LMT - Is Lockheed Martin Stock A Buy After Earnings? Yes On Any Weakness

Summary

- In this article, I update my Lockheed Martin bull case using the just-released 4Q22 earnings.

- While 2023 isn't going to be a blockbuster year, we see rapidly improving demand, fading supply chain issues, and a high likelihood of accelerating revenue growth in 2024.

- Shareholder distributions are improving, thanks to higher buybacks and gradually rising dividends.

- The stock is fairly valued, making it a buy on any weakness.

Introduction

It's time to talk about Lockheed Martin ( LMT ) , my largest dividend growth investment. We're still in week five of the new year, yet defense investors have already been through a lot. Bad defense rumors out of Washington and a rapid shift from value stocks to growth stocks aren't creating the best environment for people who are overweight defense stocks like myself. That's the bad news.

The good news is that I spent the past few weeks adding defense exposure to accounts that I (indirectly) manage and supervise. This includes Lockheed Martin. The company reported its earnings last week, which came in higher than expected. Moreover, the outlook was strong and not below expectations, as we've seen in the past, as a result of supply chain and budget uncertainty.

The company is back on track, as I wrote in October. 4Q22 earnings have proven that. Demand is rising, supply chain issues are fading, and growth is rebounding for the first time in many years.

Lockheed's future is bright. If I didn't already have such a large position, I would be buying with both hands on any weakness.

So, let's dive into the details!

What Were Lockheed Martin's Expected Earnings?

Analysts were looking for $7.37 in EPS and revenue of at least $18.25 billion. In the four quarters before 4Q22, the company had beaten EPS estimates two times. It had beaten revenue estimates just once, which had everything to do with the supply chain-related difficulties in the industry when it came to turning backlog into finished products.

Hence, sell-side analysts weren't that positive going into earnings. This is what Seeking Alpha reported before the release:

Baird expects the biggest U.S. defense contractor to have a modest quarter and address delays in F-35 deliveries. "Investors should look out for commentary on 2023-25 delivery targets of 147-153 aircraft and 156 aircraft, respectively."

Goldman Sachs downgraded Lockheed ( LMT ) due to its limited ability to buy back stock . Morgan Stanley downgraded the defense contractor due to the stock's recent gains and limited room for a move higher .

Did Lockheed Martin Beat Earnings?

Yes, LMT did beat earnings!

