FVRR - Is Fiverr Worth Owning?

2023-03-15 12:05:14 ET

Summary

- Fiverr reported its earnings a few weeks ago, and while revenue only grew 4%, the stock shot up almost 19%.

- We look at the results and the interpretation of the numbers and Fiverr's prospects.

- Is Fiverr still worth owning? And if so, why?

- Insights from the earnings call, with ample attention for ChatGPT.

- We briefly look at the valuation of the stock.

2022 was likely the most challenging year for us since I founded the company 13 years ago.

-Micha Kaufman, founder and CEO of Fiverr, in the shareholder letter

A few weeks ago, Fiverr's ( FVRR ) earnings were released. The stock shot up almost 19% as a reaction, although it is already 8.45% under the initial price again.

Why did the stock shoot up and is Fiverr's stock worth holding? That's what we will find out in this article.

The results

This is an overview of the income statement that I have made.

Made by the author

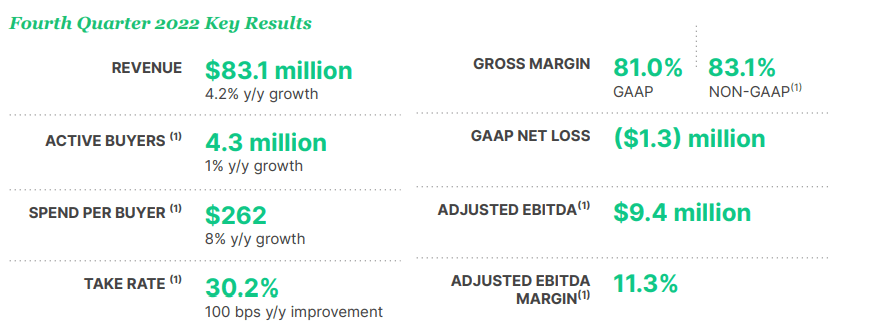

As you can see, revenue was up just 4.2% year-over-year. That is not enough for a growth stock unless it's temporary.

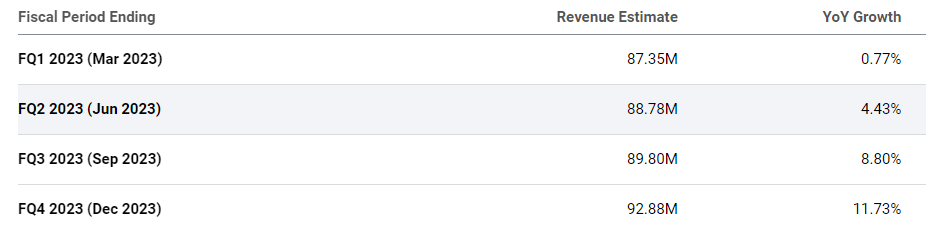

Guidance was also not that much better. For the first quarter of 2023, the quarter we are in now, the company guides for $86.5 to $88.5 million in revenue. That's about the same as the consensus of $87.31M and less than 1% growth at the midpoint.

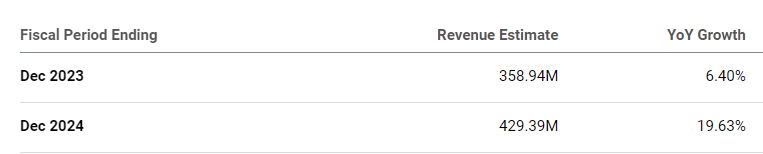

For the full year 2023, Fiverr projects revenue of $350 million to $365 million, up just 6% at the midpoint.

Those are not numbers you start dancing around in excitement or that make you want to buy a shipload of Fiverr shares, right?

Adjusted EBITDA guidance for Q1 was $9.0 million to $10.5 million, and for the full year, $45 million to $55 million. That shows where the company is putting its focus: profitability. The guidance implies doubling the EBITDA.

You can also see that in the chart I made. You don't often see operating expenses down 13% year-over-year, as Fiverr accomplished. G&A, general and administrative costs were down more than 52%.

How to think about the results

What is interesting about Fiverr's share price shooting up is that Upwork ( UPWK ), Fiverr's main competitor, had reported its earnings the week before Fiverr. This was the stock price reaction to those earnings up to now.

If you only look at the revenue growth, you can't understand these opposite reactions. Upwork's revenue was almost 18% year-over-year, which looks much better than Fiverr's 4.2%. But Fiverr impressed the market with profitability, unlike Upwork, which is expected to remain unprofitable for quite a bit longer.

Also, remember that Upwork caters to big companies, Fiverr to SMBs, which are much more sensitive to economic ups and downs. That also means that if the economy turns, you should expect Fiverr to benefit more than Upwork.

If you look at what analysts were expecting, you see that Fiverr's guidance is pretty similar.

{kind=link}

Less than 1% growth in Q1? Yep. How about that 6% for 2023?

{kind=link}

Again, as analysts had projected. Two remarks here: not going under that consensus is solid for a company so sensitive to the overall economy. This is just guidance, so Fiverr will still have to deliver. But do you also notice that estimate for 2024? Almost 20% revenue growth. If Fiverr can live up to that estimate, which is more credible with these results, things don't look as bad as you may think at first sight. Management also said it sees double-digit growth for Q4 2023, even with macro conditions not improving.

Besides revenue growth, there are more ways for a stock to be attractive: earnings growth. If you look at Fiverr, earnings are expected to grow at high speed both in the current year and the next year.

{kind=link}

To me, this is the main reason I'm not selling my Fiverr position, next to the projected re-acceleration of revenue growth in 2024. At the same time, I will not add meaningfully to my position. But I don't think the Fiverr story has been written; we have just had the first chapters, not the book.

Some more numbers from the shareholder letter .

