YY - Is JOYY Inc. A Buy? An Analysis Of Its Strengths And Challenges

2023-09-29 14:24:06 ET

Summary

- JOYY Inc. is a Singapore-based global technology conglomerate focusing on video-based social media platforms.

- The company's strategic alliances with KOLs and financial health, along with its emphasis on video-based platforms, are its main strengths.

- Concerns about the company's use of VIEs and potential fraud allegations have raised questions, but the company's competitive edge and financial standing remain strong.

- Despite potential risks, I believe YY may be undervalued. Hence, I lean towards a "buy" recommendation with caution due to uncertainties.

JOYY Inc. ( YY ), a Singapore-based global technology conglomerate, has made significant strides in the video-based social media domain, with platforms like Bigo Live, Likee, and Hago under its belt. YY's business model, strategic alliances, and financial health seem promising, strongly emphasizing video-based platforms. Additionally, YY's acquisition of Bigo marked a significant shift in its operations and shaped it into what it is today. However, the company's use of VIEs and its Chinese origins have raised questions, and there have even been fraud allegations. Nevertheless, despite concerns about its reported figures' veracity, YY's competitive edge, especially its collaboration with Key Opinion Leaders (KOLs), and its financial standing remain its main strengths. In my view, the company's valuation needs to be discounted to account for YY's inherent risks and uncertainties, but even after doing so, it looks objectively cheap. Hence, I lean bullish at these levels.

Business Overview

JOYY Inc. , based in Singapore, is a global technology company specializing in diverse video-based social media platforms. These platforms offer users a variety of engaging experiences. Specifically, YY's portfolio comprises Bigo Live, which allows users to live stream to showcase their talents, share their vital moments, socialize, and connect; Likee, a platform dedicated to short-form video content powered by its all-in-one creation tools like filters and special effects, an AI-backed personalized feed; Hago, a social networking platform with casual games; IMO, an instant messaging application equipped with features such as video and group calls, as well as document sharing; and Shopline, a comprehensive platform designed to aid merchants in expanding their online brand presence. Since its inception in 2005, YY has broadened its reach to various regions, including China, the US, Great Britain, Japan, South Korea, Australia, the Middle East, and Southeast Asia.

YY's acquisition of Singapore-based Bigo , which owns platforms such as Bigo Live, Likee, and Hago, marked a pivotal shift. Post-acquisition, JOYY's operations significantly emphasized Bigo and its associated media. While JOYY has a robust operational footprint in Singapore, its roots are undeniably Chinese (hence the VIEs ), and YY's foundational history and substantial operations in China underscore this connection. Despite its expansive presence in international markets like Singapore, JOYY's Chinese origins play a significant role in its perception, leading many to regard it as a Chinese entity. This perception is based on its history and the depth and scale of its operations within China.

Furthermore, JOYY Inc.'s strategic use of VIEs lets it indirectly hold assets in sectors with limited direct foreign ownership. Through VIEs, JOYY Inc. retains operational control and garners economic benefits without direct ownership. However, the contractual dynamics with VIEs do not equate to the control that direct ownership provides. Furthermore, it's worth noting that 92.3% of YY's revenues come from live-streaming services. Therefore, investing in YY offers the opportunity to tap into a conglomerate with a strong emphasis on video-based social platforms and a considerable international presence.

An essential aspect to highlight is YY's use of VIEs; I emphasize this because it showcases YY's adaptability and strategic foresight in a challenging regulatory environment and exposes investors to VIE-related risks. Enforcing such contracts in China presents challenges, primarily due to these structures' scarcity of legal precedents. While VIEs offer a pathway into restricted sectors, they expose the company to potential regulatory risks. If the Chinese authorities deem these arrangements non-compliant, the implications could be significant, jeopardizing JOYY Inc.'s position in a vital market. As a holding company, JOYY Inc.'s financial health depends on its subsidiaries' dividends. China's strict cash flow and cross-border controls pose operational risks. Moreover, YY's significant investments in its subsidiaries from 2020 to 2022 emphasize its operational reliance on its VIE subsidiaries.

Business Landscape and Market Dynamics

JOYY Inc.'s strategic positioning within the growing digital entertainment and social media domain underscores its ability to anticipate and cater to evolving consumer preferences. With the global populace leaning more towards digitization, there's an evident hunger for enriched content and immersive digital experiences. As more people get plugged into the digital realm, the demand for live, on-the-fly content has increased , a trend that YY seems to have adeptly tapped into.

YY's profile is different because it targets its global users with localized content, reducing regional risks. This strategy, exemplified by BIGO Live's real-time interactive offerings, ensures content isn't just abundant, engaging, and aligned with user preferences.

