ITRN - Ituran Location and Control: A Hidden Gem That Keeps Performing

2023-08-17 12:02:22 ET

Summary

- Ituran Location and Control achieved record-breaking subscription fees and strong financial performance in Q2 FY2023.

- Ituran's strategic partnerships and expansion into new markets position it for further growth in the future.

- At the same time, the stock is undervalued by ~34% according to my calculations.

The Company

Ituran Location and Control (ITRN) is an Israeli-based $560-million market cap company that provides location-based telematics services and products. They offer stolen vehicle recovery, fleet management, navigation, and tracking services. Their Telematics Products include devices for collecting and transmitting data from vehicles. The company serves insurance firms, car manufacturers, and individual subscribers.

On August 15, 2023, the firm released its quarterly report for Q2 FY2023 , and I think this is exactly where we should dive in.

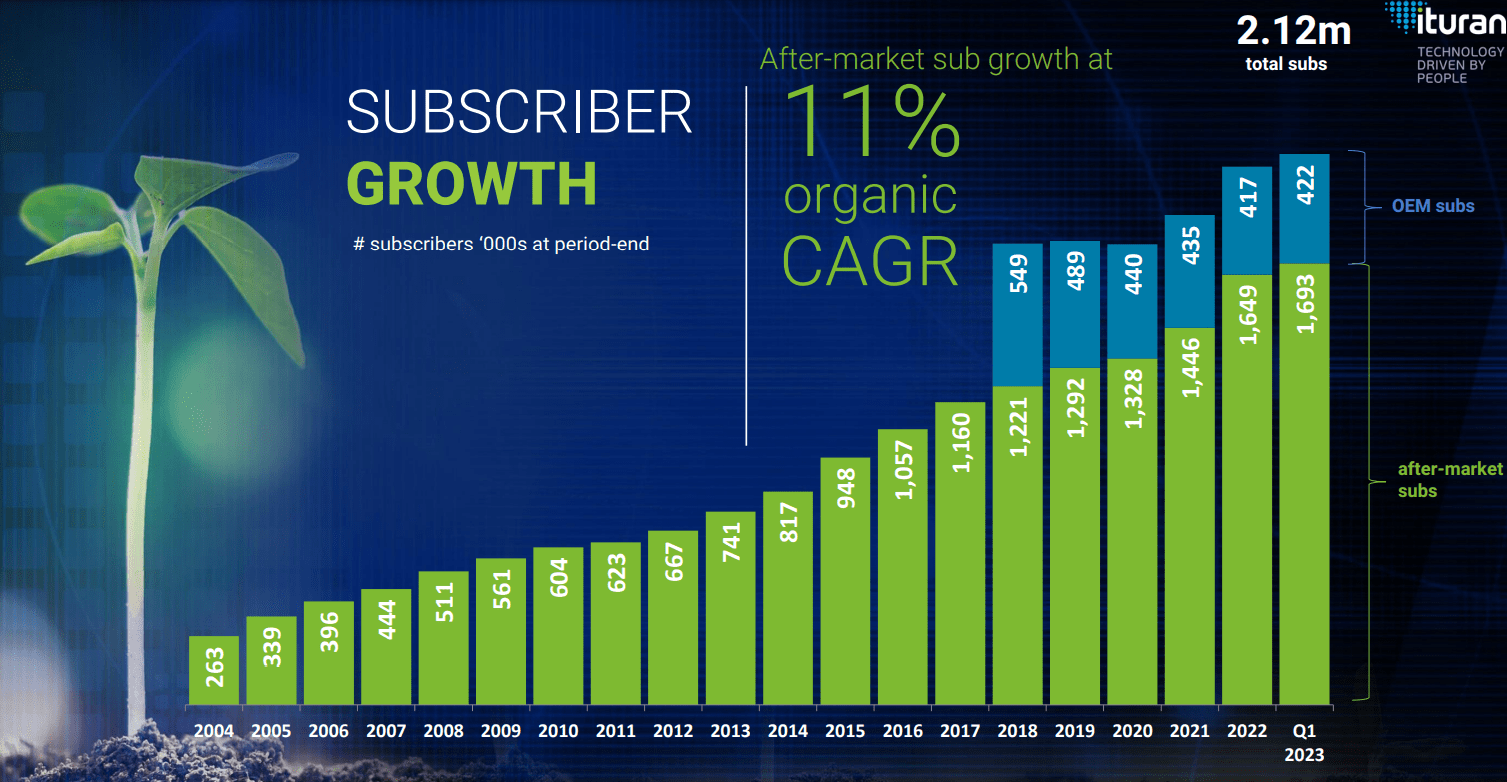

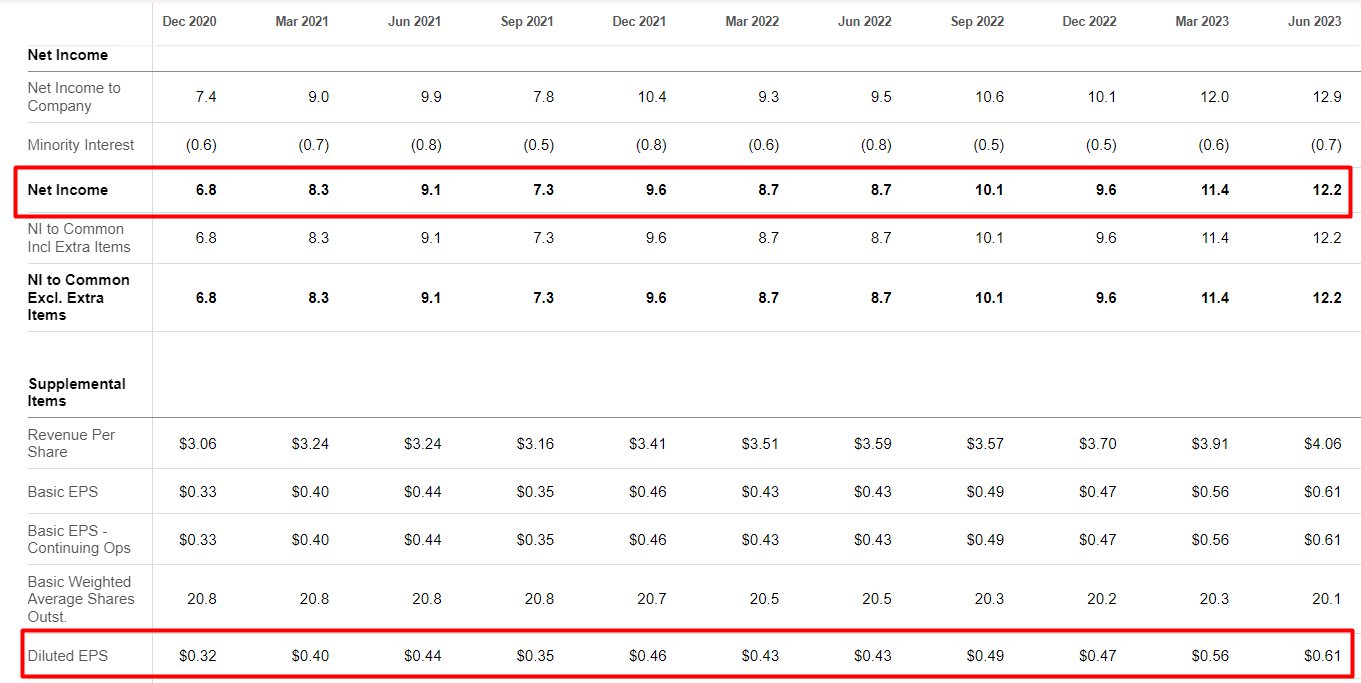

Record-breaking subscription fees and 4-year highs in net income and EBITDA have reinforced Ituran's success story in Q2 FY2023. The company's sturdy foundation, built on a solid subscriber base exceeding 2 million, bodes well for sustaining the current positive trends well into FY2023, with a positive outlook for the years ahead, the CEO Eyal Sheratzky noted during the recent earnings call .

