CA - Is Kinross Gold A Buy Or Sell? And The Great Bear Debate

2023-03-07 18:10:03 ET

Summary

- Kinross Gold Corporation has reported Q4 2022 and full-year financial results.

- Kinross reported a big net loss, but was its earnings report really that bad?

- And what's the deal with the Great Bear project?

Kinross Gold Update

This is an update on senior gold miner Kinross Gold Corporation ( KGC ), a senior gold miner which produces 2+ million ounces of gold per year from multiple gold mines in the Americas and Africa. In this update, I mainly cover its recent Q4 earnings report , and its initial resource estimate at the Great Bear property.

It wasn’t a great quarter for Kinross. Like many other gold miners, the company suffered from rising cash costs due to inflationary pressures. But Kinross also reported a big impairment charge on one of its gold mines, and released what I feel is a lackluster resource estimate at Great Bear. And, its forward production and cash cost guidance leave a lot to be desired.

Kinross Gold’s Earnings: What the Heck Happened?

{kind=link}

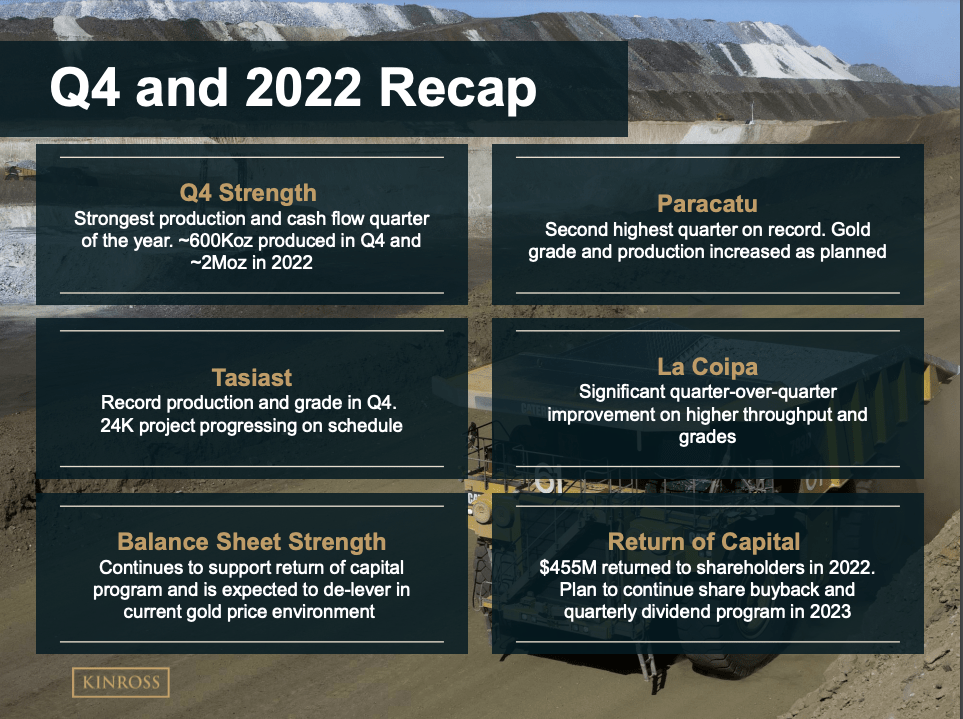

Kinross did see its production increase by 35% from last year, mainly due to higher production at the Tasiast mine, which was temporarily suspended last year, and at La Coipa, which restarted and ramped up its production this year.

