CA - InPlay Oil: Slow Growth Ahead

Summary

- InPlay went public through a reverse merger.

- The entities that originally backed this method of going public often have more resources available to management than is typically the case for this size company.

- The management emphasis appears to be on organic growth with an occasional bolt-on acquisition.

- The profitability enables a rare combination of growth, debt reduction and a small dividend. Much of the industry is focused on balance sheet repair instead.

- A basket of companies like this one should outperform the market and the industry in the future. Management experience lessens the typical small company risk.

(Note: This is a Canadian company that reports in Canadian Dollars unless otherwise noted.)

InPlay Oil (IPOOF)(IPO:CA), like many of the smaller companies, was formed with the backing of entities that know the industry. InPlay was originally formed by the reverse merge r with publicly traded Anderson Energy. The management originally decided to go public through the reverse merger back in 2016 when it looked like a typically good time in the business cycle to get in.

However, despite the success of many organizations with the strategy of going public during a time of weak prices (and then selling the company later in the cycle), 2016 turned out to be anything but an ideal time. The 2018 commodity price rally turned out to be incredibly short-lived. So many backers could not (or were not ready to) sell their companies. Then fiscal year 2020 was unusually challenging. That meant that a lot of past successful organizations either had to sell their companies at distressed prices or worse.

InPlay management navigated this rather challenging series of events to emerge at the current time as a relatively strong company. There does not appear to be that rush to acquire a lot of companies to gain size that one sees with other survivors. Instead, the area of operations appears to be good enough to allow the company to repay debt. There was one relatively small acquisition made in the past. That seems to fit the idea that acquisitions will be relatively rare with an emphasis on organic growth. To do that, profitable operations will be a key driver well into the future. That distinguishes this company from others like Tamarack Valley (TNEYF) where management wanted to gain a minimal size quickly to be a more effective competitor.

