CA - Is Magna A Good Buy After The Recent Earnings Event?

2023-11-07 13:20:54 ET

Summary

- Magna recently gapped up post earnings and is up by 9% since the event.

- We are enthused by the operational improvements demonstrated by Magna and this is something that could linger through FY25.

- Earnings through FY25 are poised to come in at 3x the pace of topline growth.

- Despite higher CAPEX commitments, Magna has not compromised on its dividend and currently one can pick up a yield figure that is 60bps higher than the historical average.

- We appreciate the current risk-reward on the charts.

Introduction

Magna International ( MGA ), the Canadian-based auto component supplier came out with its Q3 results towards the end of last week. The stock has since gapped up and is now 8-9% higher post earnings. Despite the decent rise in the share price, we think MGA could still be a rewarding investment. Here are three broad reasons why we're bullish on the stock.

Forward Valuations Don't Capture The Sustainable Operational Improvements

One of the standout aspects of Magna's Q3 results was how effectively it has been able to engender operational margin improvements, even in the face of the unwelcome UAW strikes. For context, in Q3, the UAW issue dampened the topline by 55m, and left a -10bps impact on group margins, but still, the company was able to facilitate 90bps of EBIT margin improvements (YoY), taking the overall group margin to 5.8%.

There are a couple of drivers behind the improving operational landscape. Firstly, there's the inherent strength of the operating model where MGA was able to demonstrate decent pricing strength and recover some of its higher input costs from its clients. Secondly, they were previously operating a bunch of underperforming facilities, but recently productivity and efficiencies here have stepped up there.

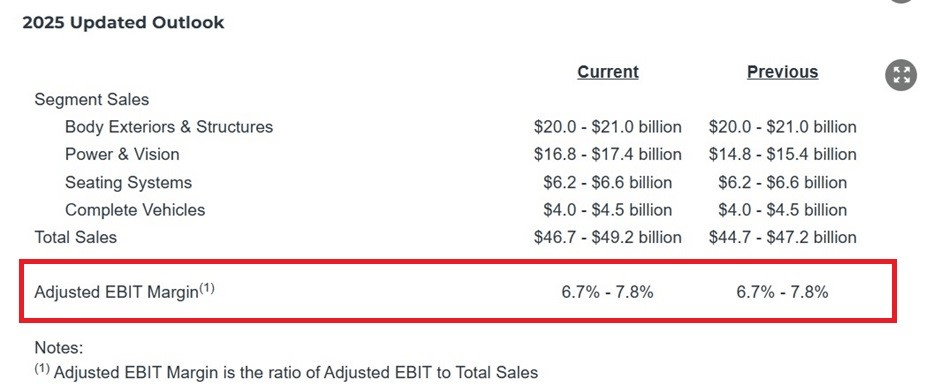

What's key is that these operational improvements aren't a one-off, and will likely linger through the foreseeable future. Besides the reported numbers, management also lifted the FY EBIT margin outlook from previous levels of 4.9-5.3% to 5.1%-5.4%. This also means that after delivering EBIT margins of only 4.8% in H1, the implied EBIT margins for H2 will likely be a lot higher at 5.6%. When MGA management was probed if margins would step down in H1, they refuted that suggestion and rather implied that they would look to kick on higher from the 5.5% base. Investors should note that over the next couple of years, these EBIT margins could potentially expand by 230bps and even hit levels of 7.8% by 2025.

{kind=link}

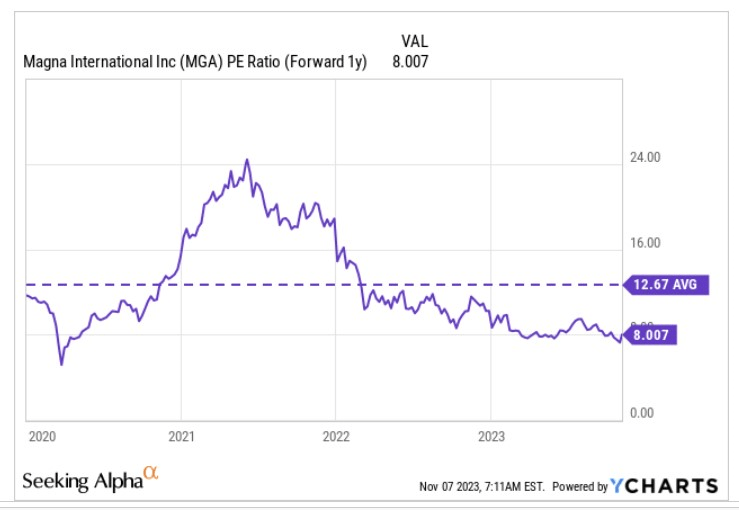

Now, if one looks at the degree of operational improvement that will likely come through, we think valuations of the stock look far too cheap. Consensus estimates all through FY25 suggest the company's topline CAGR will come in at 8%, but what's impressive is bottom-line CAGR during the same period will likely come in at over 3x that level at 25% CAGR!

YCharts

Now for a business that looks poised to deliver impressive medium-term bottom line growth of 25%, we think it's a real bargain to own as it is currently priced at a forward P/E of just 8x. This also translates to a massive 37% discount to the stock's long-term average.

