SKIN - Inter Parfums: Shares Have Gotten Cheaper Even After Soaring

2023-12-03 10:00:00 ET

Summary

- Inter Parfums has seen significant growth in revenue, profits, and cash flows, making it a promising investment opportunity.

- The company's performance has been driven by strong growth in the US market, new product launches, higher prices, and increased sales from existing offerings.

- Management has provided positive guidance for future years, with expected revenue and earnings per share growth, making it an attractive investment prospect.

One of the downsides about value investing is that it is easy to underestimate the potential of rapidly growing businesses. A great example of this can be seen by looking at Inter Parfums ( IPAR ), a firm that operates in the fragrance business and that produces and sells a wide array of fragrances and fragrance related products. Back in February of 2022, almost two years ago now, I wrote an article that took a rather neutral stance on the business. I recognized at that time that the company had fully recovered from the COVID-19 pandemic. I acknowledged that the future for the business looked bright in the long run. But at that time, shares of the enterprise were quite expensive. The forward price to earnings multiple of it, for instance, was 31.9. The forward price to operating cash flow multiple was 29.1, while the forward EV to EBITDA multiple was 17.9.

At the end of the day, this led me to rate the business a ‘hold’. But since then, management has really proven itself. Revenue, profits, and cash flows, have all risen significantly during this window of time. The stock has even gotten cheaper relative to each of these valuation metrics. Relative to similar firms, the stock is trading slightly on the cheap. But I wouldn't exactly call the business a value opportunity. Because of the attractive growth that the company continues to generate, however, I would say that some additional upside from here likely exists. So even though the stock is up 31.4% since I published that last article compared to the 0.3% seen by the S&P 500, I would argue that a soft ‘buy’ rating is appropriate at this time.

