CA - InterRent: A Discount To NAV Doesn't Mean It's A Buy

Summary

- InterRent REIT focuses on residential real estate in Vancouver, Toronto, Montreal and Ottawa.

- The REIT is a very steady performer, but trades at very high multiples. I am not prepared to pay 28 times the AFFO.

- The payout ratio is approximately 70%, resulting in a 2.5% distribution yield, which also isn't particularly exciting.

- I do think InterRent will be able to absorb interest rate increases and will be able to deal with higher capitalization rates.

- A well-managed REIT, but I'm on the sidelines.

Introduction

InterRent REIT ( IIP.UN:CA ) ( IIPZF ) is a Canada-based residential REIT focusing on the Vancouver, Toronto, Ottawa and Montreal markets where it owns almost 130 properties with in excess of 13,000 suites . InterRent is a very stable performer and its management team has been able to continuously increase its rental income per suite, allowing the REIT to grow at a steady pace. However, that doesn’t make InterRent cheap.

{kind=link}

InterRent is a very stable performer and its management team has been able to continuously increase its rental income per suite, allowing the REIT to grow at a steady pace. However, that doesn’t make InterRent cheap.

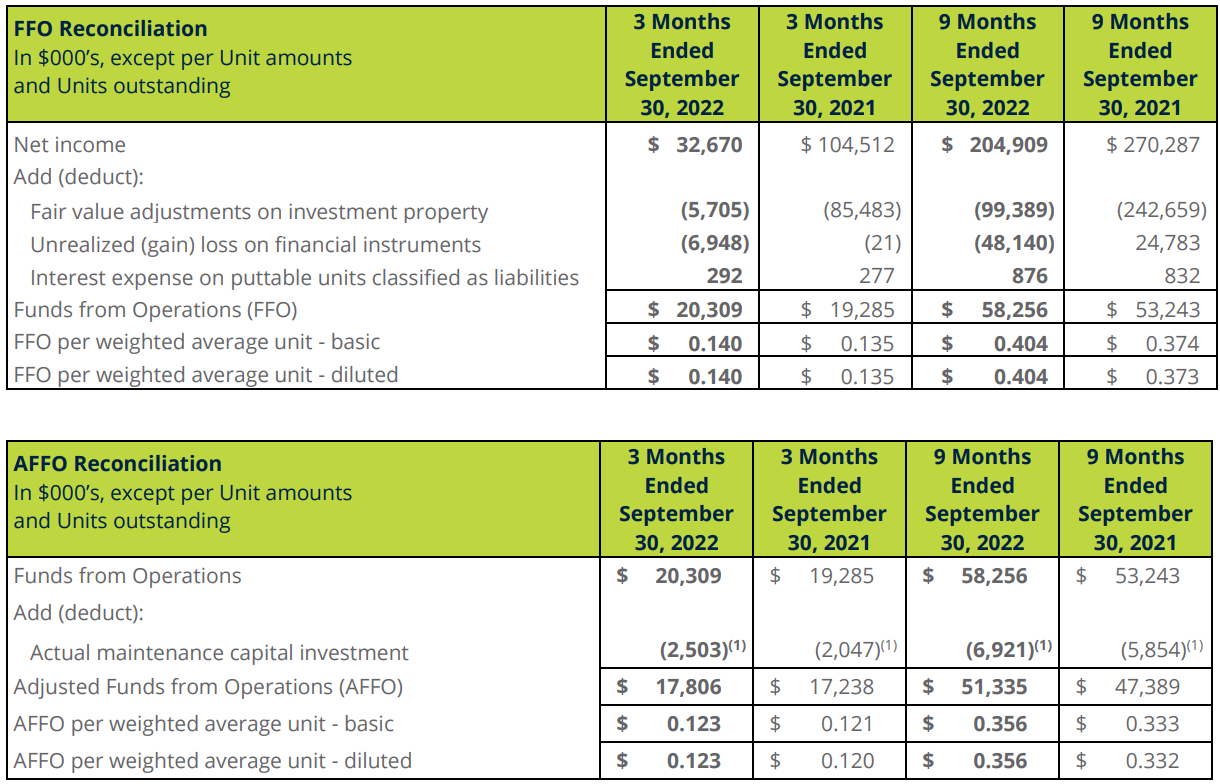

The FFO and AFFO are strong and increasing, but that doesn’t make the stock cheap

Based on the Q3 results, InterRent reported an FFO of C$0.14 per share and an AFFO of C$0.123 per share. That’s a nice improvement compared to the previous few quarters (the FFO and AFFO per share in the first half of the year were just C$0.264 and C$0.233 respectively), but even if you would annualize the AFFO you still end up with just C$0.50 per share.

