IPO - IPOs In 2023 Disappoint But 2024 Looks Brighter

2024-01-03 13:55:46 ET

Summary

- The U.S. IPO market in 2023 had negative median returns and a decrease in the number of IPOs compared to 2022.

- Smaller Asia-Pacific companies and IPOs priced at $5 or lower contributed to the overall poor performance.

- The 2024 IPO market may see incremental increases in deal volumes, but the public market/private market valuation gap will likely continue for technology subsectors.

In 2023, the U.S. IPO market produced negative median returns on stabilizing deal volume.

Asia-Pacific region-based companies and $5 per share or lower IPOs were prominent in dragging overall performance down.

With cost-of-capital assumptions moving lower, the 2024 IPO market may see incremental increases in deal volumes. However, the public market / private market valuation gap, where private market valuations are higher than public valuations, will likely continue for technology subsectors.

2024 will likely feature a few selected quality IPOs sprinkled throughout the year.

I suggest investors focus on quality companies with a history of strong revenue growth coupled with reduced operating losses or growing profits.

With the potential for large private company IPOs in 2024 from the likes of Stripe (STRIP), Reddit (REDDIT) and Panera Bread, investors should gravitate toward IPO companies with significant track records and easily understandable business models, avoid hype-induced behaviors and be highly disciplined in IPO investment choices.

2023 U.S. IPO Activity Review

2023’s U.S. IPO market concluded with a total of 141 IPOs raising $22.2 billion in gross proceeds, excluding underwriter options and concurrent private placements.

Compared to 2022’s results of 166 IPOs that raised $18.3 billion, 2023 represented a 15.1% decrease in the number of IPOs and a 21.3% increase in the gross proceeds raised, resulting in a smaller number of larger IPO sizes.

The median return for all 2023 US IPOs through the end of 2023 was negative (22%), a poor showing likely reflecting the negative impact on valuations for growing but money-losing companies from a higher cost of capital environment.

By comparison, the median return for all 2022 US IPOs through the end of 2022 was 0.3%, a paltry result but far better than 2023’s substantially negative performance.