{kind=link}

As you can see, active buyers were almost flat year-over-year. This stabilization is good, as spending on sales and marketing was down substantially. Repeat customers represent 63% of Fiverr's revenue, up from 59% in 2021. The number of buyers spending more than $10K a year grew 29% year-over-year, which is good to see, as a part of the bull case for Fiverr is that it goes upmarket. The spend per buyer was also up, 8% compared to last year.

Fiverr bears will always use the take rate in their argumentation. They'll say this high take rate is unsustainably high. If you compare 30.2% with Upwork, of which the take rates are usually below 15%, you could think Fiverr bears have a strong argument. But the take rate is based on value creation. The sellers buy more and more of Fiverr's products for their online activities. Think of ads, tax programs, success coaches, etc. It's like saying Amazon's take rate is unsustainable because its ads business growing so strongly. It's a strength, not a weakness.

These products bring value to sellers and that's why the take rate keeps going up. Promoted gigs, for example, grew its revenue by over 100% in 2022. Seller Plus, the subscription-based service for sellers, already has more than 10,000 subscribers, while it's still only a bit older than a year.

Looking at the adjusted EBITDA margin, you see the company has 11.3% now. The long-term goal is to get to 25%.

Earnings Call Insights

This is how Fiverr's founder and CEO Micha Kaufman started the conference call .

2022 was a unique year. In response to a shifting macro environment resulting in headwinds to the overall freelance demand, we quickly pivoted the company to tighten our focus on efficiency and profitability. As an entrepreneur and knowing how huge the long-term opportunity is in front of us, I must admit this wasn’t easy. But it was absolutely the right thing to do.

This quote summarizes everything: the profitability, why it was needed, and the big opportunity ahead.

Just to show you how badly the worsening macro conditions impact Fiverr, here's a quote that puts that in numbers.

In any of the previous years, we typically see buyers’ spend increase from the first half of the year to the second half of the year across all cohorts, by an average of 8%, driven by a combination of wallet share expansion as well as seasonality of investments. And we see the biggest H1 to H2 spend jump in 2020 when COVID impact kicked in around mid-year. In 2022, however, we saw buyers across cohorts reduced their spend by an average of 3% from H1 to H2.

That's a difference of 11% between what could have been expected and reality. That's not because Fiverr did something very wrong; it's the economy.

Fiverr sees the current macroeconomic circumstances as temporary, but the tech layoffs could also benefit the company.

The tech industry is also at a unique time with a significant amount of layoffs among tech and knowledge workers. Many have turned to freelancing as a temporary or permanent career choice.

Of course, Micha Kaufman had to address the worries about ChatGPT and other AI-powered tools and how they could impact Fiverr's business. Some longer quotes here, as I think this is very important.

Fiverr will uniquely benefit from AI in these aspects. First, innovation always creates more jobs, not less. The recent AI tools presented to the world in the past few months have demonstrated a significant step function in the evolutionary progress of technology. However, as much as these tools have incredible power, what really matters is how humans will make use of these tools to create inspiring, creative work for other humans to consume. As a result, it will bring many new professions related to AI that we can’t even imagine today.

(...)

Second, AI tools will bring a lot of productivity improvement to our talent community and Fiverr is uniquely positioned to democratize and distribute these tools to the freelancer community, who often lack access and resources to deploy those technologies.

(...)

Third, digital service is highly fragmented, unstructured and complicated, so matching buyers and sellers through an e-commerce model is a fairly difficult product challenge. With AI technology, we can unlock the long tail of data we have and drastically improve the overall search, browsing and matching experience. We are already working on some of these ideas.

I agree with his comments to a very high degree. I'm old enough to know that when the internet started, people feared it would take away jobs. The same happened for automation in the 80s and 90s. But the result was each time the same: more productivity and more jobs. Yes, some low-level 'stupid' work will go away from Fiverr. If you want a logo for a bachelor's evening, you'll probably use AI, not a Fiverr guy. But if you want an AI-based application, a much higher-ticket item, you could go to Fiverr. To me, ChatGPT and other AI models are indeed tools for Fiverr sellers to help them and to get rid of the most basic work.

Micha Kaufman got of course more questions about ChatGPT in the Q&A section. There he answered this:

I think that there's a natural evolutionary step between generations. I mean when I'm looking about the amount of jobs that passed through generations from my grandfather to my father or from my father's generation to mine, obviously, some jobs become obsolete. But my view is that the new jobs created will far exceed those impacted by AI. And actually, if you think about AI specifically, it's already generating thousands of jobs in just training AI. And then it's about optimizing it. And then it's about creating use cases for it.

We will need much more fact-checkers, for example, AI artists, AI programmers, AI-savvy editors and so on.

Micha Kaufman put out three points the company will focus on in 2023.

- Improve search and discovery technology, so buyers have the selection of sellers they need as fast as possible.

- Better tools for sellers to present their work, in a more differentiated way.

- Improve engagement and retention.

Fiverr will integrate AI to help with these objectives.

Valuation

Fiverr projects an adjusted EBITDA of $50 million at the midpoint for next year. With a market cap of $1.35 billion, Fiverr trades at about 27 times adjusted EBITDA. That's not a screaming buy when it comes to valuation, but also not very expensive.

Conclusion

Fiverr focused on profitability and efficiency in Q4 2022 and did this very well. While my initial reaction to the earnings was somewhat negative, with more insight, I'm not considering selling Fiverr.

For investors who don't have a position yet, I don't think they have to rush in. You could establish a small position if you believe in the company's long-term story.

It could take a whole while before growth really picks up again, but I have that patience. Once the economy turns, Fiverr should be among the first to benefit. As we saw, AI will probably not be a threat to Fiverr but rather a tailwind.

In the meantime, keep growing!

For further details see:

Is Fiverr Worth Owning?