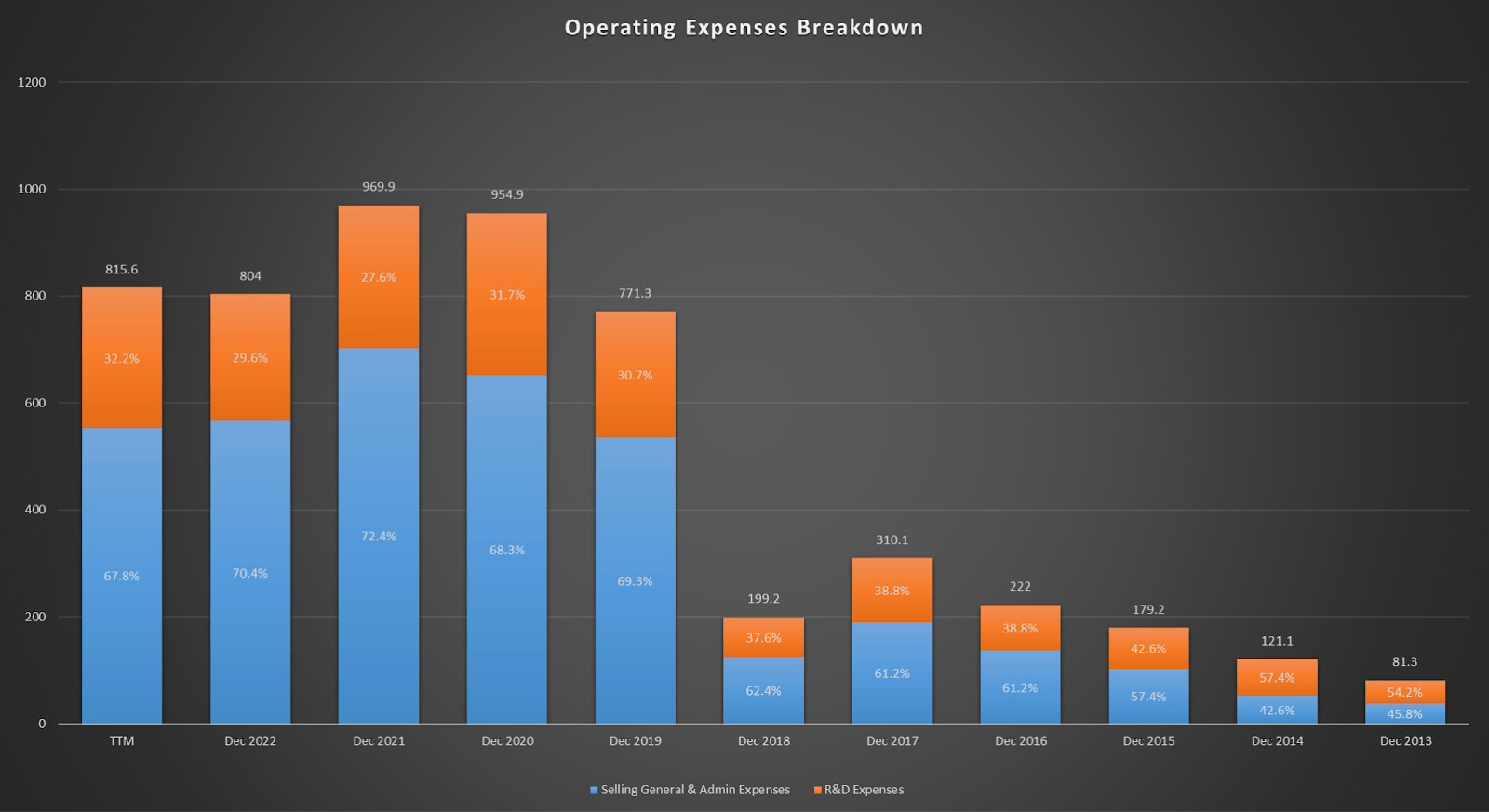

Additionally, managing operational expenses becomes crucial to maintaining profitability as the company expands its offerings and reach. JOYY Inc.'s revenue model does not solely bank on one income channel. The dual monetization strategy - capitalizing on its vast user outreach for advertising and leveraging in-app purchases - ensures a balanced revenue inflow. While advertising offers brands a platform with expansive reach, in-app purchases, especially during live sessions, ensure consumer engagement is monetized.

Seeking Alpha plus author's elaboration.

