COM - Is Enbridge Underrated As Winter Approaches

2023-10-25 03:37:52 ET

Summary

- Enbridge continues to expand its oil and gas pipeline infrastructure and is also involved in natural gas production and storage.

- The company will become a key player in today's world as more and more countries are concerned about climate change and seek to switch from coal to natural gas.

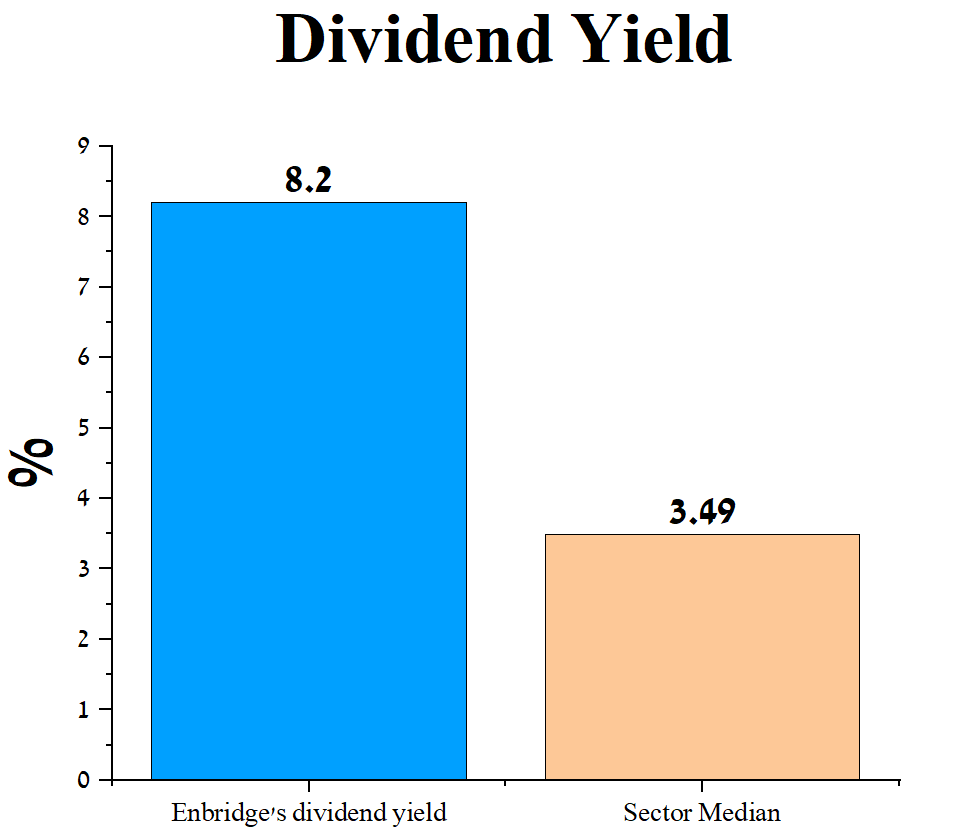

- In addition, Enbridge's dividend yield remains extremely high, exceeding 8%, which is one of the crucial investment thesis that attracts long-term investors.

- On the other hand, due to the company's annual EBITDA growth, its total debt/EBITDA ratio decreased from 6.47x to 5.71x.

- We initiate our coverage of Enbridge with an "outperform" rating for the next 12 months.

Enbridge ( ENB ) is one of the largest energy infrastructure companies in the world, headquartered in Calgary, focused on the transportation of hydrocarbons in North America.

Investment thesis

We believe the company will become a key player in today's world as more and more countries are concerned about climate change and seek to switch from coal to natural gas, one of the cheapest and cleanest energy sources. When natural gas is burned, less carbon dioxide and other chemically hazardous substances are released, which reduces the negative impact on the environment and human health.

Enbridge continues to work on renewable energy projects, which, given the growing geopolitical tensions in the world, including due to the war in the Middle East, will contribute to increased demand for its services from the US and Canadian governments, with the ultimate goal of improving their energy security.

In addition to the expected increase in the company's revenue in the second half of 2023, we expect its management to maintain its current dividend policy. Enbridge's dividend yield remains extremely high, exceeding 8%, which is one of the crucial investment thesis that attracts long-term investors.

