LMT - Is Lockheed Martin Stock Still A Buy?

2023-07-20 09:41:17 ET

Summary

- Lockheed Martin's Q2 2023 results show an 8% increase in total sales to $16.7 billion, despite challenges in the defense equipment and services sector and supply chain constraints.

- The company increased its 2023 revenue and profit outlook during the Q2 earnings presentation, with most of the EPS growth driven by share repurchases.

- Despite a challenging supply chain backdrop, elevated defense budgets in the year to come should provide solid support to growth for Lockheed Martin.

Lockheed Martin ( LMT ) posted its second quarter results on the 18 th of July before the opening bell. Since posting its first quarter results, shares have lost around 10% of their value. Indeed, there are some challenges ahead but the current environment for defense equipment and services provides an appreciable backdrop that is not yet recognized by investors and analysts.

Lockheed Martin Q2 2023 Results: Profit Growth Falls Short Of Revenue Growth

{kind=link}

A major item to wrap your head around is the fact that the demand environment for defense equipment and services is strong, but that's not going to result in increased sales from one day to the other. The evaluation and procurement processes are long with many milestones to be cleared before a sale is recovered or even a purchase agreement is drafted. So, the positive demand environment we see today is not something that translates into sales any time soon. 2024 is in fact the earliest point where defense contractors see this happening more prominently. On top of that, driven by some program-specific pressures and global supply chain issues, sales might not be directly reflective of demand but of supply chain constraints on which a layer of program transitions can be added. So, while the outlook is strong there are definitely some pressuring elements.