{kind=link}

YY's collaboration with Key Opinion Leaders (KOLs) is a noteworthy aspect of its business strategy. This alliance enhances its strategic positioning and augments user engagement by providing a platform for branded content and endorsements. While the approach of partnering with influencers is not a new concept, I believe that YY's competitors, such as Tencent ( TCEHY ), Beijing Kuaishou Technology ( KSHTY ), Momo Inc. ( MOMO ), Bilibili Inc. ( BILI ), and ByteDance ( BDNCE ), haven't leveraged this strategy as much as JOYY. In my view, this provides JOYY with a distinct advantage, primarily because such collaborations have proven effective in enhancing user engagement and brand visibility. Consequently, JOYY Inc.'s business model, which is rooted in a profound grasp of global user preferences, appears to be well-positioned for sustained growth.

YY's KOLs, known for their influential reach, effectively magnify JOYY's brand presence, leading to sustainable organic traffic and heightened user engagement. Notably, the BIGO segment's revenue benefited mainly from BIGO Live's MAUs, witnessing an 18% YoY growth , underscoring the efficacy of leveraging KOLs. Beyond diversifying content, these collaborations instill trust, a crucial factor in an age where consumers often cautiously approach direct advertisements. These long-term partnerships give JOYY Inc. a competitive edge and strengthen its market position, creating a moat against competitors. For potential investors, this matters because it shows YY knows how to leverage key influencers, indicating a trajectory poised for continued leadership in its niche.

Valuation Analysis

YY's recent earnings call showed that YY exceeded the higher end of its guidance for Q2 2023. Hence, the company's financial health is evident, with revenues surpassing guidance to $547.3 million and an 89.1% YoY increase in non-GAAP net profit. A healthy operating cash flow of $61.8 million further underscores this robust financial standing. A deep dive into the numbers reveals the BIGO segment as a standout performer, which is particularly promising given its significant contribution to total revenues. BIGO has contributed to JOYY's portfolio with revenues of $471.1 million.