Author's elaboration, based on Seeking Alpha

{kind=link}

Enbridge's Q2 2023 financial results and outlook for the 2H 2023

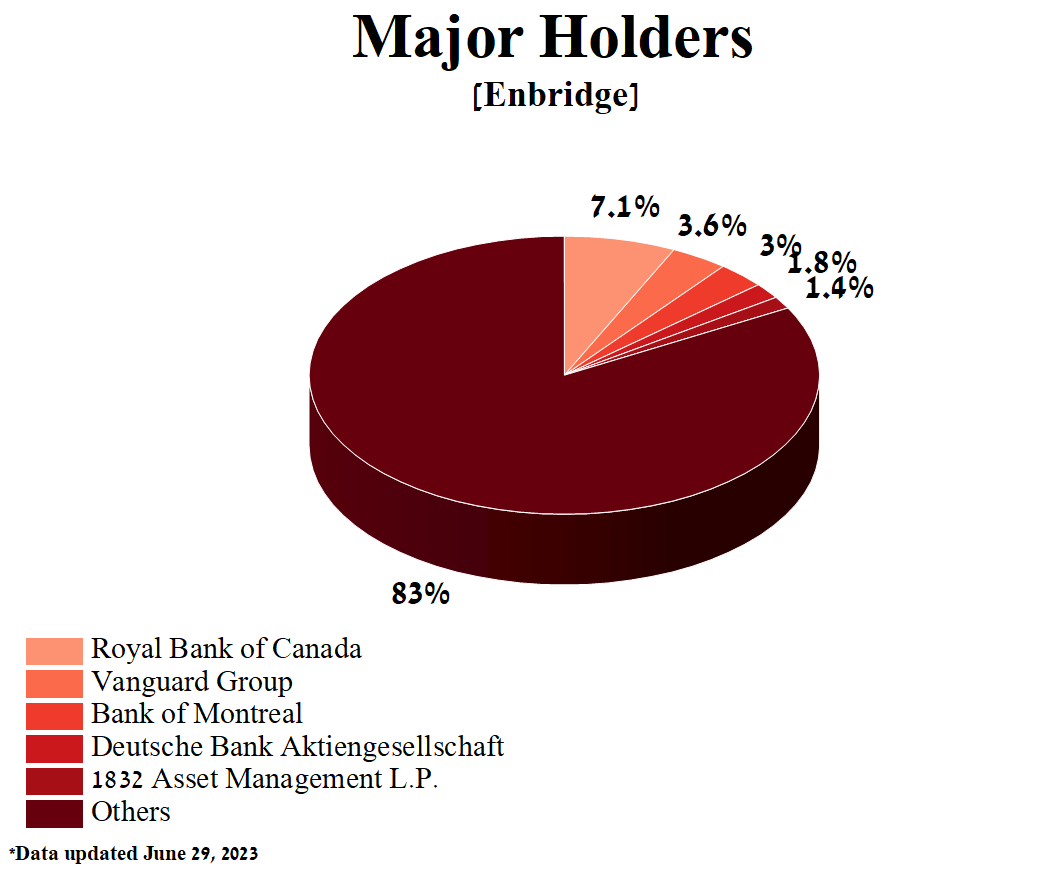

Before diving into Enbridge's Q2 2023 financial results and our expectations for the second half of 2023, we'd like to turn your attention to its institutional investors.

Thanks to the growth of Enbridge's gross margin in recent years, its five largest shareholders with a total stake in the company equal to 16.98% have long been such financial giants as Royal Bank of Canada, Vanguard Group, Bank of Montreal, Deutsche Bank and 1832 Asset Management.

Author's elaboration, based on Yahoo Finance

{kind=link}

Furthermore, despite the recent decline in the company's stock price, the percentage of shares owned by institutional investors has remained stable. This stability suggests that these investors remain confident in Enbridge's promising future.