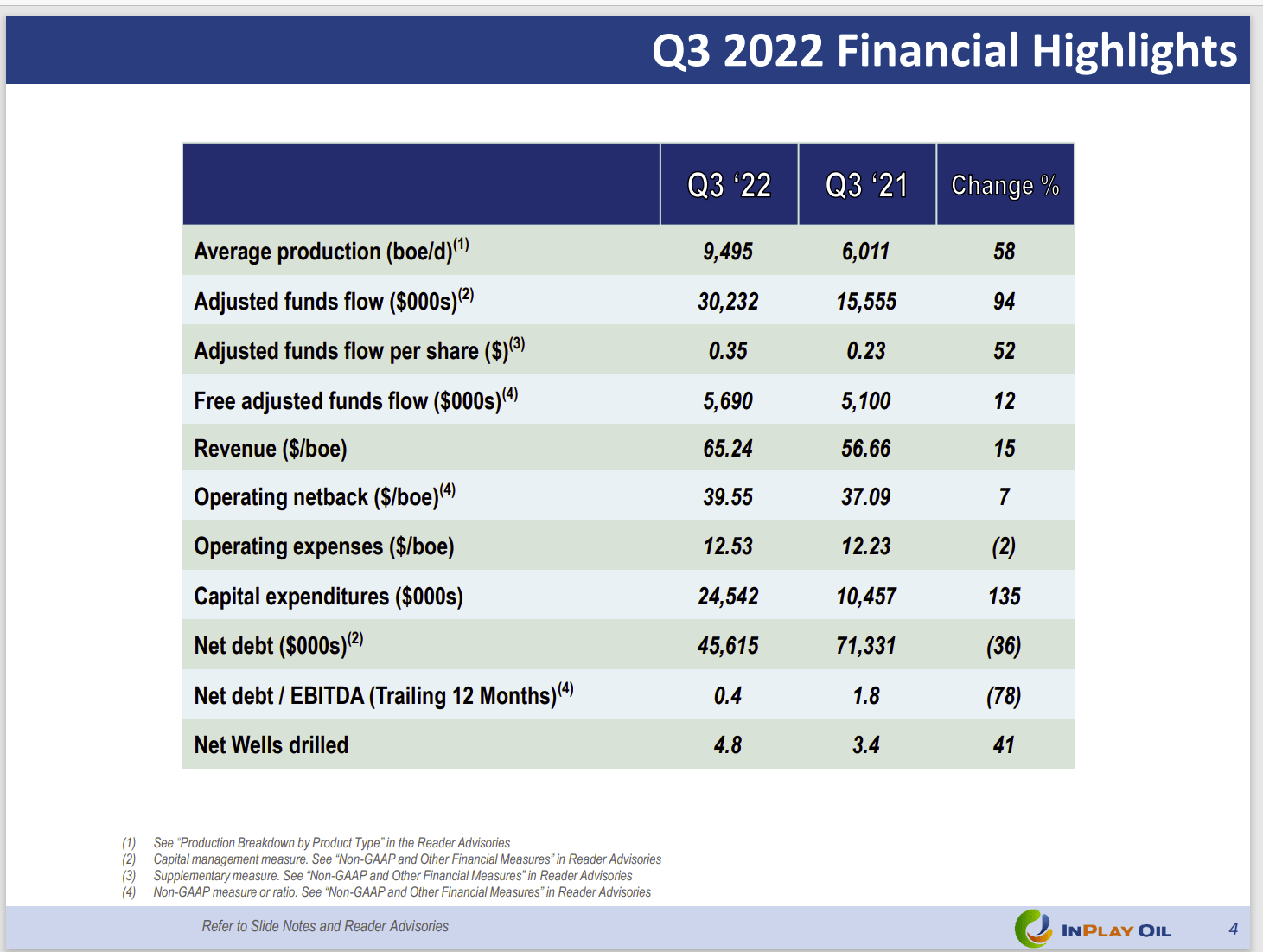

InPlay Oil Summary Of Third Quarter 2022, Operating Results (InPlay Oil January 2023, Corporate Presentation)

{kind=link}

Management has used the acquisition to grow production to nearly 10K BOED where some important cost savings are likely to begin to occur. For a small company, the results have been surprisingly good. That kind of lends credence to all the experience management touts before forming this company.

Management emphasizes the growth of the light oil part of the business in the 2023 guidance. This company is conservatively run. So, investors should expect steady growth with an occasional acquisition (probably small and "bolt-on").

A company like this one will attempt to show relatively rapid growth that is very profitable. The goal of backers of a company like this is to eventually sell the company for a good price. But the only way to do that is to demonstrate over time above average growth with above average profitability.

Therefore, investors looking for dividend income probably need to look elsewhere. The dividend yield will not nearly be as important as maximizing the long-term company value for an eventual sale.

This company, like many competitors has repaid a lot of debt so that another period of weak prices will keep the debt ratio down during that period. Canadian lenders generally think differently about the industry than United States lenders. Therefore, the ratios that happen during an industry downturn usually do not "raise alarms" as they do in the United States. However, the long-term goal of acceptable ratios has been impacted by the cyclical downturn in 2015 and again in 2020 just as it has in the United States. Therefore, Canadian companies will have acceptable debt levels that result in better ratios at far lower commodity prices than is the case right now.