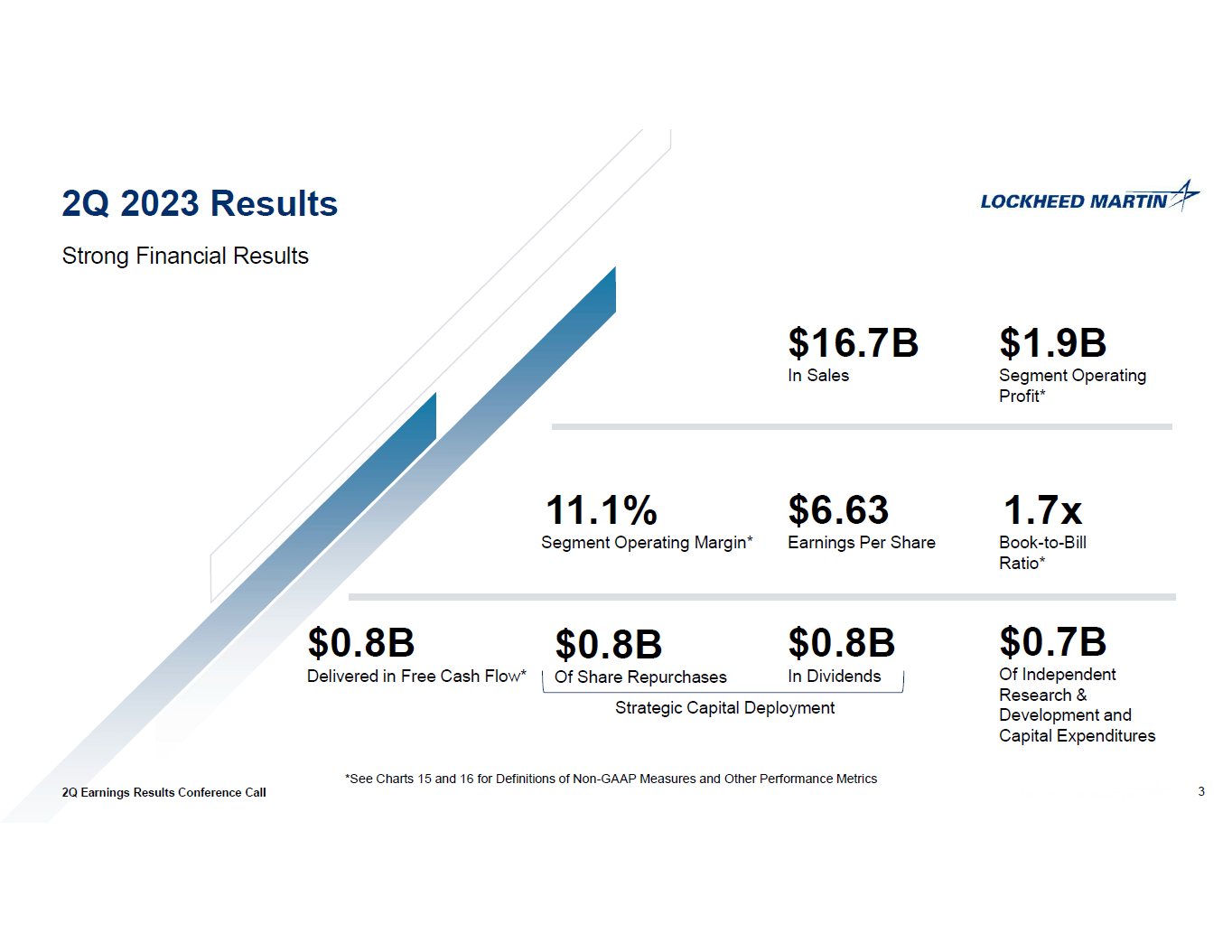

Total sales were up 8% to $16.7 billion driven by some program award timing weakness in the same period last year. Interesting to keep in mind is that book-to-bill was 1.7x which confirms that an improving defense environment is not resulting in a big addition to the backlog. As mentioned, there's a timeline for contracts to be added to the backlog, so that materialization is not immediate or near term.

