IOVA - Iovance: Approval For Historic Solid Tumor Targeting TIL Therapy Likely Outlook Promising

2024-01-21 12:04:40 ET

Summary

- Iovance's tumor infiltrating lymphocyte cell therapy candidate, lifileucel, has shown promising results in a study of melanoma patients, with a 31.4% overall response rate.

- Lifileucel uses a novel mechanism of action to treat stage IV melanoma and has the potential to address an unmet need in solid tumor treatment, and drive revenues >$1bn p.a.

- The FDA has accepted Iovance's Biologics License Application for lifileucel, with a Prescription Drug User Fee Act date set for February 24th.

- Despite concerns around safety and durability, after many years of studies and conversations with the FDA, the signs point toward the therapy being approved.

- This ought to give the stock price a lift, although the market remains cautious around TIL cell therapies, and the competition is fierce.

Investment Overview

I last updated on Iovance (IOVA), the San Carlos, California based biotech, back in September last year, after a protracted market sell-off had reduced the company's share price from ~$6 per share, to a little over $3 per share.

For a full overview of Iovance's long and somewhat tortuous journey to becoming potentially the first company to secure a Food and Drug Agency ("FDA") approval for a cell therapy targeting solid tumors, I'll refer readers to my previous post , but to summarise, it took the company almost two years to submit a Biologics License Application ("BLA") to the FDA, after releasing positive data from its C-144-01 study of its cell therapy candidate, lifileucel, in melanoma, in April 2021.

The study looked at melanoma (skin cancer) patients who had progressed on immune checkpoint and BRAF/MEK inhibitors, and the data was collected from Cohort 2 of the study, showing the following results (source: Iovance press release ).

- Lifileucel showed a 36.4% overall response rate (4.5% complete responses and 31.8% partial responses) and median duration of response ("DOR") was not reached at 28.1 months of median study follow up as assessed by investigators (n=66).

- The Cohort 2 patients had heavily pretreated metastatic melanoma with high baseline disease burden. They have progressed on multiple prior therapies (3.3 mean prior therapies), including anti-PD1 and BRAF/MEK inhibitors if BRAFV600 mutation positive.

- The adverse event profile was consistent with the underlying advanced disease, lymphodepletion and IL-2 regimens, with no additional adverse events emerging over time.

The mechanism of action ("MoA") of lifileucel is summarised as follows by the United Kingdom's National Institute for Health and Care Research ("NIHR"):

Lifileucel uses a novel mechanism of action to treat stage IV melanoma for which there are currently no autologous tumour-infiltrating lymphocytes ("TIL")-based therapies recommended.

It is composed of a patient’s own naturally occurring immune cells TIL, which are prepared from a sample of cancerous tumour removed from the patient and multiplied in a laboratory until billions of TIL are obtained.

The expanded TIL are then administered via intravenous infusion back to the patient with the intention that TIL will target and infiltrate cancer in the patient and attack the cancer in greater number.

While several cell therapies have been approved to treat hematological cancers - e.g. Gilead Sciences ( GILD ) Yescarta and Tecartus, Novartis' ( NVS ) Kymriah, Bristol-Myers Squibb's ( BMY ) Abecma and Breyanzi, and Legend Biotech ( LEGN ) / Johnson & Johnson's ( JNJ ) Carvykti - these are all Chimeric Antigen Receptor, or CAR-T cell therapies.

The difference between this approach, and Iovance's approach with lifileucel, is explained as follows by the National Institutes of Health ("NIH").

While CAR T-cell therapy requires genetic modification of a patient's T cells to express receptors that can recognize and attack tumor cells rapidly, TILs involves extraction of immune cells from tumors and their proliferation in a laboratory before being infused back to the patient.

According to Iovance, 91% of all cancer cases are solid tumors, for which no CAR-T cell therapy has been approved to treat to date, hence, understandably, the market has previously valued Iovance stock as high as >$50 per share based on an opportunity to enhance standards of care in large markets where there is unmet need, for example the ~$9bn per annum melanoma market.

The series of delays since 2021, caused by managerial comings and goings, manufacturing issues identified by the FDA, and ongoing doubts about the safety, and durability of Iovance's approach, ultimately turned the market off of Iovance and lifileucel, but now that the FDA has accepted Iovance's BLA, and set a Prescription Drug User Fee Act ("PDUFA") date (when the agency announces if the drug meets its criteria for commercial approval) of February 24th, Iovance's share price has been creeping back up, trading at ~$8 at the time of writing.

