IOVA - Iovance: Hard To Resist This Historic Solid Tumor Cell Therapy Approval Shot

2023-05-31 08:00:00 ET

Summary

- Iovance is a cell therapy pioneer with a shot at a first ever approval for this drug class in a solid tumor cancer.

- Data from Iovance's pivotal study looks relatively strong and the FDA has finally accepted the company's BLA after pushing for more data first time around.

- The delays submitting its BLA have cost Iovance a large chunk of its market cap valuation, which once stood >$4bn - if lifileucel is approved Iovance may recapture that value.

- The decision date on approval is set for November 25th - the market opportunity could even be a blockbuster one and there are other approval opportunities in play.

- In short, IOVA makes for a risk bet but one that biotech market watchers may find hard to resist.

Investment Overview

I last covered Iovance ( IOVA ) for Seeking Alpha over 3 years ago in April 2020, when shares traded ~$35 per share. Although the stock price did reach a high of >$50 in Jan 2021, it collapsed shortly afterwards when Iovance reported that it would delay its Biologics License Application ("BLA") for lead asset lifileucel to treat melanoma, and also announced the resignation of its CEO, Maria Fardis, who had led the company since 2016.

Iovance stock continued to fall throughout 2021 and 2022, despite the progress of lifileucel towards a full FDA approval - in May last year, underwhelming data from the fourth cohort of its pivotal study that saw the objective response rate ("ORR") fall to 29%, versus an earlier cohort 2 readout that suggested an ORR of 35%, saw the stock price fall by half, hitting a new low of $7 per share.

Despite the apparent setback, however, this week the FDA agreed to accept Iovance's rolling BLA, which began in August 2022, setting a target decision date of November 25th, 2023. If approved, lifileucel could become the first ever approved cell therapy for a solid tumor cancer, which would be a momentous achievement.

Iovance's market cap valuation may have slipped from >$4bn, to $1.94bn at the time of writing, but that remains a relatively high figure for a pre-commercial biotech - anyone considering buying Iovance stock should acknowledge that drug development is a highly risky process and the FDA's acceptance of Iovance's BLA is absolutely no guarantee that the product will be granted approval.

The cell therapy space has witnessed some notable success stories in recent years, with the approvals of Gilead Sciences ( GILD ) Yescarta and Tecartus, Novartis' ( NVS ) Kymriah, Bristol Myers Squibb's ( BMY ) Abecma and Breyanzi, and Legend Biotech ( LEGN ) / Johnson & Johnson's ( JNJ ) Carvykti. The 2 Gilead drugs drove $1.5bn of revenues in FY22 - up 68% year-on-year, whilst BMY is confident both of Abecma and Breyanzi will achieve blockbuster (>$1bn per annum) status before 2030.

All of these cell therapies have been approved to treat hematological, as opposed to solid tumor cancers, however, and are CAR-T, as opposed to TIL therapies. The difference between the 2 approaches is explained by the National Cancer Institute as follows:

TIL therapy uses T cells called tumor-infiltrating lymphocytes that are found in your tumor. Doctors test these lymphocytes in the lab to find out which ones best recognize your tumor cells. Then, these selected lymphocytes are treated with substances that make them grow to large numbers quickly.

CAR T-cell therapy is similar to TIL therapy, but your T cells are changed in the lab so that they make a type of protein known as CAR before they are grown and given back to you. CAR stands for chimeric antigen receptor.

As promising a field as cell therapy is, it must be noted that outside of autologous (donor derived) CAR-T in hematological cancers, biotechs and pharmas have struggled to make tangible progress. Allogeneic therapies - where cells are collected from donors rather than extracted from a patient - have struggled to make progress in the clinic, and although theoretically natural killer ("NK") cells and TILs' could be as effective as CAR-T, approval shots - other than lifileucel - are few and far between, as is the case with cell therapies targeting solid tumors.

In fact, I recently covered 3 apparently promising companies developing allogeneic or solid tumor targeting cell therapy companies using CAR-T, or NK cells, Poseida Therapeutics ( PSTX ), Adicet Bio ( ACET ), and Atara Biotherapeutics ( ATRA ). Since my notes, however, cell therapy stocks have suffered a dismal bear run, and these 3 companies stock prices have fallen by 72%, 32%, and 66%. Perhaps I was backing the wrong horses.

