NVDA - Iron Mountain: Capitalizing On The Generative AI Boom

2023-08-28 09:00:00 ET

Summary

- IRM's prospects appear to be highly promising, thanks to the generative AI boom and the management's intensified Data Center capex in FY2023.

- With growing backlog, expanded capacity, and higher service base prices, we may see its Data Center segment eventually be a top and bottom line driver.

- For now, its legacy business continues to be highly profitable, funding the Project Matterhorn, with an ambitious FY2026 revenue target of $7.2B.

- With Mr. Market likely upgrading IRM's valuation nearer to its Data Center REIT peers, we may see its long-term price target increase significantly to $90.

- Combined with its excellent forward dividend yield of 4.25%, IRM is highly suited for both income and growth REIT investors.

A REIT With A Generative AI Investment Thesis

We previously covered Iron Mountain Incorporated ( IRM ) in June 2023, discussing its unique proposition across physical data storage, digital transformation, and data center infrastructure.

The stock was also trading at a discount to its fair value of $71.45, based on its FY2023 AFFO per share guidance of $3.95 at the midpoint and NTM Price/ AFFO Per Share valuation of 18.09x then.

For now, IRM has recorded another excellent FQ2'23 earnings call , with revenues of $1.36B (+3% QoQ/ +5.3% YoY) and AFFO per share of $0.94 (-3% QoQ/ +1.1% YoY).

Most importantly, its legacy Global RIM business remains the REIT's top and bottom line driver, with $1.15B in revenues ( +2.6% QoQ / +7.4% YoY) and $499.06M in adj EBITDA in the latest quarter (+4.4% QoQ/ +6.3% YoY).

IRM continues to ramp up its data center ambitions as well, with plans to lease over 80 MW by the end of FY2023 (+23.1% from FY2022 levels of 346 MW). Due to the robust demand, the management has raised its FY2023 capital expenditure guidance by +20% to $1.2B (+37.1% YoY), with another 200 MW of capacity currently under construction.

Once completed, we are looking at a nearly doubled capacity of ~420 MW , in time to tap onto the robust hyperscaler/ generative AI demand, which has triggered the increase of the service base prices by +40% YoY. These promising developments point to the REIT's excellent monetization cadence, building upon its successful legacy business.

While we have been concerned about the elevated interest rate environment, thanks to the Fed's sustained hike and IRM's growing long-term debts of $10.84B (+2.6% QoQ/ +11.7% YoY) in the latest quarter, it appears those headwinds may abate soon.

The July 2023 CPI has shown a deceleration cadence to 3.2% (+0.2 points MoM/ -5.3 YoY), with most market analysts pricing a rate freeze in the upcoming FOMC meeting in September 2023.

Then again, with ~83% of IRM's debts at fixed rates and a weighted average interest rate of 5.4% by FQ2'23 ( +0.1 points QoQ / +0.8 YoY), the management has also made great efforts to manage risks during this period of uncertainty.

With an adj EBITDA of $475.65M (+3.2% QoQ/ +4.6% YoY), net interest expense of $144.17M (+5.1% QoQ/ +25.3% YoY), and dividend obligation of $180.55M (-3.1% QoQ/ inline YoY) in FQ2'23, we believe the management has executed brilliantly for now.

So, Is IRM Stock A Buy , Sell, or Hold?