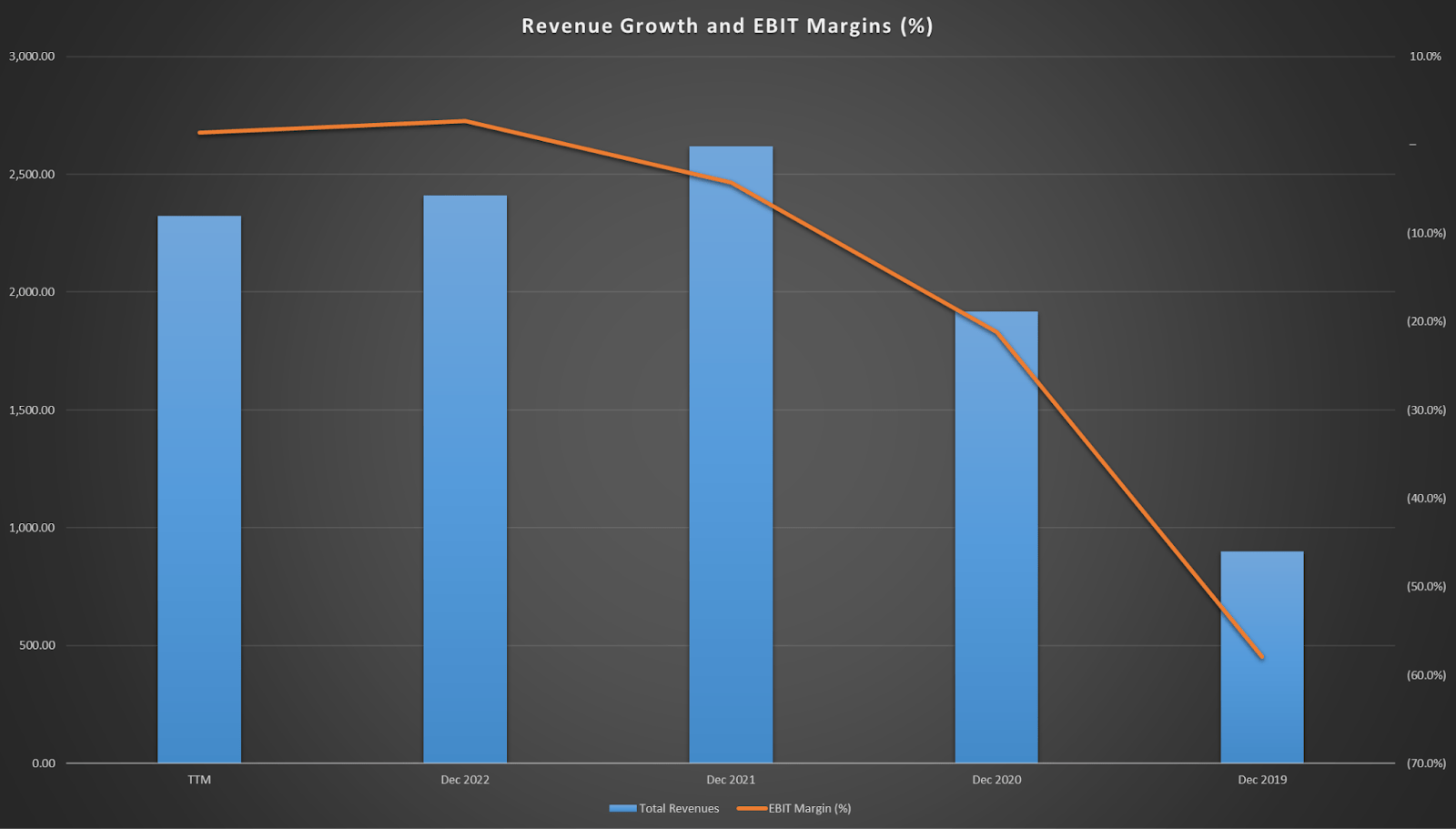

JOYY Inc.'s consistent growth over time underscores its effective strategies and deep connection with users. The rise in global MAUs led to $275.6 million in revenues from that particular user base, which indicates a product that resonates. Moreover, YY's focus on AI-driven personalized feeds and diverse collaborations with KOLs, particularly in emerging markets like Southeast Asia, positions them for continued expansion. Financially , with a massive $3.8 billion cash reserve, they're well-equipped to seize growth opportunities through R&D or strategic acquisitions. Interestingly, JOYY Inc.'s dual identity, its strong presence in Singapore and roots in China, provides a unique edge. And if you look at the company's revenues and EBIT margins since 2019, they show topline growth and improving profitability.

Seeking Alpha plus author's elaboration.

{kind=link}

Still, in light of recent investigations and the article published in April 2021, there are mounting concerns regarding the veracity of the financial figures reported by the company. Several red flags have raised suspicions, including inconsistent revenue recognition practices, unusually high margins relative to industry peers, and rapid inventory turnover rates. These anomalies, combined with whistleblower accounts and the company's reluctance to provide detailed segment breakdowns, suggest the possibility of financial manipulation. While these allegations have not been confirmed, they introduce a significant risk factor. I'll consider the reported numbers for valuation purposes but apply a discount to account for the potential misrepresentation and associated risks.

Seeking Alpha plus author's elaboration.

In my analysis, the valuation model indicates that the company may be undervalued, presenting a potential upside of approximately 59.3% from its current levels. This potential is further supported by the company's increasing MAUs and its robust balance sheet. However, it's essential to approach this with caution. The allegations of fraud and the company's dependence on the VIE structure introduce uncertainty to the valuation.

When evaluating the potential upside of an investment, it's crucial to weigh the associated risks. I believe that applying a discount to the projected upside, especially in light of fraud-related uncertainties, is a reasonable approach. It's worth noting that a recent court ruling said these allegations remain unproven. Still, we could assume the probability of this adverse scenario between 20% to 50%, depending on an investor's risk appetite. Yet, if these allegations are validated, the valuation could shift significantly. In such an event, potentially 90% of the revenues could be in doubt, leading to a valuation of YY at just about 10% of its present value. Using the expected value approach, this adjustment could mean a reduction in my valuation estimate by as much as $1.09 billion, bringing it down to $2.77 billion. However, even with these conservative estimates, my valuation suggests an upside potential of 14.5%. In my view, this indicates that YY is undervalued. Based on this analysis, I'm inclined to recommend a "buy" position for YY.

Conclusion

JOYY Inc. has showcased its adaptability and strategic depth in the rapidly evolving digital entertainment landscape. Its collaboration with KOLs, AI-driven personalized feeds, and a dual monetization strategy set it apart from competitors, as evidenced by its MAU growth. Financially, the company appears robust, with significant growth in its BIGO segment and a massive cash reserve. However, potential investors must tread cautiously, given the recent concerns about the company's potentially fraudulent financial reporting and reliance on the VIE structure. While my valuation model suggests a potential upside of 59.3%, the associated risks cannot be ignored. Still, even after discounting such an upside by 20% to 50%, the stock does appear undervalued. Hence, I lean towards a "buy" rating, but with a note of caution for potential investors.

For further details see:

Is JOYY Inc. A Buy? An Analysis Of Its Strengths And Challenges