Investing in a company such as Iovance - even after the positive news about the BLA, and a with a major potential upside catalyst - the approval of lifileucel - in play, is fraught with risk. For those prepared to embrace such risks, or are betting money they can afford to use, or with a strong interest in cell therapy, however, the upside catalysts can result in overnight, triple-digit gains for shareholders.

Let's take a closer look at Iovance the company, lifileucel, and the rest of the company's portfolio.

Iovance Overview - Pipeline Opportunities - Can Lifileucel Make History?

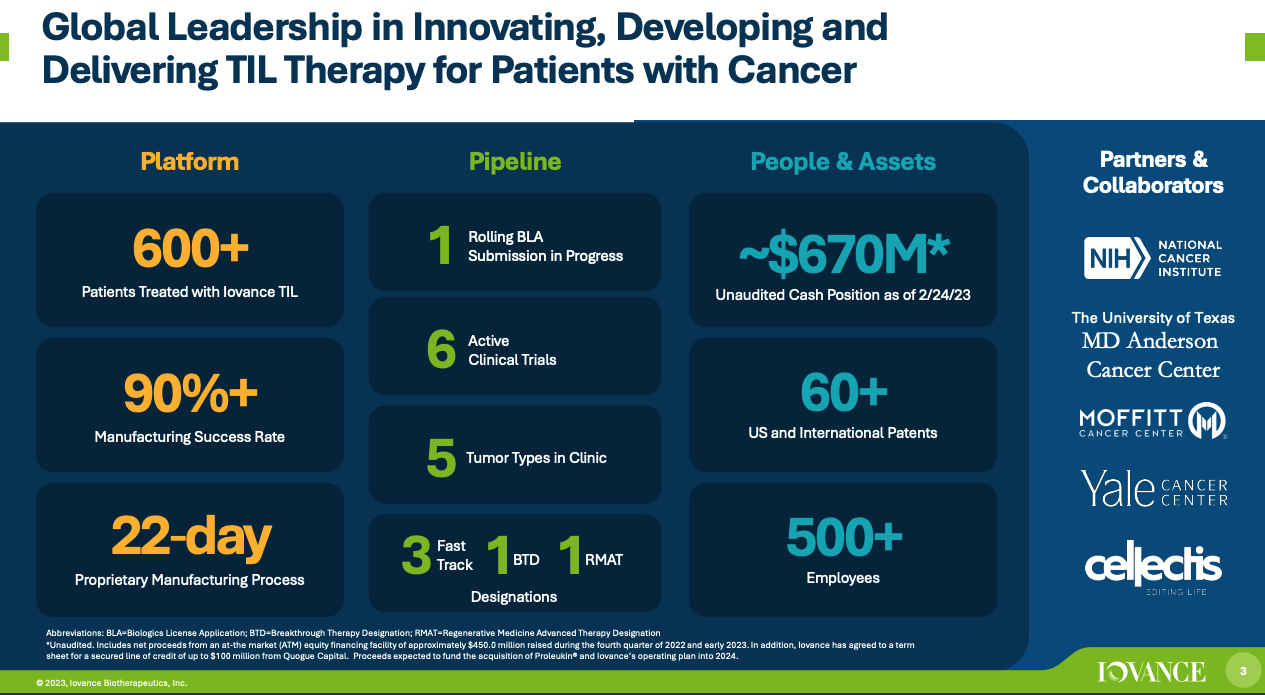

{kind=link}

The above slide is taken from a Iovance corporate presentation from January this year. One obvious positive would seem to be Iovance's strong cash position of $670m. In the company's Q123 earnings press release , that figure is quoted lower, at $628m, whilst net loss for Q123 was reported as $107m.

As strong as the current cash position may be, Iovance is a heavily loss-making company, reporting net losses of $(396m), $(342m), and $(260m) in the past 3 years, therefore it shouldn't be assumed that the cash runway will last much more than 18 months.

In short, Iovance needs lifileucel to gain approval, or another pipeline asset to deliver some promising data, before investors run out of patience and dump the stock for good.