Assessing Iovance's Initial Market Opportunity With Lifileucel

According to Iovance's Q3 2023 quarterly report / 10Q submission :

As of September 30, 2023, we had an accumulated deficit of $1.9 billion. In addition, during the nine months ended September 30, 2023, we incurred a net loss of $327.7 million.

In short, Iovance's progress to the point of a potentially major new therapeutic approval has not come cheap, although according to a recent corporate presentation , the company retains $428m of cash.

It is highly likely that, if lifileucel is approved next month, Iovance will move to raise further funding, as biotech's nearly always do when achieving a positive, share price needle moving milestone. I would not be surprised if the figure in question was in the region of $300 - $500m, similar to the raise completed by Madrigal Pharmaceuticals ( MDGL ) last September, for example, immediately after the FDA accepted its New Drug Application ("NDA") for its nonalcoholic steatohepatitis ("NASH") drug, resmetirom.

Iovance's research suggests that there are 15k new cases of melanoma diagnosed in the US annually, with 8k mortalities from the disease, while globally, there are 57k mortalities worldwide, and 15k within Iovance's ex-US target markets.

Bristol Myers Squibb's ( BMY ) LAG-3 inhibitor Opdulaog, approved to treat unresectable or metastatic melanoma in 2022, earned ~$450m of revenues across the first nine months of 2023, and although lifileucel's label would likely be restricted to later lines of therapy, management told analysts at the recent JP Morgan ( JPM ) Healthcare Conference that the drug could one day treat "several thousand" melanoma patients each year, and that lifileucel's list price would be "in the $440k range". If that were to prove to be the case, the therapy would be in line for the coveted "blockbuster" status i.e. sales of >$1bn per annum.

Whilst such a scenario would comprehensively makes the bull case for Iovance, given its current market cap of $2bn would surely increase upon the formal approval of a potential blockbuster drug, adding, in my estimation, around $1bn to its market cap at least, it's important to remember that the company will be in almost immediate trouble if the FDA does not grant commercial approval, with a funding runway that may not last much beyond the end of 2024 at current run rate.

Iovance would likely be forced to substantially streamline its operations in the event of lifileucel being rejected for approval, and depending on the FDA's reasons for rejection, potentially abandon other studies of its lead drug, for example in melanoma, in combo with Merck's ( MRK ) immune checkpoint inhibitor ("ICI") keytruda, as a first line therapy.

Lifileucel - Likelihood of Approval

On Iovance's Q3 2023 earnings call with analysts, the interim CEO and President Frederick Vogt updated analysts on the progress of the BLA as follows:

As a reminder, the FDA reiterated in September that there are no major review issues and no plans to hold an advisory committee meeting. In addition, all pre-approval inspections of all clinical sites and internal and external manufacturing and testing facilities have been successfully completed. The FDA has also engaged and has no concerns on the status of the TILVANCE-301 confirmatory trial, which remains on track to be well underway by the PDUFA date.

The fact the FDA will not carry out an advisory committee meeting, to discuss the approval with a panel of experts, is usually interpreted by the market as a positive sign that an approval will be granted, and when we also factor in the completed site inspections, status of the confirmatory study, and the fact the FDA has already delayed its decision by 3 months owing to "resource constraints", an approval come 24th February is seemingly the most likely outcome. It may have taken almost 3 years to move from positive pivotal study data, to commercial approval, but it is becoming hard to think of any more obstacles that can be placed in Iovance's path.

Iovance is beginning to look and sound like a commercial stage pharmaceutical company as opposed to a clinical stage biotech. The company has developed a "streamlined, 22-day GMP ("good manufacturing practice") manufacturing process, and has its own "built-to-suit", 136k square foot facility in Navy Yard, Philadelphia, which can presently treat hundreds of patients each year, management believes, with expansion plans in place to increase that number to >10k patients. The company has completed the acquisition of Proleukin, from Clinigen, in a $167m deal (plus milestones and royalties) - according to a press release:

Iovance expects the benefits of this transaction to include immediate and future revenue, securing the IL-2 supply chain and logistics surrounding TIL therapy administration

Finally, although doubts over the durability of lifileucel as a therapy have previously damaged Iovance's share price - most notably in May 2022, when updated data from the C-144-01 study revealed that lifileucel was "only" showing an ORR of 29% in the 87-patient, registrational Cohort 4, and a median duration of response of 10.4 months.

Despite these results arguing comparing favourably to current standards of care, the market - highly sceptical on the durability of cell therapies - dumped Iovance stock - based on Cohort 4 underperforming Cohort 2 on duration of response ("DoR") - which fell in value form >$15, to <$7.