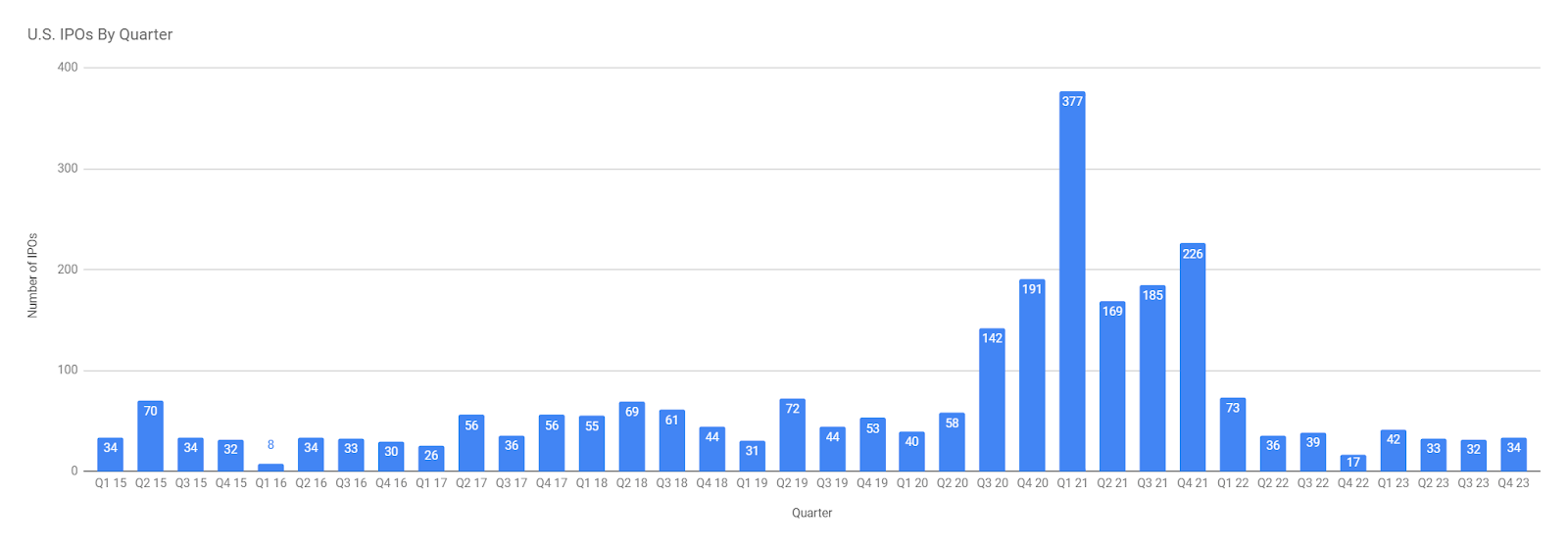

The chart below shows the number of U.S. IPOs on a quarterly basis since Q1 2015.

{kind=link}

The chart shows the sharp rise in IPO activity during the pandemic years of 2020 - 2021 as investors flush with stimulus cash invested in technology companies helped by the work-from-home movement.

This period was followed by a return to far lower numbers as the pandemic waned and inflation occurred, producing much higher cost-of-capital assumptions.

This, in turn, reduced IPO activity as valuations for money-losing companies suffered and management teams chose to delay their IPO plans.

The number of SPAC IPOs continued to drop sharply, producing only 27 IPOs for the year, a sharp reduction from 73 in 2022. Also, average SPAC IPO transaction sizes fell sharply, typically into the mid double-digit millions, from a more normal $100 million size.

The SPAC market was significantly altered by a critical rule change by the SEC, essentially extending liability for the initial IPO underwriter to include the later de-SPACing transaction and resulting exposure to not meeting performance claims. This resulted in virtually all major investment banks exiting the market.

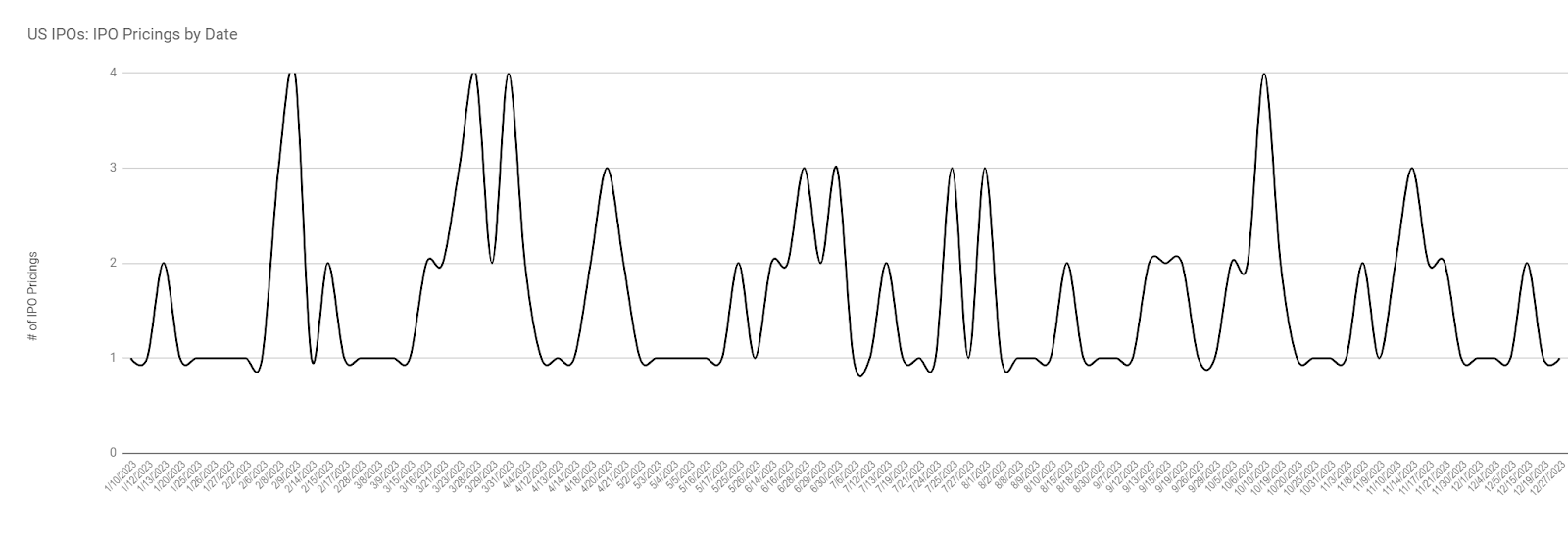

The chart below shows the seasonal variation of the number of IPOs throughout the year, with the first quarter being the busiest quarter of the year:

{kind=link}

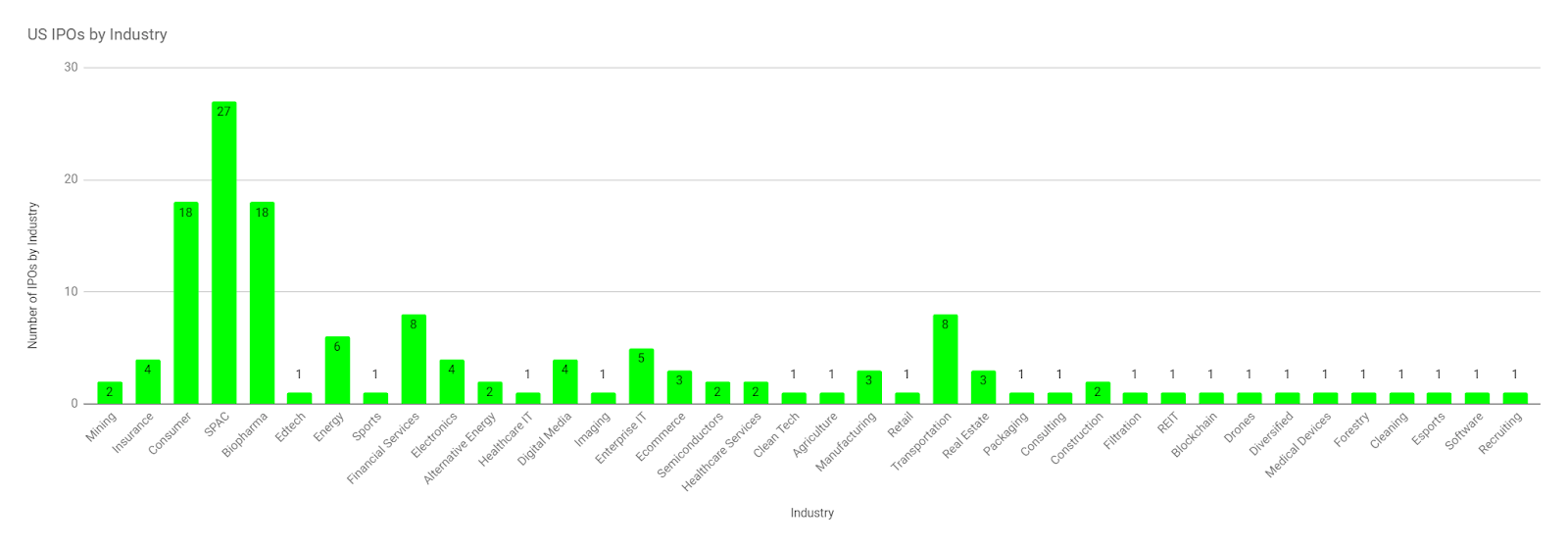

U.S. IPOs By Industry

During the year, a total of 38 industries were represented with at least one IPO.

Twenty industries had only one IPO, a wider distribution than in 2022, while 18 industries had more than one IPO, about the same as in 2022.

Here were the top five most active industries for U.S. IPOs in 2023:

-

SPACs led all industries with 27 IPOs.

-

Biopharma and consumer firms came in 2nd place with 18 IPOs each.

-

Financial services and transportation companies were each represented by eight IPOs.

-

Energy companies and enterprise IT firms accounted for six and five IPOs, respectively.

-

Insurance and digital media had four IPOs each.

The chart below shows the number of IPOs by industry during the year.