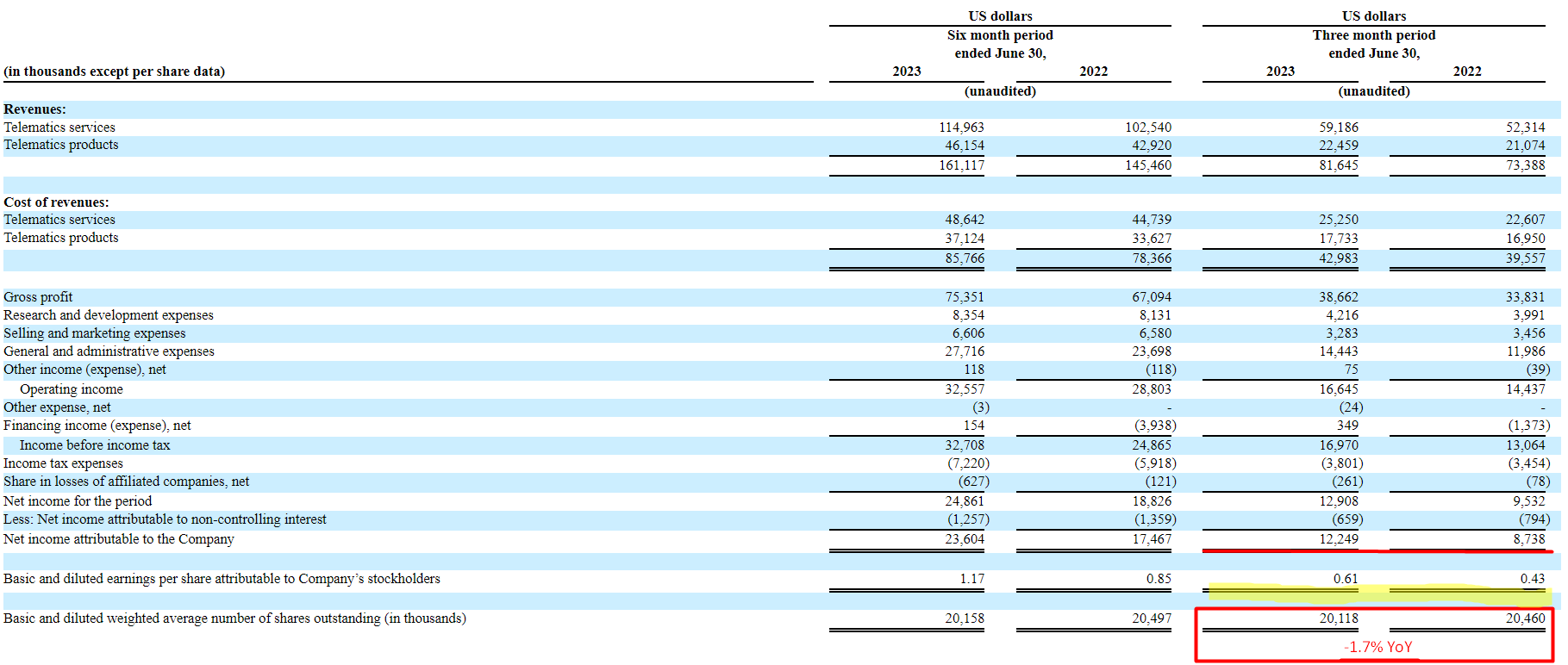

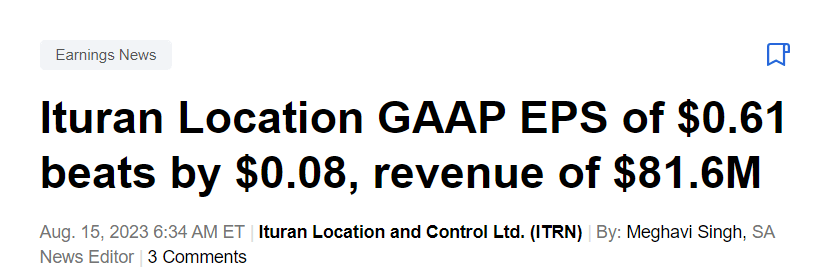

ITRN achieved strong subscriber growth, adding 47,000 new subscribers, with 45,000 from the aftermarket and 2,000 from OEM. This growth is reflected in record subscription revenue, even amidst currency challenges arising from the dollar's strength YTD in 2023. As a result, ITRN's total revenues reached $81.6 million, a notable 11% YoY increase. The subscription fee revenue hit a record $59.2 million, marking a 13% rise from Q2 2022.

Gross profit reached $38.7 million, reflecting a 14% YoY increase, and operating income and EBITDA grew by 15% and 12%, respectively [also YoY]. Net income demonstrated a substantial 40% increase, totaling $12.2 million, and cash flow from operations stood at $17.5 million (+71.3% YoY). So the FCF (calculated as CFO minus CAPEX) amounted to $14.1 million, that's ~2.5% of the market cap for Q2 alone .

The company's share buy-back program, initiated in 2019 with a total of $25 million, continued with an additional allocation of $10 million announced on February 23, 2023. As of June 30, 2023, there remains $8.6 million available for buy-backs. During the quarter, Ituran repurchased 156,138 shares for a total of $3.5 million as part of the program.

{kind=link}

Thanks to a combination of active buybacks and good organic growth, ITRN significantly exceeded analysts' forecasts for this quarter:

{kind=link}

A significant event in Q2 was Ituran's Brazilian subsidiary forming a strategic partnership with Santander Bank, aimed at simplifying credit approval for automatic financing to expand the Brazilian car ownership market and grow Ituran's subscriber base.

The management also noted that economic trends in Israel and Latin America are driving demand for Ituran's services, bolstering growth even amid a potential economic slowdown. ITRN introduced a stolen vehicle recovery product for Latin America's motorcycle market, attracting interest from manufacturers and insurers.

I see a fairly favorable environment for growth in the company's addressable markets. The market for stolen vehicle tracking software should grow at a CAGR of 7.9% over the next few years, driven by increasing demand for vehicle security. And the GPS market's size is expected to grow at a CAGR of 11.56% through FY2030, according to external research. Looking at customer growth, according to the IR presentation for Q1 FY2023 , the company is able to effectively tap into these markets:

{kind=link}

I like that the firm aims to use generated cash for growth, including acquisitions, new partnerships, and expansions into new segments, while also rewarding shareholders through dividends [2.15% FWD yield] and buybacks.