{kind=link}

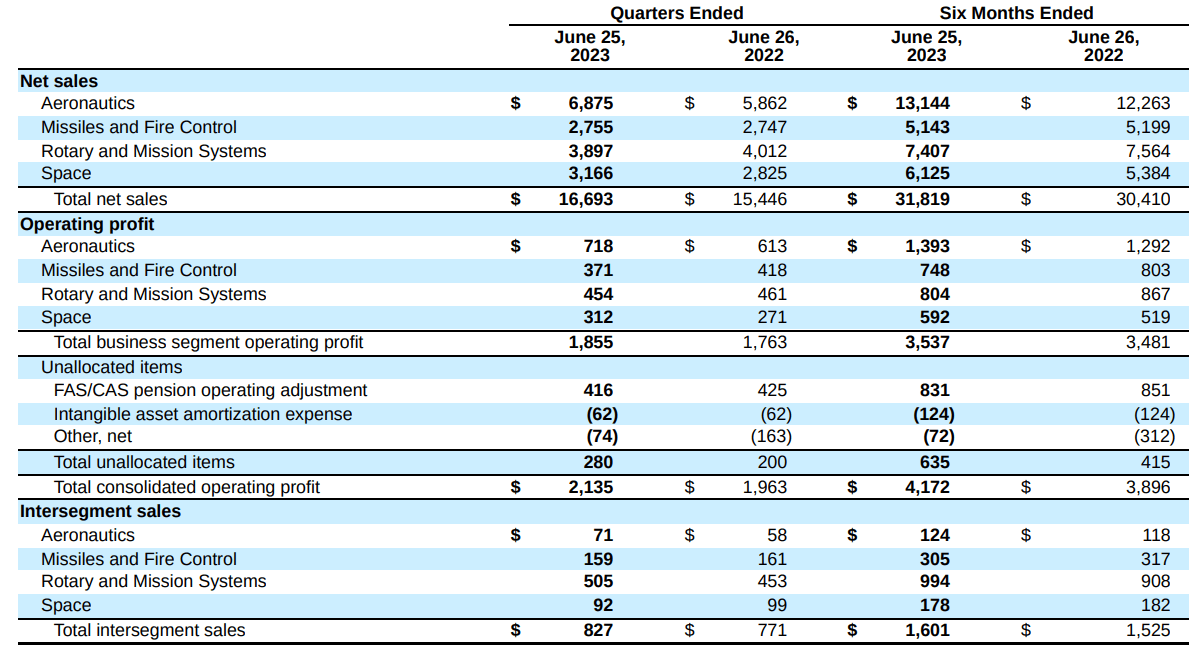

The aeronautics department saw revenues increase by 17% or $1 billion driven by lower F-35 deliveries presenting a $335 million revenue pressure. This was driven by higher F-35 volumes, higher production contracts for the F-35 given the unfavorable timing of contracting in the same quarter last year bringing the total F-35 sales increase to $735 million. C-130 program sales were $90 million higher while classified sales were $100 million higher while margins remained stable on 10.4% compared to 10.5% last year.

The Missile and Fire Control segment experienced flat sales at $2.775 billion as $20 million in higher sales in the tactical strike and missile programs was offset by lower Terminal High Altitude Area Defense sales. The margins in the segment dropped from 15.2% to 13.5% driven by lower profit booking adjustments compared to last year driven by HIMARS and the JASSM missile for the strike missiles segment and lower targeting pots and infra-red search and track adjustments of $25 million. While sales and margins were not quite as strong, the book-to-bill during the quarter was 3.3x and that shows how increased demand is adding to the backlog but not immediately or to the same extent to sales.

Rotary and Mission Systems revenues decreased by $115 million or 3% driven by lower Black Hawk sales valued $145 but partially offset by $60 higher Aegis and TPY-4 integrated warfare systems and sensors. RMS saw margins remain stable year-over-year.

The highest growth segment was Space with a $341 million or 12% increase in sales. This was driven by $150 million by the Next Generation Interceptor program and $120 million in classified programs and national security space programs while Orion sales set commercial civil space programs $65 million higher. Profit growth of 15% outpaced top line growth driven by the Orion program and higher equity earnings on ULA launch services.

Overall, results are not bad but we see some variability in the performance between segments and profit growth could not keep track of revenue growth.

