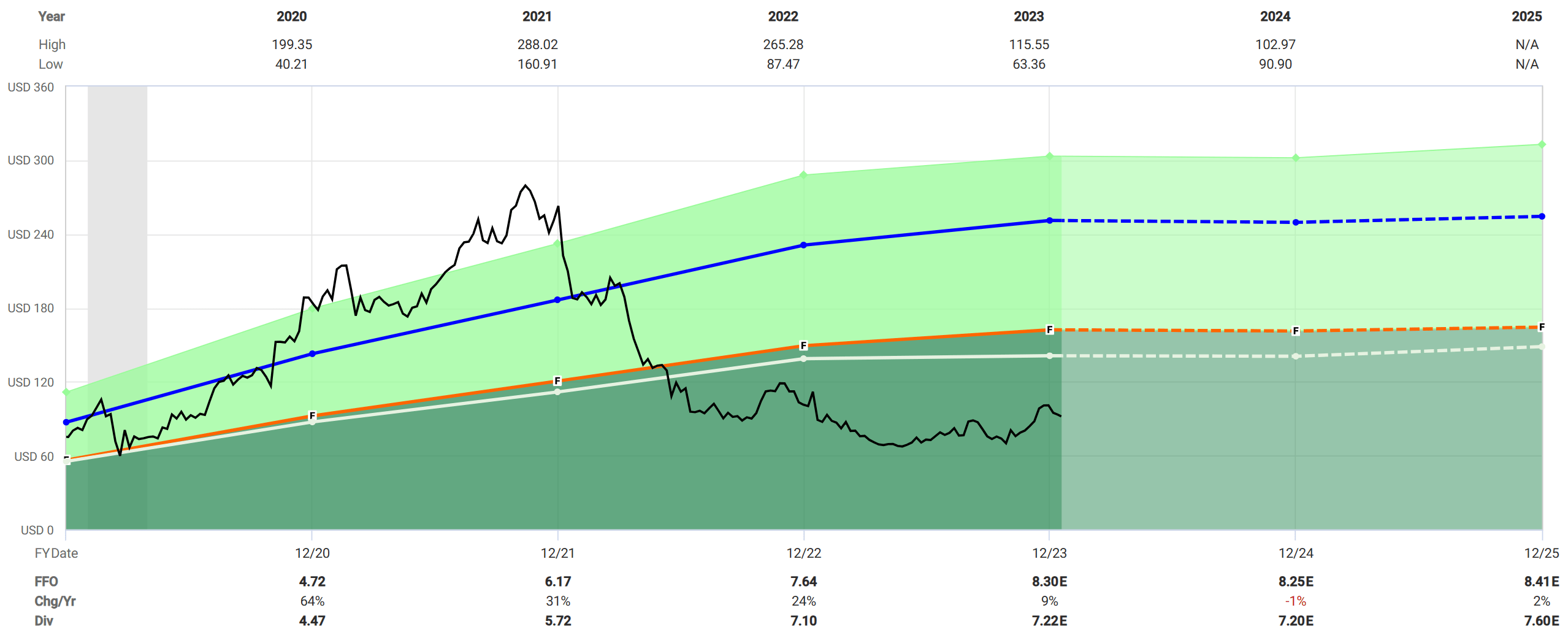

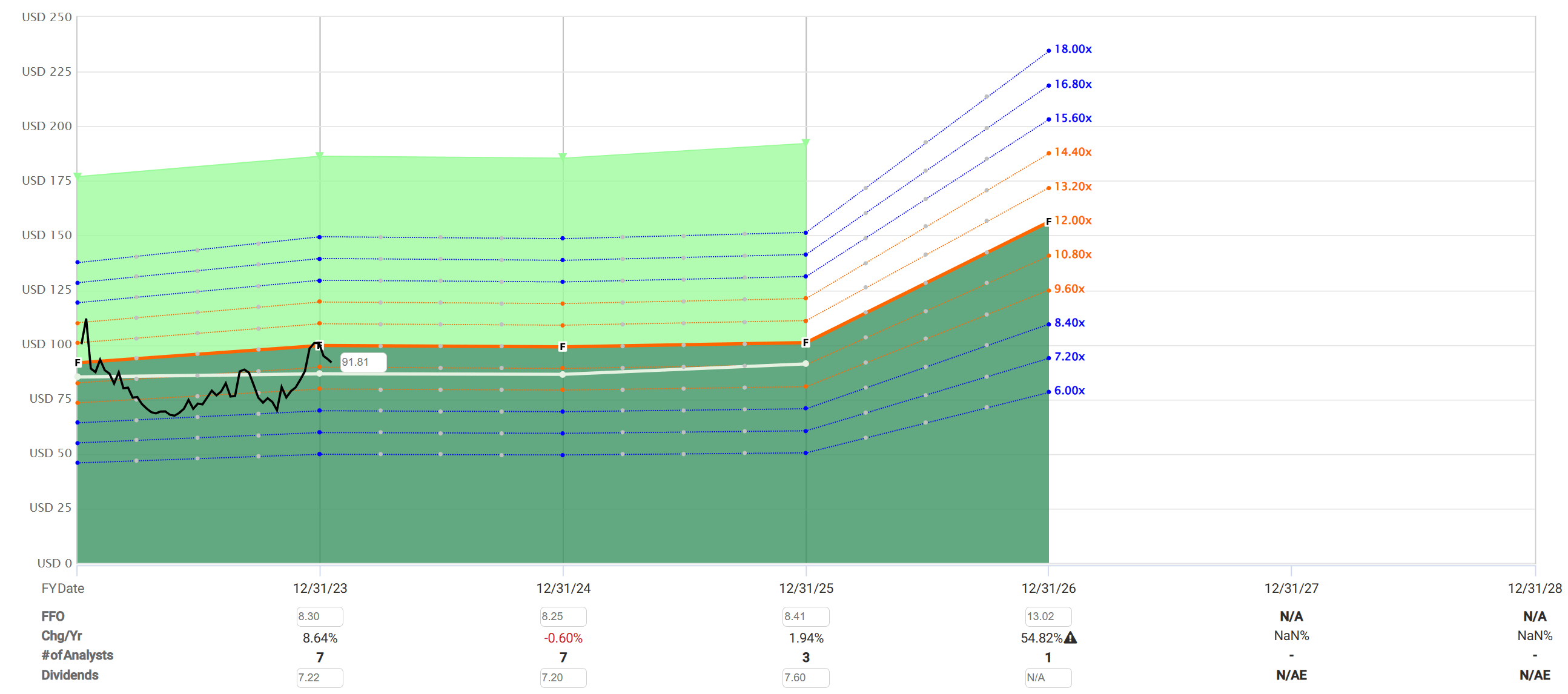

You can see this if you begin to look more closely at IIPR's forecasted growth rates, which are a hair negative for 2024, but are expected to turn back to the positive side in FY 2025:

{kind=link}

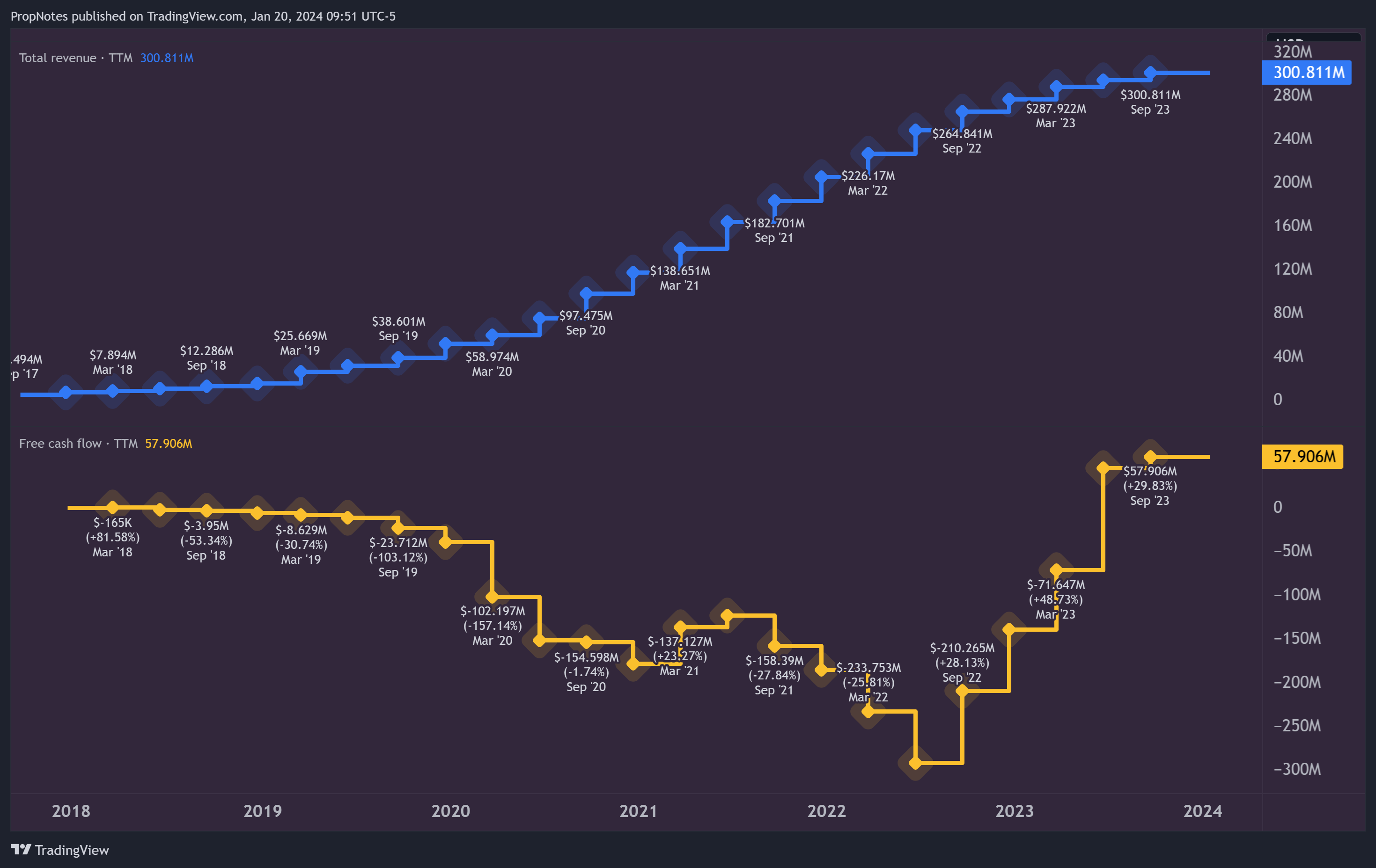

Zooming out historically, this 'recovery' narrative appears true when looking at the company's top line growth and cash flow, with TTM FCF finally in the black again following a period of challenges:

{kind=link}

This also pairs with a positive industry outlook. On a recent earnings call, CEO Paul Smithers had the following to say:

I would like to note that even during this macroeconomic environment, growth of the overall cannabis industry in the U.S. continues to remain strong, with BDSA projecting cannabis sales of $29.5 billion in 2023, representing approximately a 12% growth from 2022. Additionally, BDSA estimates that approximately 60% of U.S. adults could have access to adult-use cannabis by 2026 with new state programs coming online.

This doesn't necessarily mean that IIPR will see a lion's share of this growth given its tangential position as a landlord, but it does provide a better demand environment for its facilities over time which adds stability to our opinion of IIPR's future distributions.

Valuation

Pivoting now to valuation, if you look at the green chart above, you may be misled into thinking that IIPR is a great deal right now, as the blue line is plotting a 'fair value' of 30x FFO, and the orange line is plotting a fair value (based on historical FFO growth) of 19x.

To us, an FFO multiple closer to ~12x seems more appropriate, considering that IIPR's growth going forward is expected to be somewhat anemic. There is one lone analyst out there projecting 2025 FFO of $13 / share, which to us seems high:

{kind=link}

However, if you plot a 12x FFO, then IIPR appears to be trading right around fair value. This is also in line with the industry, which makes sense given the much slower growth trajectory that's been articulated by management and analysts.