{kind=link}

A Useful Dividend Theme That Is Not Encumbered By The Growing Capital Intensity

Even if you're not overly swayed by the core story of MGA, we feel the dividend facet is certainly worth considering. For context, note that whilst most other options in the sector have only been paying dividends for a little over 2 years, Magna has been doing so for 11 years now.

The dividend credibility gets enhanced even further when you discover that Magna is one amongst only 49 other international stocks that currently make up the Nasdaq International Dividend Achievers Index, or DAT . For a certain stock to be considered for DAT, it needs to display a track record of growing dividends for 5 successive years.

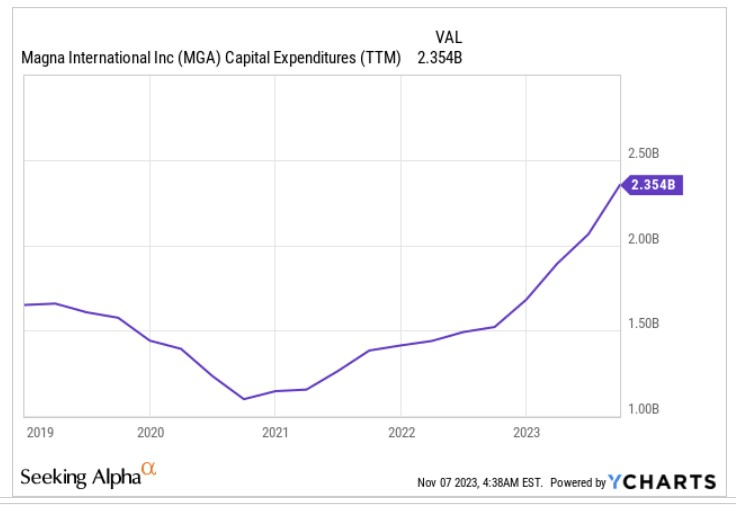

Its commendable that MGA has been able to keep growing its dividends, particularly during recent periods when it has ramped up capital spending (see image below) to support the launch of future programs. Note that even though CAPEX plans have been scaled up, MGA is not inundating itself with excess debt. As of Q3, the company's adjusted debt to EBITDA stood at a healthy level of 2x, and this is something management believes will decline by Q4 and well into FY24.

{kind=link}

Nonetheless, coming back to the dividend theme, what's key is that, if you get in at current levels, you could be locking in a rather tasty yield of 3.44%, almost 100bps better off than the sector median, and almost 60bps more than what the MGA stock typically yields (4-year average)