{kind=link}

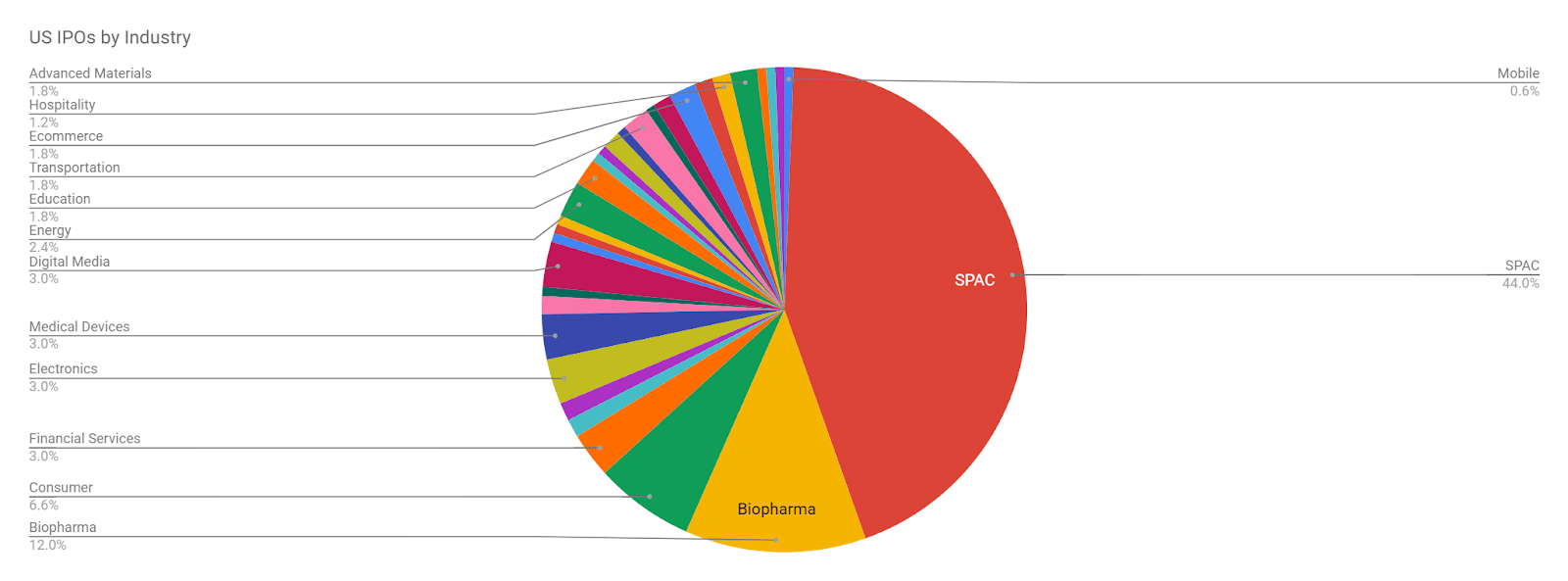

As a different way of visualizing the above information, the pie chart below shows the number of IPOs by industry, broken down as a percentage of the total:

{kind=link}

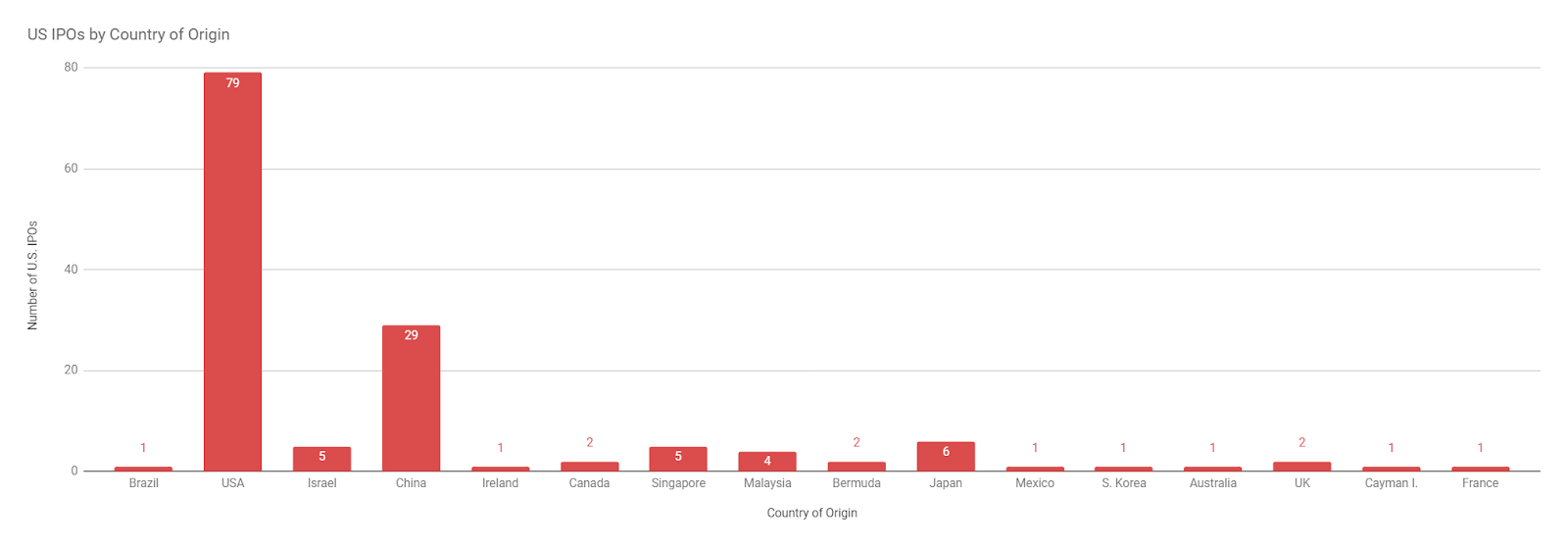

U.S. IPOs by Country of Origin

U.S.-based companies accounted for 79 of the 141 total IPOs, or 56% of the total, a much lower percentage than 2022’s 81%, highlighting increased international IPO sources during 2023.

-

China came in second place with 29 IPOs or 20.6%, up from 7.2% of the total in 2022.

-

Japan produced six IPOs, triple its 2022 count of only two.

-

Israel and Singapore accounted for five IPOs each.

-

Malaysia doubled its IPO output with four IPOs during the year.

-

Canada, the UK and Bermuda accounted for two IPOs each.

Below is a summary chart of IPOs by country of origin:

{kind=link}

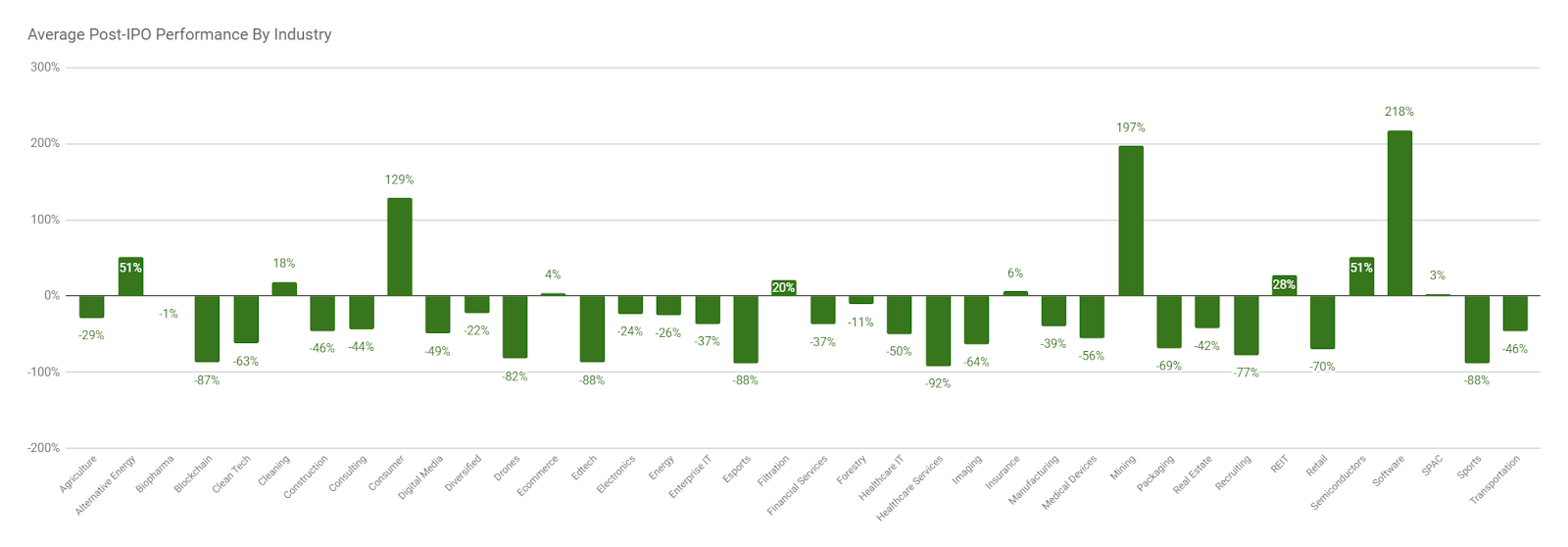

Average Percentage Return Since IPO by Industry

U.S. IPO returns ended the year performing poorly in the aggregate (a median drop of 22%), but 11 industries produced positive returns as of yearend.