More broadly, IIPR does have a widely diversified portfolio of operations, including a low level of concentration in any one customer or any one state :

Our portfolio continues to be well diversified with no one tenant representing more than 16% of our annualized base rent and no state representing more than 15% of our annualized base rent.

When combined with the pristine balance sheet, we're willing to extend our fair value FFO multiple estimate range to ~14x, which would put it at a slight premium to the sector.

Management does expect that growth will begin to re-accelerate in the future and that the current slowdown is due to the company positioning itself to capture that growth.

However, we're less certain about the growth outlook.

While industry growth should further secure the dividend as we mentioned in the last section, as a REIT, IIPR maintains a loose relationship with the growth of the regulated marijuana industry.

This has been a relative positive for the stock over the last couple years, as valuations and growth for top companies like Canopy ( CGC ) and Tilray ( TLRY ) have waned considerably.

However, on the flip side, IIPR should see less leverage to industry growth than producers, as an insulated real estate play going forward, if and when that occurs.

So, it's tough to see where exactly IIPR's growth will come from moving forward, and the company's organic sale-leaseback program isn't projected to materially boost growth either:

{kind=link}

The Dividend

So, where is the upside here?

Currently sitting at ~8%, IIPR's yield is the most attractive thing about the stock.

IIPR's FFO growth is slowing as the industry digests a number of ongoing challenges, and the stock itself (when priced on future growth) looks to be trading at something approximating fair value. However, the dividend looks quite appealing.

At present, IIPR pays out about 79% of FAD, which leads to an annual yield of 7.93% on a forward-looking basis.