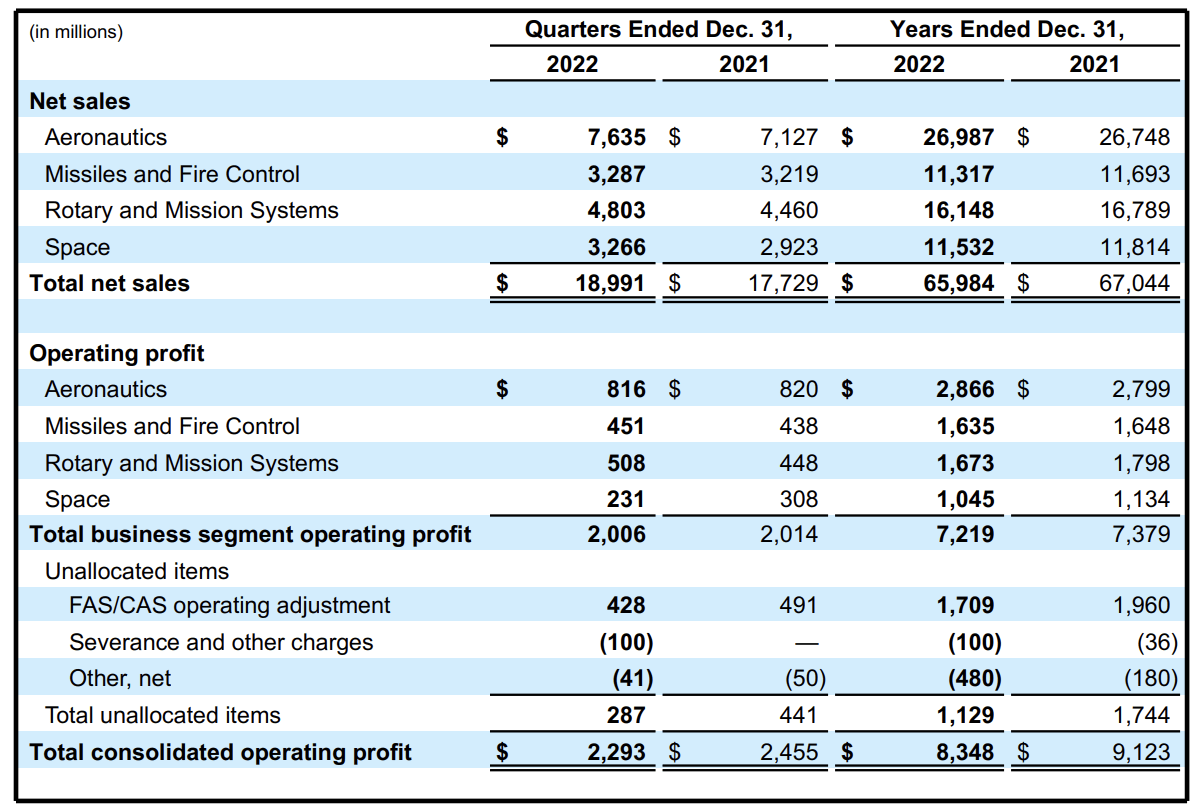

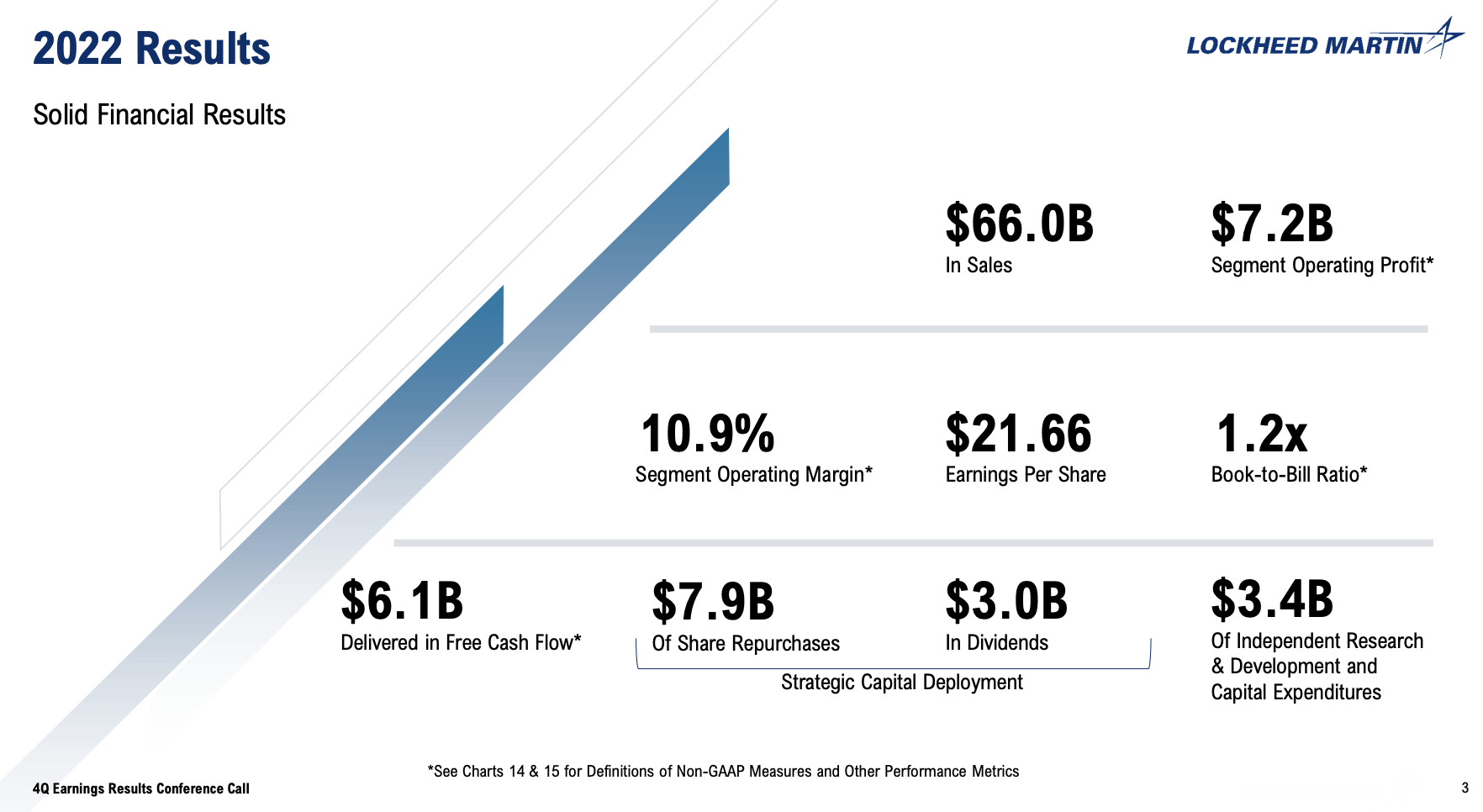

LMT reported $18.99 billion in revenue. That's a beat of $740 million and a 7.1% improvement versus 4Q21.

It helped to push adjusted EPS to $7.79, which is $0.42 higher than analysts expected.

LMT Key Metrics - What You Need To Know About 4Q22/FY22

The Bethesda-MD-based aerospace company operates four business segments.

Aeronautics, missiles and fire control, rotary and mission systems, and space.

{kind=link}

While full-year sales are down, fourth-quarter sales improved by 7%, marking the end of a turbulent year impacted by COVID, related supply chain issues, and high inflation (also related).

Besides that, the company was able to improve margins, and it also benefited from 11% growth in its order backlog. The company is now sitting on a $150 billion backlog value. The book-to-bill ratio is 1.2x, which means that orders are coming in much faster than the company can turn them into finished products/services. That is indicative of higher growth in the future and good news when it comes to demand developments.

{kind=link}

In addition to higher orders for its F-35 program, the company saw strength in all areas, including classified security solutions in its space and missiles and fire control segments. In these segments, the company booked $1.5 billion in orders, reflecting higher demand to replenish US stocks and improve global security services.

On a full-year basis, the company saw slow growth in aeronautics. 1% year-on-year growth was supported by higher classified sales. Lower F-35 sales were a headwind. Operating profit increased by 2%, thanks to higher net favorable profit adjustments, partially offset by lower sales volumes.

The backlog in this segment increased by 15%. The company also secured production for F-35 lot 15 through 17.

In missiles and fire control, sales were down 3% due to lower volume and sales related to the withdrawal from Afghanistan. However, the backlog was up 6% due to higher demand for tactical missiles.

In rotary and mission systems, sales were down 4% due to non-recurring revenue issues related to its training business in 2021. Also, lower C6ISR and Black Hawk volumes pressured the segment's top line.

That said, the backlog was up 4% due to new orders for missile defense and Sikorsky helicopters and services.

In space, sales were down 2% due to the 2021 re-nationalization of the AWE program, partially offset by growth in the next-generation interceptor program. Backlog was up 16% thanks to strong classified programs and Orion orders.