Lockheed Martin Increases 2023 Financial Outlook

{kind=link}

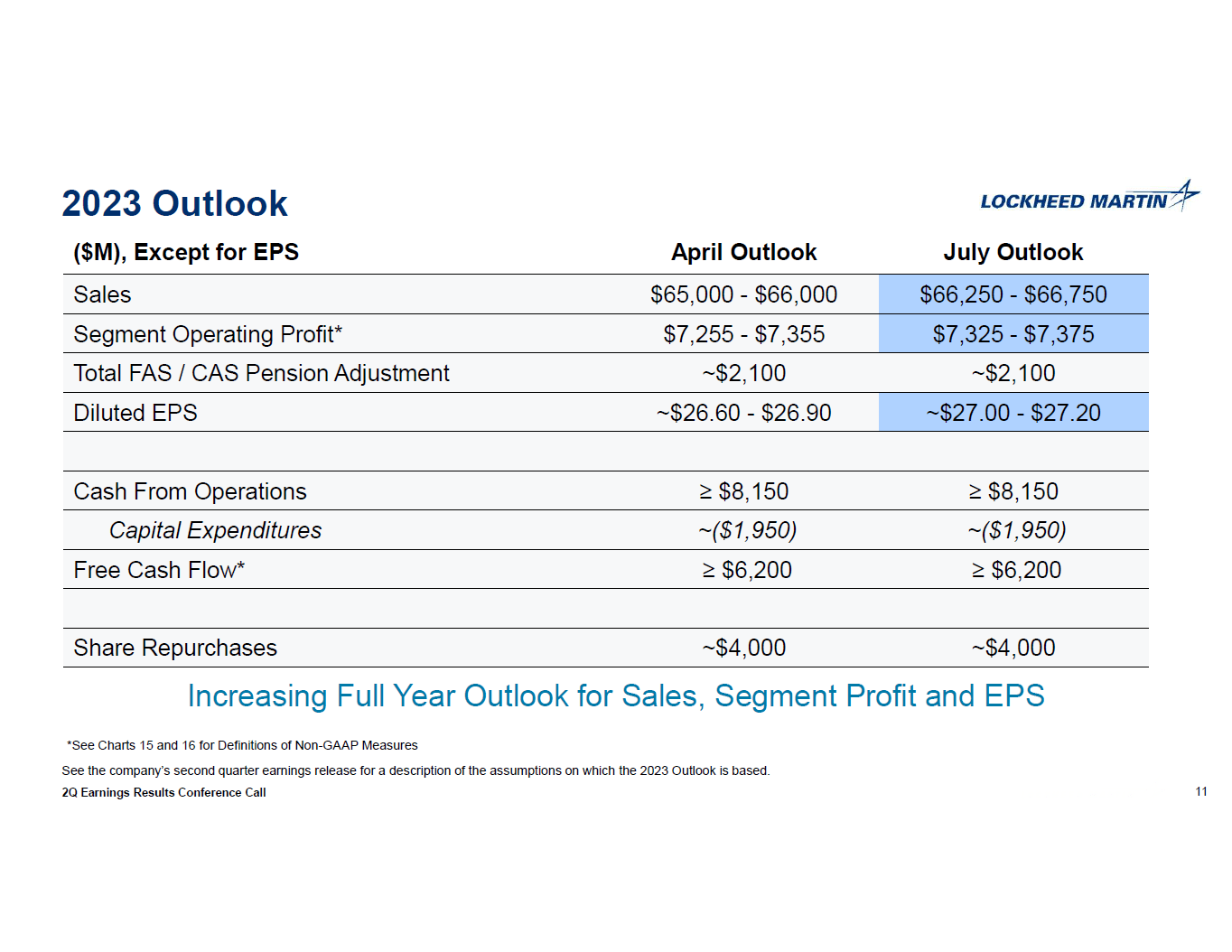

During the second quarter earnings presentation, Lockheed Martin increased its revenue guide by $1.25 billion on the low end and $750 million on the high end while it increased its profit outlook by $20 million to $70 million. In relative sense, we are not talking about big changes to the outlook, but they are nevertheless welcome ones as 2023 has been marked by Lockheed Martin as a transition year. Compared to last year, Lockheed Martin is guidance for 2% higher profit and 20% higher earnings per share. So, most of the EPS growth is really driven by share repurchases.

Is LMT Stock A Buy?