Positive results were seen in the general software, mining and consumer categories, returning an average of 218%, 197%, and 129%, respectively, from their IPO date through the end of the calendar year.

The poorest performing industries included healthcare services, edtech, sports and eSports, as healthcare services dropped by 92% and the other three categories fell by 88% each by the end of the year.

A number of well-capitalized biopharma firms performed poorly post-IPO, including Adlai Nortye (ANL), down 61%, Acelyrin (SLRN), down 59%, and Turnstone Biologics (TSBX), which fell 79% from its IPO through year end.

The chart below shows average percentage returns since IPO by industry for all IPOs in 2023, from IPO date through calendar year end:

{kind=link}

Some of the largest IPOs by size were semiconductor technology company Arm Holdings ( ARM ) at $4.9 billion, Johnson & Johnson spin-out Kenvue (KVUE), which raised $3.7 billion, and footwear maker Birkenstock (BIRK), whose IPO was $1.5 billion in size.

Arm’s IPO returned 47% by year-end, while Kenvue’s and Birkenstock’s stock returns were negative (2%) and 6%, respectively.

2023’s Poorly Performing IPO Categories

Part of achieving investing success is determining what not to invest in to avoid losing money.

During 2023, two categories of U.S. IPOs generally performed poorly post IPO: Asia-Pacific companies and IPOs where the stock price was $5 or less.

In my estimation, the reasons for these poor performers included the following observations:

Small-cap Companies from Asia-Pacific countries:

-

These companies, which are most often from China but also come increasingly from other Asia-Pacific countries, are pitched by networks that work with small U.S.-based investment banks that are usually embedded within U.S. Asian communities in order to sell these shares to the Asian diaspora in the U.S. who may quickly sell their shares if the IPO doesn’t immediately "pop."

-

Asia-Pacific IPO companies typically are small firms with more complex legal structures - a Cayman Island domicile for the U.S. entity that may only have a contractual arrangement with the Chinese operating entity (Variable Interest Entity or VIE) or owns it as a Wholly Foreign-Owned (WFOE) subsidiary. So, U.S. investors don’t own stock in the operating entity.

-

Asia-Pacific company executives typically do not have a culture of communication with public shareholders that U.S. investors are accustomed to with larger, more established public companies. In general, I’ve found their communications tend to be the absolute minimum and are usually vague, ambiguous and contain general platitudes of little or no use to investors.

-

These types of firms also are subject to opaque regulatory changes that are unpredictable and tend to favor larger companies since Asia-Pacific regulators can more easily control a smaller number of large firms rather than a large number of smaller companies.

-

Asia-Pacific companies tend to avoid focusing on one business segment, instead choosing to dilute their focus and seek unrelated businesses, frequently producing mediocre results in the process.

Below is a table showing the negative (22%) median return of all Asia-Pacific company IPOs from IPO until the end of the year.

As a note of context, 40% of all US IPOs were up by the end of the year. With only 24% of Asia-Pacific companies up by the end of the year, the category performed poorly in this respect while producing a median return of negative 22%.

| Median Return - Asia-Pacific Country IPOs |

| -22% |

| Post-IPO Performance: |

| Up |

| 11 |

| 24% |

| Down |

| 35 |

| 76% |

Companies with U.S. IPO pricings at $5 or less:

-

These companies have priced their IPOs at $5 or less essentially to aim them at retail investors because management may not be able to get institutional or private investors interested.

-

They're usually very small, micro-cap-sized companies with little revenue, material losses or a short operating history.

-

Frequently, they're in digital-oriented industries long on "hype" and short on actual results.

-

Many times, they're "narrative" companies seeking to raise a few millions in investment based on their vision of the future, which may or may not come true.

-

Management typically has little direct industry experience or no previous quantifiable successes.

-

They are usually "emerging growth" companies or "smaller reporting" companies, which, per the 2012 JOBS Act, can choose to avoid many public disclosures that normal public companies are required to have. View a summary here highlighting the differences.