{kind=link}

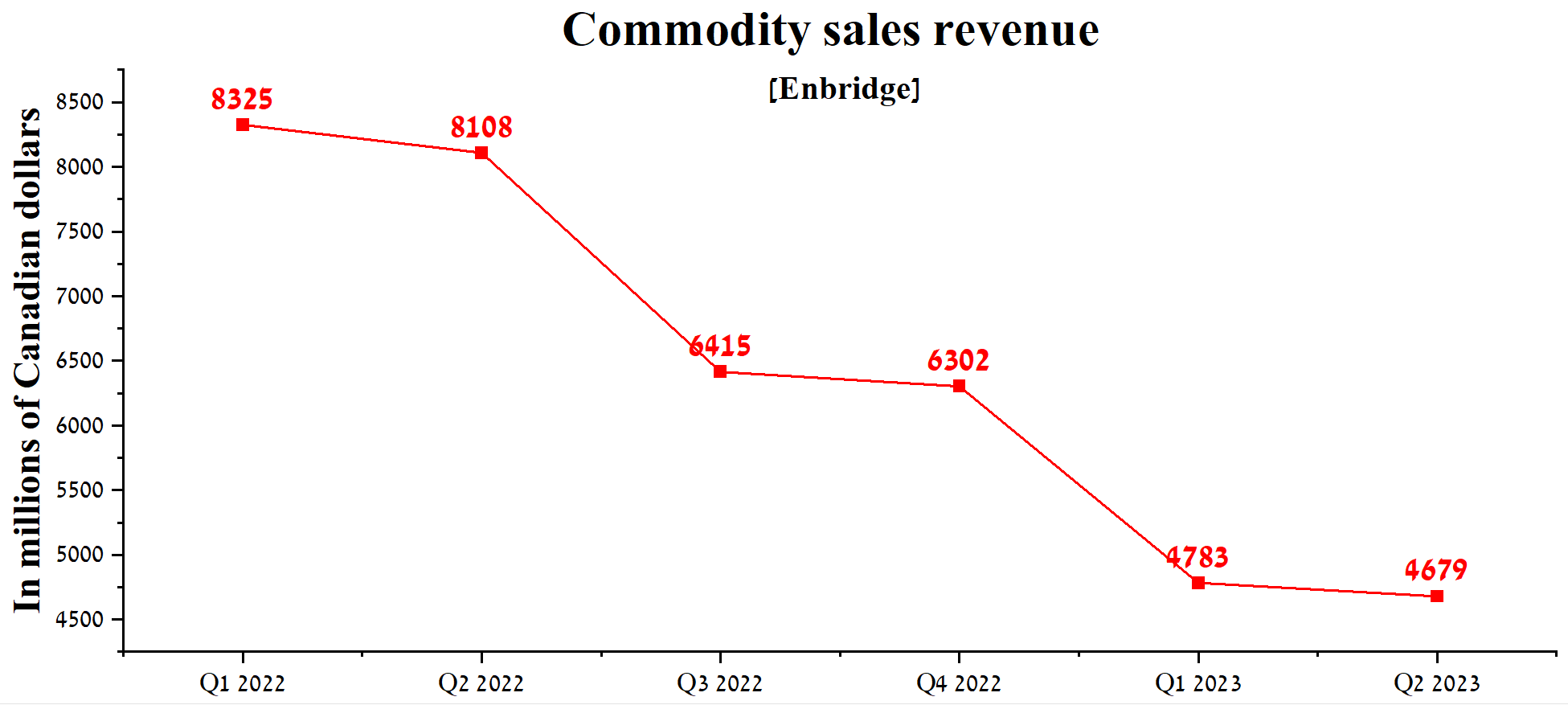

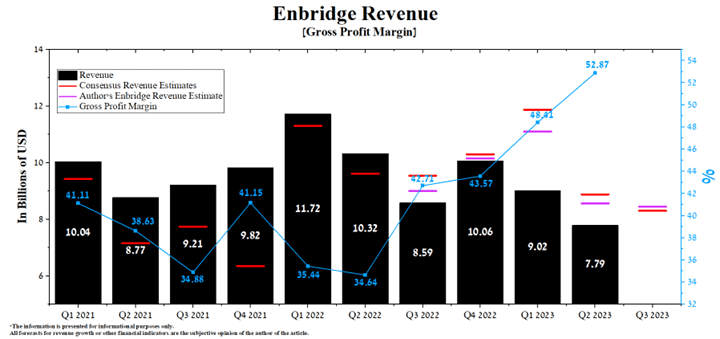

At the same time, the second quarter of 2023 showed unfavorable results, since not only Enbridge's EPS was not able to exceed analysts' expectations, but at the same time, its revenue has continued to decline for several quarters, mainly due to the impact of relatively low natural gas prices. So, Commodity sales revenue amounted to about 4.68 billion Canadian dollars, decreasing by 2.2% compared to the previous year.