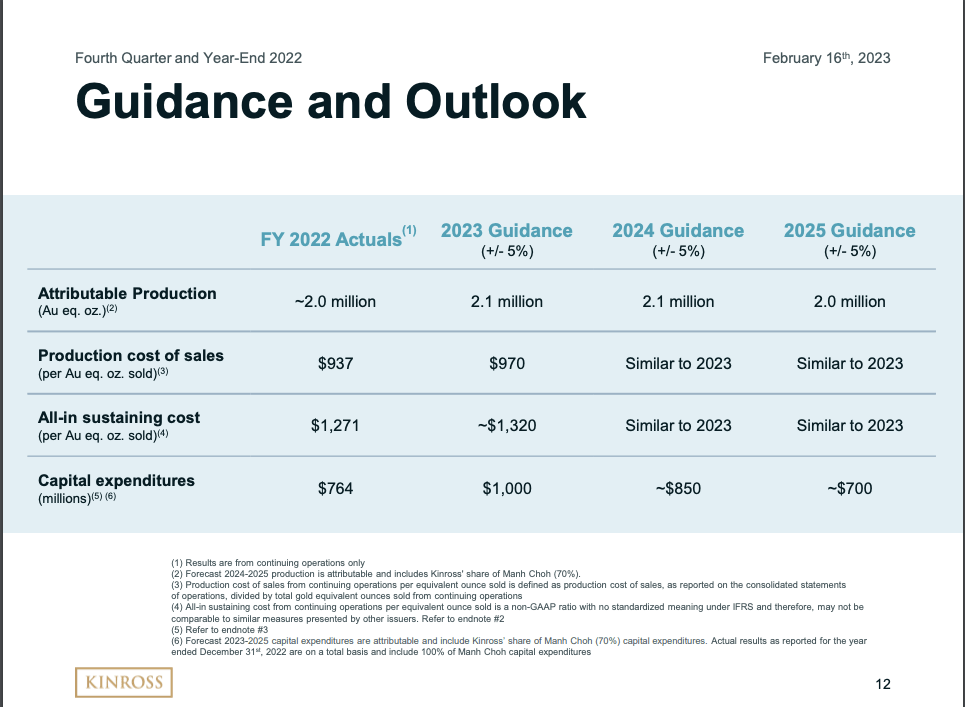

However, that’s about all the good we can take away from its earnings report. Kinross’ cost of sales and all-in sustaining costs (“AISC”) both rose, with its Q4 2022 AISC coming in at $1,236/oz, and full-year costs rising to $1,271/oz. This represents a huge $324/oz or 35.59% increase compared to 2022!

It could have been much worse, if not for higher gold prices. Kinross was able to generate $474.3 million in operating cash flow in Q4 and $1 billion for 2022.

But, after accounting for a non-cash impairment charge on its Round Mountain mine, Kinross’ net loss was -$106 million. This impairment was blamed on changes to the mine plan and slope design, and increased costs due to inflation, the company said.

Finally, Kinross ended the year with just over $400 million in cash and cash equivalents and has strong liquidity of $1.8 billion, giving it a relatively strong balance sheet compared to peers.

Kinross Gold's 2023 Guidance

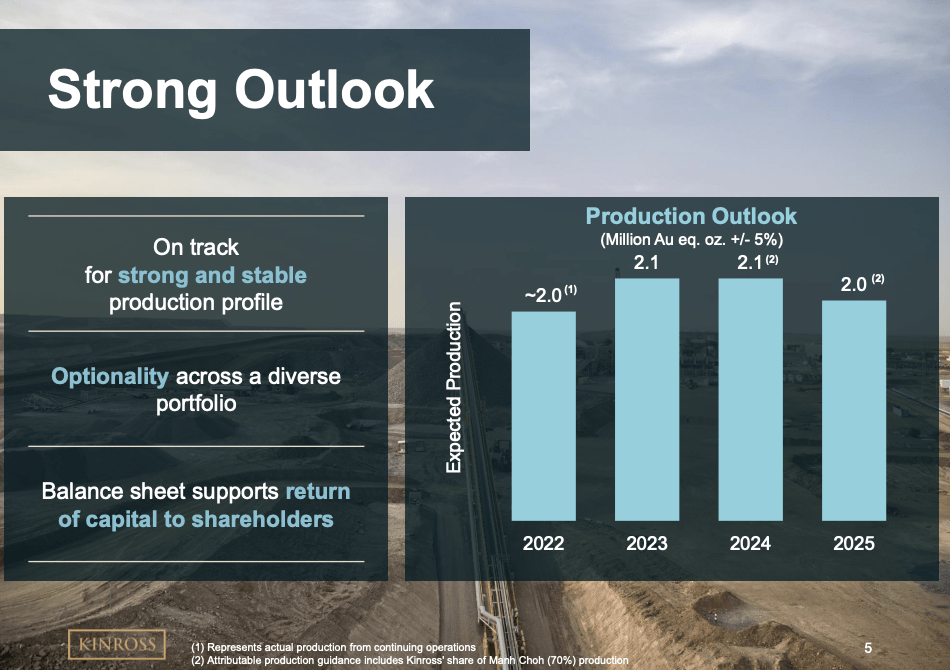

Kinross has decent production guidance. (Kinross Gold)

{kind=link}

Kinross is facing increased cash costs due to inflation, which has led to a 50% reduction in its operating cash flow, similar to other gold mining companies.

Unfortunately, this trend is expected to continue in 2023, with only a small increase in production (140,000+ ounces), but with higher cash costs.

Kinross has set its forward AISC guidance at $1,320/oz, which is one of the weaker projections compared to other gold mining companies for 2023. That means it will only produce margins of about $500/oz based on current spot gold prices; in prior years, its margins regularly exceeded $600/oz.

AISC will likely be flat in 2023-25 (Kinross Gold)

{kind=link}

Additionally, the company's annual production growth is just not impressive. It is expected to remain mostly unchanged at 2.1 million and 2.0 million ounces per year for 2024 and 2025, respectively, and at similar AISC.

This flat production and higher cash costs come at a time when the company will be investing heavily in its development projects, namely, the Great Bear project in Canada (potential 2028-29 production), while also paying out a dividend and buying back its shares.

Although I don’t believe there is an immediate risk to the company's capital returns, a potential danger arises if gold prices were to drop further, leading to an increased possibility of Kinross reducing its dividend and/or share buyback programs.

