SPY - Is The Party Over At DICK'S?

2023-10-26 21:22:27 ET

Summary

- DICK'S Sporting Goods stock has surged in recent years, outperforming the broader market.

- We think that the boom times of the post-COVID era, however, may be coming to an end.

- The resumption of student loan payments poses a threat to consumer spending, particularly in discretionary retail.

Background

The American consumer is a thing to behold--time and time again economists have forewarned us that spending is about to dry up, that consumers are now stretched too thin, and that the recession they've been forecasting for what feels like a decade now is finally around the corner.

It's happened so often that it's difficult not to see yet another prediction of a consumer spending slowdown as a Chicken Little story.

And yet, that is what we are here to do. Today, we take a look at DICK'S Sporting Goods, Inc ( DKS ). The company, despite recent bumps in the road, has had a stellar few years.

{kind=link}

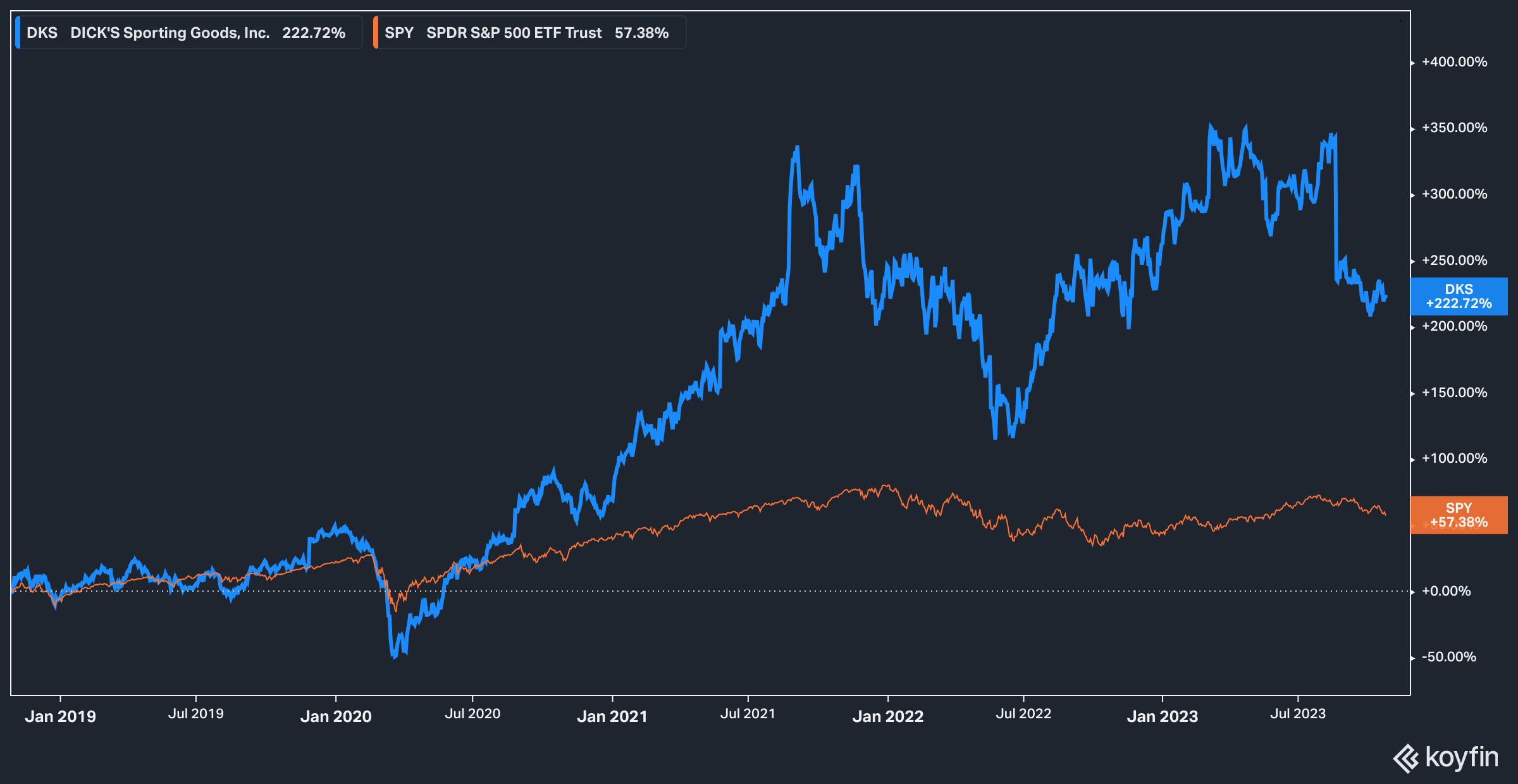

In the last five years the outdoor and athletic retailing chain has handily beaten the broader market, delivering a price return of 222% (total returns were 283%) against the S&P 500's ( SPY ) comparatively tame return of 57%.