{kind=link}

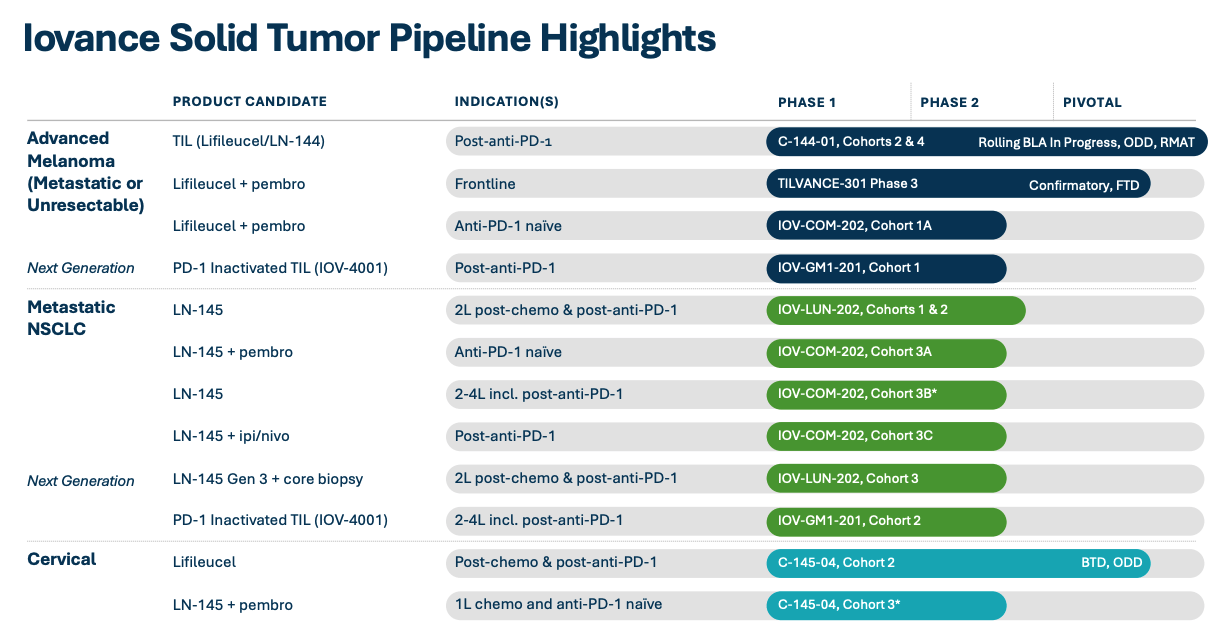

Turning to the pipeline itself, we can see that Iovance is still predominantly focused on the same two assets as it was back in 2020, lifileucel, and LN-145.

Lifileucel has progressed into Phase 3 pivotal studies, not only as a monotherapy, later line therapy for melanoma patients who failed to respond to treatment with an immune checkpoint inhibitor - e.g. Merck & Co.'s (MRK) standard of care ICI Keytruda - but also alongside Keytruda as a frontline treatment. The TILVANCE-301 study is, according to Iovance's 10Q submission:

intended to be registrational in frontline advanced melanoma and serve as a confirmatory clinical trial to support full approval of lifileucel monotherapy in post-anti-PD-1 advanced melanoma.