The Great Bear Project Resource Estimate: A Disappointment

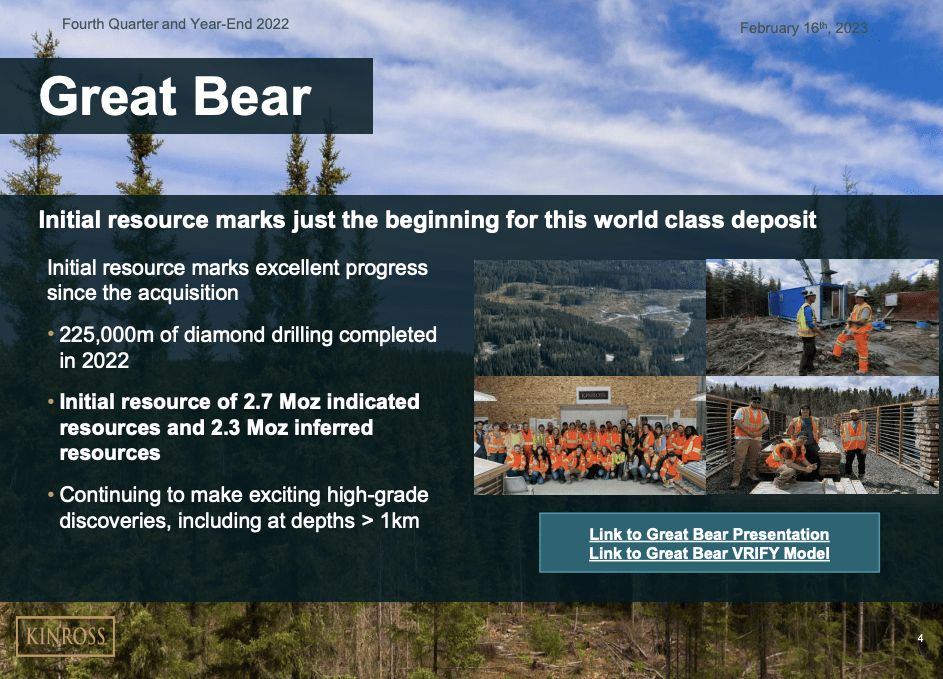

Great Bear's initial resource (Kinross Gold)

{kind=link}

In 2021, Kinross Gold paid $1.8 billion to acquire the Dixie project (now called Great Bear) from Great Bear Resources. That’s looking like a better deal for Great Bear than Kinross, at least for the moment.

When Kinross made the purchase, Dixie did not have any resource estimate yet. On Feb. 13, Kinross announced an initial 2.7 million ounce indicated and 2.3 million ounce inferred resource. So, this values the acquisition price per ounce at a whopping $360/oz, based on the 5 million ounce resource.

Note: The typical acquisition cost per ounce can vary widely depending on various factors such as the deposit's size, quality, location, and amount of infrastructure in the area. According to SP Global, miners paid $436/oz for actual gold reserves between 2020-2021, while in Q4 2020, the 4-period moving average for gold explorers was just under $50/oz .

Also keep in mind that the Great Bear project's initial resource is made up of indicated and inferred ounces, which are too speculative to be considered economic (infill drilling needs to "prove up" these resources). Therefore, the $360/oz value for the resource based on Kinross' purchase price is starting to look even pricier.

I was also expecting a bigger initial resource, based on my analysis and reading through analysts' past comments on the project.

In 2021, Mackie Research Capital Corporation predicted a mineralized inventory of more than 9.5 million ounces, and stated that “we are confident that there is upside beyond this, primarily at depth."

However, the actual initial resource was announced at 5 million ounces (2.7 million indicated, 2.3 million inferred), which is lower than the 7-8 million ounces originally predicted by the project's former operator, Great Bear Resources (in various company presentations), and lower than Mackie’s estimates.

That’s not to say that Great Bear will grow into a mammoth deposit of that size. It may still take several more years of drilling to get there. But, my current impression is that Kinross overpaid for Dixie.

Kinross Gold: The Final Verdict

In conclusion, Kinross Gold Corporation has reported its Q4 and year-end financial results, with a 35% increase in production compared to the previous year, but also a sharp increase in AISC, and a big net loss due to a non-cash impairment charge at Round Mountain.

This will not be a great year: the company is facing increased cash costs due to inflation, with only a small increase in production expected for 2023 and higher cash costs.

Its acquisition cost per ounce for the Great Bear project is starting to look high, with its initial resource estimate of 5 million ounces coming in lower than expected. This may take several more years of drilling to reach the predicted potential.

Despite these challenges, Kinross plans to invest heavily in its development projects and continue paying dividends and buying back shares. However, Kinross Gold Corporation may face a risk of reducing its capital returns if gold prices drop further.

I think there are better buying opportunities in the gold mining sector at the moment, so I'm maintaining Kinross Gold Corporation stock as a HOLD .

For further details see:

Is Kinross Gold A Buy Or Sell? And The Great Bear Debate