Author's elaboration, based on quarterly securities reports

{kind=link}

On November 3 , Enbridge will publish its financial report for the third quarter of 2023. According to Seeking Alpha , Enbridge's revenue for the third quarter of 2023 is expected to be $8.3 billion, down 19.4% year-over-year and 6.5% below analysts' expectations for the previous quarter. At the same time, under our model, the company's total revenue will be higher, amounting to $8.45 billion.

We believe Enbridge's quarter-over-quarter revenue growth will be driven by higher natural gas prices and an increase in its transportation revenue. These factors, in particular, will mitigate the negative impact of strengthening the US dollar relative to the Canadian dollar.

Author's elaboration, based on Seeking Alpha

{kind=link}

On the other hand, we predict that Enbridge's operating profit margin will reach 22.5% by 2023. Moreover, in 2024, this financial metric will rise to 24.1% due to an increase in hydrocarbon prices, a decrease in operating expenses, a growth in demand for natural gas storage, and an increase in the cost of company services.

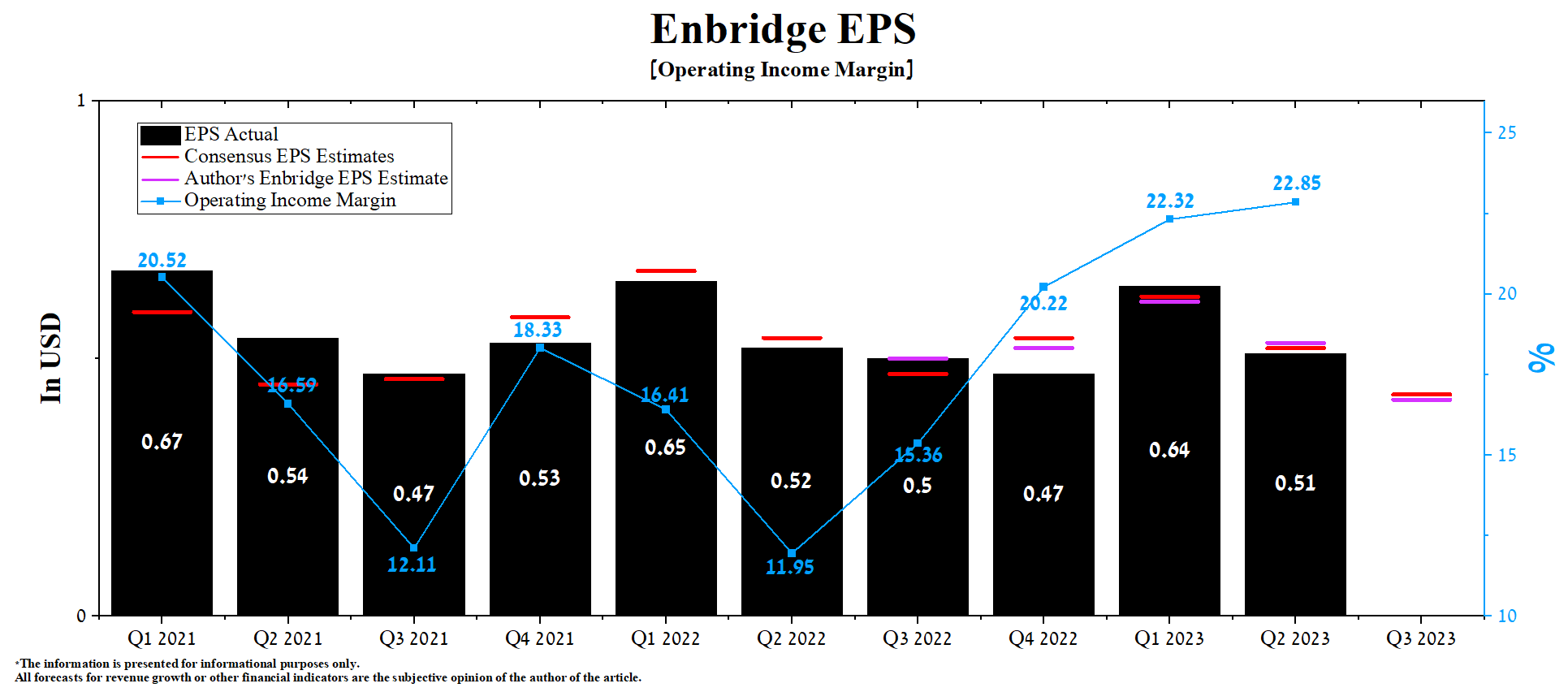

According to Seeking Alpha , Enbridge's Q3 EPS is expected to be $0.41-$0.52, down 15.4% from the Q2 2023 consensus estimate. At the same time, according to our model, Enbridge's EPS will be in this range and amount to $0.42.