In this article we intend to make the case that, unfortunately, the boom times are likely to be over at DICK'S.

Let's dive in.

A Story of Margins

To paraphrase legendary investor Jeremy Grantham, profit margins are some of the most mean-reverting numbers on Earth. This illustrates what we believe to be a fundamental truth of competition in the marketplace: when product offerings are not unique or commoditized (like outdoor gear) instead of singular and difficult to replace (like a search engine), it is nearly impossible for one participant to get away with making more money than another.

In other words, high profits can be competed away as consumers look for the best deal.

With that in mind, consider this chart:

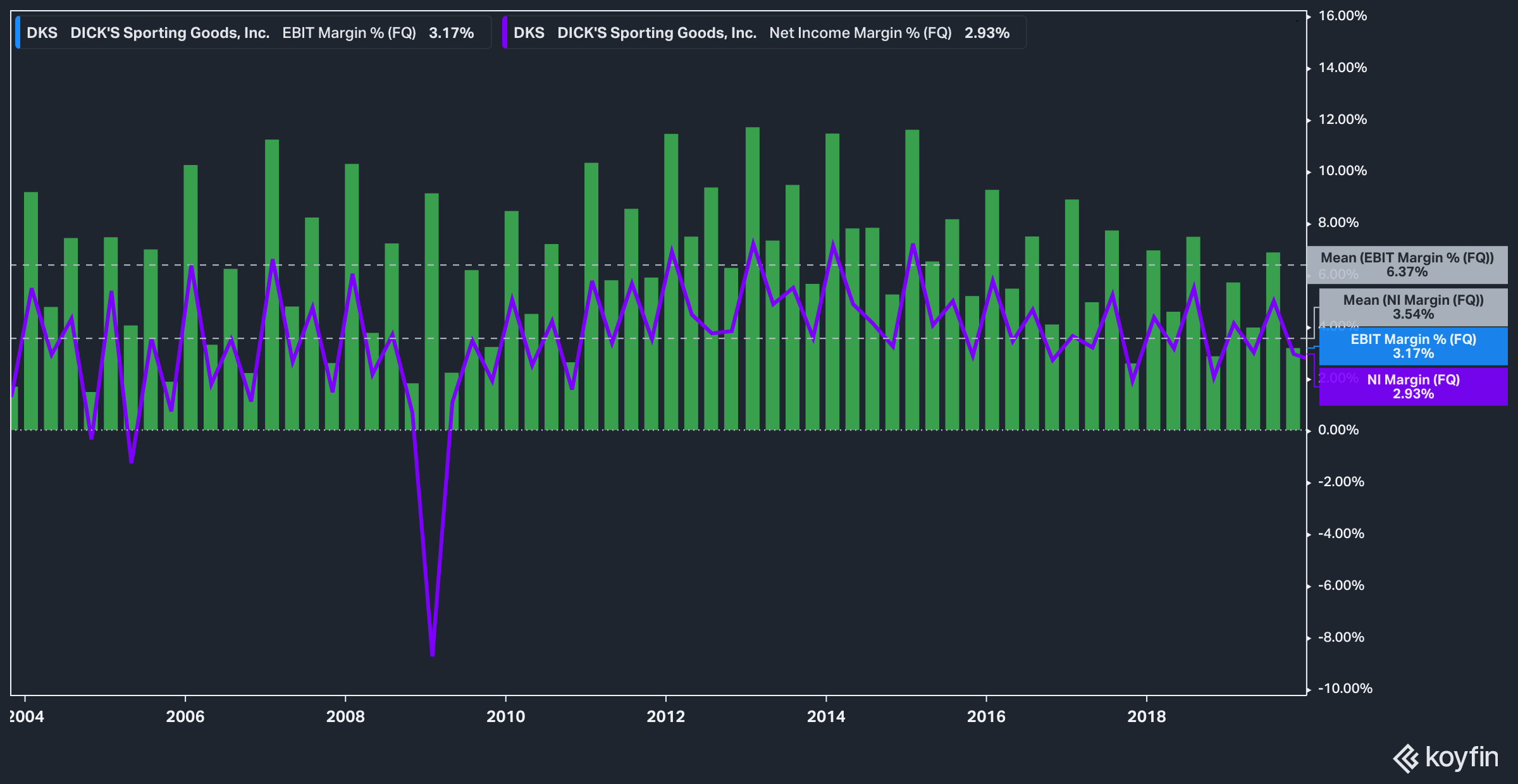

DKS EBIT and Net Profit Margin (Koyfin)

{kind=link}

From October 2003 until the end of 2019, DICK'S achieved an average operating margin of 6.37%, and a net profit margin of 3.54%, which are respectable for the consumer retail space where margins are notoriously thin.