Below are the results for stocks priced at or below $5, indicating a median return of negative (20%) by year end, with only 14% above their IPO price compared to the overall market of 40%.

| Median Return - $5.00 or Less IPO Prices |

| -20% |

| Post-IPO Performance |

| Up |

| 8 |

| 14% |

| Down |

| 51 |

| 86% |

In sum, due to the poor performance of these types of IPOs, my general bias is to avoid small-cap Asia-Pacific company IPOs and companies with IPO prices of $5 or less unless there's a very compelling and unique set of reasons to invest.

(Source: Author’s IPO Database )

2023 U.S. IPO Market Commentary

The 2023 IPO market again saw a reduction in overall deal volume versus the previous year but an upward dollar amount of gross proceeds.

If 2022 was the "hangover after the pandemic IPO party," then 2023 was a consolidation and recovery period of sorts.

Leading 2023’s tepid performance were money-losing small and mid-cap technology companies, which suffered disproportionately due to a higher cost-of-capital environment, which reduced valuations accordingly.

Many management teams chose to avoid going public due to the ongoing "valuation gap" between public valuations dropping sharply versus private valuations falling less so.

Additionally, the quality of many companies going public in 2023 was poor, as I described above, with many small firms seeking to take advantage of $5 IPO prices to ensnare unsuspecting retail investors only to produce generally poor results and quickly destroy shareholder value.

While there were a few periods during the year where investors hoped for a revived market, such as when semiconductor design firm ARM Holdings ( ARM ) went public, these stock market debut performances were generally muted, and enthusiasm subsequently waned.

As the year progressed into the last quarter, an increasing chorus of predictions about interest rate reductions turned out to be somewhat prescient as the Federal Reserve’s December meeting produced expectations of a drop in rates throughout 2024.

Whatever the trajectory of macroeconomic conditions in 2024, the U.S. IPO market, given the poor performance of many 2023 IPOs, is likely to experience only a modest rebound.

While year-end 2023 IPO initial filings have increased a bit, the public/private markets valuation gap still persists.

2024 IPO Market In Focus

If cost-of-capital assumptions drop further as 2024 progresses, the gap may start to close somewhat, possibly resulting in increased IPO volume as the year progresses.

For IPO investors, there will likely be potential opportunities for "base hits," but investors should continue to focus on quality IPO candidates and avoid low-priced companies short on growth or profitability.

Generally, the IPO market does not like volatility in the overall stock market, although, in the past, such volatility can sometimes provide the best chance for retail investors to gain access to recent IPO stocks at temporarily depressed prices.

Also, in the United States, 2024 will likely present substantial political election volatility with an uncertain outcome.

In my view, the 2024 U.S. IPO market will continue to face challenges in terms of quality and quantity of investable opportunities.

The market will likely proceed at relatively low levels of activity, punctuated with a few high-visibility IPOs throughout the year.

Some likely IPO candidates for 2024 worth noting include payments company Stripe ((STRIP)), social network firm Reddit ((REDDIT)), large Chinese online retailer Shein, fast-casual restaurant Panera Bread and Kim Kardashian’s shapewear company Skims, among others.

Coming off a disappointing IPO market return performance in 2023, my enthusiasm continues for the potential of solid growth stocks as a part of an investor’s portfolio, but with a focus on the quality of the company and its growth and earnings prospects.

With the prospect of lowered cost-of-capital assumptions resulting in a better stock market environment for high-growth technology companies, I’m cautiously hopeful that the IPO market will improve its performance in 2024.

I’ll continue to highlight IPO companies that I believe are high quality with a discernible path to profitability and quality management teams combined with large addressable markets and a solid revenue growth trajectory.

I also will not hesitate to call out poor IPO candidate companies, as I expect they will, unfortunately, continue to be presented to investors.

I urge IPO investors to avoid FOMO (Fear Of Missing Out) behaviors and cast a cold and dispassionate eye on IPOs that are heavily hyped in the media world.

Avoid $5 or less IPOs and proceed carefully with Asia-Pacific IPO candidates.

Investors should focus on quality companies with strong growth, experienced management and reduced operating losses.

Patient, detail-oriented investors who use a "watch list" proactively to track companies while waiting for good entry points stand a chance of outperforming the general market.

For further details see:

IPOs In 2023 Disappoint But 2024 Looks Brighter