Great performance leads the way

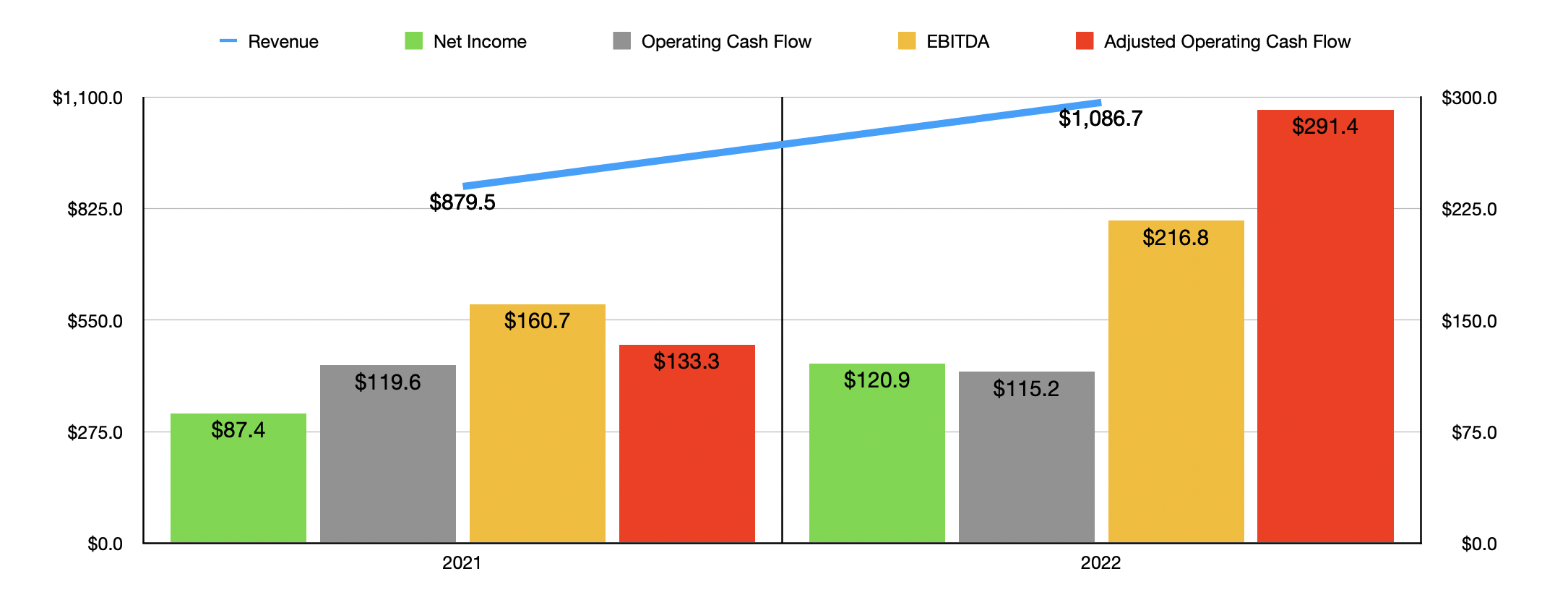

When I last wrote about Inter Parfums, the most recent data we had covered through the third quarter of the company's 2021 fiscal year. Since then, a great deal more data has come out, with the most recent data covering through the third quarter of 2023 . That's a lot of ground to cover. So to start with, let's touch on how the business performed during 2022 . During that year, revenue came in at $1.09 billion. That's 23.6% above the $879.5 million the company generated in 2021.

{kind=link}

Although the company is largely focused on the European market, it was the US market that was responsible for much of its growth recently. Back in 2020, only $116.1 million of the firm's revenue came from the US. That number has now more than doubled to $342.7 million as of the end of 2022. The increase during this time can be attributed to a combination of factors, including new product launches, higher prices so that the company charged customers for its products, and stronger sales from existing offerings.

With the rise in revenue also came higher profits. Net income skyrocketed from $87.4 million in 2021 to $120.9 million last year. That's a 38.3% increase that was driven in large part by higher revenue. However, the company also experienced growth in its gross profit margin from 63.3% to 63.9%. The improvement was spread across both its European and US operations, with a higher share of wholesale revenue, a favorable product mix, and the benefit of raising prices, responsible for much of this upside. Other profitability metrics followed suit. Operating cash flow did manage to decline from $119.6 million to $115.2 million. But if we adjust for changes in working capital, we get a massive surge from $133.3 million to $291.4 million. Meanwhile, EBITDA for the business expanded from $160.7 million to $216.8 million.