In addition, the company's Non-GAAP P/E [TTM] is 15.5x, 77.98% higher than the sector average and 14.67% lower than the average over the past five years. In contrast, Enbridge's Non-GAAP P/E [FWD] is 15.6x.

Author's elaboration, based on Seeking Alpha

{kind=link}

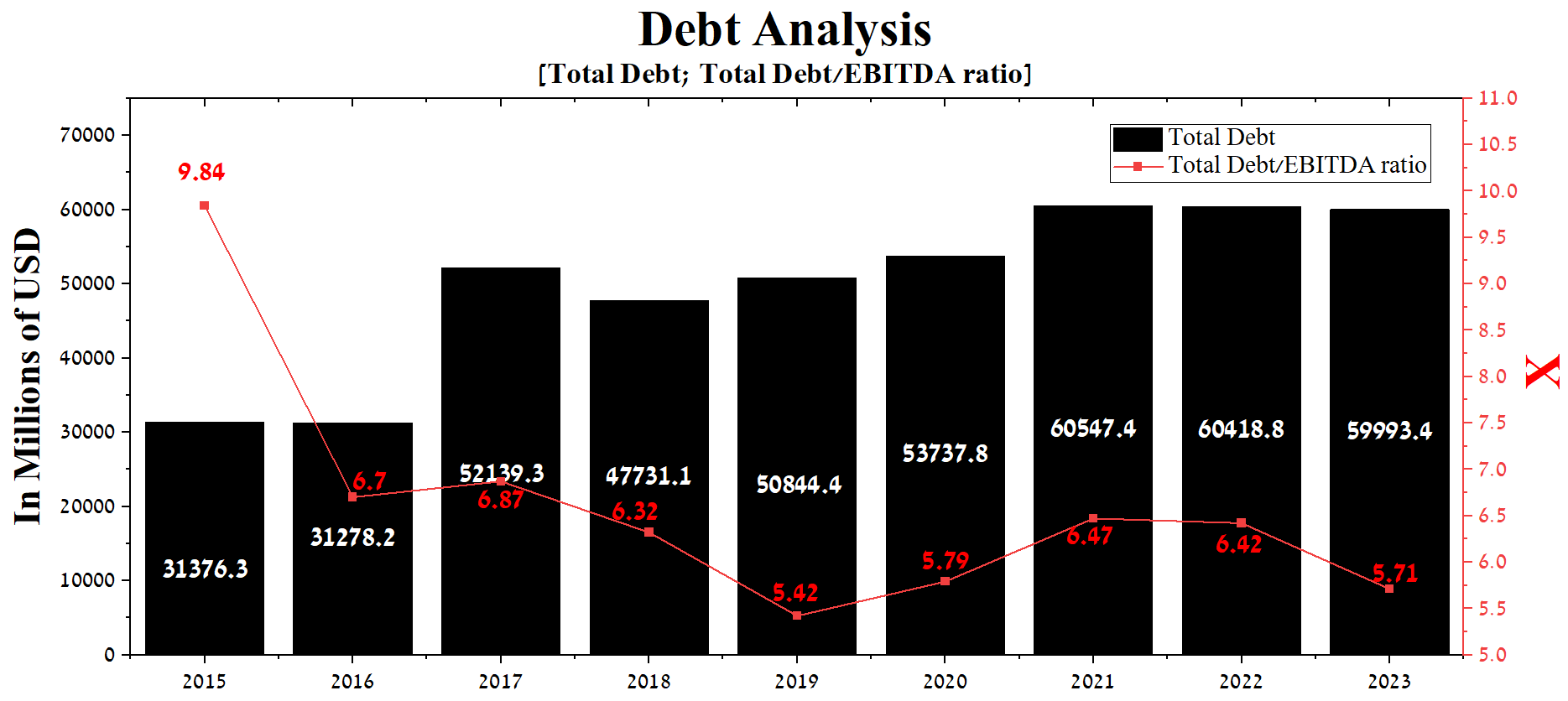

However, one of the key risks for the company remains the persistence of its debt of about $60 billion, which, among other things, negatively affects its net income and does not allow it to pursue an active M&A policy, unlike many companies in the energy sector. At the end of the second quarter of 2023, Enbridge's total debt was about $59.99 billion, down slightly from 2021. On the other hand, due to the company's annual EBITDA growth, its total debt/EBITDA ratio decreased from 6.47x to 5.71x.

Author's elaboration, based on Seeking Alpha

{kind=link}

Given the company's total debt/EBITDA ratio is well above 3x, we expect it will have to resort to refinancing some of its debt. A key reason for this is the deal concluded on September 5 with Dominion Energy ( D ) to acquire several natural gas utilities, which, among other things, will lead to an increase in Enbridge's debt.

Risks

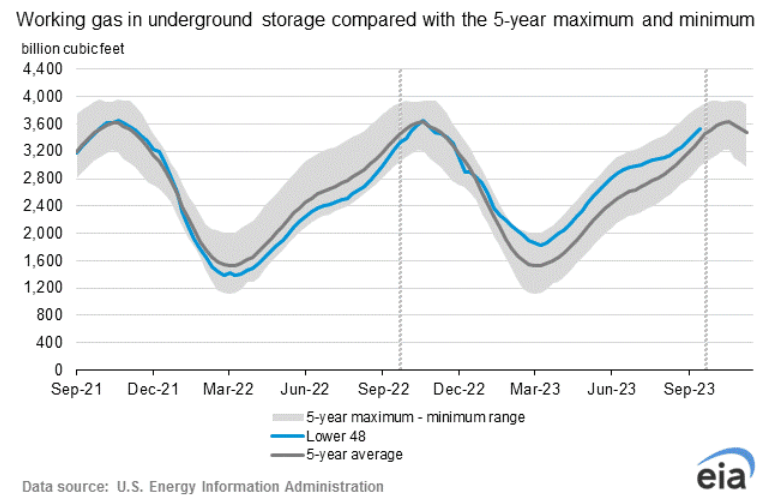