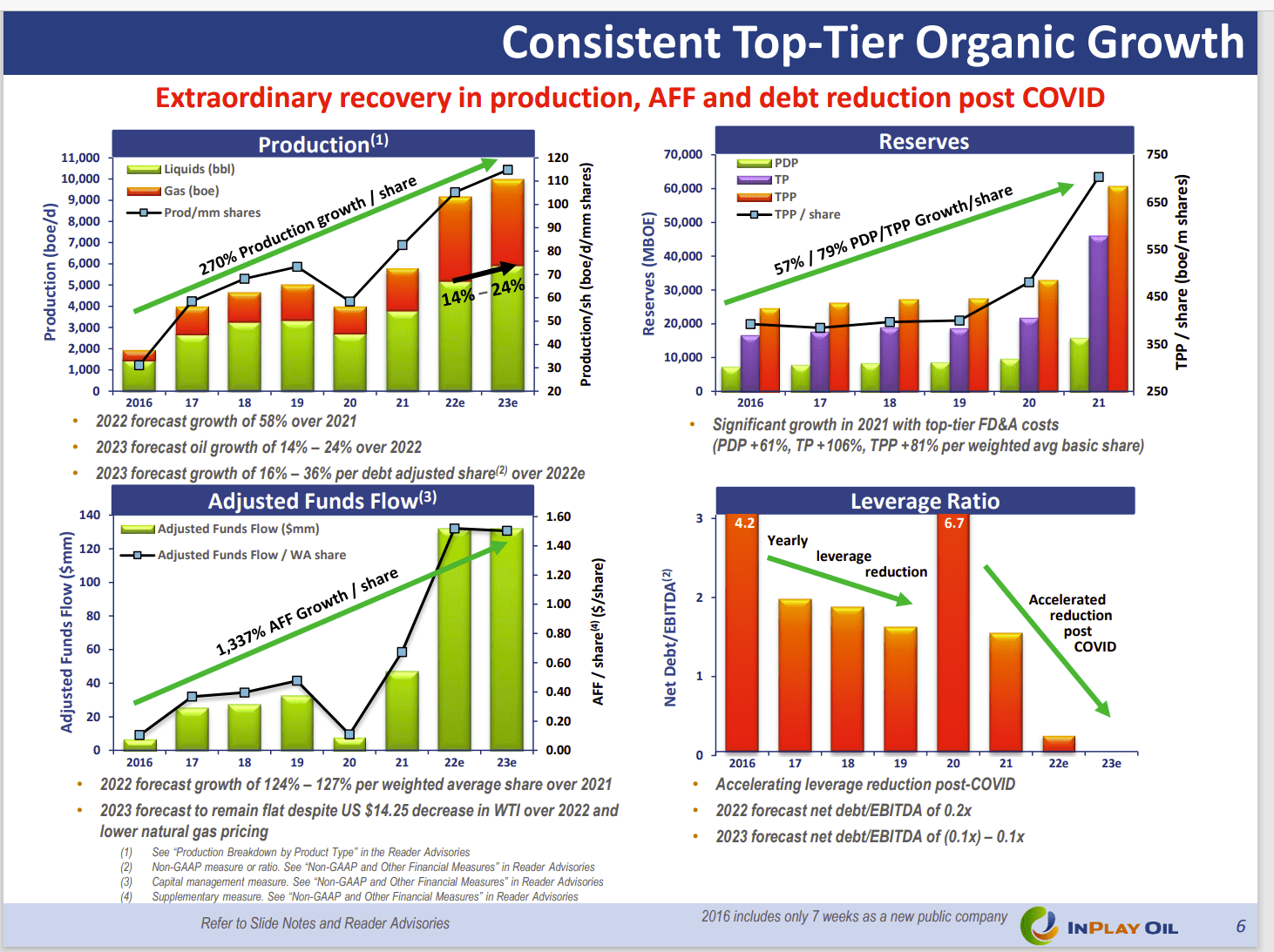

InPlay Oil Growth History As Measured By Management (InPlay Oil Corporate Presentation January 2023)

{kind=link}

Everyone focuses on profitability. The difference here is that when the debt ratios got out of line in fiscal year 2020, management fixed the situation with a small acquisition using some stock combined with a program to repay a significant amount of debt. That puts the profitability focus in a top tier range with few comparable situations. Most companies that I follow needed to acquire using stock and debt (to get enough acreage and production) to immediately improve the debt ratio.

The shareholder dilution was bigger even though the road to acceptable debt ratios was very necessary. Most acquisitions made (by various managements) were accretive on a per share basis. Here, there appears to be a focus on organic growth because that is seen as profit maximizing when the company is eventually sold.

It should be noted that growth will continue to be somewhat lumpy as shown above. Commodity prices are too volatile for a "straight line up". Leverage ratios will similarly gyrate in the future.