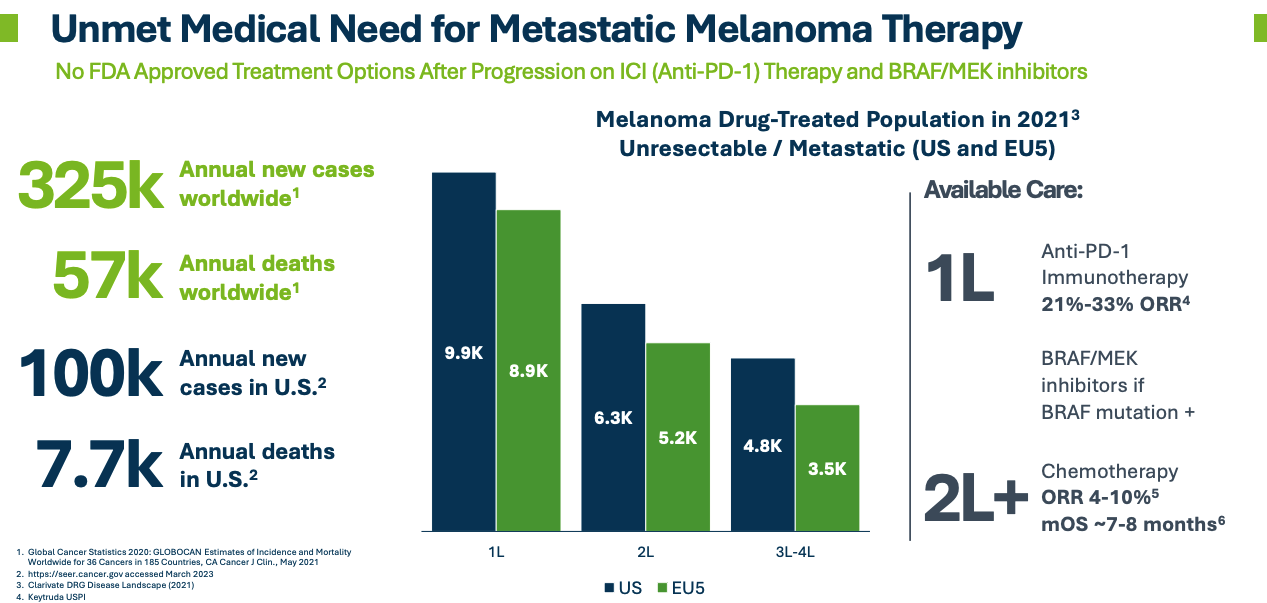

Keytruda, and Bristol Myers Squibb's CTLA4 inhibitor Yervoy are the current standard of care therapies for melanoma but for patients who fail to respond to these therapies, or surgery, or chemotherapy, there is a substantial unmet need, Iovance believes.

{kind=link}

The global malignant melanoma market will apparently be worth ~$8bn per annum by 2029, and Iovance believes the US incidence of unresectable or metastatic melanoma is ~15k patients. It is hard to estimate what the market opportunity for lifileucel is, but one very ballpark equation, based on the lower end of recommended list prices for approved CAR-T drugs of ~$300k, multiplied by the 15k unresectable or metastatic patients, would put it at ~$4.5bn, and a 20% share of such a market would imply there is a potential blockbuster (>$1bn per annum) revenue opportunity in play.