{kind=link}

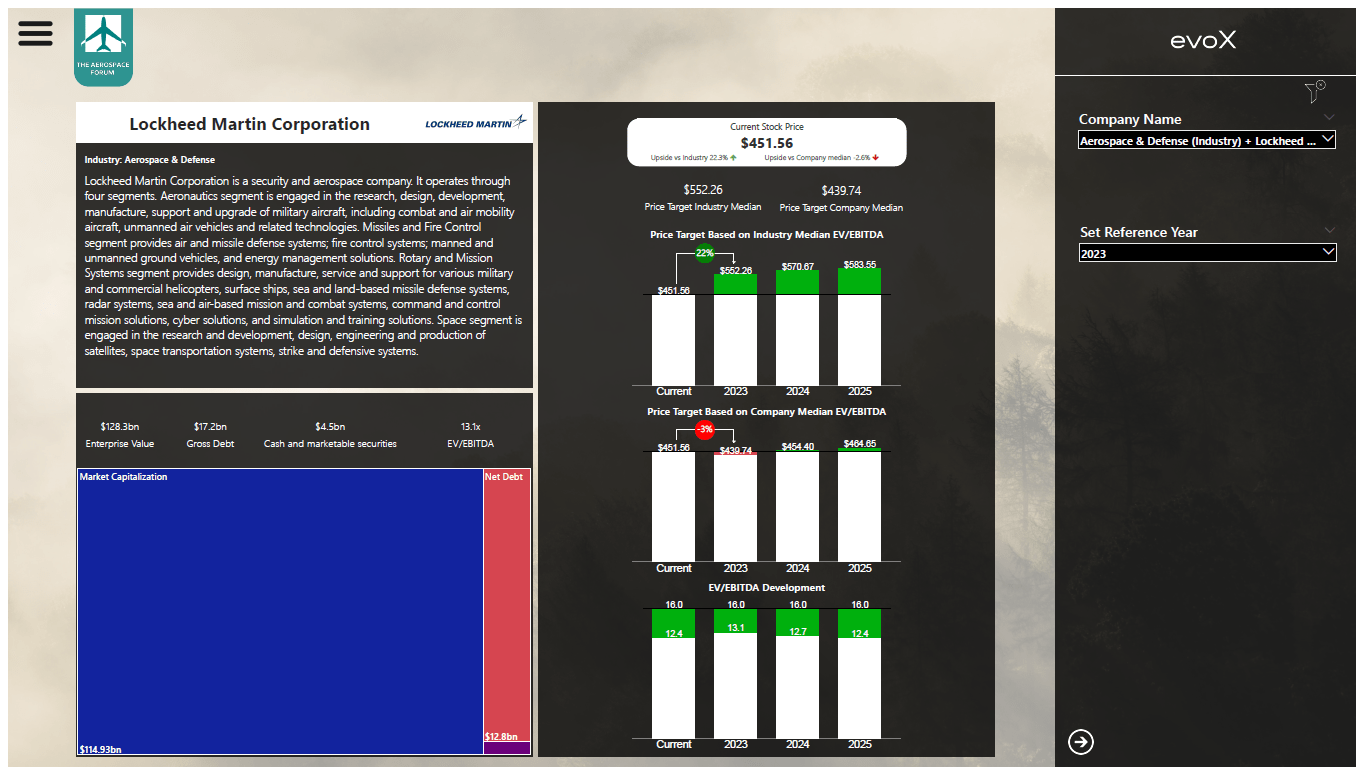

Valuing Lockheed Martin is tricky. We are currently in a high demand environment for defense equipment and services, but simultaneously the upside is constrained by supply chain issues. That means that if those issues do not dissolve in the years to come, the overall upside to results is limited. Lockheed Martin has already hinted that 2023 will be a transition year, and in the years beyond, the company will return to growth. The complicating factor is that Lockheed Martin has an EV/EBITDA median multiple that is lower than that of the industry and would suggest that even towards 2025 there is extremely little upside to the stock.

At the same time, one can wonder or should wonder whether a lower multiple compared to the industry is justified because the reality is that the defense budget environment is going to be a positive one for the years to come with F-35 and F-16 international sales potential is growing stronger rather than weaker and supply chain challenges are industrywide and not just limited to Lockheed Martin and thus a discount to the industry multiple might not make sense. I ran a valuation for Lockheed Martin using the evoX Financial Analytics tool and my estimates show that Lockheed Martin stock has 22% upside to roughly $553 per share.

Conclusion: Aerospace Industry Valuation Shows Buy Signal For Lockheed Martin

The current results are actually not extremely important to Lockheed Martin in the sense that absent of surprises in either direction, 2023 is going to be a transition year. In that regard, even the outlook for 2023, which included an increase to the guided ranges, is not the most interesting. The growth will be in 2024 and beyond driven by significant demand for defense equipment that I believe is not yet baked into the analyst assumptions for the years ahead which should also result in continued shareholder returns in the form of buybacks and dividend increases. That does justify a valuation closer to the aerospace industry median and provides significant upside for 2023 and the years ahead. I believe that while Lockheed Martin might be a hold in the books of some analysts and shareholders, it does not quite capture the growth prospects ahead yet which are difficult to assess given the long-term nature of the industry and the complexity of the industry.

For further details see:

Is Lockheed Martin Stock Still A Buy?