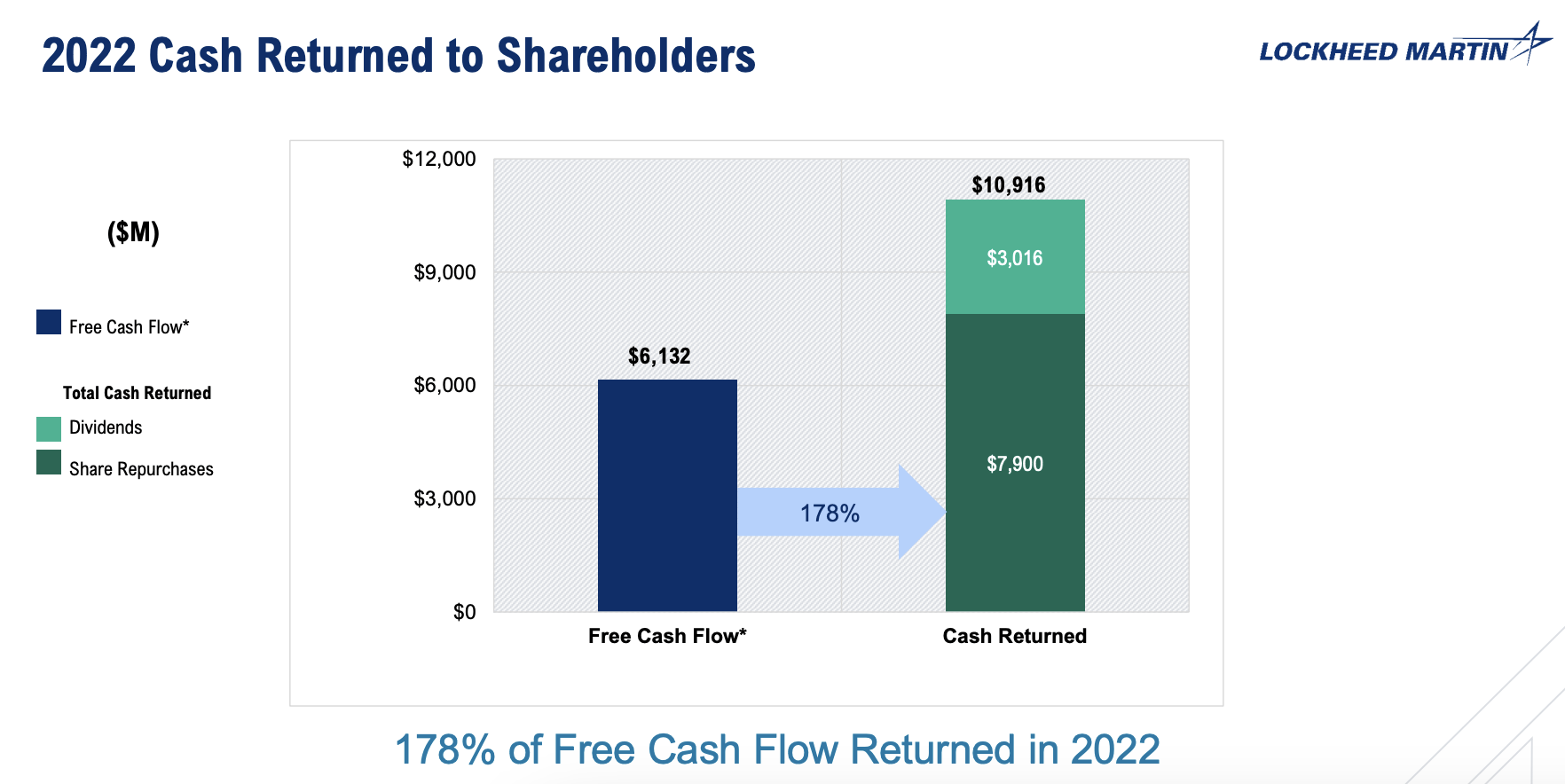

When it comes to shareholder returns, the company returned $10.9 billion to its shareholders. $7.9 billion was returned indirectly via share buybacks. $3.0 billion was returned directly via dividends. In 4Q22, LMT entered into an accelerated buyback program of $4 billion. In September, it hiked its dividend by 7.1% to $3.00 per share per quarter. This implies a 2.6% yield. Total free cash flow was $6.1 billion, which means Lockheed used its healthy balance sheet to buy back shares at attractive prices.