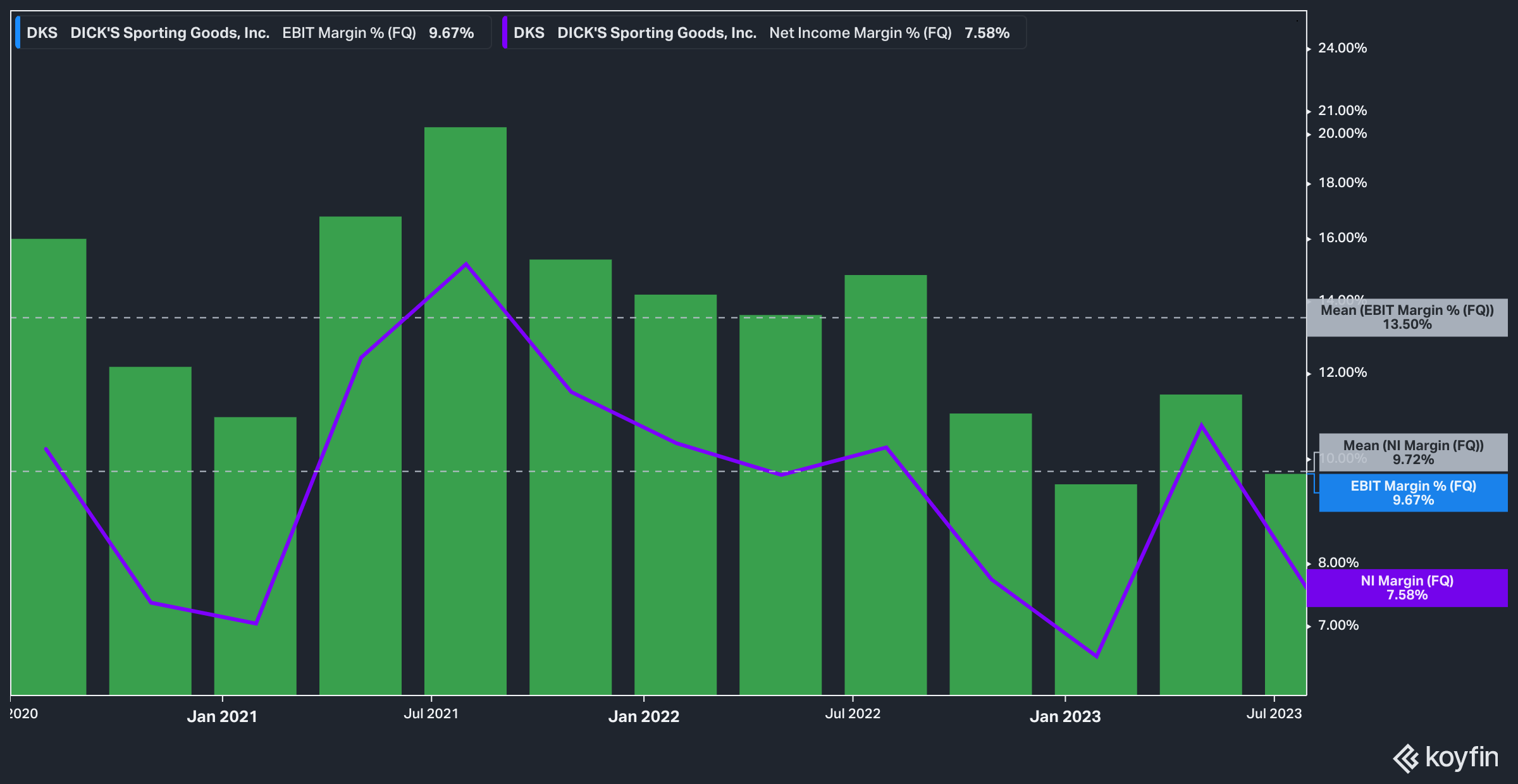

DKS EBIT & Net Profit Margin (Koyfin)

{kind=link}

Now, consider the company's average profit margin from the quarter ending August 2020 until today. In this time frame, DICK'S has achieved an average EBIT margin of 13.5%, and a net profit margin of 9.72%--both massive increases over the company's pre-pandemic averages. In the latest quarter, the company printed an EBIT margin of 9.67% and a net profit margin of 7.58%.