{kind=link}

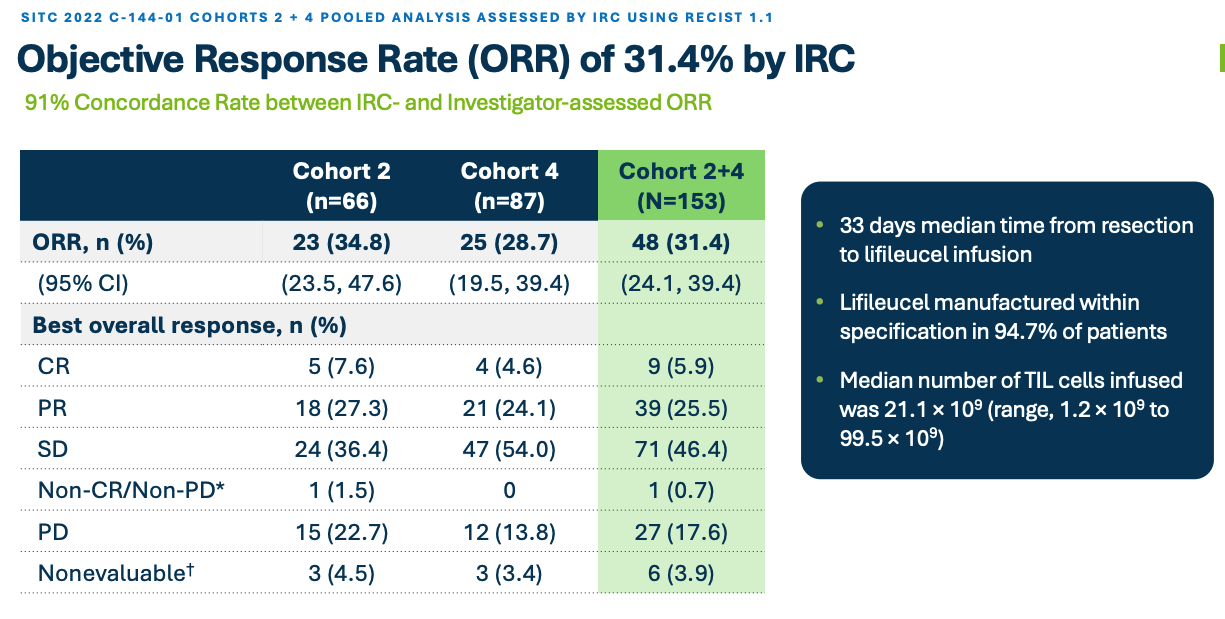

The data that the FDA will consider appears to be quite compelling - although the market was disappointed by the Cohort 4 ORR, the fact that 4 patients experienced complete responses is encouraging, and if more than 30% of patients are responding to treatment, the FDA may make history by approving a cell therapy for a solid tumor cancer.

Should that happen, I would not be surprised to see Iovance's share price and market cap double in value, to match former highs, although it may take several years for the drug to start generating meaningful - let's say triple-digit-million - revenues, as it did for the first approved CAR-T therapies.

As such, the opportunity in play for investors does look attractive, and there are more opportunities to consider. For example, the Phase 2 study of lifileucel in recurrent, metastatic or persistent cervical carcinoma is potentially pivotal i.e. positive data could be sufficient to secure FDA approval, and the first line Keytruda adjuvant opportunity is another exciting catalyst, potentially opening up a larger market opportunity that the later line approval.

Hope for LN-145 & Arrival of Proleukin

It is quite rare for a pre-commercial biotech to succeed with the only 2 assets in its portfolio, hence I would be a little cautious about assigning too much value to LN-145, although non-small cell lung cancer is the largest market in oncology and there are multiple studies ongoing - alongside Bristol Myers Squibb's ICI Opdivo, as well as Keytruda, and as a later stage therapy.

In one clinical study in a "heavily pretreated" patient population, LN-145 was able to achieve a 21% ORR, with long duration of responses of >37 months. That was as a single agent, whilst in combo with Keytruda, in the IOV-COM-202 study, according to Iovance's presentation 8/17 patients had a confirmed ORR, with 2 complete responses and 6 partial responses.