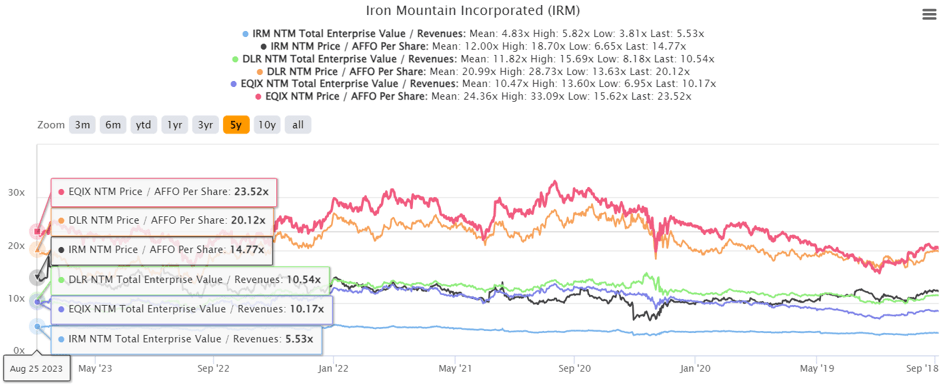

IRM 5Y EV/Revenue and Price/ AFFO Per Share Valuations

{kind=link}

S&P Capital IQ

For now, IRM trades at NTM EV/ Revenues of 5.53x and NTM Price/ AFFO Per Share of 14.77x, returning to its 1Y mean of 5.24x/ 14.13x, though still elevated compared to its 3Y pre-pandemic mean of 4.21x/ 11.88x.

This is probably attributed to Mr. Market's upward rerating closer to its data center REIT peers, such as Digital Realty (NYSE: DLR ) at NTM Price/ AFFO Per Share of 20.12x and Equinix (NASDAQ: EQIX ) at 23.52x.

The data center premium has been long observed as well, compared to their 1Y mean Price/ AFFO Per Share of 16.67x/ 22.23x and 3Y pre-pandemic mean of 19.21x/ 21.33x, respectively.

Thanks to the generative AI boom and sustained cloud migration post pandemic, we may see this optimism hold through the uncertain macroeconomic outlook.

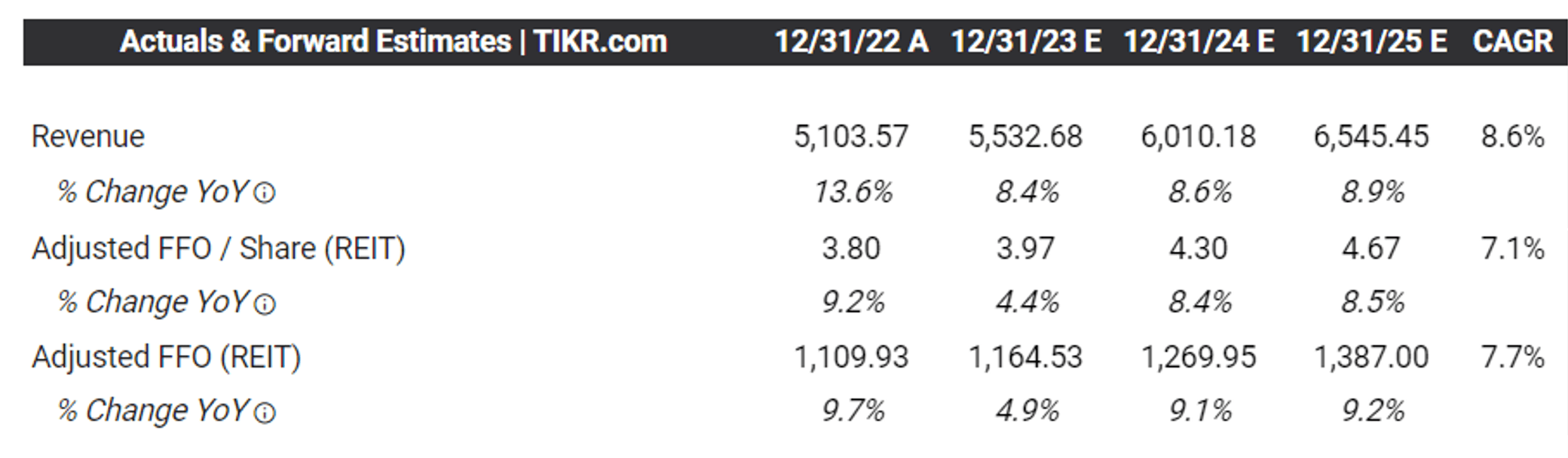

The Consensus FY2025 Revenue & AFFO Estimates

{kind=link}

Tikr Terminal

IRM's strategic choice to expand into the data center segment has also directly contributed to its excellent top/ bottom line projected expansion at a CAGR of +8.6% and +7.1% through FY2025. This sustains its growth cadence from the normalized CAGR of +6.4% and +7.3% between FY2016 and FY2022, respectively.