Iovance's most recent study data shows that 42% of responses continued for >24 months across Cohorts 2 and 4 - 20 patients out of 48. The company presented data at the European Society for Medical Oncology ("ESMO") in December - according to ESMO Daily Reporter :

As presented at the Congress, 4-year findings from the study show a sustained benefit with long-term survival in at least 20% of patients involved (Abstract 119O). In the analysis, treatment with lifileucel was associated with 1-, 2-, 3- and 4-year overall survival ("OS") rates of 54.0%, 33.9%, 28.4% and 21.9% in 153 patients with advanced ICI-resistant melanoma. The objective response rate was 31.4% and the median duration of response was not reached.

Speaking at the conference, Prof. John Haanen from the Netherlands Cancer Institute, Amsterdam, Netherlands, commented:

It is remarkable that so many of these patients are still responding, given that this is a very difficult-to-treat population that has received all ICI options.

We know that TILs are here to stay in melanoma. The next challenge is how we can improve this treatment to make it easier and safer.

To summarise, my personal take would be that while the durability data for lifileucel looks good, the jury remains out on whether the therapy will prove to driven long-term complete responses in patients, outperforming standards of care. Doubts over durability are, however, unlikely to derail the approval of the drug, but could impact its commercial sales, or in a worse case scenario, cause the drug to be removed from the market.

In December the FDA began investigating CAR-T cell therapies developed by Johnson & Johnson ( JNJ ), Novartis ( NVS ), and Gilead ( GILD ), owing to " reports of T-cell malignancies after treatment with CAR-T therapies or chimeric antigen receptor T-cell therapies". Although each company says it is confident in the safety profile of its drugs, the investigation underlines how cautious authorities are about the long-term impact of cell therapies.

Looking Ahead - The Market's Perception Of Iovance's Value

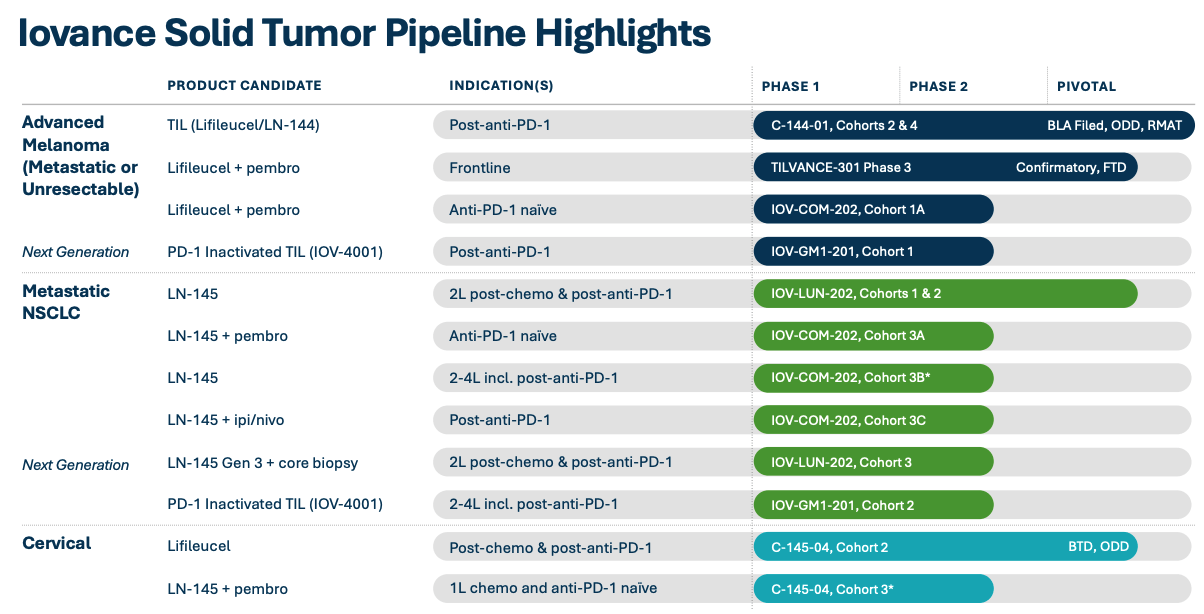

As we can see below, Iovance is not a single-drug company - besides lifileucel, it is running numerous studies for a second TIL asset, LN-145, in metastatic non-small cell lung cancer ("NSCLC") - the largest oncology market.

Iovance pipeline (Iovance presentation)

{kind=link}

This program ran into difficulties in December, after the FDA p laced a clinical hold on Iovance's Phase 2 IOV-LUN-202 trial of LN-145 after reports of a Grade 5 serious adverse event potentially related to the non-myeloablative lymphodepletion pre-conditioning regime patients must undergo before the TIL cells can be given to the patient.