How sustainable is this?

In our view, not very.

There are several things that go into our thinking here. First is the emerging trend of brands distributing their offerings through their own channels, where they can capture more of the profit for themselves.

For DICK'S, a key partner in this regard is Nike ( NKE ). On the latest conference call , Nike was brought up in three separate instances, each time being highlighted as a key partner of the company's strategy. From our reading of the transcript, Nike was the only partner mentioned by name.

Those who follow the consumer retail space closely will doubtless know then that a partnership with Nike may not be the sure thing it once was, not because the brand has lost its mojo, but because it is focusing heavily on moving its product through its direct to consumer platform. Just take a look at Foot Locker ( FL ) to get a sense for how things have unfolded for them. (For complete clarity, we are not suggesting that DICK'S relationship with Nike is in peril in any way, we simply see a risk that Nike could pull back as direct-to-consumer offerings are typically more profitable.)

Second, DICK'S lacks sustainable pricing power: it cannot reasonably charge far more for products that can be purchased more cheaply elsewhere forever. Consumer retail simply isn't that kind of business.

The Consumer

We kicked off this article discussing the ever-strong spending power of the American consumer and how plenty of people smarter than us have been made to look silly with predictions that things are about to change.

Well, we are here to say that things are about to change.

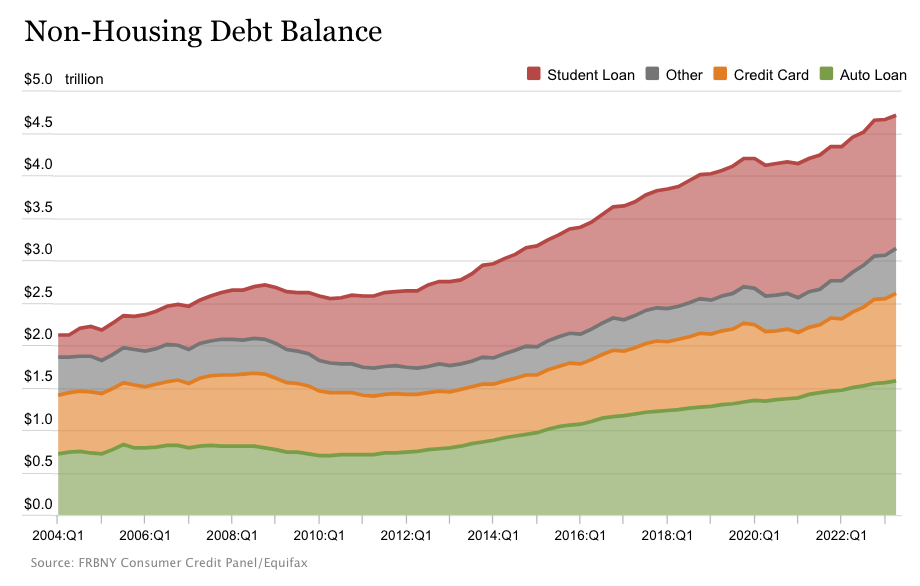

The resumption of student loan payments in October 2023 is no small thing. Consider the amount of total household non-mortgage debt outstanding in the U.S.:

Total non-housing debt balance (Federal Reserve Bank of New York / Equifax)

{kind=link}

Of the roughly $4.75 trillion of outstanding non-housing debt, $1.57 trillion is comprised of student loans--payments on which have not been made for some time. The Education Data Initiative estimates that the average monthly student loan payment is $503, which represents a significant monthly obligation for households, and poses a not-insignificant threat to disposable income.

Combine this with credit card debts surpassing $1 trillion for the first time along with delinquency rates ticking up , and it's not difficult to conclude that the free-spending of the post-Covid era may be coming to a close.

This is not good news for retailers in general, and for retailers which sell highly discretionary items (such as outdoors and athletic equipment) it is especially tough news.