Therefore, while Data Center may only comprise 8.6% of IRM's FQ2'23 revenues (+0.1 points QoQ/ +0.9 YoY), compared to DLR's at 63.2% and EQIX's at 95% , we believe the tailwinds for the former remain excellent, based on its sustained ramp thus far.

This also builds upon IRM's ambitious Project Matterhorn , with an FY2026 target revenues of ~$7.3B, expanding at a CAGR of ~10%.

We believe these numbers are not overly ambitious as well, based on Nvidia's ( NVDA ) exemplary FQ2'24 data center sales of $10.32B ( +141.1% QoQ / +171.5% YoY) and FQ3'23 overall sales guidance of $16B (+18.4% QoQ/ +169.8% YoY).

This corroborates with Gartner's projection of the global cloud market size to grow tremendously to $724.56B by 2024, expanding at a CAGR of +21.48%, attributed to the generative AI and Metaverse boom, consequently boosting the significance of data center REITs.

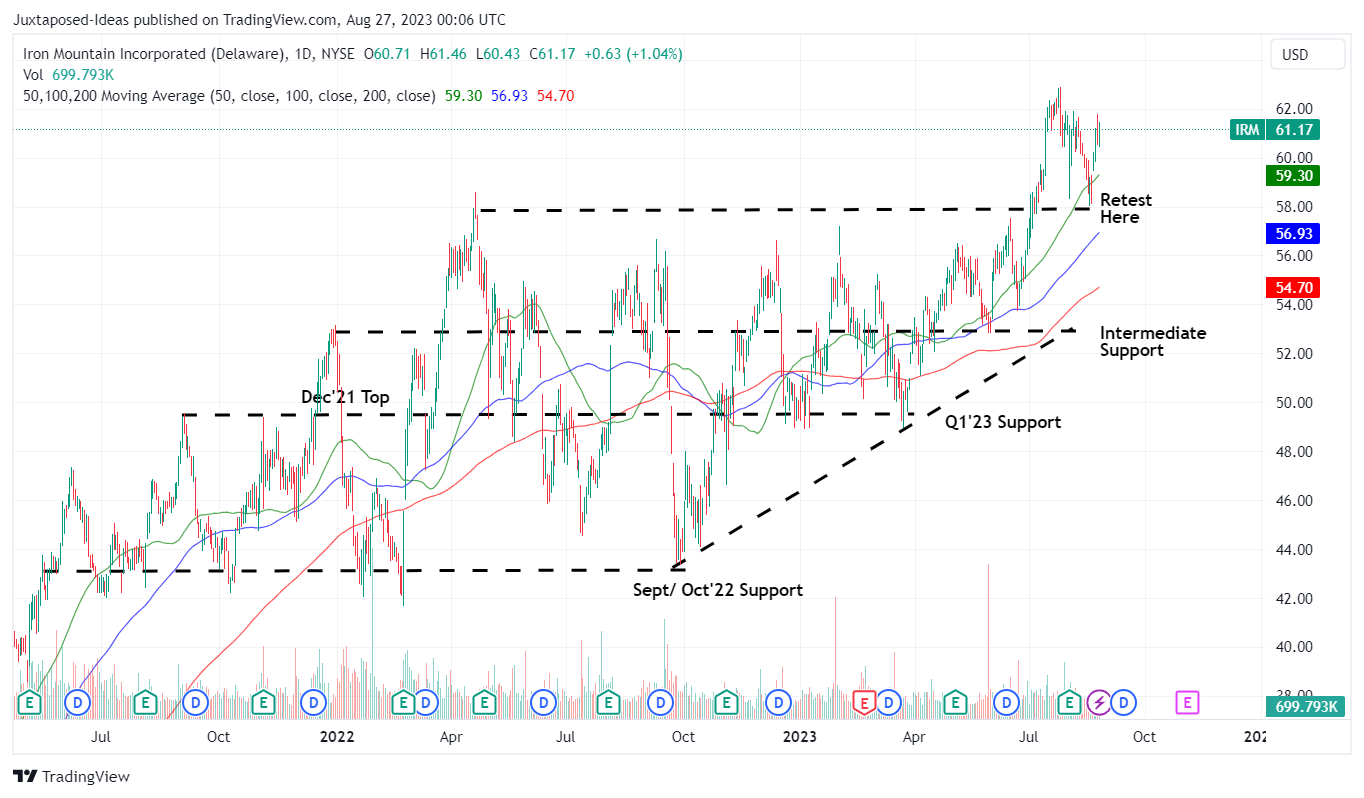

IRM 2Y Stock Price

{kind=link}

Trading View

For now, IRM has bounced from the 2022 resistance levels of $58, while charting another upward retest of the July 2023 top of $63, likely attributed to NVDA's smashing forward guidance. This also corroborates with the stock's historical movement thus far, with it to likely form another floor at the $58 levels.