So far, the company has $10 billion remaining under its buyback program, which will be used over the next few years.

{kind=link}

In 2022, net debt was $12.9 billion. That's up from $8.1 billion in 2021. This increase is caused by the aforementioned shareholder distribution funding gap. However, the debt ratio rose from 0.80 to 1.30x EBITDA. The debt ratio was way too low. I agree with management to use a very healthy balance sheet for buybacks at attractive prices. The company's credit rating remains A-, as leverage is expected to remain in the mid-1.0x range.

So far, so good. These numbers are mildly boring (as in "expected"), as supply chain issues and the timing of programs pressured sales. However, demand is improving, which is why I'm writing this article. It's also why the outlook is so much more interesting than what happened in 4Q22.

What To Expect After Earnings

On a full-year basis, LMT expects to generate net sales of $65 to $66 billion. Analysts were looking for $65.8 billion, which means it's fairly in line.

Diluted EPS is expected to be $26.60 to $26.90, which is also in line with expectations of $26.80. Free cash flow is expected to be $6.2 billion. That's slightly higher compared to 2022 and implies a 5.3% FCF yield using LMT's $117.3 billion market cap. That's a great number and supportive of dividend growth close to double-digits and buybacks.

One of the reasons why free cash flow and margins are expected to rise is the transformation of business processes. This 1LMX multi-year program aims to improve internal business processes and systems.

According to CEO Jim Taiclet :

In 2022, we completed a majority of the detail design for our new systems and business processes. And for 2023, we expect to complete the detailed design and implementation road maps that go with it, and then we'll transition to the system build and configuration phase over the next couple of years.

That said, earlier in this article, I told you that the book-to-bill ratio is now 1.20, which means that order growth is improving. One of the major drivers of demand is the US government. In late December, Congress signed the FY23 Omnibus spending bill into law, appropriating $858 billion for National Defense, including $817 billion for the Department of Defense budget. This implies 10% year-on-year growth.

It's also 6% (or $45 billion) higher than President Biden initially requested, which goes to show that the priorities have shifted.

Europe, for example, is looking to boost defense by EUR 70 billion over the next three years. Japan's defense budget is expected to rise 26% this year!

As we discussed in prior articles, Lockheed delivers the hardware and services needed that support the defense requirements of NATO members and its allies.

This is what Lockheed CEO Taiclet had to say concerning higher budget growth:

These appropriations enabled us, along with the Joint Program Office, to finalize the contract for the production and delivery of up to 398 F-35s for $30 billion in Lots 15 and 16, including the option for Lot 17. Further, several other of Lockheed Martin’s programs received the funding levels necessary to drive the growth outlook we previously identified, including our combat rescue helicopter, the C-130J, Blackhawk, CH-53K and FAAD.

Here are some noteworthy developments related to everything we just discussed:

- In addition to finalizing contracts for F-35 lots 15 and 16, the company received authorization to produce long lead items for lot 18 F-35 aircraft for the US Air Force, Marine Corps, Navy, and US allies as well.

- The company welcomed Germany to its F-35 Lightning II program. The nation is now the ninth foreign customer.

- Canada became an F-35 operator in January as it selected Lockheed to replace its aging aircraft fleet.

- Lockheed remains confident that it can ramp up F-35 deliveries by 2025 to 156 per year. In 2022, that number was just 141 due to a temporary pause in operations and the corresponding suspension of engine deliveries.

- Moreover, the U.S. Navy authorized the CH-53K King Stallion heavy-lift helicopter to enter full-rate production.

- Related to this, the Australian Army announced its intent to acquire 40 UH-60M Black Hawk helicopters to replace its current multi-role helicopter fleet. Deliveries are expected to begin this year.

- Lockheed and its partners successfully conducted a hypersonic-boosted flight test of the Air-Launched Rapid Response Weapon, meeting all of its objectives for the test. This is key in the global competition for the most efficient and powerful hypersonic weapons.