{kind=link}

That makes the current share price of approximately C$14 pretty rich as it basically indicates a multiple of 28 times the AFFO. And while I understand and acknowledge residential real estate generally has high multiples, I am not keen to pay almost 30 times AFFO.

Of course there are important factors at play here as well, as the InterRent management has an excellent history of increasing the rental income per suite, and this trend is likely to continue in the foreseeable future.

{kind=link}

In normal times, an increasing rent will result in an increase net operating income and higher FFO and AFFO results. However, in the current climate of increasing interest rates, we can safely assume InterRent’s cost of debt will increase as well and those increased interest expenses will slow down the FFO and AFFO growth. This isn’t an InterRent-related problem, but a general sector problem that everyone will have to deal with.

The recently hiked dividend should be safe though. The REIT currently pays C$0.03 per month for an annualized distribution of C$0.36. This represents a payout ratio of just over 70% based on the annualized Q3 AFFO. The dividend yield is just over 2.5% which isn’t really appealing at all.

A closer look at how the book value fluctuates with changing capitalization rates

As interest rates are increasing the odds of InterRent being able to keep its capitalization rate below 4% are pretty close to zero as that would represent a mark-up of less than 120 basis points compared to the 5-year Canadian government bond yield. An additional issue of increasing interest rates is the impact on the interest expenses.

{kind=link}

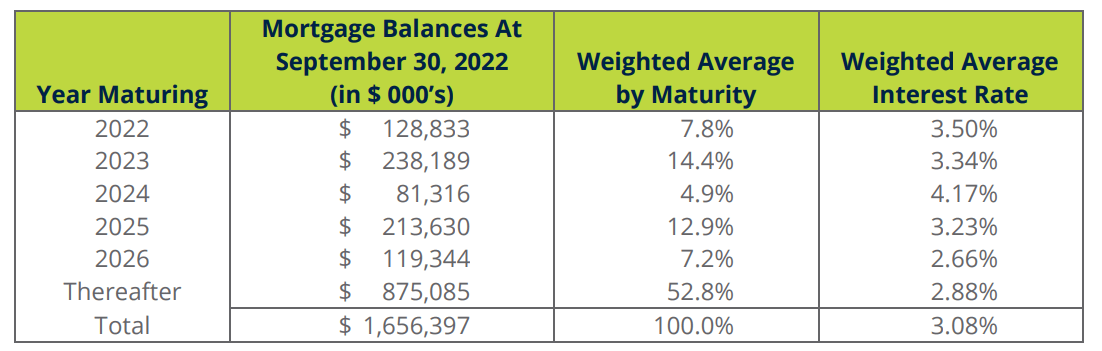

InterRent’s weighted average interest rate as of the end of September was just 3.08%, which is great. Additionally, the majority of the cheap debt (an all of the debt with an interest rate of less than 3%) matures in 2026 or beyond. This means the refinancings in 2023, when about C$238M of debt with a weighted average rate of 3.34% has to be refinanced, should be pretty benign. Even if the cost of debt increases to 5% upon refinancing the 2023 maturities, the impact should just be a few million dollar and could easily be covered by rent hikes.

That’s actually the main thing InterRent has going for itself: its debt structure is well-balanced and by the time the really cheap debt needs to be refinanced, the rent hikes should already exceed the interest cost increase. On its Q3 2022 conference call, InterRent’s management indicated it wanted to reduce the weight of its variable interest rate debt to less than 5% which should further improve the earnings visibility. So while the cost of debt will undoubtedly increase, I don’t expect the FFO and AFFO to be hit too hard.