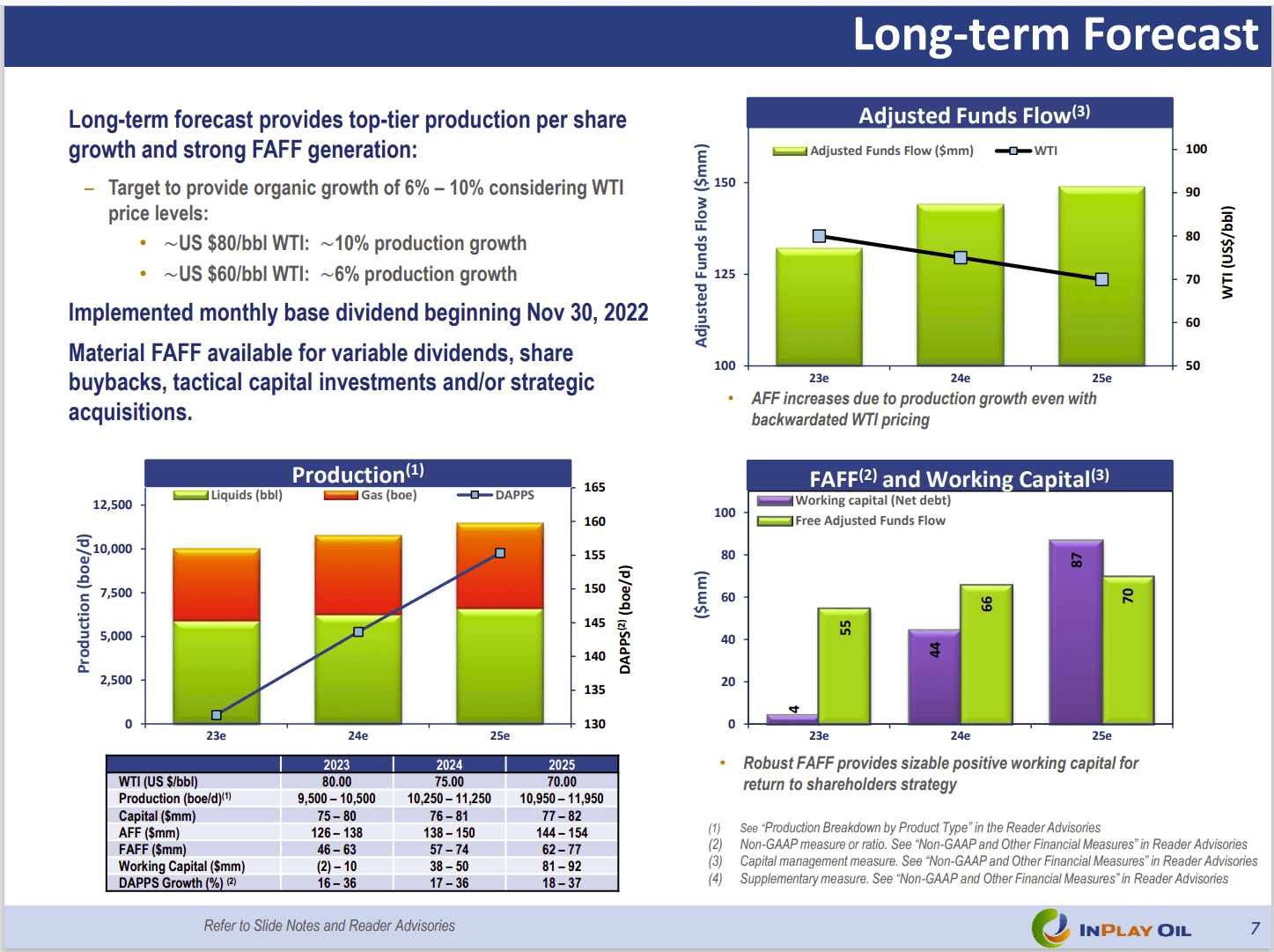

InPlay Oil Three Year Forecast (InPlay Oil Corporate Presentation January 2023)

{kind=link}

The advantage is that acreage is usually available and cheap for a company that wants to pursue organic growth. Management experience in previously building (and in some cases) selling companies makes this strategy attractive for a small company like this. The entities that were behind forming the company in the first place often have resources available to management that do not exist for similar size competitors.

As shown above, management is predicting an oil price decline. Yet they intend to grow production quickly enough to overcome the decline. But as noted before, the actual execution of the strategy is far more likely to result in lumpy growth given the volatility of the commodity prices.

The Future

Management has enough experience that the future strategy could change for the right price. This company is likely at some point to merge with another small company. But the Alberta operations appear to be very profitable for really any size company. So, until such a merger opportunity appears, this management has a very viable strategy of organic growth with an occasional bolt-on acquisition.

Management is also repaying long-term debt while establishing a small dividend. That also speaks to the profitability of operations because much of the industry is not growing at all while repairing the balance sheet.

The stock price, like many in the industry, has backed away from the high pint earlier in the fiscal year. But the enterprise value when compared to projected cash flow is in the very low single digits in most scenarios. Currently the enterprise value is in the $250 million range while cash flow is expected to exceed $100 million (in United States dollars) over the next twelve months.

A basket of companies like InPlay should outperform the market and the industry over the next few years. The industry is likely to return to historical multiples that are closer to 6 (instead of the current roughly 2.5) over time. So, the current recovery still has some "room to run".

For further details see:

InPlay Oil: Slow Growth Ahead