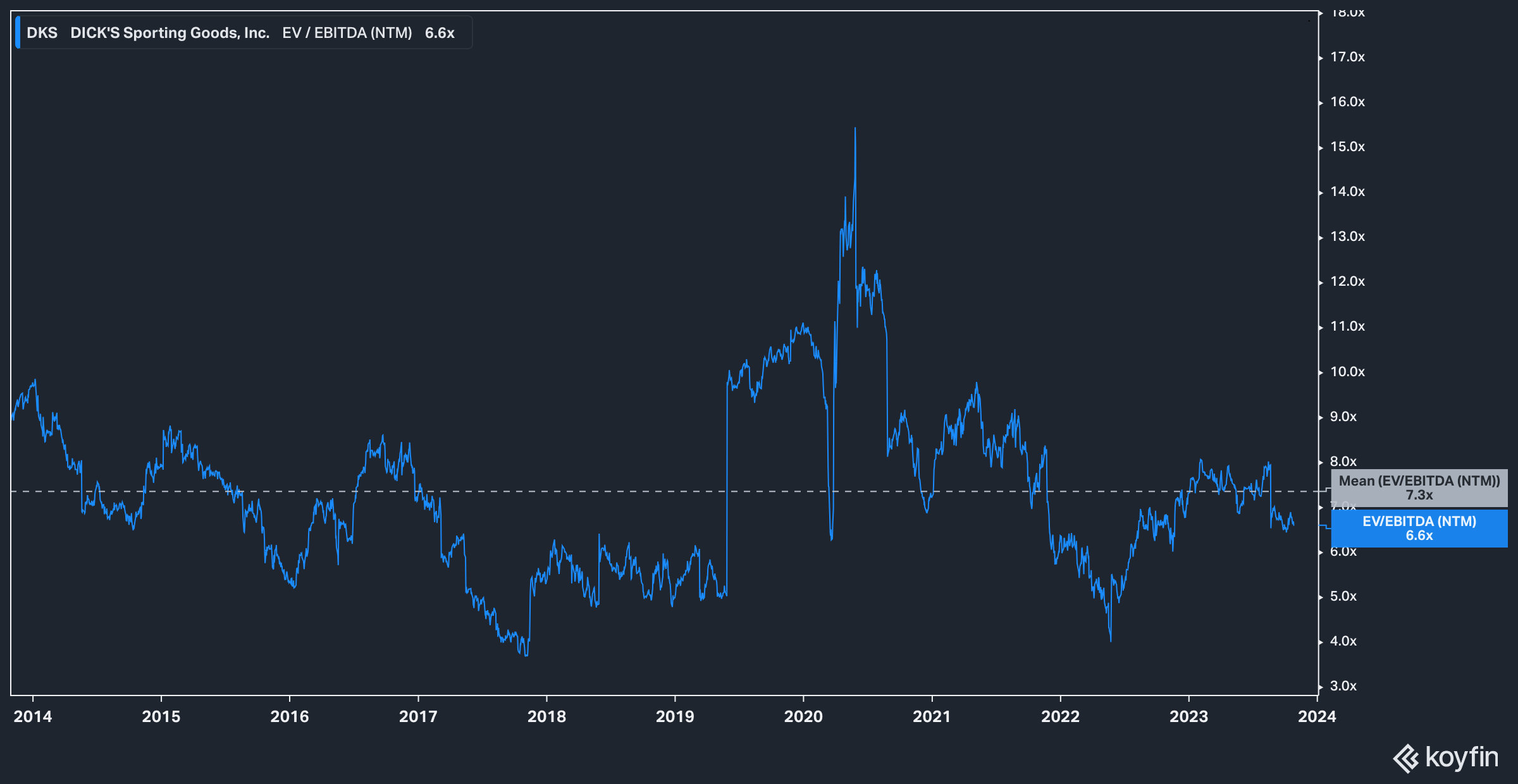

Valuation

Adding to our concerns is the fact that DICK'S isn't exactly a bargain based on historical valuation metrics.

{kind=link}

On a forward basis, DICK'S EV/EBITDA currently sits at 6.6x, only slightly below the stock's 10-year average of 7.3x. It's forward P/E of 8.8x is largely in line with historic norms as well (though the 10-year average is pulled up by the COVID-induced P/E spike in 2020).

The Bottom Line

There is no doubt that DICK'S is a quality operator, and that management has certainly made the most of what could be made in the post-COVID era when consumers, itching to get out of the house, spent big on discretionary goods. We believe, however, that incoming pressures on the consumer, a lack of pricing power, and the trend of direct-to-consumer selling pose a threat to the retail giant. While we don't see disaster in the company's future, we certainly see tougher times ahead than what it has known for the last three years.

Risks to our thesis include any legislation which further suspends student loan payments, as well as the continued resilience of the American consumer.

For further details see:

Is The Party Over At DICK'S?