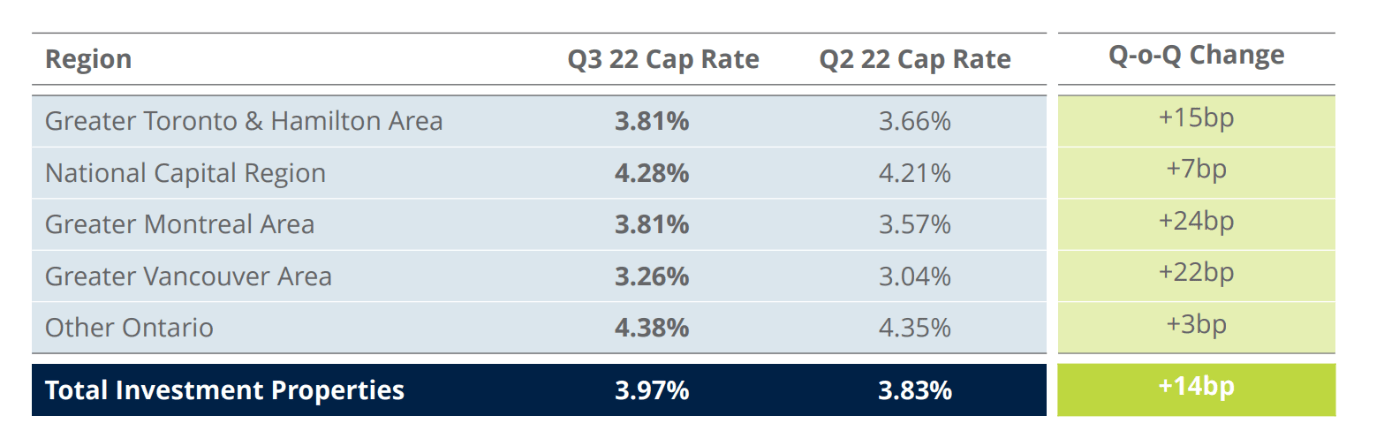

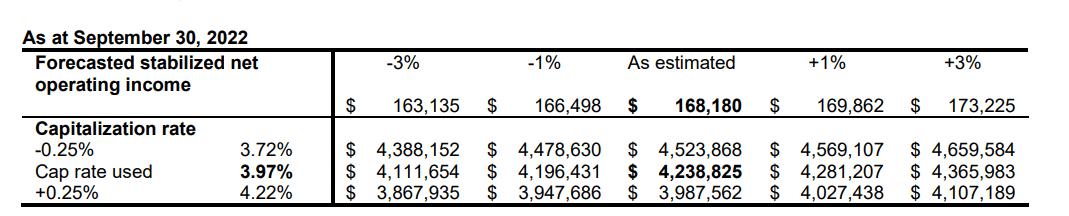

I am more worried about how the book value will be holding up in an increasing interest rate environment as the capitalization rates will increase as well. During the third quarter, InterRent already had to revalue its assets after a 14 basis point capitalization rate increase but I think even the current capitalization rate of 3.97% is pretty low.

{kind=link}

Based on that official capitalization rate, the book value of the assets is C$4.24B , as you can see below. Based on the 144.6M units outstanding (including the 3.41M units associated with the LP Class B units), the total equity value of C$2.645B would result in a book value of C$18.29.

{kind=link}

While that is great and indicates the stock is trading at a double digit discount to the book value, it is also clear that the fair value will be impacted pretty hard by an increasing capitalization rate. As the image above shows, for every 0.25% increase in the capitalization rate, the fair value of the properties decreases by in excess of C$250M.

This means that if you would use a capitalization rate of 5%, the book value of the assets would decrease by about C$1B, or roughly C$7/share. Fortunately a higher benchmark interest rate also means the REIT should be able to hike its rental income and the table above also shows that a 3% increase in the NOI increases the fair value by about C$130M.

So if we would increase the NOI by 5% in 2023 and subsequently again by 3% in 2024 while applying a 4.75% and a 5% capitalization rate, the fair value of the assets would come in at respectively C$410M and C$600M which would have a negative impact of respectively just under C$3 and just over C$4/share. Which means InterRent is currently trading at the fair value indicated in the latter scenario.

Investment thesis

InterRent REIT is not cheap on any metric. The P/AFFO is approximately 28 based on the annualized Q3 results, the dividend yield is just over 2.5% and although the stock is trading at a 25% discount to the NAV/share, that NAV will come down if the capitalization rates increase in the coming quarters and years. And considering the InterRent is retaining just C$0.14 per year in earnings, the book value per share will not increase fast.

Because of these reasons, I’m currently not interested in a position in InterRent. The management is doing an excellent job, but that doesn’t make the stock cheap.

For further details see:

InterRent: A Discount To NAV Doesn't Mean It's A Buy