The Valuation

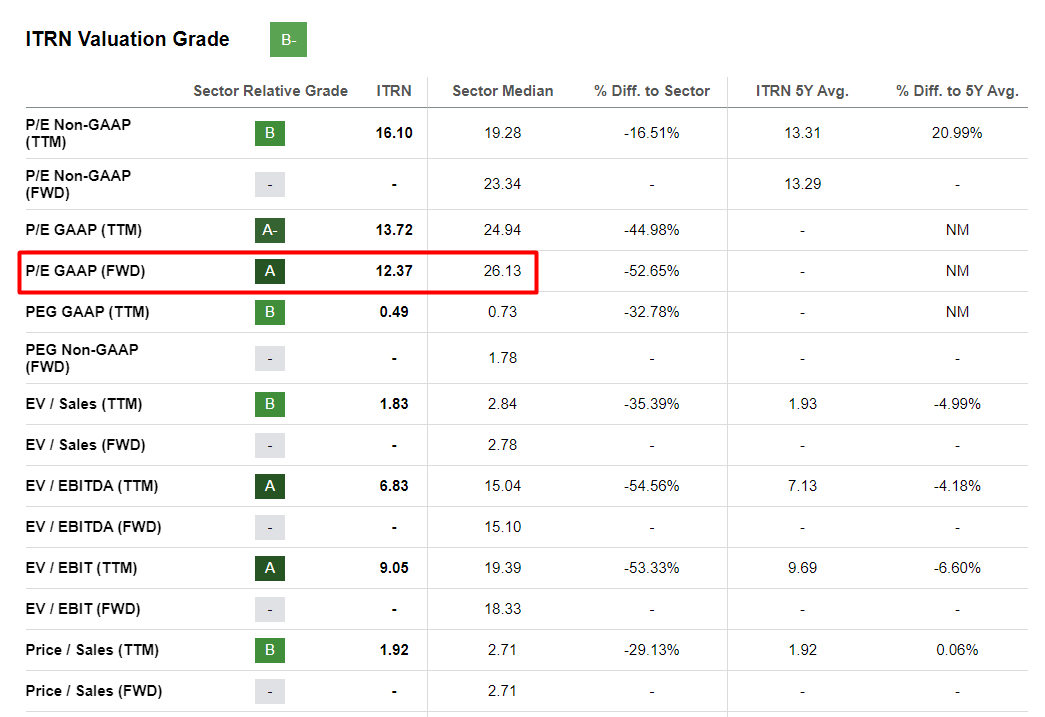

According to Seeking Alpha, whose Quant System ranks ITRN as a "B-" stock in terms of its valuation multiples, the company trades at only 12.3 times its forward earnings:

{kind=link}

Remember: The company grew its net income by almost 36% year-over-year in Q2 FY2023, while this bottom-line growth has been consistent and I don't see any pronounced cyclical patterns that might indicate instability in current growth .

{kind=link}

At the same time, the company is so invisible to the market that only 3 analysts attended the earnings call: Chris Reimer from Barclays, Abba Horwitz from Old School Partners, and Fred Foulkes from Boston University. In other words, apart from Barclays, no other representatives of major investment banks were present. Moreover, based on EPS consensus forecasts which are calculated from calculations by only one analyst (presumably Chris Reimer), the company is expected to grow its EPS by only 9.04% next year while judging by the management's commentary, the growth outlook is much more colorful today than it used to be. At least, that's the impression I got.

But even if Ituran increases its EPS by only 9%, the implied price-to-earnings ratio is only 11.3x, which I think is very modest.

In terms of operational growth, ITRN is far from past its worst days, as can be seen from its historical perspective. In terms of future plans and initiatives, the playing field also looks interesting and promising. At the same time, the valuation of the company looks quite depressing.

The Bottom Line

Of course, Ituran is not a risk-free idea, especially considering that the company has $500 million in market cap. There have been times in the past when EPS behaved unpredictably, and we have no guarantee that this won't happen again, no matter how actively the company buys back its shares from the market. Also, note that the undervaluation I noted above may be due to something I didn't understand during the analysis. Every investor needs to do their own due diligence before getting into this investment.