In addition to Enbridge's continued high debt, financial market participants must consider the second major risk to its financial position. That risk is the U.S.'s nearly full natural gas storage capacity. So, according to EIA estimates , as of October 13, 2023, the total volume of working natural gas in storage was 3,626 billion cubic feet, 300 billion cubic feet more than the previous year. As a result, this could lead to lower Enbridge's transportation revenue for the fourth quarter of 2023 if the winter in North America is warmer than usual.

U.S. Energy Information Administration (EIA)

{kind=link}

Conclusion

Enbridge continues to expand its oil and gas pipeline infrastructure and is also involved in natural gas production and storage. This initiative aims to meet the needs of commercial and industrial customers across Canada and the United States.

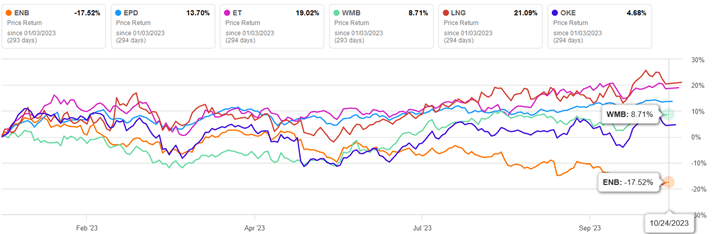

With Enbridge's second-quarter 2023 revenue down year-over-year and the issuance of 102,913,500 shares totaling C$4.6 billion to finance the acquisition of three natural gas utilities from Dominion Energy, its share price has declined by more than 17% since the beginning of 2023.

Author's elaboration, based on Seeking Alpha

{kind=link}

Despite the challenges faced by the company in recent months, its dividend yield remains high at over 8%. This factor, coupled with the increasing natural gas prices, is a key investment thesis that attracts investors.

We initiate our coverage of Enbridge with an "outperform" rating for the next 12 months.

For further details see:

Is Enbridge Underrated As Winter Approaches