{kind=link}

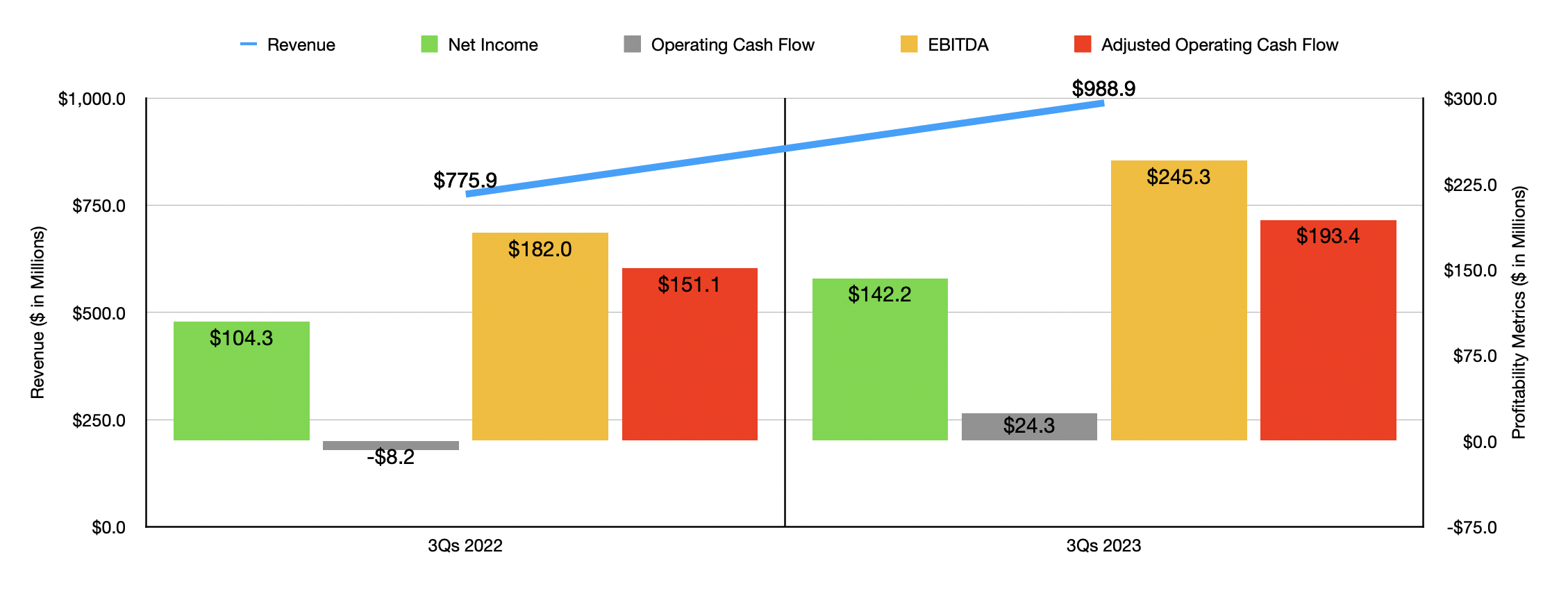

Financial performance for the business has continued to impress. Revenue in the first nine months of this year came in strong at $988.9 million. That dwarfs the $775.9 million generated one year earlier. Once again, it was the US market that led the way, with revenue rising 42.8% year over year. The continued success of the company’s Guess? ( GES ) branded fragrances really helped to push revenue higher. As a result, profits and cash flows also increased year over year. In fact, the picture is going so well that management has provided guidance not only for the rest of this year, but also for 2024.

For 2023, revenue is expected to be around $1.3 billion. That's 19.6% above what the company achieved last year. Meanwhile, earnings per share should be around $4.75. This should translate to roughly $152.6 million, which would be 26.2% above the $120.9 million reported last year. For 2024, revenue should climb further to $1.45 billion, while earnings per share of $5.15 should translate to profits of $165.5 million if share count remains unchanged. This gives us a lot to work with in terms of valuing the company.

{kind=link}

Given that the end of 2024 is still a ways off, I would like to focus our attention really on 2023. If we assume that other profitability metrics will grow at the same rate that earnings are forecasted to, then we should anticipate $367.8 million of adjusted operating cash flow and $273.6 million of EBITDA for the year. Using these figures, I was able to value the company as shown in the chart above. This chart includes not only the forward estimates for 2023, but also the historical estimates for 2022. As you can see, while the stock is pricey, it is quite a bit cheaper than when I last wrote about the business even though shares have risen materially. In the table below, meanwhile, I decided to compare Inter Parfums to the five companies I could find that were most similar to it. On a price to earnings basis and on an EV to EBITDA basis, two of the companies ended up being cheaper than it. This number drops to one if we use the price to operating cash flow approach.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Inter Parfums |

| 25.8 |

| 10.7 |

| 15.1 |

| BellRing Brands ( BRBR ) |

| 43.0 |

| 32.9 |

| 23.8 |

| Natura &Co Holding ( NTCO ) |

| 4.6 |

| 129.7 |

| 5.4 |

| Edgewell Personal Care Company ( EPC ) |

| 16.0 |

| 8.4 |

| 9.1 |

| e.l.f. Beauty ( ELF ) |

| 55.2 |

| 60.9 |

| 40.9 |

| The Beauty Health Company ( SKIN ) |

| N/A |

| 16.0 |

| 48.4 |

Takeaway

From what I can see, things are going really well for Inter Parfums and its investors. Growth far exceeded what I would have anticipated and even though shares are higher than they were when I last wrote about the company, the multiples that it's trading at do happen to be lower. I still don't see this as a value play. Rather, I see it as a GARP, or growth at a reasonable price, prospect. For those who do believe in management's guidance, I would say that a ‘buy’ rating makes sense at this point in time.

For further details see:

Inter Parfums: Shares Have Gotten Cheaper Even After Soaring