- The company is also seeing great progress in the Next-generation Interceptor program with the delivery of the first NGI flight software package to the Missile Defense Agency. Ahead of its schedule, I should add.

That said, Lockheed did not win the award for the Future Long Range Assault Aircraft (FLRAA). Textron ( TXT ) won that award, although Lockheed is now in a formal protest as it believes that its Defiant X program would be more suitable.

While we wait for that to play out, it is good to mention that Lockheed is confident that it may get the deal for the Future Attack Reconnaissance Aircraft (FARA). Its prototype is over 90% complete, and Lockheed believes it is the only company with the technology to get the job done. In 2025, we'll see who gets the deal for the FARA program.

Concerning its supply chain, the company sees gradual improvements. After having read reports from all competitors, supply chains will likely normalize going into 2024.

And I would say the entire value chain, whether it's our internal operations and the supply chain, was able to meet that increased level of requirements. So that, to me, bodes well to the future as well as expecting a gradual improvement in 2023. And I think that just provides a reasonable assumption and a reasonable basis for that assumption.

Risks

There are two major risks. The first one is ongoing supply chain issues. However, I do not expect that risk to materialize. The consensus is a return to normal at the end of 2023, I think that's a fair and safe assessment. Moreover, if economic growth slows further, competition for qualified labor and high-tech materials will fall. Defense companies have anti-cyclical demand. They will benefit from that, which could cause supply chains to improve even faster.

Risk number two is related to funding risks. As I wrote in a recent Raytheon Technologies ( RTX ) article :

While the 2023 defense budget is 10% higher, new policy risks have emerged.

Defense One

(Some) Republicans, led by Speaker Kevin McCarthy, call for defense spending cuts. McCarthy wants defense spending back at 2022 levels, implying a $75 billion cut from current levels.

After having spent way too much time watching political shows, I believe that he is mainly looking for cuts that are not related to hardware and next-gen technologies. He's combatting "woke" spending, which is mainly used for political reasons.

While I do not disagree with more targeted funding, there are now high risks that defense spending growth could be subdued in the years ahead. I believe that he won't achieve any cuts, but it's a risk to keep in mind. After all, the defense supply chain is in desperate need of funding.

Valuation

Related to what I just said above, 2023 isn't going to be a blockbuster year.

{kind=link}

Top-line growth is expected to rebound after 2023. In 2024 and 2025, revenue growth is expected to be 3.1% and 3.9%, respectively.

We continue to expect 2023 sales about the same level as we discussed back in October. We also continue to expect a return to sustained top line growth in 2024 and beyond as headwinds diminish in our program mix, the supply chain continues to recover, and our signature programs grow.

Based on these numbers, LMT is trading at 13.7x EBITDA. That valuation is not cheap. However, it's a fair value, given the bigger picture.

Moreover, an implied free cash flow yield of roughly 5.5% is a good deal. Investors are not overpaying to get access to free cash flow. As a dividend investor, that is very important to me.

Needless to say, as I said in the article, I expect another juicy dividend hike in 2023 and strong buybacks - especially at these levels.

Is LMT Stock A Buy, Sell, Or Hold?

It probably does not come as a surprise, but I continue to rate LMT as a buy.

While LMT is not a fast-growing dividend stock like some of my other holdings, I made it my largest holding for a reason. The company brings a mix of safety, moderate growth, and high shareholder distributions to the table.

After two tough years, the company is back on track. Supply chain problems are easing, and demand is rapidly improving, making it likely that the top line will accelerate on a long-term basis after 2023.

Meanwhile, free cash flow is strong, giving management reasons to engage in large buyback programs while boosting the dividend.

Hence, my advice remains simple. If you believe LMT is right for you, buy or add on any major correction. It's what I have been doing, and it has added so much value and stability to my portfolio.

(Dis)agree? Let me know in the comments!

For further details see:

Is Lockheed Martin Stock A Buy After Earnings? Yes, On Any Weakness