Based on the data center REIT mean Price/ AFFO Per Share valuations of 19.47x and the FY2025 consensus estimates AFFO Per Share of $4.67, we are still looking at a long-term price target of $90.92, implying an excellent upside potential of +48.6% from current levels.

As a result, we continue to rate the IRM stock as a Buy, depending on individual investor's dollar cost averages. Otherwise, bottom fishing investors may want to wait for another pullback to $58 for the chance to dollar cost average.

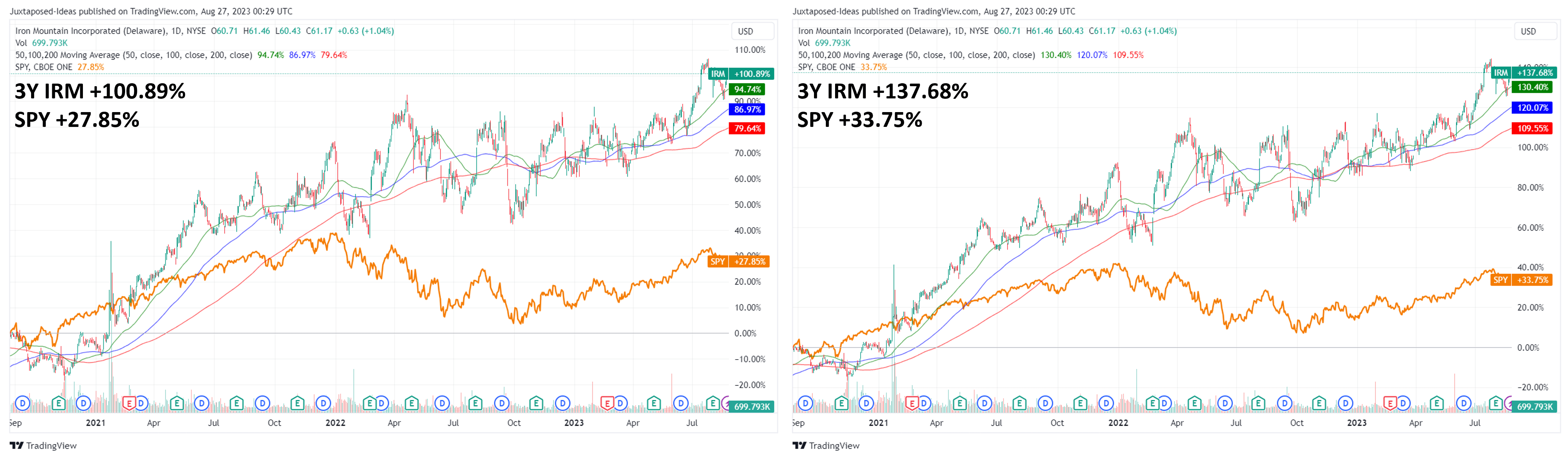

IRM 3Y Stock & Dividend Returns

{kind=link}

Trading View

However, it really depends on individual investor's risk tolerance, since IRM is both an excellent income and growth REIT stock, with a solid 4.25% in forward dividend yield. The management has also raised the FQ3'23 annualized dividends to $2.47 (+5.1%).

While some investors may lament the pull back from the 4Y average yield of 6.38%, this is only attributed to the stock's excellent 3Y return of +100.89%, compared to the SPY at +27.85% at the same time, excluding dividends.

If we are to include dividends, IRM's total 3Y returns are even more impressive at +137.68%, compared to the SPY at +33.75%. With the generative AI demand still in its nascency, we believe IRM has a long runway for growth indeed.

For further details see:

Iron Mountain: Capitalizing On The Generative AI Boom