There have been fears expressed that the LN-145 setback might affect the chances of lifileucel being approved, although the fact that Iovance's share price has been climbing in recent months, plus a note from Mizuho confirming Iovance management clarified that the death in the LN-145 study was officially classified as due to disease progression, provide some comfort that the FDA's move may been more due to an abundance of caution than a clear issue with the therapy.

With that said, Iovance's share price has been falling across the past few days - from >$10, to $7.8 at the time of writing. In my view, this suggests the market still harbours doubts about lifileucel, either due to concerns on durability and safety (although the safety profile is likely acceptable from an approval perspective, 95% of patients experienced >1 grade 3/4 treatment emergent adverse event in the pivotal study, and this is by no means an easy therapy for patients to stomach), or due to concerns about peak revenues potential.

In my view, in terms of the investment proposition, you can arguably look at Iovance in three different ways.

Firstly, that the company is on the brink of an historic breakthrough significant enough to support a market valuation far higher than Iovance's current $2bn market cap, given the fact that Iovance is ahead of the competition in a field of treatment that answers a substantial unmet need, not only in melanoma, but potentially multiple other solid tumor cancers besides.

Secondly, that Iovance does not have the perfect cell therapy solution by any means, but that lifileucel's approval represents an opportunity to enter the commercial markets and compete against standard's of care in a real-world setting, which will either establish TIL cell therapy as a viable therapeutic option with genuine blockbuster revenue potential, or a treatment of last resort capable of generating not much more than ~$250m per annum.

Thirdly, that the risks associated with the drug are too great, and that the FDA ought not approve lifileucel, and ask Iovance to complete more studies before re-submitting its BLA.

In the first scenario, the upside opportunity is clear - lifileucel will hit the ground running from a commercial launch perspective, and investors are virtually guaranteed a share price spike on approval, and an even higher valuation over time as revenues beat the market's expectations.

In the second, although we may not see much in the way of a spike upon approval, due to concerns around the commercial opportunity, the longer-term upside opportunity, with Iovance poised for approvals in earlier line melanoma, alongside keytruda, or even in NSCLC, is potentially exciting. In the third, Iovance, as mentioned earlier would be beset by problems, with an unapprovable drug and dwindling finances.

Ultimately, given I see two broadly positive outcomes for Iovance stock, and believe an approval in late February is more likely than not, I favour the bull case.

The market is right to have concerns around what is undeniably a new and radical approach to treating solid tumor cancers, but ultimately, after so many years of research, setbacks, data collection, and to-ing and fro-ing with the FDA, it is now or never for Iovance, and I believe it can be now. I therefore expect to see the market accept the FDA's endorsement of the drug as a derisking of the investment opportunity, and give the share price a sunstatial lift at the end of February.

Longer term, I also believe the outlook is promising for Iovance, as the company can raise massive funding to complete existing and future studies and try to maintain its present competitive advantage as the most advanced TIL cell therapy company.

I would also issue a caveat - competition in pharma and biotech markets is fierce, and Iovance will not necessarily have its first-mover advantage for long. Below is Iovance management review of its competition, taken from the company's 2022 10Q submission:

Due to the promising clinical therapeutic effect of competitor therapies in clinical exploratory trials, we anticipate substantial direct competition from other organizations developing advanced T-cell therapies targeting patients who have received prior anti-PD-1/-L1 therapies. In particular, we expect to compete with other new therapies for our lead indications developed by companies such as Agenus ( AGEN ), BeyondSpring ( BYSI ), Bristol-Myers Squibb ( BMY ), Merck ( MRK ), Nektar Therapeutics ( NKTR ), Checkmate Pharmaceuticals, Daiichi Sankyo, Eisai, Exelixis ( EXEL ), Moderna ( MRNA ), Mirati Therapeutics ( MRTX ), OncoSec Medical, Replimune ( REPL ), Regeneron Pharmaceuticals ( REGN ), Seagen, and Genmab.

We also may compete with other TIL therapies in development by companies such as Instil Bio ( TIL ), Achilles Therapeutics ( ACHL ), KSQ Therapeutics, Obsidian Therapeutics, Immatics ( IMTX ), TILT Biotherapeutics, WindMIL Therapeutics, GRIT Biotechnology, Lyell Immunopharma, Cellular Biomedicine Group, and others.

For further details see:

Iovance: Approval For Historic Solid Tumor Targeting TIL Therapy Likely, Outlook Promising