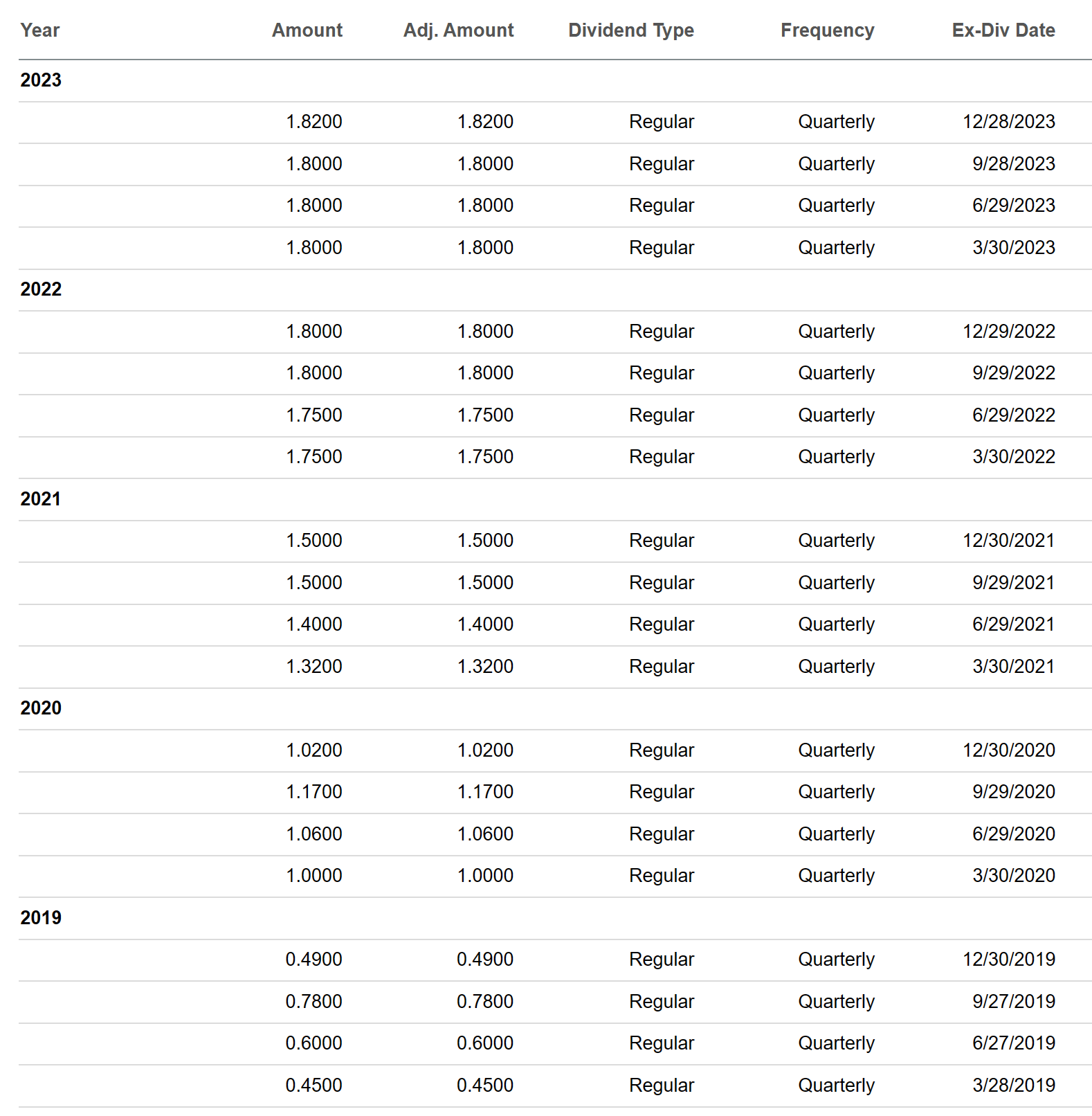

The company has grown this payout for 6 years now, from 2.32 per share in 2019, to $7.22 in FY 2023:

{kind=link}

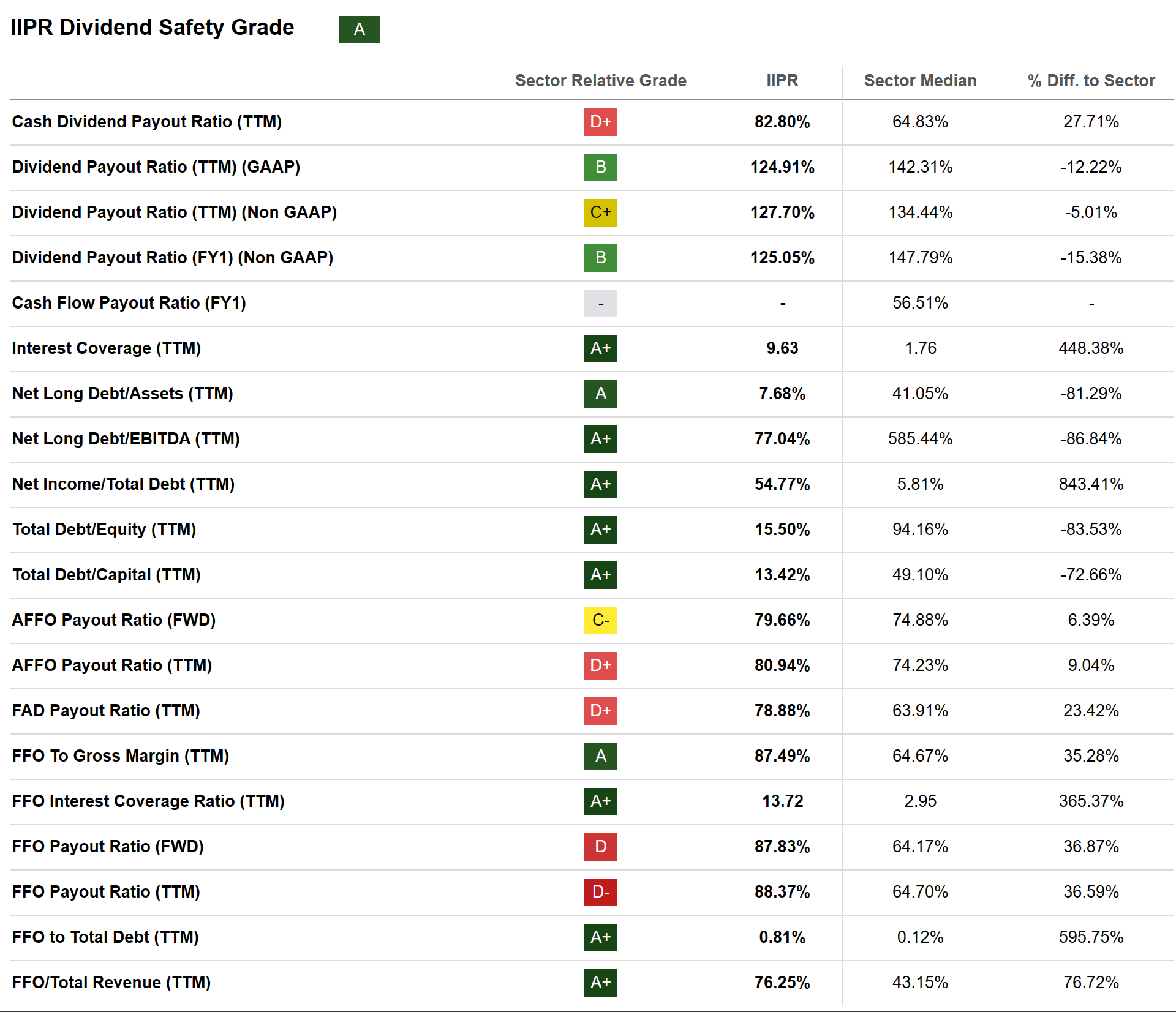

This growth has been admirably consistent and fast, but the real quality here comes when you take a look at the low level of overall risk:

{kind=link}

Seeking Alpha's Quant Rating System gives IIPR's dividend safety a grade of 'A', which is more than well-deserved when looking at some of the ratios.

Among these metrics is an interest coverage ratio of 9.6 (which is 4x higher than the sector), which indicates that IIPR has a low level of interest obligations that could get in the way of the company's future payouts.

Additionally, the company sports a very high FFO to Gross Margin percentage, which indicates that IIPR runs a very tight ship in terms of operating expenses.

Finally, IIPR's Total Debt / Capital (which we mentioned before) is very low, which indicates that the company's balance sheet is incredibly healthy. This is one of the main risks when it comes to investing in REITs - the leverage. If REITs are too highly indebted, then it can become an incredibly risky proposition being an equity holder, as banks and bondholders will eventually want their money back, which can severely constrain payouts, or prevent them entirely.

Thus, overall, it would appear that the dividend is very safe. As far as growth, it appears dependent on IIPR's FFO growth as a whole, which, as discussed, should be relatively weak.

Risks

There are a number of risks to IIPR's business, including regulatory issues and corresponding risks to the company's tenants. Here are a few ways this could manifest in reality:

- Cannabis industry changes: IIPR's business is heavily reliant on the legal status of cannabis. Any change in regulations, including prohibition or increased restrictions, could impact tenant demand and rental income.

- Tenant compliance: IIPR leases properties to cannabis operators, some of whom may face legal or compliance issues in the future. This could lead to defaults on rent, impacting IIPR's financial performance.

- Licensing delays: Obtaining state licenses for cannabis cultivation and processing is a complex and time-consuming process. Delays in licensing for IIPR's tenants could impact property occupancy and rent payments.

All of these could also impact IIPR's multiple, which has varied quite a bit over the years. In the past, IIPR has averaged an FFO valuation of ~30x, but if growth flatlines or dips into the negative, then our estimate of 12-14x FFO may be too optimistic, and the company's shares may be sold off further.

Finally, the company reports earnings in about a month and will continue to do so into the future, which always causes short-term volatility. For Q4 2023, we're expecting a modestly stronger quarter with a top line growth rate of 9.5% and marginal FFO improvements. However, if this changes or the market's reaction to the numbers is poor, then the stock could drop.

Summary

Overall, IIPR is an interesting case due to its highly robust existing operations but correspondingly weak growth profile. Thus, the shares themselves look fairly valued where they are, but the dividend appears strong and well covered.

For income seekers, it's a great option.

For those seeking capital appreciation, looking elsewhere might be more optimal.

Overall, we rate the stock a "Buy" due to its competitive Total annualized ROR profile, although we acknowledge that the stock may not be for everyone.

Cheers!

For further details see:

Innovative Industrial Properties: Dividend Safety Assessed