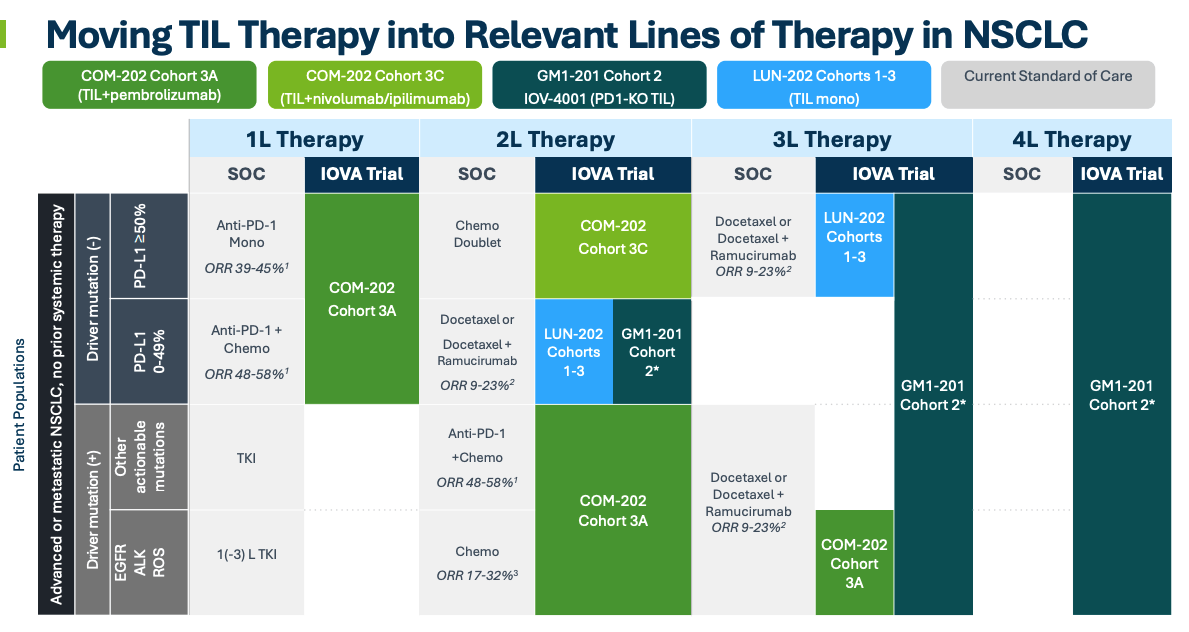

Iovance is bullish about the prospects for LN-145 and is already in discussions with the FDA about launching a pivotal study. Management even believes its therapy may have a role to play in 4 different lines of therapy, as shown below.

{kind=link}

Meanwhile, Iovance's interim President and CEO Fred Vogt (who took over from former CEO Maria Fardis, told investors on the Q123 earnings call :

Earlier this year, we entered into a strategic transaction with Clinigen to acquire worldwide rights to Proleukin, an IL-2 product with currently approved indications that is importantly also used to promote T-cell activity following TIL infusion.

We expect Proleukin to provide revenue and full control of the IL-2 supply chain and logistics surrounding TIL therapy, as well as a reduction in both clinical trial expenses and future cost of goods for lifileucel.

Iovance paid $200m upfront for Proleukin, and will pay an additional $51m milestone payment should lifileucel secure approval. When Clinigen and Iovance first announced their partnership back in January 2020, Clinigen CEO commented in a press release:

Proleukin is the only approved IL-2 in the US and Europe that is currently being used in TIL therapy development and is an inherent component of these programs. This is a product that is involved in over 80 clinical trials in the US alone, which presents other similar opportunities for us to pursue.

Concluding Thoughts - A Historic Opportunity In Play, But Is Iovance A Buy, Sell, or Hold

As mentioned in my intro, discovering and developing cell therapies is a tough business to be in. Cell therapies - that I have studies at least - do deliver some strong results in hematological cancers with high ORRs and plenty of CRs, but that needs to be balanced against negatives such as the high price of therapy, the difficult preconditioning that patients must undergo, and the dangers of a patient's immune system rejecting cells which have been engineered ex-vivo, leading to potentially fatal side effects such as graft vs host disease.

Nevertheless, companies like BMY, Gilead, and Legend have been able to successfully manage these risks, and are well on their way to achieving blockbuster sales for their products.

Can Iovance achieve what BMY, Gilead and Legend have achieved, but in solid tumors, with TILs? There is persuasive evidence to suggest that the company already has, on a smaller scale perhaps, based on the >30% ORR achieved in melanoma, and there could be better data to come as a combo therapy, and although far less certain, from LN-145 in NSCLC.

The issue that has been gnawing away at Iovance's share price is the delay in filing its BLA, but with that hurdle now overcome, triggering a >60% rise in the share price, shareholders certainly have reasons to be cheerful. CEO Vogt does not believe the FDA will need to convene an advisory committee to debate the merits of lifileucel with a panel of experts before an approval decision is made, so everything hangs on the November 25th.

I have been stung by cell therapy companies before, and given the complexity of all cell therapies and the inherent risks, it is hard to state with any confidence that lifileucel is a certainty for approval.

There is also a great deal of competition in Iovance's target markets - not just from cell therapy companies of which there are a large number ( see my Poseida post for a full list ) but from many different types of drug - perhaps most notable is the partnership between Merck and Moderna on a personalised cancer vaccine targeting melanoma, which has been show to substantially cut the risk of death in a Phase 2b study.

In conclusion, there are plenty of reasons for investor to steer clear of Iovance as an investment opportunity - past performance, delays, the lack of a permanent CEO, funding concerns, safety, and the fact the final approval decision rests with the FDA.

Nevertheless, there is one very obvious reason to back the stock - the historic approval of a first ever solid tumor targeting cell therapy. Biotech investors may find such a catalysts a hard one to ignore, and as such, I am giving Iovance a "BUY" recommendation, with the caveat that this investment carries very serious risk of losses.

For further details see:

Iovance: Hard To Resist This Historic Solid Tumor Cell Therapy Approval Shot