Closing Thoughts - Technical Considerations

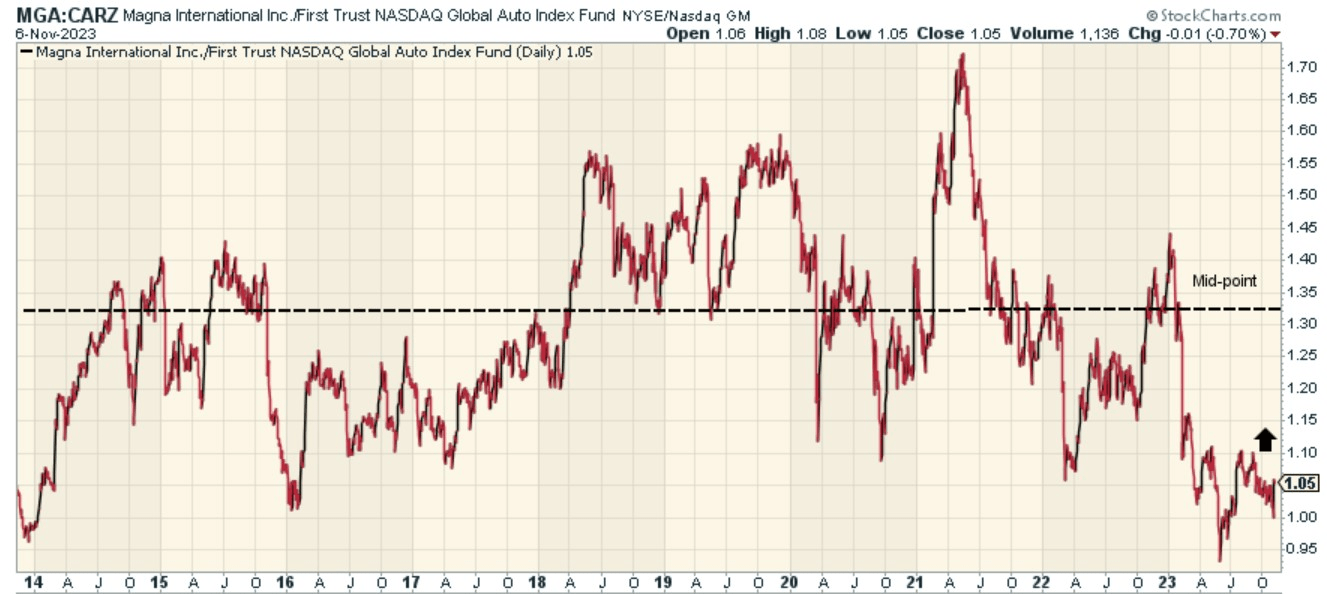

We also feel rather enthused by the current risk-reward on the charts. The image below helps speculate on MGA's potential rotational quotient, for those interested in the global auto space. Rotational quotients are typically highest when the relative strength ratios of stocks vs a diversified industry product are at the lower end of the long-term range and vice versa. What we can see is that MGA's strength relative to the CARZ universe is currently around 20% off the mid-point of the decade-long range, thus offering up decent scope for mean-reversion. It's also worth bearing in mind that currently a lot of auto stocks that are heavily exposed to the EV segment are not finding too many takers as issues of slowdown emerge. In that regard, MGA is well placed. Whilst it has long-term ambitions to flourish in the EV space, currently its EV exposure is quite marginal at less than 10%.

{kind=link}

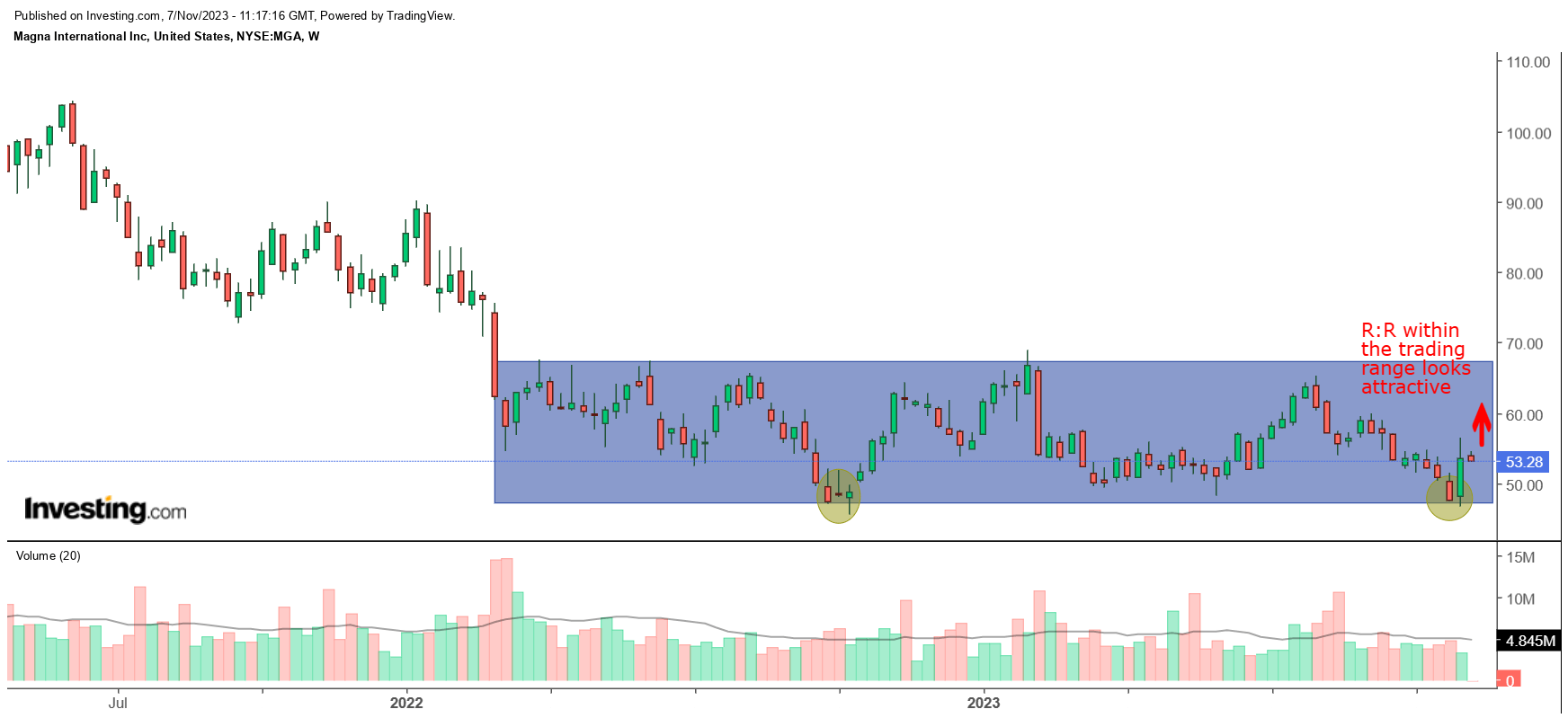

Then if we focus just on MGA's weekly price alone, what we can see is that after a steep downtrend, the stock has spent around 19 months chopping around within the $47-$67 range.

{kind=link}

This could well be an accumulation phase ahead of a breakout and last week's bullish engulfing candle was very encouraging in that it negated the three preceding candles before it. Nonetheless, even if the eventual breakout from the trading range doesn't quite take place, buying in at these levels would represent a more prudent usage of funds, rather than buying the stock just below the breakout level of $67, where the downside risk could be far greater.

For further details see:

Is Magna A Good Buy After The Recent Earnings Event?