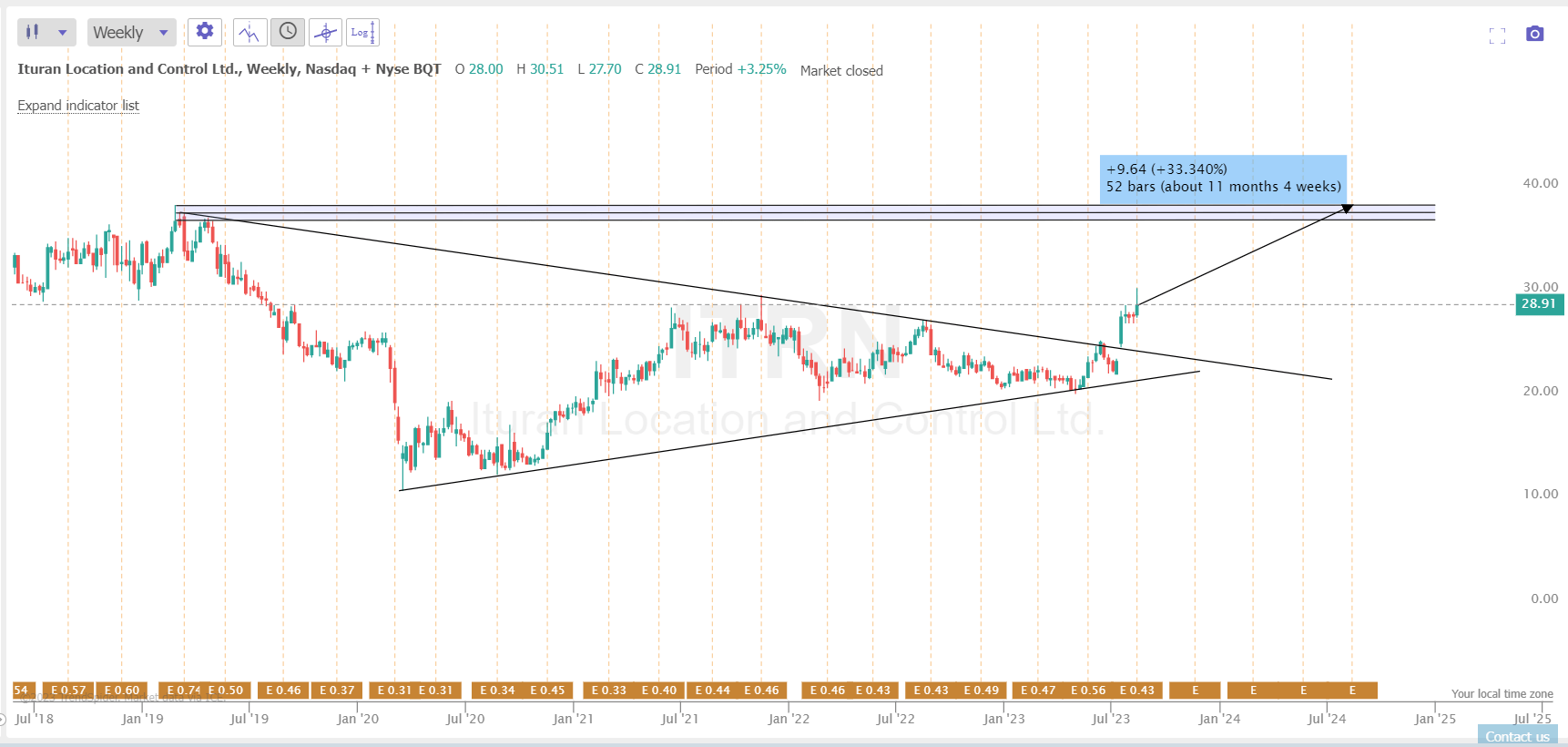

But despite all the risks, I think ITRN is a great business worthy of being rated a "Buy". Unless the current situation deteriorates further in the near future, I expect the current TTM price-to-earnings ratio of 15x to hold through FY 2024. Even with projected earnings per share growth, which the company can easily beat again (as we saw in Q2), ITRN then becomes a $38.7 stock, giving buyers an upside potential of about 34% .

The movement potential I calculated corresponds to reaching the all-time high so far:

{kind=link}

I'm not a technical analyst, but you have to agree: It's always nice to see a nice rising price chart like the one above. Past price performance says nothing about the future, but it's clear to me personally that ITRN is becoming more and more noticeable for institutional investors looking for quality small-cap companies here and there. So I hope the current rally continues.

Thank you for reading!

For further details see:

Ituran Location and Control: A Hidden Gem That Keeps Performing